Pakistan Payments Landscape - A Glance

Pakistan Payments Landscape - A Glance

You might also like

- Teaming at Disney AnimationDocument10 pagesTeaming at Disney AnimationVasudev Achar100% (5)

- Security Bank P2Document9 pagesSecurity Bank P2jancat_06100% (2)

- Latihan Soal PGDocument12 pagesLatihan Soal PGshafirasrjNo ratings yet

- Pea Petroleum EconomicsDocument68 pagesPea Petroleum EconomicsShehzad khan100% (1)

- Private Fitness LLC Case AnalysisDocument7 pagesPrivate Fitness LLC Case AnalysisKanta Rio Saputra100% (2)

- 2 Banking InstitutionsDocument13 pages2 Banking InstitutionsAsad AkhlaqNo ratings yet

- NETC Ecosystem StatisticsDocument1 pageNETC Ecosystem StatisticsAshwin RowNo ratings yet

- Vietnam Retail Banking 2022 D1tru0Document39 pagesVietnam Retail Banking 2022 D1tru0ankyanky122No ratings yet

- March PublicationDocument5 pagesMarch PublicationErnest MakunguNo ratings yet

- History of Indian BankingDocument19 pagesHistory of Indian BankingShubhamNo ratings yet

- Mobile Banking at A GlanceDocument13 pagesMobile Banking at A Glanceonyx.midnighter2No ratings yet

- Problems and Prospects of Agent Banking in Coastal Area of BangladeshDocument21 pagesProblems and Prospects of Agent Banking in Coastal Area of BangladeshAhmed RiajNo ratings yet

- June Publication 2020Document5 pagesJune Publication 2020macleanabanda44No ratings yet

- Bank Management: PGDM Iimc 2020 Praloy MajumderDocument40 pagesBank Management: PGDM Iimc 2020 Praloy MajumderLiontiniNo ratings yet

- Payments Banks Group 1 UpdatedDocument17 pagesPayments Banks Group 1 UpdatedIBatJNo ratings yet

- IFB Ethiopia Report PDFDocument3 pagesIFB Ethiopia Report PDFfeyselNo ratings yet

- Comparative Analysis Among Bank's Interest RateDocument5 pagesComparative Analysis Among Bank's Interest RateTyler Blake ZyNo ratings yet

- Table B6: Bank-Wise Non-Performing Assets (Npas) of Scheduled Commercial Banks: 2004 (Amount in Rs - Crore) As On March 31 Bank Name Gross Npas Gross Advances Gross Npa Ratio %Document2 pagesTable B6: Bank-Wise Non-Performing Assets (Npas) of Scheduled Commercial Banks: 2004 (Amount in Rs - Crore) As On March 31 Bank Name Gross Npas Gross Advances Gross Npa Ratio %abcNo ratings yet

- Banking SectorDocument14 pagesBanking SectorVivek S MayinkarNo ratings yet

- Philippine-Clearing-House-Corporation ReportDocument32 pagesPhilippine-Clearing-House-Corporation ReportJohn Carlo BuayNo ratings yet

- State Bank of PakistanDocument162 pagesState Bank of Pakistanali_mudassarNo ratings yet

- Live Bank Status in Esign Live S.No Bank NameDocument1 pageLive Bank Status in Esign Live S.No Bank NamergergregNo ratings yet

- (Amit Kumar) Foreign Banks in IndiaDocument27 pages(Amit Kumar) Foreign Banks in IndiaPrachi PandeyNo ratings yet

- Electronic Banking and E-Commerce (F-629) Term Paper Name: E-Banking Services Offered by Banks in BangladeshDocument12 pagesElectronic Banking and E-Commerce (F-629) Term Paper Name: E-Banking Services Offered by Banks in BangladeshMamun RashidNo ratings yet

- Annex 258 AU1514Document4 pagesAnnex 258 AU1514madhavjadhav2018No ratings yet

- India Credit Card ReportDocument12 pagesIndia Credit Card ReportmalvikasinghalNo ratings yet

- NPA2008Document2 pagesNPA2008vishwanathNo ratings yet

- M&B REPORTDocument29 pagesM&B REPORTMaryam KamranNo ratings yet

- Credit Information Bureau (India) LimitedDocument39 pagesCredit Information Bureau (India) LimitedmumbaiskingNo ratings yet

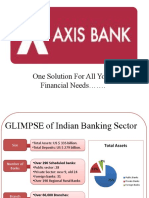

- Axis Bank: One Solution For All Your Financial NeedsDocument46 pagesAxis Bank: One Solution For All Your Financial NeedsInderpreet SinghNo ratings yet

- Estimated RateDocument10 pagesEstimated Rateashok omegaNo ratings yet

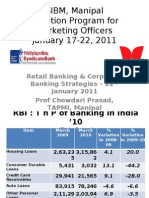

- Sibm, RBCBDocument20 pagesSibm, RBCBProf Dr Chowdari PrasadNo ratings yet

- Bank Wise Non-Performing Assets As Percentage of Total Assets Table 1-Gross Npas To Total AssetsDocument12 pagesBank Wise Non-Performing Assets As Percentage of Total Assets Table 1-Gross Npas To Total AssetsAnkit GuptaNo ratings yet

- Chapeter 2: Introduction of Pubali Bank LTDDocument16 pagesChapeter 2: Introduction of Pubali Bank LTDMuhammad Hayath ChowdhuryNo ratings yet

- What Banks Are & What Do They DoDocument22 pagesWhat Banks Are & What Do They DoladlaNo ratings yet

- Fin Nifty Components and Their WeightageDocument2 pagesFin Nifty Components and Their WeightageKittu TitanNo ratings yet

- Inclusive Smiles @bharat @2017-18Document32 pagesInclusive Smiles @bharat @2017-18Ravi MohanNo ratings yet

- Case StudyDocument87 pagesCase StudychallenegreneelNo ratings yet

- Developing A Strategic Plan For Brac BanDocument40 pagesDeveloping A Strategic Plan For Brac BanpasdNo ratings yet

- One Stop Payment Gateway Solution: Form-BuilderDocument35 pagesOne Stop Payment Gateway Solution: Form-BuilderSuryaChummaNo ratings yet

- Bank Analysis WorkingDocument21 pagesBank Analysis WorkingNajmus SakibNo ratings yet

- Mobile Banking Industry of BangladeshDocument12 pagesMobile Banking Industry of BangladeshTaymur Hasan MunnaNo ratings yet

- BCR-0-909-2022 - 0% Installment Promo - SM StoreDocument1 pageBCR-0-909-2022 - 0% Installment Promo - SM StoreVivienne MarchelineNo ratings yet

- Marketing ResearchDocument19 pagesMarketing Researchapi-3697308No ratings yet

- Midlands State University: Module: Marketing of Financial Services (Mmrk812)Document58 pagesMidlands State University: Module: Marketing of Financial Services (Mmrk812)Maxwell DziyaNo ratings yet

- Final Project Sbi (Niddhi)Document32 pagesFinal Project Sbi (Niddhi)Shraddha GaikwadNo ratings yet

- Banking: Profitability Factors of Regional Rural Banks, Cooperative Banks and Commercial BanksDocument30 pagesBanking: Profitability Factors of Regional Rural Banks, Cooperative Banks and Commercial Banksmicky=No ratings yet

- Sector Overview On Indian Banking Industry: BY BhausahebDocument38 pagesSector Overview On Indian Banking Industry: BY BhausahebPranavNo ratings yet

- Reserve Bank of India - BanklinksDocument3 pagesReserve Bank of India - BanklinksAyushNo ratings yet

- PayU Recurring Integration V4Document49 pagesPayU Recurring Integration V4Tamal SenNo ratings yet

- Lanka ClearDocument19 pagesLanka ClearRajithaNo ratings yet

- Topic 11 (Money, Banking)Document35 pagesTopic 11 (Money, Banking)a191318No ratings yet

- Core Banking SolutionDocument42 pagesCore Banking SolutionbusinessmbaNo ratings yet

- POs Pre Joining Study Material PDFDocument152 pagesPOs Pre Joining Study Material PDFKushagra Pratap SinghNo ratings yet

- Bse E-Mandate ProcessDocument18 pagesBse E-Mandate ProcessShakti ShivanandNo ratings yet

- Questionnaire - S KunduDocument3 pagesQuestionnaire - S KunduSoumyajyoti KunduNo ratings yet

- Chapter 1: Introduction: Page - 1Document41 pagesChapter 1: Introduction: Page - 1Ehasanul HamimNo ratings yet

- Punjab National Bank - Banking ReportDocument36 pagesPunjab National Bank - Banking ReportGoutham SunilNo ratings yet

- SI PPT - Group 5Document20 pagesSI PPT - Group 5Siddharth KumarNo ratings yet

- All Banks in IndiaDocument11 pagesAll Banks in Indiamehul1810No ratings yet

- Chapter 01Document24 pagesChapter 01munatasneemNo ratings yet

- List of Payment Banks & Small Finance Banks: For Bank and Government ExamsDocument7 pagesList of Payment Banks & Small Finance Banks: For Bank and Government Examsjiby georgeNo ratings yet

- The Design of Micro Credit Contracts and Micro Enterprise Finance in UgandaFrom EverandThe Design of Micro Credit Contracts and Micro Enterprise Finance in UgandaNo ratings yet

- Small Money Big Impact: Fighting Poverty with MicrofinanceFrom EverandSmall Money Big Impact: Fighting Poverty with MicrofinanceNo ratings yet

- ACT Bill December 2019Document4 pagesACT Bill December 2019kulaiNo ratings yet

- STR Op BB OkDocument18 pagesSTR Op BB OkriddhmarketingNo ratings yet

- Invoice PBT2723A00184059Document1 pageInvoice PBT2723A00184059WORK MODENo ratings yet

- Taaleem Prospectous enDocument364 pagesTaaleem Prospectous enajit23nayakNo ratings yet

- Income From SalariesDocument30 pagesIncome From SalariesSanket MhetreNo ratings yet

- Tata Steel 2015 16 PDFDocument300 pagesTata Steel 2015 16 PDFAman PrasasdNo ratings yet

- Do 237 22Document5 pagesDo 237 22Agent BlueNo ratings yet

- Maven Security Registration Form 2023 2Document1 pageMaven Security Registration Form 2023 2zab348168No ratings yet

- Chapter - Issue of Share For CPTDocument8 pagesChapter - Issue of Share For CPTCacptCoachingNo ratings yet

- Economics Notes - 1Document268 pagesEconomics Notes - 1william koechNo ratings yet

- America+Canada Les HorswillDocument15 pagesAmerica+Canada Les Horswillbrent4327No ratings yet

- Principles and Practices of ManagementDocument27 pagesPrinciples and Practices of ManagementYuvaraj patilNo ratings yet

- Admas University School of Postgraduate Studies MBA Financial Management AssignmentDocument17 pagesAdmas University School of Postgraduate Studies MBA Financial Management AssignmentAbnet BeleteNo ratings yet

- Chapter 02Document56 pagesChapter 02MD Hafizul Islam HafizNo ratings yet

- Dolmen CIty REIT Annual Financial Statments-30-June-2017Document85 pagesDolmen CIty REIT Annual Financial Statments-30-June-2017FURQANNo ratings yet

- Measureable Results Doing Business Proje PDFDocument4 pagesMeasureable Results Doing Business Proje PDFMarius TeodorNo ratings yet

- Future of Trade 2021 Crypto Edition - DMCC - ENDocument27 pagesFuture of Trade 2021 Crypto Edition - DMCC - ENAsier GarciaNo ratings yet

- Entrepreneurship BruhDocument3 pagesEntrepreneurship BruhMarl Adam S CababasadaNo ratings yet

- Leave Policy DocumentsDocument18 pagesLeave Policy DocumentsSanjay RamuNo ratings yet

- Vridhi MagazineDocument22 pagesVridhi MagazinemahboobahmedlaskarNo ratings yet

- CFO-Forum EEV Principles and Guidance April 2016Document22 pagesCFO-Forum EEV Principles and Guidance April 2016apluNo ratings yet

- Quality Service Management in Hospitality and Tourism: Taguig City UniversityDocument10 pagesQuality Service Management in Hospitality and Tourism: Taguig City UniversityRenz John Louie PullarcaNo ratings yet

- Consumers in 2030: Forecasts and Projections For Life in 2030Document15 pagesConsumers in 2030: Forecasts and Projections For Life in 2030Adriano AraujoNo ratings yet

- Struktur Organisasi: Organization StructureDocument2 pagesStruktur Organisasi: Organization StructureRalila SejahteraNo ratings yet

- Bihar Treasury Code 2011 enDocument268 pagesBihar Treasury Code 2011 enसंजय कुमार चौधरी100% (1)

- Affirmative Constructive SpeechDocument8 pagesAffirmative Constructive SpeechMahatma Kristine DinglasaNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Teaming at Disney AnimationDocument10 pagesTeaming at Disney AnimationVasudev Achar100% (5)

- Security Bank P2Document9 pagesSecurity Bank P2jancat_06100% (2)

- Latihan Soal PGDocument12 pagesLatihan Soal PGshafirasrjNo ratings yet

- Pea Petroleum EconomicsDocument68 pagesPea Petroleum EconomicsShehzad khan100% (1)

- Private Fitness LLC Case AnalysisDocument7 pagesPrivate Fitness LLC Case AnalysisKanta Rio Saputra100% (2)

- 2 Banking InstitutionsDocument13 pages2 Banking InstitutionsAsad AkhlaqNo ratings yet

- NETC Ecosystem StatisticsDocument1 pageNETC Ecosystem StatisticsAshwin RowNo ratings yet

- Vietnam Retail Banking 2022 D1tru0Document39 pagesVietnam Retail Banking 2022 D1tru0ankyanky122No ratings yet

- March PublicationDocument5 pagesMarch PublicationErnest MakunguNo ratings yet

- History of Indian BankingDocument19 pagesHistory of Indian BankingShubhamNo ratings yet

- Mobile Banking at A GlanceDocument13 pagesMobile Banking at A Glanceonyx.midnighter2No ratings yet

- Problems and Prospects of Agent Banking in Coastal Area of BangladeshDocument21 pagesProblems and Prospects of Agent Banking in Coastal Area of BangladeshAhmed RiajNo ratings yet

- June Publication 2020Document5 pagesJune Publication 2020macleanabanda44No ratings yet

- Bank Management: PGDM Iimc 2020 Praloy MajumderDocument40 pagesBank Management: PGDM Iimc 2020 Praloy MajumderLiontiniNo ratings yet

- Payments Banks Group 1 UpdatedDocument17 pagesPayments Banks Group 1 UpdatedIBatJNo ratings yet

- IFB Ethiopia Report PDFDocument3 pagesIFB Ethiopia Report PDFfeyselNo ratings yet

- Comparative Analysis Among Bank's Interest RateDocument5 pagesComparative Analysis Among Bank's Interest RateTyler Blake ZyNo ratings yet

- Table B6: Bank-Wise Non-Performing Assets (Npas) of Scheduled Commercial Banks: 2004 (Amount in Rs - Crore) As On March 31 Bank Name Gross Npas Gross Advances Gross Npa Ratio %Document2 pagesTable B6: Bank-Wise Non-Performing Assets (Npas) of Scheduled Commercial Banks: 2004 (Amount in Rs - Crore) As On March 31 Bank Name Gross Npas Gross Advances Gross Npa Ratio %abcNo ratings yet

- Banking SectorDocument14 pagesBanking SectorVivek S MayinkarNo ratings yet

- Philippine-Clearing-House-Corporation ReportDocument32 pagesPhilippine-Clearing-House-Corporation ReportJohn Carlo BuayNo ratings yet

- State Bank of PakistanDocument162 pagesState Bank of Pakistanali_mudassarNo ratings yet

- Live Bank Status in Esign Live S.No Bank NameDocument1 pageLive Bank Status in Esign Live S.No Bank NamergergregNo ratings yet

- (Amit Kumar) Foreign Banks in IndiaDocument27 pages(Amit Kumar) Foreign Banks in IndiaPrachi PandeyNo ratings yet

- Electronic Banking and E-Commerce (F-629) Term Paper Name: E-Banking Services Offered by Banks in BangladeshDocument12 pagesElectronic Banking and E-Commerce (F-629) Term Paper Name: E-Banking Services Offered by Banks in BangladeshMamun RashidNo ratings yet

- Annex 258 AU1514Document4 pagesAnnex 258 AU1514madhavjadhav2018No ratings yet

- India Credit Card ReportDocument12 pagesIndia Credit Card ReportmalvikasinghalNo ratings yet

- NPA2008Document2 pagesNPA2008vishwanathNo ratings yet

- M&B REPORTDocument29 pagesM&B REPORTMaryam KamranNo ratings yet

- Credit Information Bureau (India) LimitedDocument39 pagesCredit Information Bureau (India) LimitedmumbaiskingNo ratings yet

- Axis Bank: One Solution For All Your Financial NeedsDocument46 pagesAxis Bank: One Solution For All Your Financial NeedsInderpreet SinghNo ratings yet

- Estimated RateDocument10 pagesEstimated Rateashok omegaNo ratings yet

- Sibm, RBCBDocument20 pagesSibm, RBCBProf Dr Chowdari PrasadNo ratings yet

- Bank Wise Non-Performing Assets As Percentage of Total Assets Table 1-Gross Npas To Total AssetsDocument12 pagesBank Wise Non-Performing Assets As Percentage of Total Assets Table 1-Gross Npas To Total AssetsAnkit GuptaNo ratings yet

- Chapeter 2: Introduction of Pubali Bank LTDDocument16 pagesChapeter 2: Introduction of Pubali Bank LTDMuhammad Hayath ChowdhuryNo ratings yet

- What Banks Are & What Do They DoDocument22 pagesWhat Banks Are & What Do They DoladlaNo ratings yet

- Fin Nifty Components and Their WeightageDocument2 pagesFin Nifty Components and Their WeightageKittu TitanNo ratings yet

- Inclusive Smiles @bharat @2017-18Document32 pagesInclusive Smiles @bharat @2017-18Ravi MohanNo ratings yet

- Case StudyDocument87 pagesCase StudychallenegreneelNo ratings yet

- Developing A Strategic Plan For Brac BanDocument40 pagesDeveloping A Strategic Plan For Brac BanpasdNo ratings yet

- One Stop Payment Gateway Solution: Form-BuilderDocument35 pagesOne Stop Payment Gateway Solution: Form-BuilderSuryaChummaNo ratings yet

- Bank Analysis WorkingDocument21 pagesBank Analysis WorkingNajmus SakibNo ratings yet

- Mobile Banking Industry of BangladeshDocument12 pagesMobile Banking Industry of BangladeshTaymur Hasan MunnaNo ratings yet

- BCR-0-909-2022 - 0% Installment Promo - SM StoreDocument1 pageBCR-0-909-2022 - 0% Installment Promo - SM StoreVivienne MarchelineNo ratings yet

- Marketing ResearchDocument19 pagesMarketing Researchapi-3697308No ratings yet

- Midlands State University: Module: Marketing of Financial Services (Mmrk812)Document58 pagesMidlands State University: Module: Marketing of Financial Services (Mmrk812)Maxwell DziyaNo ratings yet

- Final Project Sbi (Niddhi)Document32 pagesFinal Project Sbi (Niddhi)Shraddha GaikwadNo ratings yet

- Banking: Profitability Factors of Regional Rural Banks, Cooperative Banks and Commercial BanksDocument30 pagesBanking: Profitability Factors of Regional Rural Banks, Cooperative Banks and Commercial Banksmicky=No ratings yet

- Sector Overview On Indian Banking Industry: BY BhausahebDocument38 pagesSector Overview On Indian Banking Industry: BY BhausahebPranavNo ratings yet

- Reserve Bank of India - BanklinksDocument3 pagesReserve Bank of India - BanklinksAyushNo ratings yet

- PayU Recurring Integration V4Document49 pagesPayU Recurring Integration V4Tamal SenNo ratings yet

- Lanka ClearDocument19 pagesLanka ClearRajithaNo ratings yet

- Topic 11 (Money, Banking)Document35 pagesTopic 11 (Money, Banking)a191318No ratings yet

- Core Banking SolutionDocument42 pagesCore Banking SolutionbusinessmbaNo ratings yet

- POs Pre Joining Study Material PDFDocument152 pagesPOs Pre Joining Study Material PDFKushagra Pratap SinghNo ratings yet

- Bse E-Mandate ProcessDocument18 pagesBse E-Mandate ProcessShakti ShivanandNo ratings yet

- Questionnaire - S KunduDocument3 pagesQuestionnaire - S KunduSoumyajyoti KunduNo ratings yet

- Chapter 1: Introduction: Page - 1Document41 pagesChapter 1: Introduction: Page - 1Ehasanul HamimNo ratings yet

- Punjab National Bank - Banking ReportDocument36 pagesPunjab National Bank - Banking ReportGoutham SunilNo ratings yet

- SI PPT - Group 5Document20 pagesSI PPT - Group 5Siddharth KumarNo ratings yet

- All Banks in IndiaDocument11 pagesAll Banks in Indiamehul1810No ratings yet

- Chapter 01Document24 pagesChapter 01munatasneemNo ratings yet

- List of Payment Banks & Small Finance Banks: For Bank and Government ExamsDocument7 pagesList of Payment Banks & Small Finance Banks: For Bank and Government Examsjiby georgeNo ratings yet

- The Design of Micro Credit Contracts and Micro Enterprise Finance in UgandaFrom EverandThe Design of Micro Credit Contracts and Micro Enterprise Finance in UgandaNo ratings yet

- Small Money Big Impact: Fighting Poverty with MicrofinanceFrom EverandSmall Money Big Impact: Fighting Poverty with MicrofinanceNo ratings yet

- ACT Bill December 2019Document4 pagesACT Bill December 2019kulaiNo ratings yet

- STR Op BB OkDocument18 pagesSTR Op BB OkriddhmarketingNo ratings yet

- Invoice PBT2723A00184059Document1 pageInvoice PBT2723A00184059WORK MODENo ratings yet

- Taaleem Prospectous enDocument364 pagesTaaleem Prospectous enajit23nayakNo ratings yet

- Income From SalariesDocument30 pagesIncome From SalariesSanket MhetreNo ratings yet

- Tata Steel 2015 16 PDFDocument300 pagesTata Steel 2015 16 PDFAman PrasasdNo ratings yet

- Do 237 22Document5 pagesDo 237 22Agent BlueNo ratings yet

- Maven Security Registration Form 2023 2Document1 pageMaven Security Registration Form 2023 2zab348168No ratings yet

- Chapter - Issue of Share For CPTDocument8 pagesChapter - Issue of Share For CPTCacptCoachingNo ratings yet

- Economics Notes - 1Document268 pagesEconomics Notes - 1william koechNo ratings yet

- America+Canada Les HorswillDocument15 pagesAmerica+Canada Les Horswillbrent4327No ratings yet

- Principles and Practices of ManagementDocument27 pagesPrinciples and Practices of ManagementYuvaraj patilNo ratings yet

- Admas University School of Postgraduate Studies MBA Financial Management AssignmentDocument17 pagesAdmas University School of Postgraduate Studies MBA Financial Management AssignmentAbnet BeleteNo ratings yet

- Chapter 02Document56 pagesChapter 02MD Hafizul Islam HafizNo ratings yet

- Dolmen CIty REIT Annual Financial Statments-30-June-2017Document85 pagesDolmen CIty REIT Annual Financial Statments-30-June-2017FURQANNo ratings yet

- Measureable Results Doing Business Proje PDFDocument4 pagesMeasureable Results Doing Business Proje PDFMarius TeodorNo ratings yet

- Future of Trade 2021 Crypto Edition - DMCC - ENDocument27 pagesFuture of Trade 2021 Crypto Edition - DMCC - ENAsier GarciaNo ratings yet

- Entrepreneurship BruhDocument3 pagesEntrepreneurship BruhMarl Adam S CababasadaNo ratings yet

- Leave Policy DocumentsDocument18 pagesLeave Policy DocumentsSanjay RamuNo ratings yet

- Vridhi MagazineDocument22 pagesVridhi MagazinemahboobahmedlaskarNo ratings yet

- CFO-Forum EEV Principles and Guidance April 2016Document22 pagesCFO-Forum EEV Principles and Guidance April 2016apluNo ratings yet

- Quality Service Management in Hospitality and Tourism: Taguig City UniversityDocument10 pagesQuality Service Management in Hospitality and Tourism: Taguig City UniversityRenz John Louie PullarcaNo ratings yet

- Consumers in 2030: Forecasts and Projections For Life in 2030Document15 pagesConsumers in 2030: Forecasts and Projections For Life in 2030Adriano AraujoNo ratings yet

- Struktur Organisasi: Organization StructureDocument2 pagesStruktur Organisasi: Organization StructureRalila SejahteraNo ratings yet

- Bihar Treasury Code 2011 enDocument268 pagesBihar Treasury Code 2011 enसंजय कुमार चौधरी100% (1)

- Affirmative Constructive SpeechDocument8 pagesAffirmative Constructive SpeechMahatma Kristine DinglasaNo ratings yet