Download as pptx, pdf, or txt

You might also like

- Swift Gpi MT 103 Cash Transfer Auiomatic Direct Account (M0) .Eg.1bDocument18 pagesSwift Gpi MT 103 Cash Transfer Auiomatic Direct Account (M0) .Eg.1bPraphon Vanaphitak82% (11)

- Financial Risk Management: A Simple IntroductionFrom EverandFinancial Risk Management: A Simple IntroductionRating: 4.5 out of 5 stars4.5/5 (7)

- Final TaxDocument26 pagesFinal TaxMarie MendozaNo ratings yet

- Pro Forma: 04/29/2020 42222 Rancho Las Palmas DR., #2141, Rancho Mirage, CA 92270Document1 pagePro Forma: 04/29/2020 42222 Rancho Las Palmas DR., #2141, Rancho Mirage, CA 92270maxwell onyekachukwuNo ratings yet

- Portfolio ManagementDocument50 pagesPortfolio ManagementmamunimamaNo ratings yet

- Group 2 - Efficient Portfolio FormationDocument29 pagesGroup 2 - Efficient Portfolio FormationCindy permatasariNo ratings yet

- Portfolio ManagementDocument50 pagesPortfolio ManagementAnshu JhaNo ratings yet

- Financial Management Revision Notes 2023-24Document163 pagesFinancial Management Revision Notes 2023-24Shermaine ChuaNo ratings yet

- JMC Invest4 PDFDocument46 pagesJMC Invest4 PDFIshanviyaNo ratings yet

- 123 AwatgDocument27 pages123 AwatgPrasadi IidiotNo ratings yet

- Return and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)Document52 pagesReturn and Risk:: Portfolio Theory AND Capital Asset Pricing Model (Capm)anna_alwanNo ratings yet

- Week 4 Lecture PDFDocument69 pagesWeek 4 Lecture PDFAkshat TiwariNo ratings yet

- Topic 2: Portfolio Theory, Selection & InvestingDocument16 pagesTopic 2: Portfolio Theory, Selection & Investing潘超No ratings yet

- #01 Session1Document36 pages#01 Session1YisraelaNo ratings yet

- Discount Rate or Hurdle Rate Module 7 (Class 24)Document18 pagesDiscount Rate or Hurdle Rate Module 7 (Class 24)Vineet Agarwal100% (1)

- Chapter 4Document73 pagesChapter 4Ermiyas KebedeNo ratings yet

- Chapter 7 PortfolioTheoryDocument42 pagesChapter 7 PortfolioTheoryAanchalNo ratings yet

- ps3 2010Document6 pagesps3 2010Ives LeeNo ratings yet

- Lecture 13Document31 pagesLecture 13Fazli WadoodNo ratings yet

- Financial Economics Bocconi Lecture4Document24 pagesFinancial Economics Bocconi Lecture4Elisa CarnevaleNo ratings yet

- Sapm Unit 5Document49 pagesSapm Unit 5Alavudeen Shajahan100% (1)

- Risk and Return S1 2018Document9 pagesRisk and Return S1 2018Quentin SchwartzNo ratings yet

- Risk and Return: Asset Pricing ModelsDocument38 pagesRisk and Return: Asset Pricing ModelsHappy AdelaNo ratings yet

- Portfolio Management & Analysis: 1. UtilityDocument10 pagesPortfolio Management & Analysis: 1. UtilityMarie Remise100% (1)

- Chapter11 Stock Valuation and RiskDocument39 pagesChapter11 Stock Valuation and RiskRaghav MadaanNo ratings yet

- Risk, Return, and The Capital Asset Pricing Model: Muhammad Abubakr NaeemDocument34 pagesRisk, Return, and The Capital Asset Pricing Model: Muhammad Abubakr NaeemMuhammad Abubakr Naeem0% (1)

- Chapter 8Document37 pagesChapter 8AparnaPriom100% (1)

- Money, Banking & Finance: Risk, Return and Portfolio TheoryDocument39 pagesMoney, Banking & Finance: Risk, Return and Portfolio TheorysarahjohnsonNo ratings yet

- Markowitz ModelDocument63 pagesMarkowitz ModeldrramaiyaNo ratings yet

- AssetAllocation v3.05Document221 pagesAssetAllocation v3.05xfsf gdfgfdgfNo ratings yet

- Capital Market LineDocument8 pagesCapital Market Linecjpadin09No ratings yet

- PMT Study Notes ExtractDocument12 pagesPMT Study Notes ExtractAlpeshkumar KabraNo ratings yet

- AssetAllocation v3.06Document221 pagesAssetAllocation v3.06xfsf gdfgfdgfNo ratings yet

- Portfolio Theory 1Document65 pagesPortfolio Theory 1arsenengimbwaNo ratings yet

- Tóm tắt Tài chính doanh nghiệp 2Document42 pagesTóm tắt Tài chính doanh nghiệp 2tranquangtruong911No ratings yet

- Lecture-5 Investors Utility and CALDocument26 pagesLecture-5 Investors Utility and CALHabiba BiboNo ratings yet

- Module #04 - Risk and Rates ReturnDocument13 pagesModule #04 - Risk and Rates ReturnRhesus UrbanoNo ratings yet

- MarkowitzPortfolioOptimisation ReportDocument6 pagesMarkowitzPortfolioOptimisation ReportHimanshu PorwalNo ratings yet

- Arbitrage Pricing TheoryDocument10 pagesArbitrage Pricing TheoryarmailgmNo ratings yet

- Aide Memoire: FTX3044F - TEST 2 (Chapters 5 - 12)Document18 pagesAide Memoire: FTX3044F - TEST 2 (Chapters 5 - 12)Callum Thain BlackNo ratings yet

- Markowitz Portpolio TheoryDocument16 pagesMarkowitz Portpolio TheoryMuhammad SualehNo ratings yet

- Portfolio OptimizationDocument27 pagesPortfolio OptimizationJeremiahOmwoyoNo ratings yet

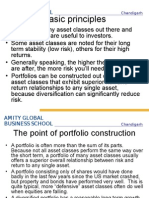

- Basic Principles: Amity Global Business SchoolDocument32 pagesBasic Principles: Amity Global Business SchoolCharu AroraNo ratings yet

- Lect5-2023Document40 pagesLect5-2023vitordias347No ratings yet

- 10 Risk and Return - Student VersionDocument59 pages10 Risk and Return - Student VersionKalyani GogoiNo ratings yet

- Risk - ReturnDocument20 pagesRisk - ReturnAli SallamNo ratings yet

- A Synopsis Report ON: Portfolio ConstructionDocument11 pagesA Synopsis Report ON: Portfolio ConstructionMOHAMMED KHAYYUMNo ratings yet

- CAPM HandoutDocument37 pagesCAPM HandoutShashank ReddyNo ratings yet

- AssetAllocation v2.13Document132 pagesAssetAllocation v2.13xfsf gdfgfdgfNo ratings yet

- Investment Analysis and Portfolio ManagementDocument33 pagesInvestment Analysis and Portfolio ManagementUqaila Mirza0% (1)

- Markowitz 2005Document47 pagesMarkowitz 2005Md Delowar Hossain MithuNo ratings yet

- Lecture # 6: Optimal Risky PortfolioDocument36 pagesLecture # 6: Optimal Risky PortfolioNguyễn VânNo ratings yet

- LECTURE 5b - Advances On Portfolio ManagementDocument36 pagesLECTURE 5b - Advances On Portfolio ManagementKim Hương Hoàng ThịNo ratings yet

- ch07Document53 pagesch07ZoannNo ratings yet

- Chapter - 5: Risk and Return: Portfolio Theory and Assets Pricing ModelsDocument23 pagesChapter - 5: Risk and Return: Portfolio Theory and Assets Pricing Modelswindsor260No ratings yet

- Section 1, Mean Variance AnalysisDocument14 pagesSection 1, Mean Variance AnalysisNeel KanakNo ratings yet

- Investment Analysis and Portfolio ManagementDocument40 pagesInvestment Analysis and Portfolio ManagementJohnNo ratings yet

- Risk and Risk AversionDocument60 pagesRisk and Risk AversionPrathiba PereraNo ratings yet

- Capital Asset Pricing Model: Make smart investment decisions to build a strong portfolioFrom EverandCapital Asset Pricing Model: Make smart investment decisions to build a strong portfolioRating: 4.5 out of 5 stars4.5/5 (3)

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- CISA Exam-Testing Concept-Knowledge of Risk AssessmentFrom EverandCISA Exam-Testing Concept-Knowledge of Risk AssessmentRating: 2.5 out of 5 stars2.5/5 (4)

- Assign.8 Construction Technique - D100164014 - Lalu Muh. A'isy AzizanDocument1 pageAssign.8 Construction Technique - D100164014 - Lalu Muh. A'isy AzizanAziesSiMadridistaNo ratings yet

- Final Exam SheduleDocument1 pageFinal Exam SheduleAziesSiMadridistaNo ratings yet

- Assgn.8 - Lalu Muh. Aisy Azizan - D100164014 - Reinforced Column FoundatinDocument2 pagesAssgn.8 - Lalu Muh. Aisy Azizan - D100164014 - Reinforced Column FoundatinAziesSiMadridistaNo ratings yet

- Final Test Constr Technique Second SMT 2019 2020Document2 pagesFinal Test Constr Technique Second SMT 2019 2020AziesSiMadridistaNo ratings yet

- Final Exam - Roof Design Assignment - Lalu Muh. Aisy Azizan - D100164014Document3 pagesFinal Exam - Roof Design Assignment - Lalu Muh. Aisy Azizan - D100164014AziesSiMadridistaNo ratings yet

- Lalu - Construction Technique Assignment 1Document1 pageLalu - Construction Technique Assignment 1AziesSiMadridistaNo ratings yet

- Visa Direct General Funds Disbursement Sellsheet PDFDocument2 pagesVisa Direct General Funds Disbursement Sellsheet PDFPablo González de PazNo ratings yet

- Monopolistic CompetitionDocument15 pagesMonopolistic Competitionhesham ashrafNo ratings yet

- CitibankDocument20 pagesCitibankjosh321No ratings yet

- SSG Expenses Report Final 2020-2021Document5 pagesSSG Expenses Report Final 2020-2021Loriee LineNo ratings yet

- SCM End Sem QPDocument3 pagesSCM End Sem QPTharun GNo ratings yet

- Tugas Kelompok 6 Bahasa Inggris Niaga Economic Started With GDocument10 pagesTugas Kelompok 6 Bahasa Inggris Niaga Economic Started With GrizkyNo ratings yet

- Project Report OBHRMDocument25 pagesProject Report OBHRMSiddharth BhujwalaNo ratings yet

- Business AsseessmentDocument28 pagesBusiness AsseessmentArisha NicholsNo ratings yet

- Associate Consultant - ATL Sept 2021Document3 pagesAssociate Consultant - ATL Sept 2021Marshay HallNo ratings yet

- Topic 11 - Open-Economy Macroeconomics - Basic Concepts.Document36 pagesTopic 11 - Open-Economy Macroeconomics - Basic Concepts.Trung Hai TrieuNo ratings yet

- Poultry Meat Supply Chains in CameroonDocument17 pagesPoultry Meat Supply Chains in CameroonAyoniseh CarolNo ratings yet

- BCG NBFC Sector Update H1FY24Document48 pagesBCG NBFC Sector Update H1FY24ashi.reportsNo ratings yet

- Tata NanoDocument17 pagesTata NanoSagar Relan100% (1)

- FN2191 Commentary 2022Document27 pagesFN2191 Commentary 2022slimshadyNo ratings yet

- Study On Down Stream Industries of Assam Gas Cracker ProjectDocument167 pagesStudy On Down Stream Industries of Assam Gas Cracker ProjectPriyanka S Rajput100% (1)

- Industrial Policies and Incentives in NigeriaDocument11 pagesIndustrial Policies and Incentives in NigeriaAlima TazabekovaNo ratings yet

- Ch. 14 Economic StabilityDocument8 pagesCh. 14 Economic StabilityHANNAH GODBEHERENo ratings yet

- Federal Government Tells Todd, Julie Chrisley It Wants Their Nearly $1M Settlement From GeorgiaDocument22 pagesFederal Government Tells Todd, Julie Chrisley It Wants Their Nearly $1M Settlement From GeorgiaWSB-TV100% (1)

- Perpetual Inventory System: Rona O. Tolentino Bsom-1DDocument7 pagesPerpetual Inventory System: Rona O. Tolentino Bsom-1DRonaNo ratings yet

- U.S. Individual Income Tax Return: Filing StatusDocument28 pagesU.S. Individual Income Tax Return: Filing StatusSenae Lopez100% (3)

- Topic 4 Finals BREAK EVEN AnalysisDocument4 pagesTopic 4 Finals BREAK EVEN Analysisrommel satajoNo ratings yet

- China Aircraft Lease IndustryDocument26 pagesChina Aircraft Lease IndustryblueraincapitalNo ratings yet

- Philippine Financial Reporting Standards 16 Leases (PFRS 16)Document3 pagesPhilippine Financial Reporting Standards 16 Leases (PFRS 16)Queen ValleNo ratings yet

- NEGOTIABLE INSTRUMENTS - ExamsDocument2 pagesNEGOTIABLE INSTRUMENTS - Examsjan bertNo ratings yet

- DealList 20221116171339Document10 pagesDealList 20221116171339Gia GiaNo ratings yet

- 2023 - Songze - Company Introduction DeckDocument45 pages2023 - Songze - Company Introduction DeckFrancois LaurentNo ratings yet

- Presentation On Government BudgetingDocument2 pagesPresentation On Government BudgetingSherry Gonzales ÜNo ratings yet