Download as pptx, pdf, or txt

You might also like

- Lloyds Bank StatementDocument2 pagesLloyds Bank StatementZheng Yang100% (1)

- Journal To Final AccountsDocument38 pagesJournal To Final Accountsguptagaurav131166100% (5)

- TurnKey Investor's Subject-To Mortgage Handbook (Table of Contents, Intro, Chapter 1)Document31 pagesTurnKey Investor's Subject-To Mortgage Handbook (Table of Contents, Intro, Chapter 1)Matthew S. Chan100% (1)

- Double Entry SystemDocument17 pagesDouble Entry SystemDastaan Ali100% (1)

- Unit 1 Introduction Journal Ledger and Trial BalanceDocument51 pagesUnit 1 Introduction Journal Ledger and Trial Balancedivimba87100% (1)

- Tally NotesDocument32 pagesTally NotesenuNo ratings yet

- Accounting SystemDocument5 pagesAccounting SystemJayanta SinghaNo ratings yet

- Accounting and Finance Unit 2Document191 pagesAccounting and Finance Unit 2vasudha100% (1)

- Tally-1Document61 pagesTally-1vidya gubbala50% (2)

- Module 2 - The Use of Double-Entry and Accounting SystemsDocument22 pagesModule 2 - The Use of Double-Entry and Accounting SystemsJewel Philip50% (2)

- The Basis of All Accounting Is Concerned With The Ascertaining and Analyzing of Business ResultsDocument42 pagesThe Basis of All Accounting Is Concerned With The Ascertaining and Analyzing of Business ResultsAswin S PanickerNo ratings yet

- 110-Chapter 3 - Books of Original Entry-Journal - WMDocument21 pages110-Chapter 3 - Books of Original Entry-Journal - WMaaditya kumar jhaNo ratings yet

- 3 Golden Rules of Accounting - YinduDocument15 pages3 Golden Rules of Accounting - YinduWo DeNo ratings yet

- Tally NotesDocument32 pagesTally NotesArun81% (16)

- Notes of Double Entry System and Journal EntryDocument35 pagesNotes of Double Entry System and Journal Entryjune100% (1)

- Journal Ledger & Trial BalanceDocument11 pagesJournal Ledger & Trial BalanceTushar SahuNo ratings yet

- Tally Prime Book by Hardik PanchalDocument55 pagesTally Prime Book by Hardik PanchalHardik PanchalNo ratings yet

- RulesDocument10 pagesRuleskainat zahid100% (1)

- Management Accounting - 3Document12 pagesManagement Accounting - 3Aditya KulkarniNo ratings yet

- Class 11 Accountancy Chapter-3 Revision NotesDocument11 pagesClass 11 Accountancy Chapter-3 Revision NotesMohd. Khushmeen KhanNo ratings yet

- Accounting CyclesDocument23 pagesAccounting CyclesrajasekarNo ratings yet

- Golden Rules of AccountingDocument5 pagesGolden Rules of AccountingVinay ChintamaneniNo ratings yet

- What Are The Golden Rules For AccountingDocument28 pagesWhat Are The Golden Rules For AccountingWong KianTatNo ratings yet

- Basics of Accounting: Chanakya Introduced The Accounting Concepts in His Book Arthashastra. in His Book, HeDocument15 pagesBasics of Accounting: Chanakya Introduced The Accounting Concepts in His Book Arthashastra. in His Book, HeShams100% (1)

- Account 1Document30 pagesAccount 1sant100% (1)

- Debit and Credit Rules of AccountingDocument6 pagesDebit and Credit Rules of AccountingsbcluincNo ratings yet

- Chapter 4-JournalDocument35 pagesChapter 4-JournalVivek Garg100% (1)

- Chapter3+4UsingT-Accounts 2Document37 pagesChapter3+4UsingT-Accounts 2الغيثيNo ratings yet

- Chapter 7 - Journal (Part 1)Document30 pagesChapter 7 - Journal (Part 1)ANNA AGARWAL100% (1)

- Session 5Document28 pagesSession 5Sarvesh ChandraNo ratings yet

- Session 5-6: Accounting Records: Instructor Dr. Jagan Kumar SurDocument48 pagesSession 5-6: Accounting Records: Instructor Dr. Jagan Kumar SurBabusona SahaNo ratings yet

- Professional Accounting PackageDocument72 pagesProfessional Accounting PackageAnmol poudelNo ratings yet

- Solution To ACCountancy - 11 NcertDocument7 pagesSolution To ACCountancy - 11 NcertsamidhamathurNo ratings yet

- 3 Accounting MechanicsDocument50 pages3 Accounting MechanicsVasu Narang100% (1)

- Personal, Real and Nominal AccountsDocument5 pagesPersonal, Real and Nominal AccountsRaghav GroverNo ratings yet

- Accounting BasicsDocument21 pagesAccounting BasicsasifparwezNo ratings yet

- Double Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaDocument34 pagesDouble Entry System & Accounting Equation: by - Mrs. Dilshad D. JalnawallaTufail GanaieNo ratings yet

- Accounting For Managers - Unit 2Document161 pagesAccounting For Managers - Unit 2Chirag JainNo ratings yet

- Accounts FinalDocument10 pagesAccounts FinalNeha PNo ratings yet

- Rules of Journalising: Personal Accounts Impersonal AcoountsDocument4 pagesRules of Journalising: Personal Accounts Impersonal AcoountsRachit DixitNo ratings yet

- Topic Thirteen Book KeepingDocument8 pagesTopic Thirteen Book KeepingSalym SadickNo ratings yet

- Accounting and Financial StatementDocument5 pagesAccounting and Financial StatementGordon SmithNo ratings yet

- Accounting ProcessDocument45 pagesAccounting ProcessRAVI DWIVEDINo ratings yet

- Journal PostingDocument22 pagesJournal PostingPoonam JadhavNo ratings yet

- Journal EntriesDocument7 pagesJournal Entriesmanthansaini8923No ratings yet

- Adeup CoDocument5 pagesAdeup CoPavan RaiNo ratings yet

- MEFA - 4th UnitDocument24 pagesMEFA - 4th UnitP.V.S. VEERANJANEYULUNo ratings yet

- Basic of Accounts Tally Is A Package: AccountingDocument9 pagesBasic of Accounts Tally Is A Package: AccountingArista TechnologiesNo ratings yet

- What Is Accounting???Document15 pagesWhat Is Accounting???Modassar NazarNo ratings yet

- Basic Guidance To AccountingDocument5 pagesBasic Guidance To AccountingAishwarya ShelarNo ratings yet

- Classification of AccountingDocument11 pagesClassification of AccountingManish DebNo ratings yet

- Convention of Conservatism: Debiting and CreditingDocument57 pagesConvention of Conservatism: Debiting and CreditingvasusantNo ratings yet

- Journal: Double Entry System of AccountingDocument17 pagesJournal: Double Entry System of AccountingBole ShubhamNo ratings yet

- 5 Basic AccountingDocument31 pages5 Basic Accounting2205611No ratings yet

- CHP 1 and 2 BbaDocument73 pagesCHP 1 and 2 BbaBarkkha MakhijaNo ratings yet

- General JournalDocument19 pagesGeneral JournalZainab AsifNo ratings yet

- Accounts Notes 1Document7 pagesAccounts Notes 1Dynmc ThugzNo ratings yet

- Chapter 2Document2 pagesChapter 2theskepticaloneNo ratings yet

- Finance Assi FinalDocument8 pagesFinance Assi FinalVagdevi YadavNo ratings yet

- Classification of AccountsDocument15 pagesClassification of AccountsBrian Reyes GangcaNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- Rushikesh Dudhat: Virtual WaterDocument3 pagesRushikesh Dudhat: Virtual WaterAkanksha GuptaNo ratings yet

- Rushikesh Dudhat: Seed BombDocument1 pageRushikesh Dudhat: Seed BombAkanksha GuptaNo ratings yet

- Rushikesh Dudhat: WheatDocument1 pageRushikesh Dudhat: WheatAkanksha GuptaNo ratings yet

- Rushikesh Dudhat: Krishna Raja Sagar (KRS) DamDocument1 pageRushikesh Dudhat: Krishna Raja Sagar (KRS) DamAkanksha GuptaNo ratings yet

- Rushikesh Dudhat: Ranthambore Tiger ReserveDocument1 pageRushikesh Dudhat: Ranthambore Tiger ReserveAkanksha GuptaNo ratings yet

- Rushikesh Dudhat: Rare Orchids in IndiaDocument2 pagesRushikesh Dudhat: Rare Orchids in IndiaAkanksha GuptaNo ratings yet

- Situation Reaction Test: Follow Us On Telegram SSB FUTURE OFFICERS @ssbgeneraldiscussionDocument4 pagesSituation Reaction Test: Follow Us On Telegram SSB FUTURE OFFICERS @ssbgeneraldiscussionAkanksha GuptaNo ratings yet

- Personal Loan Application Form: Applicant DetailDocument8 pagesPersonal Loan Application Form: Applicant DetailAkanksha GuptaNo ratings yet

- Cost Accounting PPT FinalDocument47 pagesCost Accounting PPT FinalAkanksha GuptaNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument31 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceTyrion LannisterNo ratings yet

- Fundamentals of Accountancy, Business, and Management 2: Prepared By: Mark Vincent B. Bantog, LPTDocument15 pagesFundamentals of Accountancy, Business, and Management 2: Prepared By: Mark Vincent B. Bantog, LPTSherlock HolmesNo ratings yet

- CD MaterialityDocument11 pagesCD MaterialityAMNA T.ZNo ratings yet

- Current LiabilitiesDocument94 pagesCurrent LiabilitiesDawit TilahunNo ratings yet

- Impact of Demonetization On Microfinance SectorDocument4 pagesImpact of Demonetization On Microfinance SectorGibin KollamparambilNo ratings yet

- AC - BUTU MUHAMMAD MALLAM - FEBRUARY, 2021 - 671968358 - FullStmtDocument6 pagesAC - BUTU MUHAMMAD MALLAM - FEBRUARY, 2021 - 671968358 - FullStmtmuhammad m butuNo ratings yet

- Ibps Po MainsDocument169 pagesIbps Po MainsSaurabh AnandNo ratings yet

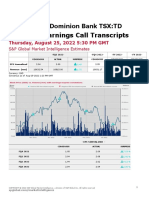

- The Toronto-Dominion Bank, Q3 2022 Earnings Call, Aug 25, 2022Document23 pagesThe Toronto-Dominion Bank, Q3 2022 Earnings Call, Aug 25, 2022Neel DoshiNo ratings yet

- Salient Features of Insurance LawDocument7 pagesSalient Features of Insurance Lawnusratopee100% (1)

- Indgiro 20181231 PDFDocument1 pageIndgiro 20181231 PDFHuiwen Cheok100% (1)

- LIC's Jeevan Lakshya (T-933) : Benefit IllustrationDocument3 pagesLIC's Jeevan Lakshya (T-933) : Benefit IllustrationrajuNo ratings yet

- Corporate Identity Number: U99999DL1993PLC054135: Registered Office: 12 Central Service Office: 2Document6 pagesCorporate Identity Number: U99999DL1993PLC054135: Registered Office: 12 Central Service Office: 2shakya jagaran manchNo ratings yet

- Open Account : A Mode of Payment in International TradeDocument10 pagesOpen Account : A Mode of Payment in International TradeAkash das100% (1)

- Yes Bank ScamDocument3 pagesYes Bank ScamKartikey Gupta100% (1)

- Express Check Out (Gurminder Preet Singh)Document2 pagesExpress Check Out (Gurminder Preet Singh)vickie_sunnieNo ratings yet

- 3 The Accounting EquationDocument35 pages3 The Accounting EquationAndruey EspirituNo ratings yet

- Chapter - Management of Money and Banking SystemDocument6 pagesChapter - Management of Money and Banking SystemNahidul Islam IUNo ratings yet

- Time Value of MoneyDocument76 pagesTime Value of Moneyrhea agnesNo ratings yet

- BBAW2103 Financial AccountingDocument336 pagesBBAW2103 Financial AccountingJohn JamesNo ratings yet

- New Era University: "Banking Industry"Document34 pagesNew Era University: "Banking Industry"Rain LpzNo ratings yet

- HDFC SL CrestDocument1 pageHDFC SL Crestk_kishan288No ratings yet

- Module 8 Business MathematicsDocument26 pagesModule 8 Business MathematicsMaam AprilNo ratings yet

- Honnur HSKDocument57 pagesHonnur HSKzeba kousarNo ratings yet

- Current Affairs CapsuleDocument76 pagesCurrent Affairs CapsuleRaviraj GhadiNo ratings yet

- Bin RulesDocument11 pagesBin RulesEduardo TolentinoNo ratings yet

- FABM 2 Lesson 1Document38 pagesFABM 2 Lesson 1Trisha ElecerioNo ratings yet

- Lecture Notes: National University Ellery de Leon Advac 1-Partnerships 1 Semester SY 2016-2017Document10 pagesLecture Notes: National University Ellery de Leon Advac 1-Partnerships 1 Semester SY 2016-2017sunflowerNo ratings yet

- Unit 4: Relative ValuationDocument47 pagesUnit 4: Relative ValuationMadhvendra BhardwajNo ratings yet