Download as pptx, pdf, or txt

You might also like

- NR EditedDocument46 pagesNR Editedirish59% (22)

- Case 7 SolutionsDocument3 pagesCase 7 SolutionsMichale Jacomilla50% (2)

- Bendijo, Bjay J. BSA 2-2: Cebu Pacific Porter's Five ForcesDocument1 pageBendijo, Bjay J. BSA 2-2: Cebu Pacific Porter's Five ForcesChen HaoNo ratings yet

- INSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyDocument15 pagesINSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyMendoza Ron NixonNo ratings yet

- Revised IFRS 16 Lease Math 1, 2Document8 pagesRevised IFRS 16 Lease Math 1, 2Feruz Sha Rakin100% (1)

- Acctbis PDFDocument2 pagesAcctbis PDFJessica C. DelaneyNo ratings yet

- Ia CH 6 & 7 NR LR 2020Document112 pagesIa CH 6 & 7 NR LR 2020Jm Sevalla57% (14)

- Unit 3: Completing Accounting CycleDocument22 pagesUnit 3: Completing Accounting CycleChen HaoNo ratings yet

- Cost-Acctg-Page49-53Document5 pagesCost-Acctg-Page49-53Chen Hao50% (2)

- Justification LetterDocument3 pagesJustification LetterAl-husaynLaoSanguilaNo ratings yet

- ROGEN AssignmentDocument9 pagesROGEN AssignmentRogen Paul GeromoNo ratings yet

- Solutions - LiabilitiesDocument10 pagesSolutions - LiabilitiesjhobsNo ratings yet

- Introduction To Financial ManagementDocument12 pagesIntroduction To Financial Managementjuguzman2020No ratings yet

- Nfjpia Cup - Auditing Problems SGV & Co. Easy Question #1: Answer: P126,816Document18 pagesNfjpia Cup - Auditing Problems SGV & Co. Easy Question #1: Answer: P126,816Merliza Jusayan100% (1)

- Chap 3 & 4 Handout V2015Document12 pagesChap 3 & 4 Handout V2015Julz JuliaNo ratings yet

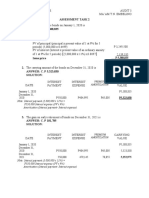

- Assessment Task 3Document5 pagesAssessment Task 3Christian N MagsinoNo ratings yet

- Solution - IntangiblesDocument9 pagesSolution - IntangiblesjhobsNo ratings yet

- Nolong, Hannah Mei L.-5Document8 pagesNolong, Hannah Mei L.-5Hannah NolongNo ratings yet

- Notes ReceivableDocument6 pagesNotes ReceivableRena Jocelle NalzaroNo ratings yet

- Practice-Exercises-Chapters-17-19 2Document5 pagesPractice-Exercises-Chapters-17-19 2Queenie Mae ArsuloNo ratings yet

- Notes in Term Bonds and Serial Bonds (Discount or Premium)Document12 pagesNotes in Term Bonds and Serial Bonds (Discount or Premium)Jae GrandeNo ratings yet

- 5 Investment AccountsDocument11 pages5 Investment AccountsBAZINGANo ratings yet

- LiabilitiesDocument2 pagesLiabilitiesCattleya0% (1)

- Audit of Liabilities. REVIEWDocument3 pagesAudit of Liabilities. REVIEWCattleyaNo ratings yet

- PQ3 BondsDocument2 pagesPQ3 BondsElla Mae MagbatoNo ratings yet

- This Study Resource WasDocument7 pagesThis Study Resource WasxagocipNo ratings yet

- Solution - Shareholders' EquityDocument14 pagesSolution - Shareholders' EquityjhobsNo ratings yet

- This Study Resource Was: Logo HereDocument5 pagesThis Study Resource Was: Logo HereMarcus MonocayNo ratings yet

- ACCTG1 PrefinalsDocument23 pagesACCTG1 PrefinalsJAN RAY CUISON VISPERAS100% (1)

- Ca5101 Adjusting Entries La 1Document13 pagesCa5101 Adjusting Entries La 1Michael MagdaogNo ratings yet

- January 1, 2020 P5,388,835 December 31, 2020 P550,000 P484,995 P65,005Document7 pagesJanuary 1, 2020 P5,388,835 December 31, 2020 P550,000 P484,995 P65,005gazer beamNo ratings yet

- Week 4 AssignmentDocument6 pagesWeek 4 AssignmentJames Bradley HuangNo ratings yet

- Fair Value of Bonds at December 31, 2019 5,250,000 Carrying Value of Bonds at December 31, 2019 4,600,000Document2 pagesFair Value of Bonds at December 31, 2019 5,250,000 Carrying Value of Bonds at December 31, 2019 4,600,000Gray JavierNo ratings yet

- ACC 211 Week 10-12Document24 pagesACC 211 Week 10-12idontcaree123312No ratings yet

- Adjusting Entries Christine Gamba CargoDocument5 pagesAdjusting Entries Christine Gamba Cargoelma wagwag100% (2)

- Examination About Investment 14Document3 pagesExamination About Investment 14BLACKPINKLisaRoseJisooJennieNo ratings yet

- Acquisition & Interest Date Interest Earned (NR X Face) A Interest Income (ER X BV) B Discount Amortization A-B Book Value 07/01/14 12/31/14 12/31/15Document3 pagesAcquisition & Interest Date Interest Earned (NR X Face) A Interest Income (ER X BV) B Discount Amortization A-B Book Value 07/01/14 12/31/14 12/31/15Gray JavierNo ratings yet

- Prof: John Bo S.Cayetano, Cpa, Mba Assessment For BONDS #01Document2 pagesProf: John Bo S.Cayetano, Cpa, Mba Assessment For BONDS #01John FloresNo ratings yet

- Module 5 Note Payable and Debt RestructureDocument15 pagesModule 5 Note Payable and Debt Restructuremmh100% (1)

- Part 2 - Leases (Accounting by Lessors)Document31 pagesPart 2 - Leases (Accounting by Lessors)Poru SenpiiNo ratings yet

- Liabilities Part 2Document43 pagesLiabilities Part 2Luisa Janelle BoquirenNo ratings yet

- Accounting 1Document10 pagesAccounting 1Jay EbuenNo ratings yet

- LT Debts Scenarios W Suggested AnswersDocument3 pagesLT Debts Scenarios W Suggested Answerskeisha santosNo ratings yet

- Investment in Bonds Diagnostic QuizzerDocument6 pagesInvestment in Bonds Diagnostic QuizzerJoefrey Pujadas BalumaNo ratings yet

- Loans Receivable Practice (Review)Document6 pagesLoans Receivable Practice (Review)Deviline MichelleNo ratings yet

- Prof. Elect 4 Lecture On CID 1Document8 pagesProf. Elect 4 Lecture On CID 1Jedidiah ManglicmotNo ratings yet

- Solution Intacc QuizDocument2 pagesSolution Intacc QuizMARIA THERESA AZURESNo ratings yet

- Bonds Payable HandoutDocument8 pagesBonds Payable HandoutJOHANNANo ratings yet

- Q.3-Question and SolutionDocument4 pagesQ.3-Question and SolutionFIROZ KHANNo ratings yet

- Module - IA Chapter 6Document10 pagesModule - IA Chapter 6Kathleen EbuenNo ratings yet

- IFRS 16 Lease MathDocument2 pagesIFRS 16 Lease MathFeruz Sha RakinNo ratings yet

- Set A Leases Problem SERANADocument6 pagesSet A Leases Problem SERANASherri BonquinNo ratings yet

- Handout Investment in Debt SecuritiesDocument28 pagesHandout Investment in Debt SecuritiesTsukishima KeiNo ratings yet

- Exercise Chapter 14Document9 pagesExercise Chapter 14hassah fahadNo ratings yet

- Exercise Chapter 14Document9 pagesExercise Chapter 14hassah fahadNo ratings yet

- Week 06 - 01 - Module 13 - Effective Interest MethodDocument14 pagesWeek 06 - 01 - Module 13 - Effective Interest Method지마리No ratings yet

- LT Debts Scenarios W Suggested AnswersDocument4 pagesLT Debts Scenarios W Suggested AnswersSam SalvadorNo ratings yet

- Examination About Investment 16Document2 pagesExamination About Investment 16BLACKPINKLisaRoseJisooJennieNo ratings yet

- Effective Interest MethodDocument31 pagesEffective Interest MethodMikaela LacabaNo ratings yet

- Accounting QuestionsDocument9 pagesAccounting QuestionsChabby ChabbyNo ratings yet

- Chapter 28 LeaseDocument5 pagesChapter 28 LeaseGelmar GloriaNo ratings yet

- DUAZO - 6th EXAM SIM ANSWERSDocument7 pagesDUAZO - 6th EXAM SIM ANSWERSJeric TorionNo ratings yet

- Real Estate Investing 101: Best Way to Buy a House and Save Big, Top 20 TipsFrom EverandReal Estate Investing 101: Best Way to Buy a House and Save Big, Top 20 TipsNo ratings yet

- Renewable energy finance: Green bondsFrom EverandRenewable energy finance: Green bondsNo ratings yet

- Choosing Nutritious FoodDocument13 pagesChoosing Nutritious FoodChen Hao100% (1)

- Weekly Home Learning Plan: What's in (pp.2Document1 pageWeekly Home Learning Plan: What's in (pp.2Chen Hao100% (1)

- Module 1-4 Acctg Ed 16 BSADocument18 pagesModule 1-4 Acctg Ed 16 BSAChen HaoNo ratings yet

- Acctg. Ed 1 - Module 10 Accounting Cycle of A Merchandising BusinessDocument35 pagesAcctg. Ed 1 - Module 10 Accounting Cycle of A Merchandising BusinessChen Hao100% (1)

- Essay About Nature of NumbersDocument1 pageEssay About Nature of NumbersChen HaoNo ratings yet

- Acctg. Ed 1 - Module5Document11 pagesAcctg. Ed 1 - Module5Chen HaoNo ratings yet

- Unit 2: General Concepts and Principles of AccountingDocument12 pagesUnit 2: General Concepts and Principles of AccountingChen HaoNo ratings yet

- Lecture On FunctionsDocument4 pagesLecture On FunctionsChen HaoNo ratings yet

- Definition of Statistics: ExamplesDocument60 pagesDefinition of Statistics: ExamplesChen HaoNo ratings yet

- MATH 1. Module 4.aldrinDocument58 pagesMATH 1. Module 4.aldrinChen HaoNo ratings yet

- MATH 1.syllabusDocument9 pagesMATH 1.syllabusChen HaoNo ratings yet

- Cost Assignment Is The Process of Assigning Costs To Cost Pools or From Cost Pools ToDocument4 pagesCost Assignment Is The Process of Assigning Costs To Cost Pools or From Cost Pools ToChen HaoNo ratings yet

- Math 1. Unit 1.module 1-2Document25 pagesMath 1. Unit 1.module 1-2Chen HaoNo ratings yet

- Module 1a - Cash & CEDocument36 pagesModule 1a - Cash & CEChen HaoNo ratings yet

- Module 1b - Bank ReconDocument37 pagesModule 1b - Bank ReconChen HaoNo ratings yet

- Module 2b Allowance For Bad DebtsDocument14 pagesModule 2b Allowance For Bad DebtsChen HaoNo ratings yet

- Module 2a - AR RecapDocument10 pagesModule 2a - AR RecapChen HaoNo ratings yet

- Review Questions, Exercises and ProblemsDocument5 pagesReview Questions, Exercises and ProblemsChen HaoNo ratings yet

- Cost Accounting Assignment #1Document1 pageCost Accounting Assignment #1Chen HaoNo ratings yet

- Frequently Asked Questions - DeED WWCC ABNDocument3 pagesFrequently Asked Questions - DeED WWCC ABNDimitri KandilasNo ratings yet

- Philippines President Warns People Violating Coronavirus Lockdown Will Be Shot Dead - World News - Mirror OnlineDocument1 pagePhilippines President Warns People Violating Coronavirus Lockdown Will Be Shot Dead - World News - Mirror OnlineElisa Medina AlbinoNo ratings yet

- Durga Prasad V/s BaldeoDocument4 pagesDurga Prasad V/s Baldeofarheen_memon5No ratings yet

- AGENDA-Tbilisi International Conference 2016Document2 pagesAGENDA-Tbilisi International Conference 2016NaTo PoPiashviliNo ratings yet

- Syllabus 2022Document204 pagesSyllabus 2022Singh SNo ratings yet

- Alejandra Mina Et. Al. Vs Ruperta Pascual Et. Al. - G.R. No. L-8321Document6 pagesAlejandra Mina Et. Al. Vs Ruperta Pascual Et. Al. - G.R. No. L-8321Ivy VillalobosNo ratings yet

- Bicol and Deped HymnDocument1 pageBicol and Deped HymnEvelyn ReyesNo ratings yet

- البنود الملزمة في عقد الاعتماد الإيجاري للأصول المنقولةDocument23 pagesالبنود الملزمة في عقد الاعتماد الإيجاري للأصول المنقولةmelissaamrouche124No ratings yet

- Claudio V Sps. SarazaDocument3 pagesClaudio V Sps. SarazaSittie Namraidah L Ali100% (1)

- UK Visas & Immigration: Personal InformationDocument3 pagesUK Visas & Immigration: Personal InformationCarmenEscalanteAldanaNo ratings yet

- Cave Springs Farm-For SaleDocument34 pagesCave Springs Farm-For SaleCraig HardingNo ratings yet

- Iso Iec 10021-8-1999Document50 pagesIso Iec 10021-8-1999gamingfloppa055No ratings yet

- Comparative Analysis and Cash Flow Statements of Hul & Itc: - Group A2Document11 pagesComparative Analysis and Cash Flow Statements of Hul & Itc: - Group A2DEBANGEE ROYNo ratings yet

- Cambridge Primary Checkpoint - English (0844) October 2020 Paper 2 QuestionDocument8 pagesCambridge Primary Checkpoint - English (0844) October 2020 Paper 2 QuestionRonald Aniana Datan100% (1)

- Motion For Preliminary InjunctionDocument16 pagesMotion For Preliminary InjunctionMajority In Mississippi blog100% (1)

- El-Filibusterismo Printing and WritingDocument1 pageEl-Filibusterismo Printing and WritingLeslie GarciaNo ratings yet

- Lesson 2 Ethical and Unethical BehaviorDocument41 pagesLesson 2 Ethical and Unethical BehaviorMarykay BermeoNo ratings yet

- Liberator MagazineDocument14 pagesLiberator Magazinemongo_beti471100% (1)

- Chapter-14: Multinational Capital BudgetingDocument14 pagesChapter-14: Multinational Capital BudgetingAminul Islam AmuNo ratings yet

- List of MBBS Graduates StudentsDocument3 pagesList of MBBS Graduates StudentsAmjadNaseemNo ratings yet

- Red Ribbon RequirementsDocument3 pagesRed Ribbon RequirementsMichael Gerard100% (1)

- AALS Section On Minority Groups Executive Committee Open Letter in Support of Miami Law Dean Anthony E. VaronaDocument4 pagesAALS Section On Minority Groups Executive Committee Open Letter in Support of Miami Law Dean Anthony E. VaronaJimena TavelNo ratings yet

- Legal UpdatesDocument1 pageLegal UpdatesCharlotteNo ratings yet

- TDA 1519cDocument21 pagesTDA 1519cCris VMNo ratings yet

- IPRO Mock Exam - 2021 - QDocument21 pagesIPRO Mock Exam - 2021 - QKevin Ch Li100% (1)

- Ernesto Villazana-Banuelos, A037 837 474 (BIA June 25, 2013)Document20 pagesErnesto Villazana-Banuelos, A037 837 474 (BIA June 25, 2013)Immigrant & Refugee Appellate Center, LLCNo ratings yet

- Letter To Postmaster General Louis DeJoyDocument2 pagesLetter To Postmaster General Louis DeJoyHonolulu Star-AdvertiserNo ratings yet

- X32 UserGuideDocument28 pagesX32 UserGuideVolmir de PaulaNo ratings yet

- Banai Adam TenDocument19 pagesBanai Adam TenMohsin MalkiNo ratings yet