Download as pptx, pdf, or txt

You might also like

- Capital Investment Analysis For Engineering and ManagementDocument316 pagesCapital Investment Analysis For Engineering and ManagementCFA100% (2)

- Options Trader 0505Document43 pagesOptions Trader 0505mhosszu100% (2)

- Always Trust The Customer How Zara Has Revolutionized The Fashion Industry and Become A Worldwide LeaderDocument27 pagesAlways Trust The Customer How Zara Has Revolutionized The Fashion Industry and Become A Worldwide LeaderbeatriceNo ratings yet

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument23 pagesIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeSahar YehiaNo ratings yet

- Appendix IDocument30 pagesAppendix ILê Chấn PhongNo ratings yet

- Completing The Cycle SystemDocument44 pagesCompleting The Cycle SystemNeri La LunaNo ratings yet

- Spesial JournalDocument22 pagesSpesial Journalefi jauhariNo ratings yet

- CH 07Document44 pagesCH 07Hasan AzmiNo ratings yet

- Accounting System (Compatibility Mode) PDFDocument10 pagesAccounting System (Compatibility Mode) PDFAftab AlamNo ratings yet

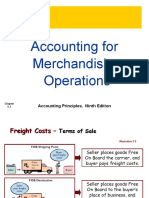

- Accounting For Merchandising Operations: Accounting Principles, Ninth EditionDocument17 pagesAccounting For Merchandising Operations: Accounting Principles, Ninth EditionMehedi HasanNo ratings yet

- Ch07 Accounting Information SystemsDocument30 pagesCh07 Accounting Information SystemsEliza NovirianiNo ratings yet

- Co 1 Fabm 1Document23 pagesCo 1 Fabm 1Eddie MabaleNo ratings yet

- Fma ImportantDocument2 pagesFma ImportanthannnzzuNo ratings yet

- CH 10 Special and Combo Journals and Voucher Sys PDFDocument41 pagesCH 10 Special and Combo Journals and Voucher Sys PDFAira Nhaira MecateNo ratings yet

- Learning Activity Sheet (Q3)Document9 pagesLearning Activity Sheet (Q3)Marlyn LotivioNo ratings yet

- Acctg. Ed 1 - Module5Document11 pagesAcctg. Ed 1 - Module5Chen HaoNo ratings yet

- Week 9&10Document83 pagesWeek 9&10antoniusyoma007No ratings yet

- Journal CompatibilityDocument4 pagesJournal CompatibilityIlham HabibullahNo ratings yet

- 2108AFE Topic 4 - Accounting Information Systems - StudentDocument38 pages2108AFE Topic 4 - Accounting Information Systems - StudentAnh TrầnNo ratings yet

- Accounting Principle Kieso 8e - Ch07Document30 pagesAccounting Principle Kieso 8e - Ch07Sania M. JayantiNo ratings yet

- Final Chapters 4Document19 pagesFinal Chapters 4Nigussie BerhanuNo ratings yet

- Accounting For Merchandising OperationsDocument27 pagesAccounting For Merchandising OperationsnoreenasyikinNo ratings yet

- TM 12-Ch07 Accounting Information System EDITDocument40 pagesTM 12-Ch07 Accounting Information System EDITLydia PujiellitaNo ratings yet

- Acctg. Ed 1 - Unit2 Module 5 Books of Accounts and Double-Entry SystemDocument15 pagesAcctg. Ed 1 - Unit2 Module 5 Books of Accounts and Double-Entry SystemAngel Justine BernardoNo ratings yet

- Accounting For Merchandising OperationsDocument58 pagesAccounting For Merchandising OperationsHEM CHEA100% (11)

- CH 07Document29 pagesCH 07palanisamyam123No ratings yet

- C7 Accounting For ReceivablesDocument36 pagesC7 Accounting For ReceivablesSteeeeeeeephNo ratings yet

- Module 4 Books of AccountDocument6 pagesModule 4 Books of AccountMica PabalanNo ratings yet

- 07 - Subsidiary Ledger and Special Journals Course MaterialsDocument49 pages07 - Subsidiary Ledger and Special Journals Course MaterialserilNo ratings yet

- Financial Accounting: Weygandt KimmelDocument23 pagesFinancial Accounting: Weygandt Kimmelgibe bullyNo ratings yet

- L4 - ABFA1173 POA (Lecturer)Document10 pagesL4 - ABFA1173 POA (Lecturer)Tan SiewsiewNo ratings yet

- CH 7Document19 pagesCH 7J PNo ratings yet

- Whole Brain Learning System Outcome-Based Education: Senior High SchoolDocument16 pagesWhole Brain Learning System Outcome-Based Education: Senior High SchoolHeiyoungNo ratings yet

- Kap 1 6th Workbook Te CH 7Document96 pagesKap 1 6th Workbook Te CH 7Gurpreet KaurNo ratings yet

- Special JournalsDocument15 pagesSpecial JournalsJan Allyson BiagNo ratings yet

- Special JournalsDocument14 pagesSpecial JournalsCriziel Ann LealNo ratings yet

- Far Chapter 4Document50 pagesFar Chapter 4Danica TorresNo ratings yet

- WeyAP 11e PPT Ch07Document45 pagesWeyAP 11e PPT Ch07Rami BadranNo ratings yet

- Accounting Information Systems: Learning ObjectivesDocument46 pagesAccounting Information Systems: Learning ObjectivesPutu DenyNo ratings yet

- Colegio de Sta, Teresa de Avila Foundation IncDocument3 pagesColegio de Sta, Teresa de Avila Foundation IncHarold LuceroNo ratings yet

- Lecture 2 Part 1-Recording ProcessDocument41 pagesLecture 2 Part 1-Recording ProcessAh Heok BoonNo ratings yet

- FAA QuestionsDocument8 pagesFAA Questionssudeepverma007No ratings yet

- Sales Journal (Sales Day Book) - Double Entry BookkeepingDocument4 pagesSales Journal (Sales Day Book) - Double Entry BookkeepingShaina Santiago AlejoNo ratings yet

- 7 Different Types of Journal in Accounting With ExamplesDocument8 pages7 Different Types of Journal in Accounting With ExamplesHaroon YousafNo ratings yet

- Non Leading Ledger Helps in Parallel AccountingDocument6 pagesNon Leading Ledger Helps in Parallel AccountingmonaNo ratings yet

- Chapter5 - Merchandising Company - Pertemuan 8 Dan 9Document95 pagesChapter5 - Merchandising Company - Pertemuan 8 Dan 9Alexandra DionNo ratings yet

- IE01-PAC Lecture Sheet 15 (Class 30)Document2 pagesIE01-PAC Lecture Sheet 15 (Class 30)WILD๛SHOTッ tanvirNo ratings yet

- CH 5 - Accounting For Merchandising OperationsDocument86 pagesCH 5 - Accounting For Merchandising OperationsAdhitya AnggaNo ratings yet

- Financial Statements Analysis - StudentsDocument63 pagesFinancial Statements Analysis - StudentsThanh TienNo ratings yet

- Final Accounts of A Proprietary ConcernDocument14 pagesFinal Accounts of A Proprietary ConcernShivam MutkuleNo ratings yet

- Basic Accounting Module 1 (Topic 5)Document3 pagesBasic Accounting Module 1 (Topic 5)angel may quinaNo ratings yet

- Accounting For Merchandising OperationsDocument58 pagesAccounting For Merchandising OperationsSalvie Perez UtanaNo ratings yet

- EBOOK6131f1fd1229c Unit 4 Subdivision of A Journal PDFDocument30 pagesEBOOK6131f1fd1229c Unit 4 Subdivision of A Journal PDFYaw Antwi-AddaeNo ratings yet

- ISR 111 - Chapter 7 MaterialsDocument9 pagesISR 111 - Chapter 7 MaterialsTrisha Nicole FajardoNo ratings yet

- 155 - Chapter 2Document59 pages155 - Chapter 2منال عبد الرازقNo ratings yet

- Introduction To AccountingDocument4 pagesIntroduction To AccountinglyesyakoubenNo ratings yet

- Accounting For Merchandising OperationsDocument53 pagesAccounting For Merchandising OperationsTanvirNo ratings yet

- Matter Must Exist. Transactions Must Be Supported by Documents Which Prove That The Transaction Did in Fact OccurDocument7 pagesMatter Must Exist. Transactions Must Be Supported by Documents Which Prove That The Transaction Did in Fact OccurDanica MamontayaoNo ratings yet

- CH 6Document16 pagesCH 6Tushar SainiNo ratings yet

- Business Studies Form 4 Schemes of WorkDocument15 pagesBusiness Studies Form 4 Schemes of WorkDavi Kapchanga KenyaNo ratings yet

- Chp. # 3Document36 pagesChp. # 3CFANo ratings yet

- Chapter 7Document40 pagesChapter 7CFANo ratings yet

- Chp. # 2Document36 pagesChp. # 2CFANo ratings yet

- Chapter 8Document54 pagesChapter 8CFANo ratings yet

- Payout PolicyDocument41 pagesPayout PolicyCFANo ratings yet

- Chapter 9 - RDocument37 pagesChapter 9 - RCFANo ratings yet

- Chapter 28RDocument29 pagesChapter 28RCFANo ratings yet

- Formula Sheet For EE406: N N N N NDocument7 pagesFormula Sheet For EE406: N N N N NCFANo ratings yet

- City of Paranaque Ordinance No. 31 Series of 2011 2Document3 pagesCity of Paranaque Ordinance No. 31 Series of 2011 2Jo Mary LudovicoNo ratings yet

- SHAZ Final ReportDocument31 pagesSHAZ Final ReportAsad MazharNo ratings yet

- DB2 9.7 LUW Full Online Backups - Experiments and ConsiderationsDocument26 pagesDB2 9.7 LUW Full Online Backups - Experiments and Considerationsraul_oliveira_83No ratings yet

- Empretec and (Indian) State Governments, Mind-Maps PDFDocument6 pagesEmpretec and (Indian) State Governments, Mind-Maps PDFTausif AhmedNo ratings yet

- Chapter 13 - Short Term Scheduling (Latihan)Document1 pageChapter 13 - Short Term Scheduling (Latihan)firaNo ratings yet

- IBM Cognos 8 4 1 Administration and Security GuideDocument841 pagesIBM Cognos 8 4 1 Administration and Security GuidecoolcapsiNo ratings yet

- CMA - Chapter 4 3eDocument91 pagesCMA - Chapter 4 3ePhomolo StoffelNo ratings yet

- SSC Model Test 01Document9 pagesSSC Model Test 01nikhilam.comNo ratings yet

- Christina M. Trujillo Proposal - RedactedDocument12 pagesChristina M. Trujillo Proposal - RedactedL. A. PatersonNo ratings yet

- Business and Education Advisory MembersDocument1 pageBusiness and Education Advisory MembersMichelle StubbsNo ratings yet

- Part 2Document179 pagesPart 2api-253241169No ratings yet

- Appraisal Comments DraftDocument4 pagesAppraisal Comments DraftPramodSadasivanNo ratings yet

- Audit Non Conformance ReportDocument4 pagesAudit Non Conformance Reportbudi_alamsyah100% (2)

- The Importance of Ethics and Social Responsibility in An OrganizationDocument4 pagesThe Importance of Ethics and Social Responsibility in An OrganizationShaheer BokhariNo ratings yet

- Project Assignment: Scope Purpose Covered inDocument6 pagesProject Assignment: Scope Purpose Covered inapplefieldNo ratings yet

- Create First OLAP Cube in SQL Server Analysis Services - CodeProjectDocument22 pagesCreate First OLAP Cube in SQL Server Analysis Services - CodeProjectchinne046No ratings yet

- Shazz ProjectDocument3 pagesShazz ProjectShahin NoorNo ratings yet

- Archibald 11 08 PDFDocument13 pagesArchibald 11 08 PDFkvijayasokNo ratings yet

- Ashok Resume.Document3 pagesAshok Resume.Pritesh MistryNo ratings yet

- Nmims Indore - BrochureDocument30 pagesNmims Indore - BrochureParas JatanaNo ratings yet

- Unit 3 Job Application Letters: ContentDocument17 pagesUnit 3 Job Application Letters: ContentanaNo ratings yet

- Briefings - LiatDocument2 pagesBriefings - Liatapi-252471713No ratings yet

- Human Resource BundlesDocument8 pagesHuman Resource Bundleskidszalor1412No ratings yet

- Top Business Schools-2009Document2 pagesTop Business Schools-2009SM OmerNo ratings yet

- GMAT Verbal and Quant Official Questions1Document3 pagesGMAT Verbal and Quant Official Questions1PratikJainNo ratings yet

- Redler Conveyor Company v. Commissioner of Internal Revenue, 303 F.2d 567, 1st Cir. (1962)Document4 pagesRedler Conveyor Company v. Commissioner of Internal Revenue, 303 F.2d 567, 1st Cir. (1962)Scribd Government DocsNo ratings yet

- Module 2 SlidesDocument46 pagesModule 2 Slideskrunoslav6077No ratings yet

- RP-Sanjiv Goenka Group: Growing LegaciesDocument10 pagesRP-Sanjiv Goenka Group: Growing Legaciessouvik dasguptaNo ratings yet