Download as ppt, pdf, or txt

You might also like

- 2018 Borrower's Validation Sheet - BvsDocument1 page2018 Borrower's Validation Sheet - BvsAr Ar67% (6)

- Adjusting EntriesDocument16 pagesAdjusting EntriesLuigi Santiago70% (27)

- Adjusting Account, WORK SHEET-FINALDocument43 pagesAdjusting Account, WORK SHEET-FINALChowdhury Mobarrat Haider Adnan100% (1)

- Promissory Note With Restructuring Agreement Promissory NoteDocument5 pagesPromissory Note With Restructuring Agreement Promissory NoteArthur AguilarNo ratings yet

- Chapter 6 Sample ProblemsDocument3 pagesChapter 6 Sample ProblemsShaiTengcoNo ratings yet

- Financial Accounting, 4eDocument42 pagesFinancial Accounting, 4eabdirahman mohamed100% (1)

- The Adjusting Process PDFDocument3 pagesThe Adjusting Process PDFMaria Cristina ArcillaNo ratings yet

- Adjusting The AccountsDocument36 pagesAdjusting The AccountsTasim Ishraque100% (1)

- Sdoc 05 04 SiDocument17 pagesSdoc 05 04 SiIchyy BoiNo ratings yet

- Inancial CCTG: Adjusting The AccountsDocument28 pagesInancial CCTG: Adjusting The AccountsLj BesaNo ratings yet

- Adjusting The Accounts: Financial Accounting - Kieso, KimmelDocument30 pagesAdjusting The Accounts: Financial Accounting - Kieso, KimmelAlvi Rahman100% (1)

- Measuring Profitability and Financial Position On The Financial Statements Chapter 4Document66 pagesMeasuring Profitability and Financial Position On The Financial Statements Chapter 4Rupesh Pol100% (1)

- Adjustment & Adjusting EntriesDocument32 pagesAdjustment & Adjusting EntriesHumair Ahmed100% (1)

- Accounting: John Wiley & Sons, IncDocument37 pagesAccounting: John Wiley & Sons, Incshafaat_90100% (1)

- Adjusting Journal EntriesDocument73 pagesAdjusting Journal EntriesHikari MicoaNo ratings yet

- ABM FABM1-Q4-Week-1Document26 pagesABM FABM1-Q4-Week-1Just OkayNo ratings yet

- FABM AJE and Adjusted Trial Balance Service BusinessDocument18 pagesFABM AJE and Adjusted Trial Balance Service BusinessMarchyrella Uoiea Olin Jovenir50% (4)

- CH 5 ACT2112Document35 pagesCH 5 ACT2112MUSTAFA KAMAL BIN ABD MUTALIP / BURSAR100% (1)

- Accounting - Chapter 3 Accrual Accounting ConceptsDocument27 pagesAccounting - Chapter 3 Accrual Accounting ConceptsheinlinnNo ratings yet

- Grade11 Fabm1 Q2 Week1Document22 pagesGrade11 Fabm1 Q2 Week1Mickaela MonterolaNo ratings yet

- Adjusting Journal Entries: (4 Step of The Accounting Process)Document47 pagesAdjusting Journal Entries: (4 Step of The Accounting Process)Joy Pacot100% (1)

- Math 11 ABM FABM1 Q2 Week 1 With TaskDocument17 pagesMath 11 ABM FABM1 Q2 Week 1 With Taskparedesaudreyrose9No ratings yet

- Math 11 ABM FABM1 Q2 Week 1 For StudentsDocument19 pagesMath 11 ABM FABM1 Q2 Week 1 For StudentsRich Allen Mier UyNo ratings yet

- Chapter 3 PresentationDocument48 pagesChapter 3 Presentationhosie.oqbeNo ratings yet

- Adjusting The Accounts: Accounting Principles, 7 EditionDocument51 pagesAdjusting The Accounts: Accounting Principles, 7 EditionBader_86100% (1)

- Explain The Accrual Basis of Accounting and The Reasons For Adjusting EntriesDocument5 pagesExplain The Accrual Basis of Accounting and The Reasons For Adjusting EntrieshelenaNo ratings yet

- Adjusting The AccountsDocument51 pagesAdjusting The AccountsKlarecel Bautista Mariano100% (1)

- Adjusting EntriesDocument4 pagesAdjusting EntriesDaphne TallorinNo ratings yet

- 6-Principles and Concepts of Measuring IncomeDocument25 pages6-Principles and Concepts of Measuring Incomechobiipiggy26No ratings yet

- Ccounting Principles,: Weygandt, Kieso, & KimmelDocument58 pagesCcounting Principles,: Weygandt, Kieso, & Kimmelpiash246100% (2)

- Chidananda Bhaula - 13 Manan Gupta - 21 Megha Dhamal - 22 Mrunalini Sawarkar - 25 Sagar Chandnani - 42 Saloni Pasad - 43Document16 pagesChidananda Bhaula - 13 Manan Gupta - 21 Megha Dhamal - 22 Mrunalini Sawarkar - 25 Sagar Chandnani - 42 Saloni Pasad - 43saloni pasadNo ratings yet

- Acc 3Document25 pagesAcc 3ruthu ruthvikNo ratings yet

- Day 4 Income Statement and Statement of Cash FlowDocument31 pagesDay 4 Income Statement and Statement of Cash FlowSue-Allen Mardenborough100% (1)

- Adjusting The Accounts: Accounting Principles, 8 EditionDocument44 pagesAdjusting The Accounts: Accounting Principles, 8 EditionSheikh Azizul IslamNo ratings yet

- HANDOUT - PENYESUAIANDocument54 pagesHANDOUT - PENYESUAIANCicilia Intan NovianaNo ratings yet

- Chapter 4 End of The Period Adjustments Final ModuleDocument75 pagesChapter 4 End of The Period Adjustments Final ModuleRian Hanz AlbercaNo ratings yet

- Accounting Principles: Second Canadian EditionDocument30 pagesAccounting Principles: Second Canadian EditionAhmed FahmyNo ratings yet

- Chapter 3: Preparing Financial StatementsDocument17 pagesChapter 3: Preparing Financial StatementsSittie Haynah Moominah BualanNo ratings yet

- Accrual Accounting Concepts: Learning ObjectivesDocument32 pagesAccrual Accounting Concepts: Learning ObjectiveszemeNo ratings yet

- Lesson 3: Basic Accounting: Completing The Accounting Cycle Adjusting The AccountsDocument18 pagesLesson 3: Basic Accounting: Completing The Accounting Cycle Adjusting The AccountsAra ArinqueNo ratings yet

- Completing The Accounting CycleDocument46 pagesCompleting The Accounting CycleGaluh Boga Kuswara100% (1)

- Fundamentals of ABM1 - Q4 - LAS1 DRAFTDocument17 pagesFundamentals of ABM1 - Q4 - LAS1 DRAFTSitti Halima Amilbahar AdgesNo ratings yet

- 1st Semester (Digital Notebook - FABM2)Document5 pages1st Semester (Digital Notebook - FABM2)Raven RubiNo ratings yet

- Business Transactions and Their Analysis As Applied To The Accounting Cycle of A Service BusinessDocument8 pagesBusiness Transactions and Their Analysis As Applied To The Accounting Cycle of A Service BusinessNinia Cresil Ann JalagatNo ratings yet

- Adjusting Journal EntriesDocument34 pagesAdjusting Journal Entriesロザリーロザレス ロザリー・マキルNo ratings yet

- Adjustments 20200216101400Document44 pagesAdjustments 20200216101400Chi Cheng100% (1)

- Module 2 Accounting Concepts and PrinciplesDocument10 pagesModule 2 Accounting Concepts and PrinciplesMica PabalanNo ratings yet

- Ch.3 - Accrual Accounting and The Financial Statements (Pearson 6th Edition) - MHDocument85 pagesCh.3 - Accrual Accounting and The Financial Statements (Pearson 6th Edition) - MHSamZhao100% (1)

- AdjustingDocument39 pagesAdjustingRica mae camon100% (1)

- Unit 8 Adjusting EntriesDocument8 pagesUnit 8 Adjusting EntriesRey ViloriaNo ratings yet

- Unit 8 Adjusting EntriesDocument8 pagesUnit 8 Adjusting EntriesRey ViloriaNo ratings yet

- Accounting Adjustment-Accrued & PrepaidDocument30 pagesAccounting Adjustment-Accrued & PrepaidEida HidayahNo ratings yet

- Accrual Accounting Concepts PDFDocument21 pagesAccrual Accounting Concepts PDFPhillip Gordon MulesNo ratings yet

- Basic Accounting RefresherDocument132 pagesBasic Accounting RefresherJustine BalonaNo ratings yet

- ACCY901 Accounting Foundations For Professionals: Topic 3 Accrual Accounting and Adjusting EntriesDocument35 pagesACCY901 Accounting Foundations For Professionals: Topic 3 Accrual Accounting and Adjusting Entriesvenkatachalam radhakrishnan100% (1)

- Finals ReviewerDocument5 pagesFinals ReviewerGaia BautistaNo ratings yet

- Module 8. FARDocument9 pagesModule 8. FARAntonNo ratings yet

- Financial Statement AnalysisDocument32 pagesFinancial Statement AnalysisMuhammad KhawajaNo ratings yet

- Session 4R - PGP2018 - Accounting MechanicsDocument41 pagesSession 4R - PGP2018 - Accounting MechanicsArty DrillNo ratings yet

- Castellano Fa1 Midterm Module Ba1 ABC LeganesDocument28 pagesCastellano Fa1 Midterm Module Ba1 ABC Leganesma. tricia soberanoNo ratings yet

- Chapter 03 Adjusting The AccountsDocument24 pagesChapter 03 Adjusting The AccountsMohamedNo ratings yet

- Adjusting EntriesDocument18 pagesAdjusting Entriesfrancismaminta2496No ratings yet

- SSS Salary Loan 02-2013Document3 pagesSSS Salary Loan 02-2013Jon Allan Buenaobra100% (2)

- Accounting Methods For GoodwillDocument4 pagesAccounting Methods For GoodwillaskmeeNo ratings yet

- Diagnostic Exam 1.1 AKDocument15 pagesDiagnostic Exam 1.1 AKmarygraceomacNo ratings yet

- SSS LoanDocument3 pagesSSS LoanBudang MasaudlingNo ratings yet

- Standardized Financial Statements - SolutionDocument25 pagesStandardized Financial Statements - SolutionanisaNo ratings yet

- Cash To Inventory Reviewer 1Document15 pagesCash To Inventory Reviewer 1Patricia Camille AustriaNo ratings yet

- SLF066 Calamity Loan Application Form - V05Document2 pagesSLF066 Calamity Loan Application Form - V05Selyun E OnnajNo ratings yet

- Intermidiate Accounting 4Document4 pagesIntermidiate Accounting 4BABANo ratings yet

- 4thEXAM REVIEWERDocument9 pages4thEXAM REVIEWERmarites yuNo ratings yet

- 1205 Fa 08WDocument8 pages1205 Fa 08WomareiNo ratings yet

- FR (New) Suggested Ans CA Final Jan 21Document33 pagesFR (New) Suggested Ans CA Final Jan 21ritz meshNo ratings yet

- Lease ProblemsDocument13 pagesLease Problemssai vishnuNo ratings yet

- Trademarkcopyrightsample ProblemsDocument11 pagesTrademarkcopyrightsample ProblemsFel Jamace MiraNo ratings yet

- Chapter 18 LEASES - Winter 2022 Canvas VersionDocument63 pagesChapter 18 LEASES - Winter 2022 Canvas VersionJared ScottNo ratings yet

- Chapter 9 Assigned Question SOLUTIONSDocument31 pagesChapter 9 Assigned Question SOLUTIONSDang ThanhNo ratings yet

- Quiz 7 - CH 13 & 14 ACC563Document14 pagesQuiz 7 - CH 13 & 14 ACC563scokni1973_130667106No ratings yet

- Pensions Practice QuizDocument10 pagesPensions Practice QuizJyNo ratings yet

- Loan CalculatorDocument24 pagesLoan Calculatoramit22505No ratings yet

- Oblicon-DBP Vs CADocument16 pagesOblicon-DBP Vs CASuiNo ratings yet

- Financial StatemnetDocument23 pagesFinancial Statemnetmelaniekudo100% (1)

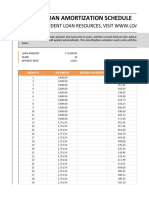

- Excel Student Loan Amortization TableDocument18 pagesExcel Student Loan Amortization TableIsmail UsmanNo ratings yet

- ACC 642 - CH 01 SolutionsDocument17 pagesACC 642 - CH 01 SolutionstboneuncwNo ratings yet

- Soal Kuis Minggu 11Document7 pagesSoal Kuis Minggu 11Natasya ZahraNo ratings yet

- Notes RecievableDocument50 pagesNotes RecievableRyan Abonales BagatuaNo ratings yet

- Reviewer Intangible AssetsDocument10 pagesReviewer Intangible AssetsMay100% (1)

- TVL Finance PLC 2016 Q3 Quarterly Report FINALDocument27 pagesTVL Finance PLC 2016 Q3 Quarterly Report FINALsaxobobNo ratings yet

- 1 Intangible Assets PDFDocument56 pages1 Intangible Assets PDFCatherine RiveraNo ratings yet