Download as pptx, pdf, or txt

You might also like

- Vungle A B TestDocument1 pageVungle A B TestAparna SinghNo ratings yet

- Introduction To Financial Markets and Investment PDFDocument64 pagesIntroduction To Financial Markets and Investment PDFDr. Chhiv Sok Thet100% (12)

- Entrepreneurship Midterm-Examination-2019-20Document4 pagesEntrepreneurship Midterm-Examination-2019-20Ray Faustino67% (3)

- BitMEX Survival Guide v1.5Document33 pagesBitMEX Survival Guide v1.5Kraft DinnerNo ratings yet

- Cgbe Midterm Important SlidesDocument65 pagesCgbe Midterm Important Slideskaustav kunduNo ratings yet

- For Class Iim N Nagpur PGP Mba CG CSR SusDocument354 pagesFor Class Iim N Nagpur PGP Mba CG CSR SusTanisha SinghaiNo ratings yet

- Lecture 1 Slides Week1Document40 pagesLecture 1 Slides Week1Rachita ArikrishnanNo ratings yet

- SIBM CGE Part IIDocument128 pagesSIBM CGE Part IIAkash Amiangshu DuttaNo ratings yet

- 22mba510a BLCG Module 5Document55 pages22mba510a BLCG Module 5Shivakami RajanNo ratings yet

- CG BoardDocument168 pagesCG BoardSANELISO FUTURE MOYONo ratings yet

- Corporate Governance 13Document29 pagesCorporate Governance 13dont_forgetme2004No ratings yet

- Forms of Business Organization: Sole Proprietorships PartnershipsDocument21 pagesForms of Business Organization: Sole Proprietorships PartnershipsMalashaDsouzaNo ratings yet

- Module 1 and 2Document49 pagesModule 1 and 222bba044No ratings yet

- Leadership & Governance (Document33 pagesLeadership & Governance (oforijulius77No ratings yet

- Corporate Law and GovernanceDocument5 pagesCorporate Law and GovernanceShambhavi ChoudharyNo ratings yet

- Corporate Governance IntroductionDocument20 pagesCorporate Governance IntroductionRaviKumarNo ratings yet

- Theory, Practice - CG SummaryDocument31 pagesTheory, Practice - CG SummaryMark K. EapenNo ratings yet

- Corporate Governence .1Document29 pagesCorporate Governence .1AMAN MISHRANo ratings yet

- Issues in Corporate GovernanceDocument15 pagesIssues in Corporate GovernanceVandana ŘwţNo ratings yet

- BBA VI Semester: Business and SocietyDocument15 pagesBBA VI Semester: Business and SocietyChhaya sharmaNo ratings yet

- Corporate GovernanceDocument25 pagesCorporate GovernanceSameer Patro0% (1)

- Corporate Governance: Group - EDocument30 pagesCorporate Governance: Group - Esammi singhNo ratings yet

- Corporate Ethics: By: Raoof Zubair Section B1 FW/9-11 By: Mahoob Pasha HR FW/ 9-11Document26 pagesCorporate Ethics: By: Raoof Zubair Section B1 FW/9-11 By: Mahoob Pasha HR FW/ 9-11Raoof ZubairNo ratings yet

- MCSConcepts Chs 13 - 20mar23Document14 pagesMCSConcepts Chs 13 - 20mar23Elvis TecNo ratings yet

- W2 - Introduction To CGDocument18 pagesW2 - Introduction To CGHelmi ZainonNo ratings yet

- Corporate GovernanceDocument137 pagesCorporate GovernancePriyansh Jindal100% (1)

- BECG PowerPointDocument92 pagesBECG PowerPointHussain NazNo ratings yet

- Class 1 IntroductionDocument39 pagesClass 1 Introduction常超No ratings yet

- Corporate Governance TheoriesDocument11 pagesCorporate Governance TheoriesAnkit JainNo ratings yet

- CG 4th Chapter Family Owned FirmsDocument18 pagesCG 4th Chapter Family Owned FirmsSani DasNo ratings yet

- Unit 5 Class SlidesDocument40 pagesUnit 5 Class SlidesRichard SibekoNo ratings yet

- Besr ReviewerDocument41 pagesBesr ReviewerZabeth villalonNo ratings yet

- 08 Corporate Ethical Governance & Accountability (MTM)Document35 pages08 Corporate Ethical Governance & Accountability (MTM)Sadman Ashiqur RahmanNo ratings yet

- Aspects of Private Law and Corporate Law Blackboard VersionDocument23 pagesAspects of Private Law and Corporate Law Blackboard Versiondwandile12No ratings yet

- Unit2 - BPSM Corporate GovernanceDocument50 pagesUnit2 - BPSM Corporate GovernanceKunal GuptaNo ratings yet

- Becg Corporate Governance:: Notes Complied by Dr. Dhimen Jani Mba, CBS, Pgdibo, PHD MBA Sem. 1Document32 pagesBecg Corporate Governance:: Notes Complied by Dr. Dhimen Jani Mba, CBS, Pgdibo, PHD MBA Sem. 112Twinkal ModiNo ratings yet

- BBA VI Semester: Business and SocietyDocument15 pagesBBA VI Semester: Business and Societysumeet kcNo ratings yet

- Module 3 - BE & CGDocument120 pagesModule 3 - BE & CGMital ParmarNo ratings yet

- Mba 8 Business Ethics & Corporate Governance: Class 1bDocument43 pagesMba 8 Business Ethics & Corporate Governance: Class 1bPragyan NayakNo ratings yet

- BBA VI Semester: Business and SocietyDocument17 pagesBBA VI Semester: Business and SocietyBCom HonsNo ratings yet

- Chapter II Choosing A Form of Business OwnershipDocument36 pagesChapter II Choosing A Form of Business OwnershipTrần Lê NaNo ratings yet

- Lecture 6Document58 pagesLecture 6saad aliNo ratings yet

- Cgri Quick Guide 03 Board Directors Duties LiabilitiesDocument18 pagesCgri Quick Guide 03 Board Directors Duties LiabilitiesGapo Tanim PunoNo ratings yet

- Becg Unit 3Document43 pagesBecg Unit 3boosNo ratings yet

- Introduction of Corporate Governance: Unit-1Document20 pagesIntroduction of Corporate Governance: Unit-1Kusum LataNo ratings yet

- Corporate GovernanceDocument22 pagesCorporate Governancerobinkapoor100% (1)

- Governance, Risk, and EthicsDocument6 pagesGovernance, Risk, and EthicsbhoomailidNo ratings yet

- Corporate Governance: Board and CommitteeDocument3 pagesCorporate Governance: Board and CommitteeAbhishek SinghNo ratings yet

- CORPORATE GOVERNANCE ppt-1Document26 pagesCORPORATE GOVERNANCE ppt-1lakshmiNo ratings yet

- Lesson 13 Future CGDocument33 pagesLesson 13 Future CGfarich09No ratings yet

- Chapter 1 Social Responsibility FrameworkDocument53 pagesChapter 1 Social Responsibility FrameworkbryanbernabeNo ratings yet

- Corporate Governance and Finance (Notes For Exam) 2Document51 pagesCorporate Governance and Finance (Notes For Exam) 2KriyaNo ratings yet

- Ethics ReportDocument39 pagesEthics ReportRuby Rose EntrataNo ratings yet

- Corporate Governance: John Paul Ragandap Lyka Mia QuitorianoDocument26 pagesCorporate Governance: John Paul Ragandap Lyka Mia QuitorianoLyka Mia QuitorianoNo ratings yet

- Lecture 1A - Introduction, Agency and Financial MarketsDocument54 pagesLecture 1A - Introduction, Agency and Financial MarketsJackieNo ratings yet

- Legal and Ethical Dimensions of EntrepreneurshipDocument19 pagesLegal and Ethical Dimensions of EntrepreneurshipsauravNo ratings yet

- Corporate GovernanceDocument21 pagesCorporate GovernanceHardik Patel91% (46)

- Chapter 9 - Corporate GovernanceDocument26 pagesChapter 9 - Corporate GovernanceAdrienne SmithNo ratings yet

- Section 1.4 (Limited Companies & Multinationals)Document20 pagesSection 1.4 (Limited Companies & Multinationals)Ei Shwe Sin PhooNo ratings yet

- Code of Corporate Governance in Emerging Economies - A Case of IndiaDocument29 pagesCode of Corporate Governance in Emerging Economies - A Case of IndiaSabbir MahmoodNo ratings yet

- Corporate Governance Lectures 1Document29 pagesCorporate Governance Lectures 1RewardMaturureNo ratings yet

- ZERO TO MASTERY IN CORPORATE GOVERNANCE: Become Zero To Hero In Corporate Governance, This Book Covers A-Z Corporate Governance Concepts, 2022 Latest EditionFrom EverandZERO TO MASTERY IN CORPORATE GOVERNANCE: Become Zero To Hero In Corporate Governance, This Book Covers A-Z Corporate Governance Concepts, 2022 Latest EditionNo ratings yet

- LLC: A Complete Guide To Limited Liability Companies And Setting Up Your Own LLCFrom EverandLLC: A Complete Guide To Limited Liability Companies And Setting Up Your Own LLCNo ratings yet

- Business Organizations: Outlines and Case Summaries: Law School Survival Guides, #10From EverandBusiness Organizations: Outlines and Case Summaries: Law School Survival Guides, #10No ratings yet

- 8B SA2 CompScMarkListDocument2 pages8B SA2 CompScMarkListAparna SinghNo ratings yet

- CASE-Indian Staffing Industry (SWOT Analysis) : Submitted By: - Aparna Singh - 19021141023 M.B.A. (2019-21)Document6 pagesCASE-Indian Staffing Industry (SWOT Analysis) : Submitted By: - Aparna Singh - 19021141023 M.B.A. (2019-21)Aparna SinghNo ratings yet

- Speculation and Postponement NewDocument7 pagesSpeculation and Postponement NewAparna SinghNo ratings yet

- Untitled DocumentDocument3 pagesUntitled DocumentAparna SinghNo ratings yet

- Aparna Singh: Work ExperienceDocument1 pageAparna Singh: Work ExperienceAparna SinghNo ratings yet

- Marketing Plan l2j 2mmsDocument28 pagesMarketing Plan l2j 2mmsAparna SinghNo ratings yet

- IMC Marketing Cottle Taylor CaseDocument22 pagesIMC Marketing Cottle Taylor CaseAparna SinghNo ratings yet

- Solution of Sarvodaya Samiti Case StudyDocument29 pagesSolution of Sarvodaya Samiti Case StudyAparna SinghNo ratings yet

- 18 Customer Relationship Marketing in The Airline Industry: Reinhold RappDocument2 pages18 Customer Relationship Marketing in The Airline Industry: Reinhold RappAparna SinghNo ratings yet

- Material DA 7Document3 pagesMaterial DA 7Aparna SinghNo ratings yet

- Business Analytics IntroductionDocument8 pagesBusiness Analytics IntroductionAparna SinghNo ratings yet

- BA GROUP ASSIGNMENT 3 (FOR Histogram On Mtcars and Iris)Document21 pagesBA GROUP ASSIGNMENT 3 (FOR Histogram On Mtcars and Iris)Aparna SinghNo ratings yet

- International Business ManagementDocument10 pagesInternational Business Managementmohit jainNo ratings yet

- P8 Financial AnalysisDocument32 pagesP8 Financial AnalysisDhanushka Rajapaksha100% (1)

- IDX Fact Book 2006Document177 pagesIDX Fact Book 2006Anindyajati Sila PranabhaktiNo ratings yet

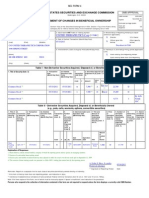

- Sec Form 4 5Document1 pageSec Form 4 5Anonymous Feglbx5No ratings yet

- South Korean Companies Plan To InvestDocument2 pagesSouth Korean Companies Plan To InvestFeby AuliaNo ratings yet

- Finance PracticeDocument6 pagesFinance PracticePriya IBDPexternalNo ratings yet

- (M) Controllable CostsDocument2 pages(M) Controllable CostsdragjoNo ratings yet

- PTTCDN D02 Team-05 Hoa-Sen-GroupDocument61 pagesPTTCDN D02 Team-05 Hoa-Sen-GroupHợp NguyễnNo ratings yet

- Test Series: October, 2019 Mock Test Paper Final (Old) Course: Group - I Paper - 1: Financial ReportingDocument8 pagesTest Series: October, 2019 Mock Test Paper Final (Old) Course: Group - I Paper - 1: Financial ReportingDev ReddyNo ratings yet

- Paper:4 Mock Test-5 MARKS:100Document16 pagesPaper:4 Mock Test-5 MARKS:100Ayathii EducareNo ratings yet

- C3 ValuationDocument26 pagesC3 ValuationMinh Lưu NhậtNo ratings yet

- LatihanDocument12 pagesLatihanSurameto HariyadiNo ratings yet

- Auditing Problems You Can UseDocument51 pagesAuditing Problems You Can UseChinita VirayNo ratings yet

- Barclays CMBS Strategy Weekly Comparing Bookrunners Versus Other Contributors inDocument18 pagesBarclays CMBS Strategy Weekly Comparing Bookrunners Versus Other Contributors inykkwonNo ratings yet

- TN Smart Start Up GuideDocument82 pagesTN Smart Start Up GuideGold SunriseNo ratings yet

- Ratio Analysis Solved ProblemsDocument34 pagesRatio Analysis Solved ProblemsHaroon KhanNo ratings yet

- Canada-China Trade Agreemnt BriefDocument9 pagesCanada-China Trade Agreemnt BriefSujata DeyNo ratings yet

- Ud WirastriDocument18 pagesUd WirastriyumamhrnptrNo ratings yet

- Question #2: A. Both The Current and Acid-Test Ratios. B. Only The Current RatioDocument11 pagesQuestion #2: A. Both The Current and Acid-Test Ratios. B. Only The Current Ratioiceman2167No ratings yet

- ABM 1 Q1-Week 8 For Teacher1Document14 pagesABM 1 Q1-Week 8 For Teacher1Kassandra Kay De Roxas100% (2)

- BL-A2-Hữu KhảiDocument40 pagesBL-A2-Hữu KhảiHữu KhảiNo ratings yet

- Fysal BankDocument48 pagesFysal BankAnoosha Abbas SheikhNo ratings yet

- CH4 David SMCC16ge Ppt04Document41 pagesCH4 David SMCC16ge Ppt04Yanty IbrahimNo ratings yet

- Indian Bank Investment Note - QIPDocument5 pagesIndian Bank Investment Note - QIPAyushi somaniNo ratings yet

- Assessment 5-m1 de Mesakk Con15 ReferencesDocument2 pagesAssessment 5-m1 de Mesakk Con15 Referencesdemesakathleen2105No ratings yet

- Indiabulls Dual Advantage Commercial Asset Fund FebDocument40 pagesIndiabulls Dual Advantage Commercial Asset Fund FebLijo John100% (2)

- CIHB - Annual Report 2022Document120 pagesCIHB - Annual Report 2022siranepNo ratings yet