1 Overview Slides Banking v2 SC

1 Overview Slides Banking v2 SC

You might also like

- Truck Drivers FormatDocument1 pageTruck Drivers Formatdbbgnwnf6z70% (74)

- Finance Interview QuestionsDocument12 pagesFinance Interview QuestionsMD RehanNo ratings yet

- A Framework For The Design of Warehouse Layout: Mohsen M.D. HassanDocument9 pagesA Framework For The Design of Warehouse Layout: Mohsen M.D. HassanHo Van RoiNo ratings yet

- Change Is Inevitable. Growth Is Optional.Document32 pagesChange Is Inevitable. Growth Is Optional.chanishaNo ratings yet

- Fundamentals of Financial ServicesDocument27 pagesFundamentals of Financial ServicesfacticalNo ratings yet

- Consumer CreditDocument33 pagesConsumer CreditNeeraj KumarNo ratings yet

- Consumer Credit Commercial Banks Credit Unions (Cus)Document5 pagesConsumer Credit Commercial Banks Credit Unions (Cus)Euly SlaterNo ratings yet

- Section 3: SwapsDocument32 pagesSection 3: Swapsswesam123No ratings yet

- Current Liabilities ManagementDocument7 pagesCurrent Liabilities ManagementJack Herer100% (1)

- Mortgage Markets and Derivatives 2Document35 pagesMortgage Markets and Derivatives 2caballerod0343No ratings yet

- Week 2 Consumer Credit 2024Document56 pagesWeek 2 Consumer Credit 2024Atika HassanNo ratings yet

- Types of Credit FacilitiesDocument23 pagesTypes of Credit Facilitiesarshita sharmaNo ratings yet

- Arranging Funds ModuleDocument34 pagesArranging Funds ModulekylieNo ratings yet

- Economics, Chapter 3 Money and CreditDocument3 pagesEconomics, Chapter 3 Money and CreditshambhaviNo ratings yet

- Antim Prahar Test - Financial and Credit Risk AnalyticsDocument35 pagesAntim Prahar Test - Financial and Credit Risk Analyticsmoviewala1005No ratings yet

- Chapter 01Document24 pagesChapter 01kai liNo ratings yet

- RES 3200 Chapter 4 Fixed Interest Rate Mortgage LoansDocument11 pagesRES 3200 Chapter 4 Fixed Interest Rate Mortgage LoansbaorunchenNo ratings yet

- Access To Capital 1 1 Debt Funding Key InsightsDocument11 pagesAccess To Capital 1 1 Debt Funding Key InsightsH.I.M Dr. Lawiy ZodokNo ratings yet

- Chapter 1 - Introduction To Bank Lending - Sv2.0Document81 pagesChapter 1 - Introduction To Bank Lending - Sv2.0k60.2112340010No ratings yet

- 07 - Consumer CreditDocument23 pages07 - Consumer Creditjay-ar dimaculanganNo ratings yet

- Chapter 7Document12 pagesChapter 7Muskan KumariNo ratings yet

- 15 Days Challenge Money and Credit & Globalization and The IndianDocument86 pages15 Days Challenge Money and Credit & Globalization and The IndianRachit JainNo ratings yet

- ARAG Guidebook Buying A HomeDocument16 pagesARAG Guidebook Buying A HomeJamal AbunahelNo ratings yet

- PaolaDocument9 pagesPaolalorenaNo ratings yet

- SYBBA Unit 4Document40 pagesSYBBA Unit 4idea8433No ratings yet

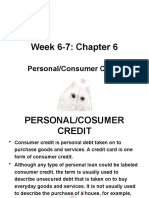

- Week 6-7: Chapter 6: Personal/Consumer CreditDocument24 pagesWeek 6-7: Chapter 6: Personal/Consumer CreditGiselle Bronda CastañedaNo ratings yet

- Chapter 4 - ABSDocument22 pagesChapter 4 - ABSRiha MachireddyNo ratings yet

- Consumer FinanceDocument16 pagesConsumer Financenageshalways100% (1)

- 0 - Retail Banking Doc2Document8 pages0 - Retail Banking Doc2Niyati BagweNo ratings yet

- Types of Credit Instruments & Its FeaturesDocument22 pagesTypes of Credit Instruments & Its Featuresninpra94% (18)

- AFN 221 W05 Consumer Credit vF2021Document23 pagesAFN 221 W05 Consumer Credit vF2021Dina SboulNo ratings yet

- Corporate BankingDocument57 pagesCorporate BankingSoumya TiwaryNo ratings yet

- Bfsi PPTDocument10 pagesBfsi PPTadrishNo ratings yet

- Personal Finance CreditDocument33 pagesPersonal Finance CreditTejashwari todkerNo ratings yet

- Banking Interview QuestionsDocument5 pagesBanking Interview Questionsresearchr.aadi02No ratings yet

- The Bond Market: Financial Markets and Institutions, Mishkin & EakinsDocument26 pagesThe Bond Market: Financial Markets and Institutions, Mishkin & EakinsKhondoker ShidurNo ratings yet

- Mortgage MarketDocument32 pagesMortgage MarketAnathea Gabrielle OrnopiaNo ratings yet

- Debt MarketDocument14 pagesDebt MarketDivya KeswaniNo ratings yet

- Financing Source - Debt ValuationDocument56 pagesFinancing Source - Debt ValuationTacitus KilgoreNo ratings yet

- A Presentation BY Ayush GargDocument33 pagesA Presentation BY Ayush Gargsahilmonga1No ratings yet

- The Big ShortDocument5 pagesThe Big ShortАлександр НефедовNo ratings yet

- Loans and DocumentationDocument30 pagesLoans and DocumentationThejo JoseNo ratings yet

- Money & Credit - Mind MapDocument2 pagesMoney & Credit - Mind MapMohd RazaNo ratings yet

- Chapter No 4Document5 pagesChapter No 4V7 FishyNo ratings yet

- Personal Finance 9th Edition pdf-181-185Document5 pagesPersonal Finance 9th Edition pdf-181-185Jan Allyson BiagNo ratings yet

- Bonds & Fixed-Income Securities: Investment StrategiesDocument12 pagesBonds & Fixed-Income Securities: Investment StrategiesNeelam AnjelNo ratings yet

- Module1 - Introduction To CreditDocument24 pagesModule1 - Introduction To CreditXoxo NiggaNo ratings yet

- Module4 - Managing DebtDocument41 pagesModule4 - Managing DebtXoxo NiggaNo ratings yet

- Article On LoanDocument4 pagesArticle On LoanSaurabh AnandNo ratings yet

- UNIT5Loan SyndicationDocument28 pagesUNIT5Loan SyndicationRohit Kumar 4170No ratings yet

- Chapter 5 Short Term Long Term FinancingDocument40 pagesChapter 5 Short Term Long Term Financingshawal hamzahNo ratings yet

- Mortgage MarketsDocument28 pagesMortgage Marketssweya juliusNo ratings yet

- Chapter Six: Risk Management in Financial InstitutionsDocument22 pagesChapter Six: Risk Management in Financial InstitutionsMikias DegwaleNo ratings yet

- Chapter 3 (Lending)Document13 pagesChapter 3 (Lending)Mohammad Minhaz Hossain RiyadNo ratings yet

- Corporate Credit: References: Gopinath, Banking Principles & OperationsDocument25 pagesCorporate Credit: References: Gopinath, Banking Principles & OperationsJagdish AgarwalNo ratings yet

- CHP 17 - Commercial Bank Sources & Uses of FundsDocument22 pagesCHP 17 - Commercial Bank Sources & Uses of Fundsrashu892No ratings yet

- 2.2 Consumer LoanDocument29 pages2.2 Consumer LoanshkaparovNo ratings yet

- Introduction To CreditDocument34 pagesIntroduction To CreditElle RaineNo ratings yet

- Capital MarketDocument19 pagesCapital MarketUrbano, Lourene Fe S. BSBA FM 2CNo ratings yet

- Chapter 9 - 10-2Document12 pagesChapter 9 - 10-2fouad.mlwbdNo ratings yet

- Short Term Sources of FinanceDocument18 pagesShort Term Sources of FinanceJithin Krishnan100% (1)

- Insider's Keys: To The Best Rates And Terms On Your Next Mortgage, #1From EverandInsider's Keys: To The Best Rates And Terms On Your Next Mortgage, #1No ratings yet

- A Presentation BY Ayush GargDocument33 pagesA Presentation BY Ayush Gargsahilmonga1No ratings yet

- Course Code: SLGM 501 Semester-1 Credits: 3 Sessions: 33: Business Communication MBA-The Class of 2015Document12 pagesCourse Code: SLGM 501 Semester-1 Credits: 3 Sessions: 33: Business Communication MBA-The Class of 2015sahilmonga1No ratings yet

- Investment BankingDocument35 pagesInvestment Bankingsahilmonga1No ratings yet

- Proposal For WorkshopDocument3 pagesProposal For Workshopsahilmonga1No ratings yet

- ME0006 Do Soaring Price and Mounting Demand in IndianDocument5 pagesME0006 Do Soaring Price and Mounting Demand in Indiansahilmonga1No ratings yet

- AccountingDocument1 pageAccountingsamuel debebeNo ratings yet

- Yogesh Kumawat:, Assistant Professor, Sit Legal Aspect of Business NotesDocument53 pagesYogesh Kumawat:, Assistant Professor, Sit Legal Aspect of Business NotesYogesh KumawatNo ratings yet

- Act 51 Public Acts 1951Document61 pagesAct 51 Public Acts 1951Clickon DetroitNo ratings yet

- Backflush CostingDocument45 pagesBackflush CostingKIROJOHNo ratings yet

- SPJMIR Professional Certificate in Brand StrategyDocument27 pagesSPJMIR Professional Certificate in Brand StrategyTanishka PatidarNo ratings yet

- Personal Selling Slide-2Document23 pagesPersonal Selling Slide-2shailendraNo ratings yet

- Internship Report On Sui GasDocument77 pagesInternship Report On Sui Gassiaapa84% (19)

- Company Background AnalysisDocument3 pagesCompany Background AnalysisWeb SitesNo ratings yet

- Presented by - Abilash D Reddy Ravindar .R Sandarsh SureshDocument15 pagesPresented by - Abilash D Reddy Ravindar .R Sandarsh SureshSandarsh SureshNo ratings yet

- Inital Flow Management Productivity ProcedureDocument4 pagesInital Flow Management Productivity Procedureshaggyrahul100% (3)

- Audit Assignment Chapter 13Document3 pagesAudit Assignment Chapter 13il kasNo ratings yet

- Haslil Penelitian Penerapan Bisnis CanvasDocument10 pagesHaslil Penelitian Penerapan Bisnis CanvasRizky MaulanaNo ratings yet

- Comprehensive Problem Master BudgetDocument1 pageComprehensive Problem Master BudgethdejnNo ratings yet

- Abhijeet Parle GDocument41 pagesAbhijeet Parle GvipulpgdmNo ratings yet

- Purchasing and Supply Management 16Th Edition Johnson Solutions Manual Full Chapter PDFDocument43 pagesPurchasing and Supply Management 16Th Edition Johnson Solutions Manual Full Chapter PDFkennethwolfeycqrzmaobe100% (11)

- Alemayehu Tadesse Third Draft Proposal, Alex3 LastDocument37 pagesAlemayehu Tadesse Third Draft Proposal, Alex3 LastZeleke WondimuNo ratings yet

- Inspiring Case Study On Bits Pilani Based Innovative Entrepreneurs in High Tech Growth Sector of Higher Education in IndiaDocument12 pagesInspiring Case Study On Bits Pilani Based Innovative Entrepreneurs in High Tech Growth Sector of Higher Education in IndiaKNOWLEDGE CREATORSNo ratings yet

- Capital BudgetingDocument50 pagesCapital Budgetinghimanshujoshi7789No ratings yet

- Secrets and Agents: Information AsymmetryDocument5 pagesSecrets and Agents: Information AsymmetryNoelpolloNo ratings yet

- AIS (Chapter 5 - MC) Flashcards - QuizletDocument4 pagesAIS (Chapter 5 - MC) Flashcards - QuizletJohn Carlo D MedallaNo ratings yet

- NIST Information Security HandbookDocument176 pagesNIST Information Security HandbooknemonbNo ratings yet

- Entfin f2010Document24 pagesEntfin f2010Toni MartinezNo ratings yet

- (External) Blume Ventures EdTech Market SizingDocument32 pages(External) Blume Ventures EdTech Market Sizingbhanu64No ratings yet

- Week 2 Power PointDocument21 pagesWeek 2 Power PointHenri BenardNo ratings yet

- Mba-Iii-Industrial Relations & Legislations M1Document28 pagesMba-Iii-Industrial Relations & Legislations M1Jyoti YadavNo ratings yet

- Chap 3Document26 pagesChap 3SonNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Truck Drivers FormatDocument1 pageTruck Drivers Formatdbbgnwnf6z70% (74)

- Finance Interview QuestionsDocument12 pagesFinance Interview QuestionsMD RehanNo ratings yet

- A Framework For The Design of Warehouse Layout: Mohsen M.D. HassanDocument9 pagesA Framework For The Design of Warehouse Layout: Mohsen M.D. HassanHo Van RoiNo ratings yet

- Change Is Inevitable. Growth Is Optional.Document32 pagesChange Is Inevitable. Growth Is Optional.chanishaNo ratings yet

- Fundamentals of Financial ServicesDocument27 pagesFundamentals of Financial ServicesfacticalNo ratings yet

- Consumer CreditDocument33 pagesConsumer CreditNeeraj KumarNo ratings yet

- Consumer Credit Commercial Banks Credit Unions (Cus)Document5 pagesConsumer Credit Commercial Banks Credit Unions (Cus)Euly SlaterNo ratings yet

- Section 3: SwapsDocument32 pagesSection 3: Swapsswesam123No ratings yet

- Current Liabilities ManagementDocument7 pagesCurrent Liabilities ManagementJack Herer100% (1)

- Mortgage Markets and Derivatives 2Document35 pagesMortgage Markets and Derivatives 2caballerod0343No ratings yet

- Week 2 Consumer Credit 2024Document56 pagesWeek 2 Consumer Credit 2024Atika HassanNo ratings yet

- Types of Credit FacilitiesDocument23 pagesTypes of Credit Facilitiesarshita sharmaNo ratings yet

- Arranging Funds ModuleDocument34 pagesArranging Funds ModulekylieNo ratings yet

- Economics, Chapter 3 Money and CreditDocument3 pagesEconomics, Chapter 3 Money and CreditshambhaviNo ratings yet

- Antim Prahar Test - Financial and Credit Risk AnalyticsDocument35 pagesAntim Prahar Test - Financial and Credit Risk Analyticsmoviewala1005No ratings yet

- Chapter 01Document24 pagesChapter 01kai liNo ratings yet

- RES 3200 Chapter 4 Fixed Interest Rate Mortgage LoansDocument11 pagesRES 3200 Chapter 4 Fixed Interest Rate Mortgage LoansbaorunchenNo ratings yet

- Access To Capital 1 1 Debt Funding Key InsightsDocument11 pagesAccess To Capital 1 1 Debt Funding Key InsightsH.I.M Dr. Lawiy ZodokNo ratings yet

- Chapter 1 - Introduction To Bank Lending - Sv2.0Document81 pagesChapter 1 - Introduction To Bank Lending - Sv2.0k60.2112340010No ratings yet

- 07 - Consumer CreditDocument23 pages07 - Consumer Creditjay-ar dimaculanganNo ratings yet

- Chapter 7Document12 pagesChapter 7Muskan KumariNo ratings yet

- 15 Days Challenge Money and Credit & Globalization and The IndianDocument86 pages15 Days Challenge Money and Credit & Globalization and The IndianRachit JainNo ratings yet

- ARAG Guidebook Buying A HomeDocument16 pagesARAG Guidebook Buying A HomeJamal AbunahelNo ratings yet

- PaolaDocument9 pagesPaolalorenaNo ratings yet

- SYBBA Unit 4Document40 pagesSYBBA Unit 4idea8433No ratings yet

- Week 6-7: Chapter 6: Personal/Consumer CreditDocument24 pagesWeek 6-7: Chapter 6: Personal/Consumer CreditGiselle Bronda CastañedaNo ratings yet

- Chapter 4 - ABSDocument22 pagesChapter 4 - ABSRiha MachireddyNo ratings yet

- Consumer FinanceDocument16 pagesConsumer Financenageshalways100% (1)

- 0 - Retail Banking Doc2Document8 pages0 - Retail Banking Doc2Niyati BagweNo ratings yet

- Types of Credit Instruments & Its FeaturesDocument22 pagesTypes of Credit Instruments & Its Featuresninpra94% (18)

- AFN 221 W05 Consumer Credit vF2021Document23 pagesAFN 221 W05 Consumer Credit vF2021Dina SboulNo ratings yet

- Corporate BankingDocument57 pagesCorporate BankingSoumya TiwaryNo ratings yet

- Bfsi PPTDocument10 pagesBfsi PPTadrishNo ratings yet

- Personal Finance CreditDocument33 pagesPersonal Finance CreditTejashwari todkerNo ratings yet

- Banking Interview QuestionsDocument5 pagesBanking Interview Questionsresearchr.aadi02No ratings yet

- The Bond Market: Financial Markets and Institutions, Mishkin & EakinsDocument26 pagesThe Bond Market: Financial Markets and Institutions, Mishkin & EakinsKhondoker ShidurNo ratings yet

- Mortgage MarketDocument32 pagesMortgage MarketAnathea Gabrielle OrnopiaNo ratings yet

- Debt MarketDocument14 pagesDebt MarketDivya KeswaniNo ratings yet

- Financing Source - Debt ValuationDocument56 pagesFinancing Source - Debt ValuationTacitus KilgoreNo ratings yet

- A Presentation BY Ayush GargDocument33 pagesA Presentation BY Ayush Gargsahilmonga1No ratings yet

- The Big ShortDocument5 pagesThe Big ShortАлександр НефедовNo ratings yet

- Loans and DocumentationDocument30 pagesLoans and DocumentationThejo JoseNo ratings yet

- Money & Credit - Mind MapDocument2 pagesMoney & Credit - Mind MapMohd RazaNo ratings yet

- Chapter No 4Document5 pagesChapter No 4V7 FishyNo ratings yet

- Personal Finance 9th Edition pdf-181-185Document5 pagesPersonal Finance 9th Edition pdf-181-185Jan Allyson BiagNo ratings yet

- Bonds & Fixed-Income Securities: Investment StrategiesDocument12 pagesBonds & Fixed-Income Securities: Investment StrategiesNeelam AnjelNo ratings yet

- Module1 - Introduction To CreditDocument24 pagesModule1 - Introduction To CreditXoxo NiggaNo ratings yet

- Module4 - Managing DebtDocument41 pagesModule4 - Managing DebtXoxo NiggaNo ratings yet

- Article On LoanDocument4 pagesArticle On LoanSaurabh AnandNo ratings yet

- UNIT5Loan SyndicationDocument28 pagesUNIT5Loan SyndicationRohit Kumar 4170No ratings yet

- Chapter 5 Short Term Long Term FinancingDocument40 pagesChapter 5 Short Term Long Term Financingshawal hamzahNo ratings yet

- Mortgage MarketsDocument28 pagesMortgage Marketssweya juliusNo ratings yet

- Chapter Six: Risk Management in Financial InstitutionsDocument22 pagesChapter Six: Risk Management in Financial InstitutionsMikias DegwaleNo ratings yet

- Chapter 3 (Lending)Document13 pagesChapter 3 (Lending)Mohammad Minhaz Hossain RiyadNo ratings yet

- Corporate Credit: References: Gopinath, Banking Principles & OperationsDocument25 pagesCorporate Credit: References: Gopinath, Banking Principles & OperationsJagdish AgarwalNo ratings yet

- CHP 17 - Commercial Bank Sources & Uses of FundsDocument22 pagesCHP 17 - Commercial Bank Sources & Uses of Fundsrashu892No ratings yet

- 2.2 Consumer LoanDocument29 pages2.2 Consumer LoanshkaparovNo ratings yet

- Introduction To CreditDocument34 pagesIntroduction To CreditElle RaineNo ratings yet

- Capital MarketDocument19 pagesCapital MarketUrbano, Lourene Fe S. BSBA FM 2CNo ratings yet

- Chapter 9 - 10-2Document12 pagesChapter 9 - 10-2fouad.mlwbdNo ratings yet

- Short Term Sources of FinanceDocument18 pagesShort Term Sources of FinanceJithin Krishnan100% (1)

- Insider's Keys: To The Best Rates And Terms On Your Next Mortgage, #1From EverandInsider's Keys: To The Best Rates And Terms On Your Next Mortgage, #1No ratings yet

- A Presentation BY Ayush GargDocument33 pagesA Presentation BY Ayush Gargsahilmonga1No ratings yet

- Course Code: SLGM 501 Semester-1 Credits: 3 Sessions: 33: Business Communication MBA-The Class of 2015Document12 pagesCourse Code: SLGM 501 Semester-1 Credits: 3 Sessions: 33: Business Communication MBA-The Class of 2015sahilmonga1No ratings yet

- Investment BankingDocument35 pagesInvestment Bankingsahilmonga1No ratings yet

- Proposal For WorkshopDocument3 pagesProposal For Workshopsahilmonga1No ratings yet

- ME0006 Do Soaring Price and Mounting Demand in IndianDocument5 pagesME0006 Do Soaring Price and Mounting Demand in Indiansahilmonga1No ratings yet

- AccountingDocument1 pageAccountingsamuel debebeNo ratings yet

- Yogesh Kumawat:, Assistant Professor, Sit Legal Aspect of Business NotesDocument53 pagesYogesh Kumawat:, Assistant Professor, Sit Legal Aspect of Business NotesYogesh KumawatNo ratings yet

- Act 51 Public Acts 1951Document61 pagesAct 51 Public Acts 1951Clickon DetroitNo ratings yet

- Backflush CostingDocument45 pagesBackflush CostingKIROJOHNo ratings yet

- SPJMIR Professional Certificate in Brand StrategyDocument27 pagesSPJMIR Professional Certificate in Brand StrategyTanishka PatidarNo ratings yet

- Personal Selling Slide-2Document23 pagesPersonal Selling Slide-2shailendraNo ratings yet

- Internship Report On Sui GasDocument77 pagesInternship Report On Sui Gassiaapa84% (19)

- Company Background AnalysisDocument3 pagesCompany Background AnalysisWeb SitesNo ratings yet

- Presented by - Abilash D Reddy Ravindar .R Sandarsh SureshDocument15 pagesPresented by - Abilash D Reddy Ravindar .R Sandarsh SureshSandarsh SureshNo ratings yet

- Inital Flow Management Productivity ProcedureDocument4 pagesInital Flow Management Productivity Procedureshaggyrahul100% (3)

- Audit Assignment Chapter 13Document3 pagesAudit Assignment Chapter 13il kasNo ratings yet

- Haslil Penelitian Penerapan Bisnis CanvasDocument10 pagesHaslil Penelitian Penerapan Bisnis CanvasRizky MaulanaNo ratings yet

- Comprehensive Problem Master BudgetDocument1 pageComprehensive Problem Master BudgethdejnNo ratings yet

- Abhijeet Parle GDocument41 pagesAbhijeet Parle GvipulpgdmNo ratings yet

- Purchasing and Supply Management 16Th Edition Johnson Solutions Manual Full Chapter PDFDocument43 pagesPurchasing and Supply Management 16Th Edition Johnson Solutions Manual Full Chapter PDFkennethwolfeycqrzmaobe100% (11)

- Alemayehu Tadesse Third Draft Proposal, Alex3 LastDocument37 pagesAlemayehu Tadesse Third Draft Proposal, Alex3 LastZeleke WondimuNo ratings yet

- Inspiring Case Study On Bits Pilani Based Innovative Entrepreneurs in High Tech Growth Sector of Higher Education in IndiaDocument12 pagesInspiring Case Study On Bits Pilani Based Innovative Entrepreneurs in High Tech Growth Sector of Higher Education in IndiaKNOWLEDGE CREATORSNo ratings yet

- Capital BudgetingDocument50 pagesCapital Budgetinghimanshujoshi7789No ratings yet

- Secrets and Agents: Information AsymmetryDocument5 pagesSecrets and Agents: Information AsymmetryNoelpolloNo ratings yet

- AIS (Chapter 5 - MC) Flashcards - QuizletDocument4 pagesAIS (Chapter 5 - MC) Flashcards - QuizletJohn Carlo D MedallaNo ratings yet

- NIST Information Security HandbookDocument176 pagesNIST Information Security HandbooknemonbNo ratings yet

- Entfin f2010Document24 pagesEntfin f2010Toni MartinezNo ratings yet

- (External) Blume Ventures EdTech Market SizingDocument32 pages(External) Blume Ventures EdTech Market Sizingbhanu64No ratings yet

- Week 2 Power PointDocument21 pagesWeek 2 Power PointHenri BenardNo ratings yet

- Mba-Iii-Industrial Relations & Legislations M1Document28 pagesMba-Iii-Industrial Relations & Legislations M1Jyoti YadavNo ratings yet

- Chap 3Document26 pagesChap 3SonNo ratings yet