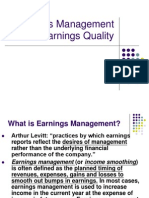

Earnings Management and Earnings Quality (2010)

Earnings Management and Earnings Quality (2010)

You might also like

- Worldcom Case AnalysisDocument6 pagesWorldcom Case AnalysisNithya NairNo ratings yet

- Creative AccountingDocument7 pagesCreative Accountingeugeniastefania raduNo ratings yet

- Next 4Document10 pagesNext 4Nurhasanah Asyari100% (1)

- ACCO 400 Weeks 5 and 6 Discussion Questions and AnswersDocument4 pagesACCO 400 Weeks 5 and 6 Discussion Questions and AnswersWasif SethNo ratings yet

- Mauboussin - What You See and What You Get PDFDocument39 pagesMauboussin - What You See and What You Get PDFRob72081No ratings yet

- Reference Book On Staff MattersDocument910 pagesReference Book On Staff Matterssiddharthdatta89% (9)

- Earnings Management and Earnings QualityDocument23 pagesEarnings Management and Earnings QualityZa HanfiNo ratings yet

- Bacc 402 Financial Stat 1Document9 pagesBacc 402 Financial Stat 1ItdarareNo ratings yet

- Financial Shenanigans What Are Financial Shenanigans?Document9 pagesFinancial Shenanigans What Are Financial Shenanigans?Qorry NittyNo ratings yet

- Financial ShenanigansDocument13 pagesFinancial ShenanigansCLEO COLEEN FORTUNADONo ratings yet

- Creative Accounting: Goa Institute of ManagementDocument7 pagesCreative Accounting: Goa Institute of Managementnishan01234No ratings yet

- Waste Mngt. ScandalDocument3 pagesWaste Mngt. ScandalVilma HoseñaNo ratings yet

- PFA 3e 2021 SM CH 01 - Accounting in BusinessDocument57 pagesPFA 3e 2021 SM CH 01 - Accounting in Businesscalista sNo ratings yet

- Practices.) : Depreciation Charge Per Year. James E. Koenig, The Chief Financial Officer (CFO) Applied TheDocument2 pagesPractices.) : Depreciation Charge Per Year. James E. Koenig, The Chief Financial Officer (CFO) Applied TheRhoville HoseñaNo ratings yet

- Case Study WorldCom Accounting ScandalDocument6 pagesCase Study WorldCom Accounting ScandalSer JeromeNo ratings yet

- Creative AccountingDocument5 pagesCreative Accountingvikas_nair_2No ratings yet

- FINANCIAL SHENANIGANS Kel 3Document17 pagesFINANCIAL SHENANIGANS Kel 3Qorry NittyNo ratings yet

- Types of Earnings Management and Manipulation Examples of Earnings ManipulationDocument6 pagesTypes of Earnings Management and Manipulation Examples of Earnings Manipulationkhurram riazNo ratings yet

- Creative AccountingDocument2 pagesCreative AccountingElton LopesNo ratings yet

- Worldcom ScandalDocument5 pagesWorldcom ScandalThea Marie GuiljonNo ratings yet

- Creative Accounting-Meaning, Scope and Case StudyDocument5 pagesCreative Accounting-Meaning, Scope and Case Studysahanvit100% (1)

- Group Project Far 661Document19 pagesGroup Project Far 661azri2701No ratings yet

- ???????? ???? ?????Document7 pages???????? ???? ?????Gabriely MligulaNo ratings yet

- Financial Information For Business DecisionDocument9 pagesFinancial Information For Business DecisionMohamed FAVAZIL pulloorsangattilNo ratings yet

- Abdelghany (2005) PDFDocument15 pagesAbdelghany (2005) PDFBowo BoombaystiexNo ratings yet

- Introduction To Financial Statements: Wirecard ScandalDocument22 pagesIntroduction To Financial Statements: Wirecard ScandalNilesh Kumar GuptaNo ratings yet

- Financial Accounting Management: Report On Creative AccountingDocument5 pagesFinancial Accounting Management: Report On Creative Accountinganiket_dNo ratings yet

- Creative AccountingDocument7 pagesCreative Accountingeugeniastefania raduNo ratings yet

- Introduce To Management AccountingDocument9 pagesIntroduce To Management AccountingSagung AdvaitaNo ratings yet

- Ethics of Accounting Information 1. Creative Accounting and Earnings ManagementDocument9 pagesEthics of Accounting Information 1. Creative Accounting and Earnings Managementumarawat_omNo ratings yet

- 2 Managerial Accounting and The Budgeting ProcessDocument9 pages2 Managerial Accounting and The Budgeting ProcessAshraf Galal100% (1)

- Discussion Question W9 Creative AccountingDocument5 pagesDiscussion Question W9 Creative AccountingElaine LimNo ratings yet

- CASE STUDY - WHAT WENT WRONG-WorldComDocument3 pagesCASE STUDY - WHAT WENT WRONG-WorldComMark Jaypee SantiagoNo ratings yet

- International ProjectDocument26 pagesInternational ProjectZiad MohammedNo ratings yet

- cREATIVE ACCOUNTINGDocument12 pagescREATIVE ACCOUNTINGAshraful Jaygirdar0% (1)

- Defn CreativeDocument11 pagesDefn CreativeDamulira DavidNo ratings yet

- Planning and Working Capital ManagementDocument4 pagesPlanning and Working Capital ManagementSheena Mari Uy ElleveraNo ratings yet

- Solution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 4th EditionDocument30 pagesSolution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 4th Editiongabrielthuym96j100% (19)

- Exemplu Big BathDocument16 pagesExemplu Big BathValentin BurcaNo ratings yet

- Chapter 2Document67 pagesChapter 2Adam MilakaraNo ratings yet

- Where Financial Report Still Falls ShortDocument2 pagesWhere Financial Report Still Falls ShortJoel Swapnil SinghNo ratings yet

- 2014 3a. Explain Why Operating Leverage Decreases As A Company Increases Sales and Shifts Away From The Break-Even PointDocument10 pages2014 3a. Explain Why Operating Leverage Decreases As A Company Increases Sales and Shifts Away From The Break-Even PointHiew fuxiangNo ratings yet

- Analyzing Tyco: Aggressive or Out of Line?: Rahmat Faizal & Sensony DPDocument10 pagesAnalyzing Tyco: Aggressive or Out of Line?: Rahmat Faizal & Sensony DPLheegar TanNo ratings yet

- BA 297 Final Exam The Bankruptcy of Lehman BrothersDocument3 pagesBA 297 Final Exam The Bankruptcy of Lehman BrothersChristian Paul BonguezNo ratings yet

- Financial Statement FraudDocument19 pagesFinancial Statement FraudAulia HidayatNo ratings yet

- The Effect of Creative Accounting On The Job Performance of Accountants Auditors in Reporting Financial Statementin Nigeria 2224 8358-1-173Document30 pagesThe Effect of Creative Accounting On The Job Performance of Accountants Auditors in Reporting Financial Statementin Nigeria 2224 8358-1-173Harshini RamasNo ratings yet

- Module 1 Financial Accounting For MBAs - 6th EditionDocument15 pagesModule 1 Financial Accounting For MBAs - 6th EditionjoshNo ratings yet

- Patterns of Earnings ManagementDocument6 pagesPatterns of Earnings ManagementAnis SofiaNo ratings yet

- Creative AccountingDocument13 pagesCreative AccountingMira CE100% (1)

- Accounting Theory Mid-Exam: By: Rusmian Nuzulul P. / 0910233137Document6 pagesAccounting Theory Mid-Exam: By: Rusmian Nuzulul P. / 0910233137Rusmian Nuzulul PujakaneoNo ratings yet

- Ways of Manipulating Accounting StatementsDocument5 pagesWays of Manipulating Accounting StatementsSabyasachi ChowdhuryNo ratings yet

- FR & FasDocument195 pagesFR & FasPrerana SharmaNo ratings yet

- AFM NotesDocument110 pagesAFM NotesNguyen NhanNo ratings yet

- ACC 111 Assessment 2 - Project: Adam MuhammadDocument7 pagesACC 111 Assessment 2 - Project: Adam Muhammadmuhammad raqibNo ratings yet

- Creative Accounting: Case Study:WorldcomDocument11 pagesCreative Accounting: Case Study:WorldcomVikash KumarNo ratings yet

- TUI UniversityDocument9 pagesTUI UniversityChris NailonNo ratings yet

- Fin STM Fraud 2Document6 pagesFin STM Fraud 2Okwuchi AlaukwuNo ratings yet

- Computer AssociatesDocument18 pagesComputer AssociatesRosel RicafortNo ratings yet

- Summary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionFrom EverandSummary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionNo ratings yet

- Balance Sheet Management: Squeezing Extra Profits and Cash from Your BusinessFrom EverandBalance Sheet Management: Squeezing Extra Profits and Cash from Your BusinessNo ratings yet

- Tut 6-IpmDocument3 pagesTut 6-IpmNguyễn Phương ThảoNo ratings yet

- Reduce Reuse RecycleDocument14 pagesReduce Reuse RecycleBombe ZombeNo ratings yet

- Final Behavioral Finance White PaperDocument8 pagesFinal Behavioral Finance White PapernroposNo ratings yet

- Go Negosyo ActDocument26 pagesGo Negosyo ActEngiemar Barbasa TupasNo ratings yet

- Seminar 14 Accounting For Underlying Financial AssetsDocument105 pagesSeminar 14 Accounting For Underlying Financial AssetsPoun GerrNo ratings yet

- ECO1Document5 pagesECO1Precious Mae Sales100% (1)

- Standard Oil Company of New York v. Juan Posadas, JR., 55 Phil. 715Document2 pagesStandard Oil Company of New York v. Juan Posadas, JR., 55 Phil. 715Icel LacanilaoNo ratings yet

- Business Studies Project: Class 12 Marketing Management (Jeans)Document25 pagesBusiness Studies Project: Class 12 Marketing Management (Jeans)Shivam SharmaNo ratings yet

- Applied Auditing Review Course Pre-Board - Answer KeyDocument13 pagesApplied Auditing Review Course Pre-Board - Answer KeyROMAR A. PIGANo ratings yet

- Baldwin Bicycle Case MBA Case StudyDocument24 pagesBaldwin Bicycle Case MBA Case StudyRobin L. M. Cheung100% (9)

- India - Korea Relationship (Khan, Alveera)Document9 pagesIndia - Korea Relationship (Khan, Alveera)Alveera KhanNo ratings yet

- Pricing StrategiesDocument9 pagesPricing StrategiesRajaRam BommarajuNo ratings yet

- Managerial Accounting and CostDocument19 pagesManagerial Accounting and CostIqra MughalNo ratings yet

- Customer Relationship ManmagementDocument51 pagesCustomer Relationship ManmagementmuneerppNo ratings yet

- Rajeswari Barika - Insta Foam Insulation by Tata BlueScope Steel - CharterDocument3 pagesRajeswari Barika - Insta Foam Insulation by Tata BlueScope Steel - CharterDGN ProductionsNo ratings yet

- AXISCADES Engineering Technologies Completes Acquisition of AXISCADES Aerospace & Technologies Pvt. LTD (Company Update)Document3 pagesAXISCADES Engineering Technologies Completes Acquisition of AXISCADES Aerospace & Technologies Pvt. LTD (Company Update)Shyam SunderNo ratings yet

- Essex Crossing Affordable Housing Lottery (Site 2)Document1 pageEssex Crossing Affordable Housing Lottery (Site 2)The Lo-DownNo ratings yet

- Industrial Project On Reliance Life Insurance Company LimitedDocument116 pagesIndustrial Project On Reliance Life Insurance Company LimitedTimothy Brown100% (1)

- 4 Types of Capacity StrategyDocument7 pages4 Types of Capacity StrategySaga HayyuNo ratings yet

- Acai Chapter 17 QuestionnairesDocument5 pagesAcai Chapter 17 QuestionnairesKathleenCusipagNo ratings yet

- 2024 24 01 Technical Due Diligence Report On LongonjoDocument4 pages2024 24 01 Technical Due Diligence Report On Longonjoqoyise.zamaNo ratings yet

- Third Point Q3 2021 Investor Letter TPILDocument10 pagesThird Point Q3 2021 Investor Letter TPILZerohedge100% (2)

- VRIODocument1 pageVRIOrahul_mahajan100% (1)

- Low Cost Strategy 040405Document40 pagesLow Cost Strategy 040405Ranjan JosephNo ratings yet

- NDPL Case StudyDocument10 pagesNDPL Case StudyPrateek BhargavaNo ratings yet

- Usa BrasilDocument185 pagesUsa BrasilCésar NuñezNo ratings yet

- Merchant BankingDocument55 pagesMerchant Bankingsuhaspatel84No ratings yet

- Habitat International: Nesru H. Koroso, Monica Lengoiboni, Jaap A. ZevenbergenDocument15 pagesHabitat International: Nesru H. Koroso, Monica Lengoiboni, Jaap A. ZevenbergenSG GhoshNo ratings yet

- CME - Option Box Spreads As A Financing ToolDocument6 pagesCME - Option Box Spreads As A Financing ToolDavid TaylorNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Worldcom Case AnalysisDocument6 pagesWorldcom Case AnalysisNithya NairNo ratings yet

- Creative AccountingDocument7 pagesCreative Accountingeugeniastefania raduNo ratings yet

- Next 4Document10 pagesNext 4Nurhasanah Asyari100% (1)

- ACCO 400 Weeks 5 and 6 Discussion Questions and AnswersDocument4 pagesACCO 400 Weeks 5 and 6 Discussion Questions and AnswersWasif SethNo ratings yet

- Mauboussin - What You See and What You Get PDFDocument39 pagesMauboussin - What You See and What You Get PDFRob72081No ratings yet

- Reference Book On Staff MattersDocument910 pagesReference Book On Staff Matterssiddharthdatta89% (9)

- Earnings Management and Earnings QualityDocument23 pagesEarnings Management and Earnings QualityZa HanfiNo ratings yet

- Bacc 402 Financial Stat 1Document9 pagesBacc 402 Financial Stat 1ItdarareNo ratings yet

- Financial Shenanigans What Are Financial Shenanigans?Document9 pagesFinancial Shenanigans What Are Financial Shenanigans?Qorry NittyNo ratings yet

- Financial ShenanigansDocument13 pagesFinancial ShenanigansCLEO COLEEN FORTUNADONo ratings yet

- Creative Accounting: Goa Institute of ManagementDocument7 pagesCreative Accounting: Goa Institute of Managementnishan01234No ratings yet

- Waste Mngt. ScandalDocument3 pagesWaste Mngt. ScandalVilma HoseñaNo ratings yet

- PFA 3e 2021 SM CH 01 - Accounting in BusinessDocument57 pagesPFA 3e 2021 SM CH 01 - Accounting in Businesscalista sNo ratings yet

- Practices.) : Depreciation Charge Per Year. James E. Koenig, The Chief Financial Officer (CFO) Applied TheDocument2 pagesPractices.) : Depreciation Charge Per Year. James E. Koenig, The Chief Financial Officer (CFO) Applied TheRhoville HoseñaNo ratings yet

- Case Study WorldCom Accounting ScandalDocument6 pagesCase Study WorldCom Accounting ScandalSer JeromeNo ratings yet

- Creative AccountingDocument5 pagesCreative Accountingvikas_nair_2No ratings yet

- FINANCIAL SHENANIGANS Kel 3Document17 pagesFINANCIAL SHENANIGANS Kel 3Qorry NittyNo ratings yet

- Types of Earnings Management and Manipulation Examples of Earnings ManipulationDocument6 pagesTypes of Earnings Management and Manipulation Examples of Earnings Manipulationkhurram riazNo ratings yet

- Creative AccountingDocument2 pagesCreative AccountingElton LopesNo ratings yet

- Worldcom ScandalDocument5 pagesWorldcom ScandalThea Marie GuiljonNo ratings yet

- Creative Accounting-Meaning, Scope and Case StudyDocument5 pagesCreative Accounting-Meaning, Scope and Case Studysahanvit100% (1)

- Group Project Far 661Document19 pagesGroup Project Far 661azri2701No ratings yet

- ???????? ???? ?????Document7 pages???????? ???? ?????Gabriely MligulaNo ratings yet

- Financial Information For Business DecisionDocument9 pagesFinancial Information For Business DecisionMohamed FAVAZIL pulloorsangattilNo ratings yet

- Abdelghany (2005) PDFDocument15 pagesAbdelghany (2005) PDFBowo BoombaystiexNo ratings yet

- Introduction To Financial Statements: Wirecard ScandalDocument22 pagesIntroduction To Financial Statements: Wirecard ScandalNilesh Kumar GuptaNo ratings yet

- Financial Accounting Management: Report On Creative AccountingDocument5 pagesFinancial Accounting Management: Report On Creative Accountinganiket_dNo ratings yet

- Creative AccountingDocument7 pagesCreative Accountingeugeniastefania raduNo ratings yet

- Introduce To Management AccountingDocument9 pagesIntroduce To Management AccountingSagung AdvaitaNo ratings yet

- Ethics of Accounting Information 1. Creative Accounting and Earnings ManagementDocument9 pagesEthics of Accounting Information 1. Creative Accounting and Earnings Managementumarawat_omNo ratings yet

- 2 Managerial Accounting and The Budgeting ProcessDocument9 pages2 Managerial Accounting and The Budgeting ProcessAshraf Galal100% (1)

- Discussion Question W9 Creative AccountingDocument5 pagesDiscussion Question W9 Creative AccountingElaine LimNo ratings yet

- CASE STUDY - WHAT WENT WRONG-WorldComDocument3 pagesCASE STUDY - WHAT WENT WRONG-WorldComMark Jaypee SantiagoNo ratings yet

- International ProjectDocument26 pagesInternational ProjectZiad MohammedNo ratings yet

- cREATIVE ACCOUNTINGDocument12 pagescREATIVE ACCOUNTINGAshraful Jaygirdar0% (1)

- Defn CreativeDocument11 pagesDefn CreativeDamulira DavidNo ratings yet

- Planning and Working Capital ManagementDocument4 pagesPlanning and Working Capital ManagementSheena Mari Uy ElleveraNo ratings yet

- Solution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 4th EditionDocument30 pagesSolution Manual For Ethical Obligations and Decision Making in Accounting Text and Cases 4th Editiongabrielthuym96j100% (19)

- Exemplu Big BathDocument16 pagesExemplu Big BathValentin BurcaNo ratings yet

- Chapter 2Document67 pagesChapter 2Adam MilakaraNo ratings yet

- Where Financial Report Still Falls ShortDocument2 pagesWhere Financial Report Still Falls ShortJoel Swapnil SinghNo ratings yet

- 2014 3a. Explain Why Operating Leverage Decreases As A Company Increases Sales and Shifts Away From The Break-Even PointDocument10 pages2014 3a. Explain Why Operating Leverage Decreases As A Company Increases Sales and Shifts Away From The Break-Even PointHiew fuxiangNo ratings yet

- Analyzing Tyco: Aggressive or Out of Line?: Rahmat Faizal & Sensony DPDocument10 pagesAnalyzing Tyco: Aggressive or Out of Line?: Rahmat Faizal & Sensony DPLheegar TanNo ratings yet

- BA 297 Final Exam The Bankruptcy of Lehman BrothersDocument3 pagesBA 297 Final Exam The Bankruptcy of Lehman BrothersChristian Paul BonguezNo ratings yet

- Financial Statement FraudDocument19 pagesFinancial Statement FraudAulia HidayatNo ratings yet

- The Effect of Creative Accounting On The Job Performance of Accountants Auditors in Reporting Financial Statementin Nigeria 2224 8358-1-173Document30 pagesThe Effect of Creative Accounting On The Job Performance of Accountants Auditors in Reporting Financial Statementin Nigeria 2224 8358-1-173Harshini RamasNo ratings yet

- Module 1 Financial Accounting For MBAs - 6th EditionDocument15 pagesModule 1 Financial Accounting For MBAs - 6th EditionjoshNo ratings yet

- Patterns of Earnings ManagementDocument6 pagesPatterns of Earnings ManagementAnis SofiaNo ratings yet

- Creative AccountingDocument13 pagesCreative AccountingMira CE100% (1)

- Accounting Theory Mid-Exam: By: Rusmian Nuzulul P. / 0910233137Document6 pagesAccounting Theory Mid-Exam: By: Rusmian Nuzulul P. / 0910233137Rusmian Nuzulul PujakaneoNo ratings yet

- Ways of Manipulating Accounting StatementsDocument5 pagesWays of Manipulating Accounting StatementsSabyasachi ChowdhuryNo ratings yet

- FR & FasDocument195 pagesFR & FasPrerana SharmaNo ratings yet

- AFM NotesDocument110 pagesAFM NotesNguyen NhanNo ratings yet

- ACC 111 Assessment 2 - Project: Adam MuhammadDocument7 pagesACC 111 Assessment 2 - Project: Adam Muhammadmuhammad raqibNo ratings yet

- Creative Accounting: Case Study:WorldcomDocument11 pagesCreative Accounting: Case Study:WorldcomVikash KumarNo ratings yet

- TUI UniversityDocument9 pagesTUI UniversityChris NailonNo ratings yet

- Fin STM Fraud 2Document6 pagesFin STM Fraud 2Okwuchi AlaukwuNo ratings yet

- Computer AssociatesDocument18 pagesComputer AssociatesRosel RicafortNo ratings yet

- Summary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionFrom EverandSummary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionNo ratings yet

- Balance Sheet Management: Squeezing Extra Profits and Cash from Your BusinessFrom EverandBalance Sheet Management: Squeezing Extra Profits and Cash from Your BusinessNo ratings yet

- Tut 6-IpmDocument3 pagesTut 6-IpmNguyễn Phương ThảoNo ratings yet

- Reduce Reuse RecycleDocument14 pagesReduce Reuse RecycleBombe ZombeNo ratings yet

- Final Behavioral Finance White PaperDocument8 pagesFinal Behavioral Finance White PapernroposNo ratings yet

- Go Negosyo ActDocument26 pagesGo Negosyo ActEngiemar Barbasa TupasNo ratings yet

- Seminar 14 Accounting For Underlying Financial AssetsDocument105 pagesSeminar 14 Accounting For Underlying Financial AssetsPoun GerrNo ratings yet

- ECO1Document5 pagesECO1Precious Mae Sales100% (1)

- Standard Oil Company of New York v. Juan Posadas, JR., 55 Phil. 715Document2 pagesStandard Oil Company of New York v. Juan Posadas, JR., 55 Phil. 715Icel LacanilaoNo ratings yet

- Business Studies Project: Class 12 Marketing Management (Jeans)Document25 pagesBusiness Studies Project: Class 12 Marketing Management (Jeans)Shivam SharmaNo ratings yet

- Applied Auditing Review Course Pre-Board - Answer KeyDocument13 pagesApplied Auditing Review Course Pre-Board - Answer KeyROMAR A. PIGANo ratings yet

- Baldwin Bicycle Case MBA Case StudyDocument24 pagesBaldwin Bicycle Case MBA Case StudyRobin L. M. Cheung100% (9)

- India - Korea Relationship (Khan, Alveera)Document9 pagesIndia - Korea Relationship (Khan, Alveera)Alveera KhanNo ratings yet

- Pricing StrategiesDocument9 pagesPricing StrategiesRajaRam BommarajuNo ratings yet

- Managerial Accounting and CostDocument19 pagesManagerial Accounting and CostIqra MughalNo ratings yet

- Customer Relationship ManmagementDocument51 pagesCustomer Relationship ManmagementmuneerppNo ratings yet

- Rajeswari Barika - Insta Foam Insulation by Tata BlueScope Steel - CharterDocument3 pagesRajeswari Barika - Insta Foam Insulation by Tata BlueScope Steel - CharterDGN ProductionsNo ratings yet

- AXISCADES Engineering Technologies Completes Acquisition of AXISCADES Aerospace & Technologies Pvt. LTD (Company Update)Document3 pagesAXISCADES Engineering Technologies Completes Acquisition of AXISCADES Aerospace & Technologies Pvt. LTD (Company Update)Shyam SunderNo ratings yet

- Essex Crossing Affordable Housing Lottery (Site 2)Document1 pageEssex Crossing Affordable Housing Lottery (Site 2)The Lo-DownNo ratings yet

- Industrial Project On Reliance Life Insurance Company LimitedDocument116 pagesIndustrial Project On Reliance Life Insurance Company LimitedTimothy Brown100% (1)

- 4 Types of Capacity StrategyDocument7 pages4 Types of Capacity StrategySaga HayyuNo ratings yet

- Acai Chapter 17 QuestionnairesDocument5 pagesAcai Chapter 17 QuestionnairesKathleenCusipagNo ratings yet

- 2024 24 01 Technical Due Diligence Report On LongonjoDocument4 pages2024 24 01 Technical Due Diligence Report On Longonjoqoyise.zamaNo ratings yet

- Third Point Q3 2021 Investor Letter TPILDocument10 pagesThird Point Q3 2021 Investor Letter TPILZerohedge100% (2)

- VRIODocument1 pageVRIOrahul_mahajan100% (1)

- Low Cost Strategy 040405Document40 pagesLow Cost Strategy 040405Ranjan JosephNo ratings yet

- NDPL Case StudyDocument10 pagesNDPL Case StudyPrateek BhargavaNo ratings yet

- Usa BrasilDocument185 pagesUsa BrasilCésar NuñezNo ratings yet

- Merchant BankingDocument55 pagesMerchant Bankingsuhaspatel84No ratings yet

- Habitat International: Nesru H. Koroso, Monica Lengoiboni, Jaap A. ZevenbergenDocument15 pagesHabitat International: Nesru H. Koroso, Monica Lengoiboni, Jaap A. ZevenbergenSG GhoshNo ratings yet

- CME - Option Box Spreads As A Financing ToolDocument6 pagesCME - Option Box Spreads As A Financing ToolDavid TaylorNo ratings yet