The Accounting Cycle Continued - Preparing Worksheets and Financial Statements

The Accounting Cycle Continued - Preparing Worksheets and Financial Statements

You might also like

- Heagy and Lehmann Accounting Information SystemDocument53 pagesHeagy and Lehmann Accounting Information SystemVal Mercury Faburada100% (1)

- Mid Term IDocument10 pagesMid Term Ichaos1989No ratings yet

- US Army Identification of Ammunition CourseDocument90 pagesUS Army Identification of Ammunition Courselygore100% (2)

- Managerial Accounting 15th Ed. GNB - Chapter 6 Variable CostingDocument11 pagesManagerial Accounting 15th Ed. GNB - Chapter 6 Variable CostingAivie PangilinanNo ratings yet

- BAM 127 Day 11 - TGDocument8 pagesBAM 127 Day 11 - TGPaulo BelenNo ratings yet

- The Simplex Method MaximizationDocument21 pagesThe Simplex Method MaximizationJohn Rovic GamanaNo ratings yet

- Year 1Document15 pagesYear 1James De TorresNo ratings yet

- FAR - Chapter 8Document3 pagesFAR - Chapter 8Jynilou PinoteNo ratings yet

- Transaction Type of Transaction Effect Journal EntryDocument4 pagesTransaction Type of Transaction Effect Journal EntryDonabelle MarimonNo ratings yet

- Post Quiz Chapter 10Document1 pagePost Quiz Chapter 10joanna supresenciaNo ratings yet

- Chart of Accounts General Ledger General Ledger Page No. Page No. Assets IncomeDocument44 pagesChart of Accounts General Ledger General Ledger Page No. Page No. Assets IncomeJireh RiveraNo ratings yet

- Chapter 5 Financial Statement Analysis 1Document3 pagesChapter 5 Financial Statement Analysis 1Syrill CayetanoNo ratings yet

- Quiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeDocument6 pagesQuiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeJOHN MITCHELL GALLARDONo ratings yet

- Expanded Accounting EquationDocument18 pagesExpanded Accounting EquationBelen GonzalesNo ratings yet

- Individual Income Tax ComputationsDocument13 pagesIndividual Income Tax ComputationsclarizaNo ratings yet

- Taxation May Board ExamDocument25 pagesTaxation May Board ExamjaysonNo ratings yet

- Certified Bookkeeper Program: January 12, 19, 26 and February 2, 2007 ADB Ave. OrtigasDocument63 pagesCertified Bookkeeper Program: January 12, 19, 26 and February 2, 2007 ADB Ave. OrtigasAllen CarlNo ratings yet

- Writing Up A Case StudyDocument3 pagesWriting Up A Case StudyalliahnahNo ratings yet

- Pas 10 - SummaryDocument1 pagePas 10 - SummaryBirdWin WinNo ratings yet

- Lecture : Day 1: Adjusting Entries & Chart of Accounts (Periodic & Perpetual)Document7 pagesLecture : Day 1: Adjusting Entries & Chart of Accounts (Periodic & Perpetual)khrysna ayra villanuevaNo ratings yet

- Qualifying Exam Review Qs Final Answers2Document30 pagesQualifying Exam Review Qs Final Answers2sunq hccnNo ratings yet

- Chapter 1 Statement of Financial PositionDocument3 pagesChapter 1 Statement of Financial PositionMartha Nicole MaristelaNo ratings yet

- ACCO Module 2Document5 pagesACCO Module 2Lala BoraNo ratings yet

- Module 1 SCMDocument19 pagesModule 1 SCMDummy AccNo ratings yet

- Overview of Philippine Financial Reporting Standards 9 (PFRS 9)Document4 pagesOverview of Philippine Financial Reporting Standards 9 (PFRS 9)Earl John ROSALESNo ratings yet

- 85184767Document9 pages85184767Garp BarrocaNo ratings yet

- 01 Activity 2Document4 pages01 Activity 2Laisan SantosNo ratings yet

- Week 2 - Lesson 2 The Accounting ProcessDocument16 pagesWeek 2 - Lesson 2 The Accounting ProcessRose RaboNo ratings yet

- PFRS 1 - FIRST-TIME ADOPTION OF PFRSsDocument10 pagesPFRS 1 - FIRST-TIME ADOPTION OF PFRSsHannah TaduranNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument2 pagesAccounting Cycle of A Merchandising BusinessAnne Alag100% (1)

- Chapter 06-Sales Mix and ICPDocument11 pagesChapter 06-Sales Mix and ICPbbckk1No ratings yet

- Intacc 1Document17 pagesIntacc 1Xyza Faye RegaladoNo ratings yet

- II. Multiple Choice.: Archdiocese of TuguegaraoDocument3 pagesII. Multiple Choice.: Archdiocese of TuguegaraoRamojifly LinganNo ratings yet

- CAT Exam 1 1Document5 pagesCAT Exam 1 1YeppeuddaNo ratings yet

- Closing EntriesDocument14 pagesClosing EntriesAlbert Moreno100% (1)

- Comprehensive Illustrative ProblemDocument2 pagesComprehensive Illustrative ProblemLyssa Marie Avenido GuelosNo ratings yet

- 2.0assessment ExamDocument2 pages2.0assessment ExamyeshaNo ratings yet

- Job Order CostingDocument1 pageJob Order CostingVincent Pham100% (1)

- Adjusting Entries For Bad DebtsDocument6 pagesAdjusting Entries For Bad DebtsKristine IvyNo ratings yet

- Finals Non Graded Exercises 002 - Journalizing Under Mechandising Concern With Vat Page 28Document6 pagesFinals Non Graded Exercises 002 - Journalizing Under Mechandising Concern With Vat Page 28Garpt KudasaiNo ratings yet

- Merchandising Accounting Cycle: Periodic: Subject-Descriptive Title Subject - CodeDocument22 pagesMerchandising Accounting Cycle: Periodic: Subject-Descriptive Title Subject - CodeRose LaureanoNo ratings yet

- Adjusting Entries PracticeDocument11 pagesAdjusting Entries Practiceback4peaceNo ratings yet

- Gapminder WebsiteDocument2 pagesGapminder WebsitejenieNo ratings yet

- CosAcc Unit 1 Introduction PDFDocument13 pagesCosAcc Unit 1 Introduction PDFKrisha NicoleNo ratings yet

- Philippine Financial Reporting Standards: Number TitleDocument4 pagesPhilippine Financial Reporting Standards: Number TitleAlexis AlipudoNo ratings yet

- Completing The Accounting Cycle: Service Concern: Subject-Descriptive Title Subject - CodeDocument12 pagesCompleting The Accounting Cycle: Service Concern: Subject-Descriptive Title Subject - CodeRose LaureanoNo ratings yet

- Table of ContentsDocument1 pageTable of ContentsJohn Rey EnriquezNo ratings yet

- Ourladyoffatimauniversity: The Problem and ItDocument19 pagesOurladyoffatimauniversity: The Problem and ItOwen PacenioNo ratings yet

- Accounting Cycle of A Service Business-Step 4-Trial BalanceDocument30 pagesAccounting Cycle of A Service Business-Step 4-Trial BalancedelgadojudithNo ratings yet

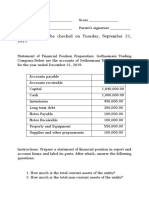

- Answer This To Be Checked On Tuesday, September 21, 2021Document2 pagesAnswer This To Be Checked On Tuesday, September 21, 2021Teresa Mae OrquiaNo ratings yet

- Accounting Concepts and PrinciplesDocument4 pagesAccounting Concepts and Principlesdane alvarezNo ratings yet

- Standard Costing & Variance AnalysisDocument10 pagesStandard Costing & Variance AnalysisMariella Antonio-NarsicoNo ratings yet

- FINMAN Cash-Flow-Analysis-Practice-Problem-2Document2 pagesFINMAN Cash-Flow-Analysis-Practice-Problem-2stel mariNo ratings yet

- Chapter OneDocument5 pagesChapter OneHazraphine LinsoNo ratings yet

- Pfrs 1: First Time Adoption of PfrsDocument12 pagesPfrs 1: First Time Adoption of PfrsZeo AlcantaraNo ratings yet

- q4 Abm Fundamentals of Abm1 11 Week 3Document6 pagesq4 Abm Fundamentals of Abm1 11 Week 3Judy Ann Villanueva100% (1)

- Accounting ReviewerDocument7 pagesAccounting ReviewerJaphet RiveraNo ratings yet

- Concept of Income (Gross Income) - Ref CEU School of Business and ManagementDocument61 pagesConcept of Income (Gross Income) - Ref CEU School of Business and ManagementMeden Robrigado-LabogNo ratings yet

- Enclosure 1. Teacher-Made Learner's Home Task (Week 9) : The Nature of A Service BusinessDocument7 pagesEnclosure 1. Teacher-Made Learner's Home Task (Week 9) : The Nature of A Service BusinessKim FloresNo ratings yet

- Accounting Principles: Second Canadian EditionDocument75 pagesAccounting Principles: Second Canadian EditionMuhammad AfzalNo ratings yet

- District Profile ThattaDocument52 pagesDistrict Profile ThattaUrooj Fatima100% (1)

- Notes Industrial Security ConceptsDocument40 pagesNotes Industrial Security ConceptsAC GonzagaNo ratings yet

- BIMDocument15 pagesBIMAhmed AbdelMaksoud100% (1)

- Info 15614 - 2017Document34 pagesInfo 15614 - 2017uğur özdemirNo ratings yet

- Power Calculation Drum MotorsDocument2 pagesPower Calculation Drum MotorsFitra VertikalNo ratings yet

- Compressed Gas Cylinder Safety GuideDocument1 pageCompressed Gas Cylinder Safety GuideNguyenLinh27No ratings yet

- PregnylDocument4 pagesPregnylAdina DraghiciNo ratings yet

- Hospitals Emails PKDocument4 pagesHospitals Emails PKEngr Hamid AliNo ratings yet

- Knightcorp 20170330 Invoice - Idathletic - 37412Document4 pagesKnightcorp 20170330 Invoice - Idathletic - 37412Michael FarnellNo ratings yet

- Michael Porter's: Five Forces ModelDocument17 pagesMichael Porter's: Five Forces ModelBindu MalviyaNo ratings yet

- Market Development ReportDocument121 pagesMarket Development ReportSrivinayaga XNo ratings yet

- Resume Juan Pablo Garc°a de Presno HRBP DirectorDocument3 pagesResume Juan Pablo Garc°a de Presno HRBP DirectorLuis Fernando QuiroaNo ratings yet

- Sales ManagementDocument26 pagesSales ManagementBenita S MonicaNo ratings yet

- T14 CalculatorDocument5 pagesT14 CalculatorUsamaNo ratings yet

- Depth-First Search: COMP171 Fall 2005Document27 pagesDepth-First Search: COMP171 Fall 2005Praveen KumarNo ratings yet

- 02 Energy Harvesting For Aut. SystemsDocument304 pages02 Energy Harvesting For Aut. SystemsJúlio Véras100% (2)

- Piping SystemsDocument137 pagesPiping SystemsSwapnil KoshtiNo ratings yet

- Acquistion of Jaguar Land Rover by Tata MotorsDocument9 pagesAcquistion of Jaguar Land Rover by Tata Motorsajinkya8400No ratings yet

- Lovato 2013Document5 pagesLovato 2013AjaNo ratings yet

- Lexical and Syntax Analysis: TopicsDocument5 pagesLexical and Syntax Analysis: TopicsReshma PiseNo ratings yet

- Water PollutionDocument36 pagesWater PollutionAgnivesh MangalNo ratings yet

- Study Guide: Reading Comprehension & Sample Test QuestionsDocument12 pagesStudy Guide: Reading Comprehension & Sample Test QuestionsRhymer Indico MendozaNo ratings yet

- Rift Valley University: Department: - Weekend Computer ScienceDocument13 pagesRift Valley University: Department: - Weekend Computer ScienceAyele MitkuNo ratings yet

- TW Supplement WSA 02-2002 V2 3 MRWA - DRAFT 05 Sewerage CodeDocument35 pagesTW Supplement WSA 02-2002 V2 3 MRWA - DRAFT 05 Sewerage CodeDivesh rahulNo ratings yet

- Third Periodical Test in Mathematics 7: Violeta Integrated SchoolDocument4 pagesThird Periodical Test in Mathematics 7: Violeta Integrated SchoolWerty Gigz DurendezNo ratings yet

- Chapter Three Edited - Public EnterpriseDocument9 pagesChapter Three Edited - Public EnterpriseMarah Moses BallaNo ratings yet

- PDF File Rites of The Lock-Picking With Surgat Lapaca by AftahhDocument7 pagesPDF File Rites of The Lock-Picking With Surgat Lapaca by AftahhvrsNo ratings yet

- Water Tank Design CalcDocument5 pagesWater Tank Design CalcUttam Kumar Ghosh100% (1)

- Inergen System Operation and Maintenance InstructionDocument16 pagesInergen System Operation and Maintenance InstructionchuminhNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Heagy and Lehmann Accounting Information SystemDocument53 pagesHeagy and Lehmann Accounting Information SystemVal Mercury Faburada100% (1)

- Mid Term IDocument10 pagesMid Term Ichaos1989No ratings yet

- US Army Identification of Ammunition CourseDocument90 pagesUS Army Identification of Ammunition Courselygore100% (2)

- Managerial Accounting 15th Ed. GNB - Chapter 6 Variable CostingDocument11 pagesManagerial Accounting 15th Ed. GNB - Chapter 6 Variable CostingAivie PangilinanNo ratings yet

- BAM 127 Day 11 - TGDocument8 pagesBAM 127 Day 11 - TGPaulo BelenNo ratings yet

- The Simplex Method MaximizationDocument21 pagesThe Simplex Method MaximizationJohn Rovic GamanaNo ratings yet

- Year 1Document15 pagesYear 1James De TorresNo ratings yet

- FAR - Chapter 8Document3 pagesFAR - Chapter 8Jynilou PinoteNo ratings yet

- Transaction Type of Transaction Effect Journal EntryDocument4 pagesTransaction Type of Transaction Effect Journal EntryDonabelle MarimonNo ratings yet

- Post Quiz Chapter 10Document1 pagePost Quiz Chapter 10joanna supresenciaNo ratings yet

- Chart of Accounts General Ledger General Ledger Page No. Page No. Assets IncomeDocument44 pagesChart of Accounts General Ledger General Ledger Page No. Page No. Assets IncomeJireh RiveraNo ratings yet

- Chapter 5 Financial Statement Analysis 1Document3 pagesChapter 5 Financial Statement Analysis 1Syrill CayetanoNo ratings yet

- Quiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeDocument6 pagesQuiz No. 7: A. MULTIPLE CHOICE: Write The Correct Letter Choice BeforeJOHN MITCHELL GALLARDONo ratings yet

- Expanded Accounting EquationDocument18 pagesExpanded Accounting EquationBelen GonzalesNo ratings yet

- Individual Income Tax ComputationsDocument13 pagesIndividual Income Tax ComputationsclarizaNo ratings yet

- Taxation May Board ExamDocument25 pagesTaxation May Board ExamjaysonNo ratings yet

- Certified Bookkeeper Program: January 12, 19, 26 and February 2, 2007 ADB Ave. OrtigasDocument63 pagesCertified Bookkeeper Program: January 12, 19, 26 and February 2, 2007 ADB Ave. OrtigasAllen CarlNo ratings yet

- Writing Up A Case StudyDocument3 pagesWriting Up A Case StudyalliahnahNo ratings yet

- Pas 10 - SummaryDocument1 pagePas 10 - SummaryBirdWin WinNo ratings yet

- Lecture : Day 1: Adjusting Entries & Chart of Accounts (Periodic & Perpetual)Document7 pagesLecture : Day 1: Adjusting Entries & Chart of Accounts (Periodic & Perpetual)khrysna ayra villanuevaNo ratings yet

- Qualifying Exam Review Qs Final Answers2Document30 pagesQualifying Exam Review Qs Final Answers2sunq hccnNo ratings yet

- Chapter 1 Statement of Financial PositionDocument3 pagesChapter 1 Statement of Financial PositionMartha Nicole MaristelaNo ratings yet

- ACCO Module 2Document5 pagesACCO Module 2Lala BoraNo ratings yet

- Module 1 SCMDocument19 pagesModule 1 SCMDummy AccNo ratings yet

- Overview of Philippine Financial Reporting Standards 9 (PFRS 9)Document4 pagesOverview of Philippine Financial Reporting Standards 9 (PFRS 9)Earl John ROSALESNo ratings yet

- 85184767Document9 pages85184767Garp BarrocaNo ratings yet

- 01 Activity 2Document4 pages01 Activity 2Laisan SantosNo ratings yet

- Week 2 - Lesson 2 The Accounting ProcessDocument16 pagesWeek 2 - Lesson 2 The Accounting ProcessRose RaboNo ratings yet

- PFRS 1 - FIRST-TIME ADOPTION OF PFRSsDocument10 pagesPFRS 1 - FIRST-TIME ADOPTION OF PFRSsHannah TaduranNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument2 pagesAccounting Cycle of A Merchandising BusinessAnne Alag100% (1)

- Chapter 06-Sales Mix and ICPDocument11 pagesChapter 06-Sales Mix and ICPbbckk1No ratings yet

- Intacc 1Document17 pagesIntacc 1Xyza Faye RegaladoNo ratings yet

- II. Multiple Choice.: Archdiocese of TuguegaraoDocument3 pagesII. Multiple Choice.: Archdiocese of TuguegaraoRamojifly LinganNo ratings yet

- CAT Exam 1 1Document5 pagesCAT Exam 1 1YeppeuddaNo ratings yet

- Closing EntriesDocument14 pagesClosing EntriesAlbert Moreno100% (1)

- Comprehensive Illustrative ProblemDocument2 pagesComprehensive Illustrative ProblemLyssa Marie Avenido GuelosNo ratings yet

- 2.0assessment ExamDocument2 pages2.0assessment ExamyeshaNo ratings yet

- Job Order CostingDocument1 pageJob Order CostingVincent Pham100% (1)

- Adjusting Entries For Bad DebtsDocument6 pagesAdjusting Entries For Bad DebtsKristine IvyNo ratings yet

- Finals Non Graded Exercises 002 - Journalizing Under Mechandising Concern With Vat Page 28Document6 pagesFinals Non Graded Exercises 002 - Journalizing Under Mechandising Concern With Vat Page 28Garpt KudasaiNo ratings yet

- Merchandising Accounting Cycle: Periodic: Subject-Descriptive Title Subject - CodeDocument22 pagesMerchandising Accounting Cycle: Periodic: Subject-Descriptive Title Subject - CodeRose LaureanoNo ratings yet

- Adjusting Entries PracticeDocument11 pagesAdjusting Entries Practiceback4peaceNo ratings yet

- Gapminder WebsiteDocument2 pagesGapminder WebsitejenieNo ratings yet

- CosAcc Unit 1 Introduction PDFDocument13 pagesCosAcc Unit 1 Introduction PDFKrisha NicoleNo ratings yet

- Philippine Financial Reporting Standards: Number TitleDocument4 pagesPhilippine Financial Reporting Standards: Number TitleAlexis AlipudoNo ratings yet

- Completing The Accounting Cycle: Service Concern: Subject-Descriptive Title Subject - CodeDocument12 pagesCompleting The Accounting Cycle: Service Concern: Subject-Descriptive Title Subject - CodeRose LaureanoNo ratings yet

- Table of ContentsDocument1 pageTable of ContentsJohn Rey EnriquezNo ratings yet

- Ourladyoffatimauniversity: The Problem and ItDocument19 pagesOurladyoffatimauniversity: The Problem and ItOwen PacenioNo ratings yet

- Accounting Cycle of A Service Business-Step 4-Trial BalanceDocument30 pagesAccounting Cycle of A Service Business-Step 4-Trial BalancedelgadojudithNo ratings yet

- Answer This To Be Checked On Tuesday, September 21, 2021Document2 pagesAnswer This To Be Checked On Tuesday, September 21, 2021Teresa Mae OrquiaNo ratings yet

- Accounting Concepts and PrinciplesDocument4 pagesAccounting Concepts and Principlesdane alvarezNo ratings yet

- Standard Costing & Variance AnalysisDocument10 pagesStandard Costing & Variance AnalysisMariella Antonio-NarsicoNo ratings yet

- FINMAN Cash-Flow-Analysis-Practice-Problem-2Document2 pagesFINMAN Cash-Flow-Analysis-Practice-Problem-2stel mariNo ratings yet

- Chapter OneDocument5 pagesChapter OneHazraphine LinsoNo ratings yet

- Pfrs 1: First Time Adoption of PfrsDocument12 pagesPfrs 1: First Time Adoption of PfrsZeo AlcantaraNo ratings yet

- q4 Abm Fundamentals of Abm1 11 Week 3Document6 pagesq4 Abm Fundamentals of Abm1 11 Week 3Judy Ann Villanueva100% (1)

- Accounting ReviewerDocument7 pagesAccounting ReviewerJaphet RiveraNo ratings yet

- Concept of Income (Gross Income) - Ref CEU School of Business and ManagementDocument61 pagesConcept of Income (Gross Income) - Ref CEU School of Business and ManagementMeden Robrigado-LabogNo ratings yet

- Enclosure 1. Teacher-Made Learner's Home Task (Week 9) : The Nature of A Service BusinessDocument7 pagesEnclosure 1. Teacher-Made Learner's Home Task (Week 9) : The Nature of A Service BusinessKim FloresNo ratings yet

- Accounting Principles: Second Canadian EditionDocument75 pagesAccounting Principles: Second Canadian EditionMuhammad AfzalNo ratings yet

- District Profile ThattaDocument52 pagesDistrict Profile ThattaUrooj Fatima100% (1)

- Notes Industrial Security ConceptsDocument40 pagesNotes Industrial Security ConceptsAC GonzagaNo ratings yet

- BIMDocument15 pagesBIMAhmed AbdelMaksoud100% (1)

- Info 15614 - 2017Document34 pagesInfo 15614 - 2017uğur özdemirNo ratings yet

- Power Calculation Drum MotorsDocument2 pagesPower Calculation Drum MotorsFitra VertikalNo ratings yet

- Compressed Gas Cylinder Safety GuideDocument1 pageCompressed Gas Cylinder Safety GuideNguyenLinh27No ratings yet

- PregnylDocument4 pagesPregnylAdina DraghiciNo ratings yet

- Hospitals Emails PKDocument4 pagesHospitals Emails PKEngr Hamid AliNo ratings yet

- Knightcorp 20170330 Invoice - Idathletic - 37412Document4 pagesKnightcorp 20170330 Invoice - Idathletic - 37412Michael FarnellNo ratings yet

- Michael Porter's: Five Forces ModelDocument17 pagesMichael Porter's: Five Forces ModelBindu MalviyaNo ratings yet

- Market Development ReportDocument121 pagesMarket Development ReportSrivinayaga XNo ratings yet

- Resume Juan Pablo Garc°a de Presno HRBP DirectorDocument3 pagesResume Juan Pablo Garc°a de Presno HRBP DirectorLuis Fernando QuiroaNo ratings yet

- Sales ManagementDocument26 pagesSales ManagementBenita S MonicaNo ratings yet

- T14 CalculatorDocument5 pagesT14 CalculatorUsamaNo ratings yet

- Depth-First Search: COMP171 Fall 2005Document27 pagesDepth-First Search: COMP171 Fall 2005Praveen KumarNo ratings yet

- 02 Energy Harvesting For Aut. SystemsDocument304 pages02 Energy Harvesting For Aut. SystemsJúlio Véras100% (2)

- Piping SystemsDocument137 pagesPiping SystemsSwapnil KoshtiNo ratings yet

- Acquistion of Jaguar Land Rover by Tata MotorsDocument9 pagesAcquistion of Jaguar Land Rover by Tata Motorsajinkya8400No ratings yet

- Lovato 2013Document5 pagesLovato 2013AjaNo ratings yet

- Lexical and Syntax Analysis: TopicsDocument5 pagesLexical and Syntax Analysis: TopicsReshma PiseNo ratings yet

- Water PollutionDocument36 pagesWater PollutionAgnivesh MangalNo ratings yet

- Study Guide: Reading Comprehension & Sample Test QuestionsDocument12 pagesStudy Guide: Reading Comprehension & Sample Test QuestionsRhymer Indico MendozaNo ratings yet

- Rift Valley University: Department: - Weekend Computer ScienceDocument13 pagesRift Valley University: Department: - Weekend Computer ScienceAyele MitkuNo ratings yet

- TW Supplement WSA 02-2002 V2 3 MRWA - DRAFT 05 Sewerage CodeDocument35 pagesTW Supplement WSA 02-2002 V2 3 MRWA - DRAFT 05 Sewerage CodeDivesh rahulNo ratings yet

- Third Periodical Test in Mathematics 7: Violeta Integrated SchoolDocument4 pagesThird Periodical Test in Mathematics 7: Violeta Integrated SchoolWerty Gigz DurendezNo ratings yet

- Chapter Three Edited - Public EnterpriseDocument9 pagesChapter Three Edited - Public EnterpriseMarah Moses BallaNo ratings yet

- PDF File Rites of The Lock-Picking With Surgat Lapaca by AftahhDocument7 pagesPDF File Rites of The Lock-Picking With Surgat Lapaca by AftahhvrsNo ratings yet

- Water Tank Design CalcDocument5 pagesWater Tank Design CalcUttam Kumar Ghosh100% (1)

- Inergen System Operation and Maintenance InstructionDocument16 pagesInergen System Operation and Maintenance InstructionchuminhNo ratings yet