Transfer Duty Botswana

Transfer Duty Botswana

You might also like

- 1 One Page Purchase ContractDocument1 page1 One Page Purchase ContractJackson Palmer50% (4)

- IMTC633Document33 pagesIMTC633Ajit Kumar71% (7)

- Lesson 6 Corporate LiquidationDocument11 pagesLesson 6 Corporate Liquidationheyhey100% (2)

- Method Statement For Installation of Steel Supports For Gratings at TR A...Document9 pagesMethod Statement For Installation of Steel Supports For Gratings at TR A...Faraaz MohammedNo ratings yet

- Triple Net LeaseDocument8 pagesTriple Net LeaseRocketLawyer100% (3)

- Kansas Property Management Agreement PDFDocument5 pagesKansas Property Management Agreement PDFDrake MontgomeryNo ratings yet

- PMS Agreement SampleDocument9 pagesPMS Agreement SamplesureshvgkNo ratings yet

- Rent To Own AgreementDocument10 pagesRent To Own AgreementRocketLawyer100% (5)

- Lease With Option To PurchaseDocument10 pagesLease With Option To PurchaseRocketLawyer100% (2)

- Rotating Saving and Credit Association (Rosca)Document4 pagesRotating Saving and Credit Association (Rosca)Misheck D BandaNo ratings yet

- Closing of Real Estate Sale Transactions and Transfer of TitleDocument6 pagesClosing of Real Estate Sale Transactions and Transfer of TitleescaNo ratings yet

- Costs To Transfer A Land Title in The PhilippinesDocument4 pagesCosts To Transfer A Land Title in The PhilippinesCitoy LabadanNo ratings yet

- Extrajudicial Settlement of Estate Rule 74, Section 1 ChecklistDocument8 pagesExtrajudicial Settlement of Estate Rule 74, Section 1 ChecklistMsyang Ann Corbo DiazNo ratings yet

- Property Marketing Assgnmnt 1Document6 pagesProperty Marketing Assgnmnt 1Clive MuchenjeNo ratings yet

- Land Admn and Management Property TaxationDocument4 pagesLand Admn and Management Property TaxationsammiemeshNo ratings yet

- RA 10752 LeafletDocument7 pagesRA 10752 LeafletMark Jefferson Cudal RamosNo ratings yet

- Grant of RightsDocument4 pagesGrant of Rightssanjay singh yadavNo ratings yet

- Tax On Transfer of Real PropertiesDocument8 pagesTax On Transfer of Real PropertiesKristine Astorga-NgNo ratings yet

- Washington Property Management Agreement PDFDocument5 pagesWashington Property Management Agreement PDFDrake MontgomeryNo ratings yet

- CARL ANDREW Assignment Tax 102Document7 pagesCARL ANDREW Assignment Tax 102Carl Andrew Aborquez Arcinal0% (1)

- Quick Sell Repossessed Properties FNB: WWW - Quicksell.co - ZaDocument9 pagesQuick Sell Repossessed Properties FNB: WWW - Quicksell.co - ZaChristian MakandeNo ratings yet

- Transfer Tax (Tax 1)Document5 pagesTransfer Tax (Tax 1)Irdo Kwan100% (1)

- Presentation 3 Real Property Gains TaxDocument29 pagesPresentation 3 Real Property Gains TaxAimi AzemiNo ratings yet

- Lgu ProceduresDocument6 pagesLgu ProceduresAli IsaacNo ratings yet

- Steps in Transfer of TCTDocument2 pagesSteps in Transfer of TCTPogi akoNo ratings yet

- We Will Be Bringing You A Series of Articles That Discuss Commonly Asked Questions Regarding Real Estate in GeneralDocument2 pagesWe Will Be Bringing You A Series of Articles That Discuss Commonly Asked Questions Regarding Real Estate in Generalmarnil alfornonNo ratings yet

- Retainer AgreementDocument1 pageRetainer AgreementJoel Agtarap Ildefonso100% (1)

- Estate Tax ReviewerDocument20 pagesEstate Tax ReviewerEller-JedManalacMendozaNo ratings yet

- Lease 2 TDocument2 pagesLease 2 TLeopold StiltskinNo ratings yet

- Residential Rental Lease Agreement: Nome Partners LLCDocument35 pagesResidential Rental Lease Agreement: Nome Partners LLCJose medina carvajalNo ratings yet

- Registration ResearchesDocument2 pagesRegistration ResearchesAnonymous rVFG5CNo ratings yet

- Guideline in The Transfer of Titles of Real PropertyDocument4 pagesGuideline in The Transfer of Titles of Real PropertyLeolaida AragonNo ratings yet

- TAX With TRAIN LAW - Transfer and Business TaxDocument61 pagesTAX With TRAIN LAW - Transfer and Business TaxRamon AngelesNo ratings yet

- Rblex QuestionDocument17 pagesRblex QuestionIsaac CursoNo ratings yet

- Estate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andDocument6 pagesEstate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andAngelyn SamandeNo ratings yet

- Rent Collection TermsDocument10 pagesRent Collection TermsstephintonftNo ratings yet

- Class Notes Virginia 13 GradeDocument13 pagesClass Notes Virginia 13 GradeAnonymusNo ratings yet

- Chapter 6 - Donors TaxDocument59 pagesChapter 6 - Donors Taxargene.malubayNo ratings yet

- Legal Services AgreementDocument2 pagesLegal Services AgreementRocketLawyer100% (5)

- Doclib001 Homebuyer Disclosure StatementDocument4 pagesDoclib001 Homebuyer Disclosure StatementgreenfieldwindersNo ratings yet

- Msi Owner Occupancy AffidavitDocument1 pageMsi Owner Occupancy AffidavitbatinatorNo ratings yet

- Re-Appraisal and Offer To Lease (Signed) - 1Document4 pagesRe-Appraisal and Offer To Lease (Signed) - 1Daniel Lazona JejillosNo ratings yet

- Residential Buy or Sell ContractDocument8 pagesResidential Buy or Sell Contractrotgers5100% (1)

- How Much Does It Cost To Transfer A Land TitleDocument2 pagesHow Much Does It Cost To Transfer A Land TitleMark Jeson Lianza PuraNo ratings yet

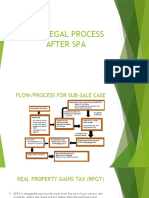

- The Legal Process After SpaDocument16 pagesThe Legal Process After SpaIzat AmirNo ratings yet

- Notes in Estate TaxDocument32 pagesNotes in Estate TaxAngelyn SamandeNo ratings yet

- 11 19 19sampleleaseDocument13 pages11 19 19sampleleaseapi-487640535No ratings yet

- Master Consignment Agreement PDFDocument4 pagesMaster Consignment Agreement PDFL. A. PatersonNo ratings yet

- Samplemaagreement9 19 19Document7 pagesSamplemaagreement9 19 19api-487640535No ratings yet

- Course SynthesisDocument7 pagesCourse SynthesisZiyeon SongNo ratings yet

- Phone: FaxDocument8 pagesPhone: FaxscrealtorsNo ratings yet

- How Much Does It Cost To Transfer A Land Title in The PhilippinesDocument5 pagesHow Much Does It Cost To Transfer A Land Title in The PhilippinesDebra BraciaNo ratings yet

- Litigation Retainer AgreementDocument4 pagesLitigation Retainer AgreementDonita Mariz PalarcaNo ratings yet

- Tax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsDocument31 pagesTax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsMama MiyaNo ratings yet

- Real Estate Purchase AgreementDocument7 pagesReal Estate Purchase AgreementRocketLawyer100% (7)

- Conveyancing LessleyDocument3 pagesConveyancing Lessleylesley chirangoNo ratings yet

- Sign Lease: PagesDocument27 pagesSign Lease: PagesRobert GreeverNo ratings yet

- TMP Lease Documents 20210701050658Document5 pagesTMP Lease Documents 20210701050658ALISONNo ratings yet

- Guide To Tenants: Once Your Offer On A Property Is Agreed, Our Fees Upon Your ApplicationDocument29 pagesGuide To Tenants: Once Your Offer On A Property Is Agreed, Our Fees Upon Your ApplicationAlex DraghiciNo ratings yet

- Property Sale AgreementDocument7 pagesProperty Sale AgreementRocketLawyerNo ratings yet

- Sale Deed TpaDocument16 pagesSale Deed TpaSHIVUM RANANo ratings yet

- Sell A Property JamaicaDocument2 pagesSell A Property Jamaicashantelwest48No ratings yet

- Bill October 1Document2 pagesBill October 1Muhammad RashidNo ratings yet

- Second Call For Paper: National Symposium On Sustainable Waste Management (NSSWM-2019)Document2 pagesSecond Call For Paper: National Symposium On Sustainable Waste Management (NSSWM-2019)Aprizon PutraNo ratings yet

- Analysis of Projection of Women in Advertisements On SocietyDocument4 pagesAnalysis of Projection of Women in Advertisements On SocietyTarun AbrahamNo ratings yet

- Market Never Ending Cycle: ChannelDocument1 pageMarket Never Ending Cycle: ChannelfizzNo ratings yet

- Urc DiscussionDocument3 pagesUrc DiscussionME ValleserNo ratings yet

- MGT601 Solved MCQsDocument32 pagesMGT601 Solved MCQsdani100% (1)

- Ukcs Production Efficiency GuidanceDocument13 pagesUkcs Production Efficiency GuidanceLesly RiveraNo ratings yet

- ProjectDocument69 pagesProjectChandan YadavNo ratings yet

- Let's Check Activity 1: Practice Set 7 Mathematics in Our WorldDocument6 pagesLet's Check Activity 1: Practice Set 7 Mathematics in Our WorldMarybelle Torres VotacionNo ratings yet

- Week 2 Principles of MarketingDocument37 pagesWeek 2 Principles of MarketingOfelia PedelinoNo ratings yet

- Project ReportDocument48 pagesProject ReportMalharNo ratings yet

- Ionut - Unit 8 - ICDocument17 pagesIonut - Unit 8 - ICComsec JonNo ratings yet

- Contract - RegularDocument5 pagesContract - Regularabanganjm08No ratings yet

- Group Assignment: Microeconomics 1 (Bt10203)Document25 pagesGroup Assignment: Microeconomics 1 (Bt10203)Evan YapNo ratings yet

- Demystifying Marketing - A Guide To The Fundamentals For EngineersDocument223 pagesDemystifying Marketing - A Guide To The Fundamentals For EngineersMohamed AbdelAzizNo ratings yet

- Financial StatementsDocument12 pagesFinancial StatementsDino DizonNo ratings yet

- Armitage1995 - Methods AR PDFDocument28 pagesArmitage1995 - Methods AR PDFNicolas CopernicNo ratings yet

- Copy To Be Retained Statement of TDS Under Section 200 (3) of The Income-Tax Act, 1961Document1 pageCopy To Be Retained Statement of TDS Under Section 200 (3) of The Income-Tax Act, 1961suneet bansalNo ratings yet

- AIM's Startup-Guide To Music BusinessDocument64 pagesAIM's Startup-Guide To Music BusinessFA Rakotoniaina100% (2)

- Implementing Information Security System: Prof. Georgette Carpio-Balajadia, Cpa, PHDDocument33 pagesImplementing Information Security System: Prof. Georgette Carpio-Balajadia, Cpa, PHDMike AntolinoNo ratings yet

- Gbm-Balaji Mba College - KadapaDocument172 pagesGbm-Balaji Mba College - KadapaMounishaNo ratings yet

- Types of Supply ChainDocument6 pagesTypes of Supply ChainLusimer AtencioNo ratings yet

- Mba Research Project ReportDocument88 pagesMba Research Project Reportketan monapara100% (1)

- Nicholas Chandler: ProfessionalDocument2 pagesNicholas Chandler: ProfessionalMaritza HuertasNo ratings yet

- 1BS0 02 Que 20201117Document24 pages1BS0 02 Que 20201117FatimaNo ratings yet

- Samara University: College of Business and EconomicsDocument23 pagesSamara University: College of Business and Economicsfeyeko aberaNo ratings yet

Download as pptx, pdf, or txt

You might also like

- 1 One Page Purchase ContractDocument1 page1 One Page Purchase ContractJackson Palmer50% (4)

- IMTC633Document33 pagesIMTC633Ajit Kumar71% (7)

- Lesson 6 Corporate LiquidationDocument11 pagesLesson 6 Corporate Liquidationheyhey100% (2)

- Method Statement For Installation of Steel Supports For Gratings at TR A...Document9 pagesMethod Statement For Installation of Steel Supports For Gratings at TR A...Faraaz MohammedNo ratings yet

- Triple Net LeaseDocument8 pagesTriple Net LeaseRocketLawyer100% (3)

- Kansas Property Management Agreement PDFDocument5 pagesKansas Property Management Agreement PDFDrake MontgomeryNo ratings yet

- PMS Agreement SampleDocument9 pagesPMS Agreement SamplesureshvgkNo ratings yet

- Rent To Own AgreementDocument10 pagesRent To Own AgreementRocketLawyer100% (5)

- Lease With Option To PurchaseDocument10 pagesLease With Option To PurchaseRocketLawyer100% (2)

- Rotating Saving and Credit Association (Rosca)Document4 pagesRotating Saving and Credit Association (Rosca)Misheck D BandaNo ratings yet

- Closing of Real Estate Sale Transactions and Transfer of TitleDocument6 pagesClosing of Real Estate Sale Transactions and Transfer of TitleescaNo ratings yet

- Costs To Transfer A Land Title in The PhilippinesDocument4 pagesCosts To Transfer A Land Title in The PhilippinesCitoy LabadanNo ratings yet

- Extrajudicial Settlement of Estate Rule 74, Section 1 ChecklistDocument8 pagesExtrajudicial Settlement of Estate Rule 74, Section 1 ChecklistMsyang Ann Corbo DiazNo ratings yet

- Property Marketing Assgnmnt 1Document6 pagesProperty Marketing Assgnmnt 1Clive MuchenjeNo ratings yet

- Land Admn and Management Property TaxationDocument4 pagesLand Admn and Management Property TaxationsammiemeshNo ratings yet

- RA 10752 LeafletDocument7 pagesRA 10752 LeafletMark Jefferson Cudal RamosNo ratings yet

- Grant of RightsDocument4 pagesGrant of Rightssanjay singh yadavNo ratings yet

- Tax On Transfer of Real PropertiesDocument8 pagesTax On Transfer of Real PropertiesKristine Astorga-NgNo ratings yet

- Washington Property Management Agreement PDFDocument5 pagesWashington Property Management Agreement PDFDrake MontgomeryNo ratings yet

- CARL ANDREW Assignment Tax 102Document7 pagesCARL ANDREW Assignment Tax 102Carl Andrew Aborquez Arcinal0% (1)

- Quick Sell Repossessed Properties FNB: WWW - Quicksell.co - ZaDocument9 pagesQuick Sell Repossessed Properties FNB: WWW - Quicksell.co - ZaChristian MakandeNo ratings yet

- Transfer Tax (Tax 1)Document5 pagesTransfer Tax (Tax 1)Irdo Kwan100% (1)

- Presentation 3 Real Property Gains TaxDocument29 pagesPresentation 3 Real Property Gains TaxAimi AzemiNo ratings yet

- Lgu ProceduresDocument6 pagesLgu ProceduresAli IsaacNo ratings yet

- Steps in Transfer of TCTDocument2 pagesSteps in Transfer of TCTPogi akoNo ratings yet

- We Will Be Bringing You A Series of Articles That Discuss Commonly Asked Questions Regarding Real Estate in GeneralDocument2 pagesWe Will Be Bringing You A Series of Articles That Discuss Commonly Asked Questions Regarding Real Estate in Generalmarnil alfornonNo ratings yet

- Retainer AgreementDocument1 pageRetainer AgreementJoel Agtarap Ildefonso100% (1)

- Estate Tax ReviewerDocument20 pagesEstate Tax ReviewerEller-JedManalacMendozaNo ratings yet

- Lease 2 TDocument2 pagesLease 2 TLeopold StiltskinNo ratings yet

- Residential Rental Lease Agreement: Nome Partners LLCDocument35 pagesResidential Rental Lease Agreement: Nome Partners LLCJose medina carvajalNo ratings yet

- Registration ResearchesDocument2 pagesRegistration ResearchesAnonymous rVFG5CNo ratings yet

- Guideline in The Transfer of Titles of Real PropertyDocument4 pagesGuideline in The Transfer of Titles of Real PropertyLeolaida AragonNo ratings yet

- TAX With TRAIN LAW - Transfer and Business TaxDocument61 pagesTAX With TRAIN LAW - Transfer and Business TaxRamon AngelesNo ratings yet

- Rblex QuestionDocument17 pagesRblex QuestionIsaac CursoNo ratings yet

- Estate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andDocument6 pagesEstate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andAngelyn SamandeNo ratings yet

- Rent Collection TermsDocument10 pagesRent Collection TermsstephintonftNo ratings yet

- Class Notes Virginia 13 GradeDocument13 pagesClass Notes Virginia 13 GradeAnonymusNo ratings yet

- Chapter 6 - Donors TaxDocument59 pagesChapter 6 - Donors Taxargene.malubayNo ratings yet

- Legal Services AgreementDocument2 pagesLegal Services AgreementRocketLawyer100% (5)

- Doclib001 Homebuyer Disclosure StatementDocument4 pagesDoclib001 Homebuyer Disclosure StatementgreenfieldwindersNo ratings yet

- Msi Owner Occupancy AffidavitDocument1 pageMsi Owner Occupancy AffidavitbatinatorNo ratings yet

- Re-Appraisal and Offer To Lease (Signed) - 1Document4 pagesRe-Appraisal and Offer To Lease (Signed) - 1Daniel Lazona JejillosNo ratings yet

- Residential Buy or Sell ContractDocument8 pagesResidential Buy or Sell Contractrotgers5100% (1)

- How Much Does It Cost To Transfer A Land TitleDocument2 pagesHow Much Does It Cost To Transfer A Land TitleMark Jeson Lianza PuraNo ratings yet

- The Legal Process After SpaDocument16 pagesThe Legal Process After SpaIzat AmirNo ratings yet

- Notes in Estate TaxDocument32 pagesNotes in Estate TaxAngelyn SamandeNo ratings yet

- 11 19 19sampleleaseDocument13 pages11 19 19sampleleaseapi-487640535No ratings yet

- Master Consignment Agreement PDFDocument4 pagesMaster Consignment Agreement PDFL. A. PatersonNo ratings yet

- Samplemaagreement9 19 19Document7 pagesSamplemaagreement9 19 19api-487640535No ratings yet

- Course SynthesisDocument7 pagesCourse SynthesisZiyeon SongNo ratings yet

- Phone: FaxDocument8 pagesPhone: FaxscrealtorsNo ratings yet

- How Much Does It Cost To Transfer A Land Title in The PhilippinesDocument5 pagesHow Much Does It Cost To Transfer A Land Title in The PhilippinesDebra BraciaNo ratings yet

- Litigation Retainer AgreementDocument4 pagesLitigation Retainer AgreementDonita Mariz PalarcaNo ratings yet

- Tax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsDocument31 pagesTax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsMama MiyaNo ratings yet

- Real Estate Purchase AgreementDocument7 pagesReal Estate Purchase AgreementRocketLawyer100% (7)

- Conveyancing LessleyDocument3 pagesConveyancing Lessleylesley chirangoNo ratings yet

- Sign Lease: PagesDocument27 pagesSign Lease: PagesRobert GreeverNo ratings yet

- TMP Lease Documents 20210701050658Document5 pagesTMP Lease Documents 20210701050658ALISONNo ratings yet

- Guide To Tenants: Once Your Offer On A Property Is Agreed, Our Fees Upon Your ApplicationDocument29 pagesGuide To Tenants: Once Your Offer On A Property Is Agreed, Our Fees Upon Your ApplicationAlex DraghiciNo ratings yet

- Property Sale AgreementDocument7 pagesProperty Sale AgreementRocketLawyerNo ratings yet

- Sale Deed TpaDocument16 pagesSale Deed TpaSHIVUM RANANo ratings yet

- Sell A Property JamaicaDocument2 pagesSell A Property Jamaicashantelwest48No ratings yet

- Bill October 1Document2 pagesBill October 1Muhammad RashidNo ratings yet

- Second Call For Paper: National Symposium On Sustainable Waste Management (NSSWM-2019)Document2 pagesSecond Call For Paper: National Symposium On Sustainable Waste Management (NSSWM-2019)Aprizon PutraNo ratings yet

- Analysis of Projection of Women in Advertisements On SocietyDocument4 pagesAnalysis of Projection of Women in Advertisements On SocietyTarun AbrahamNo ratings yet

- Market Never Ending Cycle: ChannelDocument1 pageMarket Never Ending Cycle: ChannelfizzNo ratings yet

- Urc DiscussionDocument3 pagesUrc DiscussionME ValleserNo ratings yet

- MGT601 Solved MCQsDocument32 pagesMGT601 Solved MCQsdani100% (1)

- Ukcs Production Efficiency GuidanceDocument13 pagesUkcs Production Efficiency GuidanceLesly RiveraNo ratings yet

- ProjectDocument69 pagesProjectChandan YadavNo ratings yet

- Let's Check Activity 1: Practice Set 7 Mathematics in Our WorldDocument6 pagesLet's Check Activity 1: Practice Set 7 Mathematics in Our WorldMarybelle Torres VotacionNo ratings yet

- Week 2 Principles of MarketingDocument37 pagesWeek 2 Principles of MarketingOfelia PedelinoNo ratings yet

- Project ReportDocument48 pagesProject ReportMalharNo ratings yet

- Ionut - Unit 8 - ICDocument17 pagesIonut - Unit 8 - ICComsec JonNo ratings yet

- Contract - RegularDocument5 pagesContract - Regularabanganjm08No ratings yet

- Group Assignment: Microeconomics 1 (Bt10203)Document25 pagesGroup Assignment: Microeconomics 1 (Bt10203)Evan YapNo ratings yet

- Demystifying Marketing - A Guide To The Fundamentals For EngineersDocument223 pagesDemystifying Marketing - A Guide To The Fundamentals For EngineersMohamed AbdelAzizNo ratings yet

- Financial StatementsDocument12 pagesFinancial StatementsDino DizonNo ratings yet

- Armitage1995 - Methods AR PDFDocument28 pagesArmitage1995 - Methods AR PDFNicolas CopernicNo ratings yet

- Copy To Be Retained Statement of TDS Under Section 200 (3) of The Income-Tax Act, 1961Document1 pageCopy To Be Retained Statement of TDS Under Section 200 (3) of The Income-Tax Act, 1961suneet bansalNo ratings yet

- AIM's Startup-Guide To Music BusinessDocument64 pagesAIM's Startup-Guide To Music BusinessFA Rakotoniaina100% (2)

- Implementing Information Security System: Prof. Georgette Carpio-Balajadia, Cpa, PHDDocument33 pagesImplementing Information Security System: Prof. Georgette Carpio-Balajadia, Cpa, PHDMike AntolinoNo ratings yet

- Gbm-Balaji Mba College - KadapaDocument172 pagesGbm-Balaji Mba College - KadapaMounishaNo ratings yet

- Types of Supply ChainDocument6 pagesTypes of Supply ChainLusimer AtencioNo ratings yet

- Mba Research Project ReportDocument88 pagesMba Research Project Reportketan monapara100% (1)

- Nicholas Chandler: ProfessionalDocument2 pagesNicholas Chandler: ProfessionalMaritza HuertasNo ratings yet

- 1BS0 02 Que 20201117Document24 pages1BS0 02 Que 20201117FatimaNo ratings yet

- Samara University: College of Business and EconomicsDocument23 pagesSamara University: College of Business and Economicsfeyeko aberaNo ratings yet