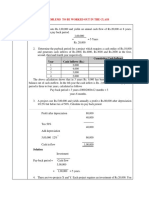

Present Worth Analysis

Present Worth Analysis

You might also like

- Chapter Finance Present Worth Part 2 2023Document32 pagesChapter Finance Present Worth Part 2 2023Danial LuqmanNo ratings yet

- Chapter 8 Part 2 (B)Document30 pagesChapter 8 Part 2 (B)zulhairiNo ratings yet

- Engineering Economy and System AnalysisDocument35 pagesEngineering Economy and System AnalysisNurul BussinessNo ratings yet

- CH 5 - Present Worth AnalysisDocument27 pagesCH 5 - Present Worth AnalysisAli MakkiNo ratings yet

- Chap. 6Document8 pagesChap. 6Khuram MaqsoodNo ratings yet

- 05 Present Worth AnalysisDocument25 pages05 Present Worth Analysis王泓鈞No ratings yet

- Chapter 5 Part 3 of 4 SEPT 2018 PDFDocument24 pagesChapter 5 Part 3 of 4 SEPT 2018 PDFمحمد فائزNo ratings yet

- Ch6 newAnnualWorthAnalysis 2020Document11 pagesCh6 newAnnualWorthAnalysis 2020NUR IZZAH NABILA BINTI ISKANDAR SYAH A18KT0230No ratings yet

- Engineering Economy Alday Ric Harold MDocument6 pagesEngineering Economy Alday Ric Harold MHarold AldayNo ratings yet

- Mcgraw-Hill, Inc: Lecture Notes 5Document6 pagesMcgraw-Hill, Inc: Lecture Notes 5Hassan ShehadiNo ratings yet

- Unit III-PROBLEMSDocument6 pagesUnit III-PROBLEMSPranav GaikwadNo ratings yet

- T 4Document3 pagesT 4Muntasir AhmmedNo ratings yet

- Principles of Corporate Finance: 6th EditionDocument4 pagesPrinciples of Corporate Finance: 6th EditionParin MaruNo ratings yet

- 1 Property, Plant and Equipment IAS 16 Slides 2022Document49 pages1 Property, Plant and Equipment IAS 16 Slides 2022Tuyakula ShipadiNo ratings yet

- Section 5.5 Case 2: Study Period Useful Life: ConditionsDocument18 pagesSection 5.5 Case 2: Study Period Useful Life: ConditionsZoloft Zithromax ProzacNo ratings yet

- GGFGGDocument12 pagesGGFGGkarimNo ratings yet

- Chapter 8 Part 3 (B)Document30 pagesChapter 8 Part 3 (B)zulhairiNo ratings yet

- Summary of Answers PPE Part 2 Theory QuestionsDocument3 pagesSummary of Answers PPE Part 2 Theory QuestionsYameteKudasaiNo ratings yet

- CFAS - Depreciation Methods - Barcelona, JoyceAnnDocument9 pagesCFAS - Depreciation Methods - Barcelona, JoyceAnnJoyce Ann Agdippa BarcelonaNo ratings yet

- CMA Garrison SuggestedSolutions Chap2Document12 pagesCMA Garrison SuggestedSolutions Chap2PIYUSH SINGHNo ratings yet

- Sba SemDocument9 pagesSba SemChelsa Mae AntonioNo ratings yet

- Engineering Economy ENC3310 F18 Ch5Document14 pagesEngineering Economy ENC3310 F18 Ch5ako.rashedNo ratings yet

- Annual Cash Flow AnalysisDocument35 pagesAnnual Cash Flow AnalysisMuhammad Kurnia SandyNo ratings yet

- Pham Le Thuy Duong - HW9Document4 pagesPham Le Thuy Duong - HW9Dương PhạmNo ratings yet

- Replacement Studies NotesDocument4 pagesReplacement Studies NotesVHIMBER GALLUTANNo ratings yet

- Topic 5 - Benefit CostDocument24 pagesTopic 5 - Benefit CostTain WeiShengNo ratings yet

- Om 08.12.2022Document18 pagesOm 08.12.2022raviNo ratings yet

- Annual Cash Flow AnalysisDocument35 pagesAnnual Cash Flow AnalysisNur Irfana Mardiyah DiyahlikebarcelonaNo ratings yet

- Annual Cash Flow AnalysisDocument35 pagesAnnual Cash Flow AnalysisNur Irfana Mardiyah DiyahlikebarcelonaNo ratings yet

- Problems 6Document3 pagesProblems 6jojNo ratings yet

- Capital Budgeting PDocument14 pagesCapital Budgeting PAjayNo ratings yet

- Comparing Investment and Cost AlternativesDocument41 pagesComparing Investment and Cost AlternativesAna Yulieth García GarcíaNo ratings yet

- Ch. 6 - Annual Worth AnalysisDocument7 pagesCh. 6 - Annual Worth AnalysisSidra IqbalNo ratings yet

- Final PB87 Sol. MASDocument2 pagesFinal PB87 Sol. MASLJ AggabaoNo ratings yet

- Present Worth Analysis: Lecture Slides To Accompany Engineering Economy 7th EditionDocument17 pagesPresent Worth Analysis: Lecture Slides To Accompany Engineering Economy 7th EditionJessy LestariNo ratings yet

- A) What Is The Effective Interest Rate Per Payment Period (I B) Compute The Monthly PaymentDocument2 pagesA) What Is The Effective Interest Rate Per Payment Period (I B) Compute The Monthly PaymentTamara al bittarNo ratings yet

- Flexible BudgetsDocument23 pagesFlexible BudgetsscienceplexNo ratings yet

- I. Payback Period Same CF Project A Different CF Project BDocument6 pagesI. Payback Period Same CF Project A Different CF Project Bzh12w8No ratings yet

- Chapter 5 - Present Worth AnalysisDocument17 pagesChapter 5 - Present Worth AnalysisMuhammad Saad Bin AkbarNo ratings yet

- Engineering Economics (BEG495MS)Document1 pageEngineering Economics (BEG495MS)Subas ShresthaNo ratings yet

- Cap Buget ProblemsDocument8 pagesCap Buget ProblemsramakrishnanNo ratings yet

- PB Exam - Answers - SolutionsDocument5 pagesPB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Chapter 10 Dealing With Uncertainty: General ProcedureDocument15 pagesChapter 10 Dealing With Uncertainty: General ProcedureHannan Mahmood TonmoyNo ratings yet

- Property, Plant and Equipment (Part 2) : Problem 1: True or FalseDocument13 pagesProperty, Plant and Equipment (Part 2) : Problem 1: True or FalseJannelle SalacNo ratings yet

- Assignment # 4 - Ch.5 SolvedDocument25 pagesAssignment # 4 - Ch.5 SolvedHidayat UllahNo ratings yet

- Flexible Budgeting Lecture: Fixed/Static BudgetsDocument4 pagesFlexible Budgeting Lecture: Fixed/Static BudgetsSeana GeddesNo ratings yet

- Answer - Capital BudgetingDocument19 pagesAnswer - Capital Budgetingchowchow123No ratings yet

- Lecture 1. Basic Costing CVPDocument14 pagesLecture 1. Basic Costing CVPTân NguyênNo ratings yet

- Ch6 AnnualWorthAnalysisDocument15 pagesCh6 AnnualWorthAnalysisLei YinNo ratings yet

- Chapter 8 Part 4 (B)Document26 pagesChapter 8 Part 4 (B)zulhairiNo ratings yet

- Chapter 8 Part 4 (B)Document26 pagesChapter 8 Part 4 (B)Nurul AsyilahNo ratings yet

- Accounting Seatwork - Analyzing Mixed Costs (5A-1, 5A-3, and 5A-7) - Sheet1Document3 pagesAccounting Seatwork - Analyzing Mixed Costs (5A-1, 5A-3, and 5A-7) - Sheet1liandra espinosaNo ratings yet

- Financial Management - Capital Budgeting Answer KeyDocument5 pagesFinancial Management - Capital Budgeting Answer KeyRed Velvet100% (1)

- Chapter 11 Replacement AnalysisDocument41 pagesChapter 11 Replacement Analysisabdullah 3mar abou reashaNo ratings yet

- Chapter 46 Investment AppraisalDocument4 pagesChapter 46 Investment AppraisalAbdur RafayNo ratings yet

- Annual Equivalence Analysis: Annual Equivalent Criterion Applying Annual Worth Analysis Mutually Exclusive ProjectsDocument43 pagesAnnual Equivalence Analysis: Annual Equivalent Criterion Applying Annual Worth Analysis Mutually Exclusive ProjectsGayuh WNo ratings yet

- Group2 PPEDocument2 pagesGroup2 PPELeane MarcoletaNo ratings yet

- Energy Management & Economics: By: Lec. Ahmed ReyadhDocument20 pagesEnergy Management & Economics: By: Lec. Ahmed Reyadhاحمد محمد عريبيNo ratings yet

- PaybackDocument14 pagesPaybackHema LathaNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Contract 103 One Way 13 May 2020Document19 pagesContract 103 One Way 13 May 2020ruby caldeNo ratings yet

- Sample LetterDocument10 pagesSample LetterSean BovaNo ratings yet

- Dissolution of Partnership FirmDocument28 pagesDissolution of Partnership FirmViransh Coaching Classes100% (2)

- Supply GSTDocument16 pagesSupply GSTMehak Kaushikk100% (1)

- Financial Analysis of Hindustan Uniliver Limited: Group 01Document10 pagesFinancial Analysis of Hindustan Uniliver Limited: Group 01Atindra SahaNo ratings yet

- Cost of CapitalDocument16 pagesCost of CapitalParth BindalNo ratings yet

- Chapter 4 - Q&ADocument19 pagesChapter 4 - Q&APro TenNo ratings yet

- Corporate Law MCQsDocument33 pagesCorporate Law MCQsSalman AliNo ratings yet

- Tle He6 Module 1Document73 pagesTle He6 Module 1ANGELINA RAMBOYONGNo ratings yet

- Homework+3+2015+FALL 2Document4 pagesHomework+3+2015+FALL 2Cecil SagehenNo ratings yet

- FDIC Sues Former Officers, Directors of Westsound BankDocument3 pagesFDIC Sues Former Officers, Directors of Westsound Bankbreil77No ratings yet

- Investors Perception and Investment PatternDocument10 pagesInvestors Perception and Investment PatternAbhiNo ratings yet

- Bar Questions and Answers For CredtransDocument120 pagesBar Questions and Answers For CredtransGreggy LawNo ratings yet

- Dwnload Full Introduction To Operations Research 10th Edition Fred Hillier Solutions Manual PDFDocument36 pagesDwnload Full Introduction To Operations Research 10th Edition Fred Hillier Solutions Manual PDFsquiffycis9444t8100% (17)

- Mobile Services: Your Account Summary This Month'S ChargesDocument3 pagesMobile Services: Your Account Summary This Month'S Chargeskumarvaibhav301745No ratings yet

- SC Annual 11 PDFDocument100 pagesSC Annual 11 PDFRogelio BataclanNo ratings yet

- Qualified Theft and Estafa As Furtive CrimesDocument37 pagesQualified Theft and Estafa As Furtive CrimesNikki Delgado100% (1)

- Advanced Property ValuationDocument8 pagesAdvanced Property ValuationAssignmentLab.comNo ratings yet

- Global Portfolio ManagementDocument3 pagesGlobal Portfolio ManagementVasudevarao MalicherlaNo ratings yet

- VIII. Consideration of Internal ControlDocument15 pagesVIII. Consideration of Internal ControlKrizza MaeNo ratings yet

- What Is Seed and Angel FundingDocument2 pagesWhat Is Seed and Angel FundingQueen ValleNo ratings yet

- Case 22-19361-MBKDocument122 pagesCase 22-19361-MBKasdasdasdNo ratings yet

- Accounting For Manufacturing Concern Lecture 1Document3 pagesAccounting For Manufacturing Concern Lecture 1marites yuNo ratings yet

- CH 4 Feasibility Study and Business PlanDocument87 pagesCH 4 Feasibility Study and Business PlanMihretab Bizuayehu (Mera)No ratings yet

- Jorge RivasDocument1 pageJorge RivasJuan José CastilloNo ratings yet

- OVGU IBE Program HandbookDocument52 pagesOVGU IBE Program HandbookFilip JuncuNo ratings yet

- Budgetory ControlDocument6 pagesBudgetory ControlJash SanghviNo ratings yet

- Elements-Of Money FinancesDocument2 pagesElements-Of Money FinancesMayte DeliyoreNo ratings yet

- NZF Zakat GuideDocument12 pagesNZF Zakat GuideAnonymous xjXXHDlIdNo ratings yet

- Overall Activities of Radiant Communications LTD (1) .Doc 25Document47 pagesOverall Activities of Radiant Communications LTD (1) .Doc 25Sohel Rana0% (1)

Download as pptx, pdf, or txt

You might also like

- Chapter Finance Present Worth Part 2 2023Document32 pagesChapter Finance Present Worth Part 2 2023Danial LuqmanNo ratings yet

- Chapter 8 Part 2 (B)Document30 pagesChapter 8 Part 2 (B)zulhairiNo ratings yet

- Engineering Economy and System AnalysisDocument35 pagesEngineering Economy and System AnalysisNurul BussinessNo ratings yet

- CH 5 - Present Worth AnalysisDocument27 pagesCH 5 - Present Worth AnalysisAli MakkiNo ratings yet

- Chap. 6Document8 pagesChap. 6Khuram MaqsoodNo ratings yet

- 05 Present Worth AnalysisDocument25 pages05 Present Worth Analysis王泓鈞No ratings yet

- Chapter 5 Part 3 of 4 SEPT 2018 PDFDocument24 pagesChapter 5 Part 3 of 4 SEPT 2018 PDFمحمد فائزNo ratings yet

- Ch6 newAnnualWorthAnalysis 2020Document11 pagesCh6 newAnnualWorthAnalysis 2020NUR IZZAH NABILA BINTI ISKANDAR SYAH A18KT0230No ratings yet

- Engineering Economy Alday Ric Harold MDocument6 pagesEngineering Economy Alday Ric Harold MHarold AldayNo ratings yet

- Mcgraw-Hill, Inc: Lecture Notes 5Document6 pagesMcgraw-Hill, Inc: Lecture Notes 5Hassan ShehadiNo ratings yet

- Unit III-PROBLEMSDocument6 pagesUnit III-PROBLEMSPranav GaikwadNo ratings yet

- T 4Document3 pagesT 4Muntasir AhmmedNo ratings yet

- Principles of Corporate Finance: 6th EditionDocument4 pagesPrinciples of Corporate Finance: 6th EditionParin MaruNo ratings yet

- 1 Property, Plant and Equipment IAS 16 Slides 2022Document49 pages1 Property, Plant and Equipment IAS 16 Slides 2022Tuyakula ShipadiNo ratings yet

- Section 5.5 Case 2: Study Period Useful Life: ConditionsDocument18 pagesSection 5.5 Case 2: Study Period Useful Life: ConditionsZoloft Zithromax ProzacNo ratings yet

- GGFGGDocument12 pagesGGFGGkarimNo ratings yet

- Chapter 8 Part 3 (B)Document30 pagesChapter 8 Part 3 (B)zulhairiNo ratings yet

- Summary of Answers PPE Part 2 Theory QuestionsDocument3 pagesSummary of Answers PPE Part 2 Theory QuestionsYameteKudasaiNo ratings yet

- CFAS - Depreciation Methods - Barcelona, JoyceAnnDocument9 pagesCFAS - Depreciation Methods - Barcelona, JoyceAnnJoyce Ann Agdippa BarcelonaNo ratings yet

- CMA Garrison SuggestedSolutions Chap2Document12 pagesCMA Garrison SuggestedSolutions Chap2PIYUSH SINGHNo ratings yet

- Sba SemDocument9 pagesSba SemChelsa Mae AntonioNo ratings yet

- Engineering Economy ENC3310 F18 Ch5Document14 pagesEngineering Economy ENC3310 F18 Ch5ako.rashedNo ratings yet

- Annual Cash Flow AnalysisDocument35 pagesAnnual Cash Flow AnalysisMuhammad Kurnia SandyNo ratings yet

- Pham Le Thuy Duong - HW9Document4 pagesPham Le Thuy Duong - HW9Dương PhạmNo ratings yet

- Replacement Studies NotesDocument4 pagesReplacement Studies NotesVHIMBER GALLUTANNo ratings yet

- Topic 5 - Benefit CostDocument24 pagesTopic 5 - Benefit CostTain WeiShengNo ratings yet

- Om 08.12.2022Document18 pagesOm 08.12.2022raviNo ratings yet

- Annual Cash Flow AnalysisDocument35 pagesAnnual Cash Flow AnalysisNur Irfana Mardiyah DiyahlikebarcelonaNo ratings yet

- Annual Cash Flow AnalysisDocument35 pagesAnnual Cash Flow AnalysisNur Irfana Mardiyah DiyahlikebarcelonaNo ratings yet

- Problems 6Document3 pagesProblems 6jojNo ratings yet

- Capital Budgeting PDocument14 pagesCapital Budgeting PAjayNo ratings yet

- Comparing Investment and Cost AlternativesDocument41 pagesComparing Investment and Cost AlternativesAna Yulieth García GarcíaNo ratings yet

- Ch. 6 - Annual Worth AnalysisDocument7 pagesCh. 6 - Annual Worth AnalysisSidra IqbalNo ratings yet

- Final PB87 Sol. MASDocument2 pagesFinal PB87 Sol. MASLJ AggabaoNo ratings yet

- Present Worth Analysis: Lecture Slides To Accompany Engineering Economy 7th EditionDocument17 pagesPresent Worth Analysis: Lecture Slides To Accompany Engineering Economy 7th EditionJessy LestariNo ratings yet

- A) What Is The Effective Interest Rate Per Payment Period (I B) Compute The Monthly PaymentDocument2 pagesA) What Is The Effective Interest Rate Per Payment Period (I B) Compute The Monthly PaymentTamara al bittarNo ratings yet

- Flexible BudgetsDocument23 pagesFlexible BudgetsscienceplexNo ratings yet

- I. Payback Period Same CF Project A Different CF Project BDocument6 pagesI. Payback Period Same CF Project A Different CF Project Bzh12w8No ratings yet

- Chapter 5 - Present Worth AnalysisDocument17 pagesChapter 5 - Present Worth AnalysisMuhammad Saad Bin AkbarNo ratings yet

- Engineering Economics (BEG495MS)Document1 pageEngineering Economics (BEG495MS)Subas ShresthaNo ratings yet

- Cap Buget ProblemsDocument8 pagesCap Buget ProblemsramakrishnanNo ratings yet

- PB Exam - Answers - SolutionsDocument5 pagesPB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Chapter 10 Dealing With Uncertainty: General ProcedureDocument15 pagesChapter 10 Dealing With Uncertainty: General ProcedureHannan Mahmood TonmoyNo ratings yet

- Property, Plant and Equipment (Part 2) : Problem 1: True or FalseDocument13 pagesProperty, Plant and Equipment (Part 2) : Problem 1: True or FalseJannelle SalacNo ratings yet

- Assignment # 4 - Ch.5 SolvedDocument25 pagesAssignment # 4 - Ch.5 SolvedHidayat UllahNo ratings yet

- Flexible Budgeting Lecture: Fixed/Static BudgetsDocument4 pagesFlexible Budgeting Lecture: Fixed/Static BudgetsSeana GeddesNo ratings yet

- Answer - Capital BudgetingDocument19 pagesAnswer - Capital Budgetingchowchow123No ratings yet

- Lecture 1. Basic Costing CVPDocument14 pagesLecture 1. Basic Costing CVPTân NguyênNo ratings yet

- Ch6 AnnualWorthAnalysisDocument15 pagesCh6 AnnualWorthAnalysisLei YinNo ratings yet

- Chapter 8 Part 4 (B)Document26 pagesChapter 8 Part 4 (B)zulhairiNo ratings yet

- Chapter 8 Part 4 (B)Document26 pagesChapter 8 Part 4 (B)Nurul AsyilahNo ratings yet

- Accounting Seatwork - Analyzing Mixed Costs (5A-1, 5A-3, and 5A-7) - Sheet1Document3 pagesAccounting Seatwork - Analyzing Mixed Costs (5A-1, 5A-3, and 5A-7) - Sheet1liandra espinosaNo ratings yet

- Financial Management - Capital Budgeting Answer KeyDocument5 pagesFinancial Management - Capital Budgeting Answer KeyRed Velvet100% (1)

- Chapter 11 Replacement AnalysisDocument41 pagesChapter 11 Replacement Analysisabdullah 3mar abou reashaNo ratings yet

- Chapter 46 Investment AppraisalDocument4 pagesChapter 46 Investment AppraisalAbdur RafayNo ratings yet

- Annual Equivalence Analysis: Annual Equivalent Criterion Applying Annual Worth Analysis Mutually Exclusive ProjectsDocument43 pagesAnnual Equivalence Analysis: Annual Equivalent Criterion Applying Annual Worth Analysis Mutually Exclusive ProjectsGayuh WNo ratings yet

- Group2 PPEDocument2 pagesGroup2 PPELeane MarcoletaNo ratings yet

- Energy Management & Economics: By: Lec. Ahmed ReyadhDocument20 pagesEnergy Management & Economics: By: Lec. Ahmed Reyadhاحمد محمد عريبيNo ratings yet

- PaybackDocument14 pagesPaybackHema LathaNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Contract 103 One Way 13 May 2020Document19 pagesContract 103 One Way 13 May 2020ruby caldeNo ratings yet

- Sample LetterDocument10 pagesSample LetterSean BovaNo ratings yet

- Dissolution of Partnership FirmDocument28 pagesDissolution of Partnership FirmViransh Coaching Classes100% (2)

- Supply GSTDocument16 pagesSupply GSTMehak Kaushikk100% (1)

- Financial Analysis of Hindustan Uniliver Limited: Group 01Document10 pagesFinancial Analysis of Hindustan Uniliver Limited: Group 01Atindra SahaNo ratings yet

- Cost of CapitalDocument16 pagesCost of CapitalParth BindalNo ratings yet

- Chapter 4 - Q&ADocument19 pagesChapter 4 - Q&APro TenNo ratings yet

- Corporate Law MCQsDocument33 pagesCorporate Law MCQsSalman AliNo ratings yet

- Tle He6 Module 1Document73 pagesTle He6 Module 1ANGELINA RAMBOYONGNo ratings yet

- Homework+3+2015+FALL 2Document4 pagesHomework+3+2015+FALL 2Cecil SagehenNo ratings yet

- FDIC Sues Former Officers, Directors of Westsound BankDocument3 pagesFDIC Sues Former Officers, Directors of Westsound Bankbreil77No ratings yet

- Investors Perception and Investment PatternDocument10 pagesInvestors Perception and Investment PatternAbhiNo ratings yet

- Bar Questions and Answers For CredtransDocument120 pagesBar Questions and Answers For CredtransGreggy LawNo ratings yet

- Dwnload Full Introduction To Operations Research 10th Edition Fred Hillier Solutions Manual PDFDocument36 pagesDwnload Full Introduction To Operations Research 10th Edition Fred Hillier Solutions Manual PDFsquiffycis9444t8100% (17)

- Mobile Services: Your Account Summary This Month'S ChargesDocument3 pagesMobile Services: Your Account Summary This Month'S Chargeskumarvaibhav301745No ratings yet

- SC Annual 11 PDFDocument100 pagesSC Annual 11 PDFRogelio BataclanNo ratings yet

- Qualified Theft and Estafa As Furtive CrimesDocument37 pagesQualified Theft and Estafa As Furtive CrimesNikki Delgado100% (1)

- Advanced Property ValuationDocument8 pagesAdvanced Property ValuationAssignmentLab.comNo ratings yet

- Global Portfolio ManagementDocument3 pagesGlobal Portfolio ManagementVasudevarao MalicherlaNo ratings yet

- VIII. Consideration of Internal ControlDocument15 pagesVIII. Consideration of Internal ControlKrizza MaeNo ratings yet

- What Is Seed and Angel FundingDocument2 pagesWhat Is Seed and Angel FundingQueen ValleNo ratings yet

- Case 22-19361-MBKDocument122 pagesCase 22-19361-MBKasdasdasdNo ratings yet

- Accounting For Manufacturing Concern Lecture 1Document3 pagesAccounting For Manufacturing Concern Lecture 1marites yuNo ratings yet

- CH 4 Feasibility Study and Business PlanDocument87 pagesCH 4 Feasibility Study and Business PlanMihretab Bizuayehu (Mera)No ratings yet

- Jorge RivasDocument1 pageJorge RivasJuan José CastilloNo ratings yet

- OVGU IBE Program HandbookDocument52 pagesOVGU IBE Program HandbookFilip JuncuNo ratings yet

- Budgetory ControlDocument6 pagesBudgetory ControlJash SanghviNo ratings yet

- Elements-Of Money FinancesDocument2 pagesElements-Of Money FinancesMayte DeliyoreNo ratings yet

- NZF Zakat GuideDocument12 pagesNZF Zakat GuideAnonymous xjXXHDlIdNo ratings yet

- Overall Activities of Radiant Communications LTD (1) .Doc 25Document47 pagesOverall Activities of Radiant Communications LTD (1) .Doc 25Sohel Rana0% (1)