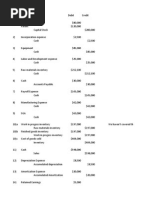

Introduction To Cost Accounting/Costing

Introduction To Cost Accounting/Costing

You might also like

- Volume 2 India Ver 141005 PDFDocument222 pagesVolume 2 India Ver 141005 PDFLittin Thankachan82% (17)

- Personal Assignment 4 Week 8: English ProfessionalDocument4 pagesPersonal Assignment 4 Week 8: English ProfessionalBonardo Raja Ishak StanggangNo ratings yet

- Cost Accounting Quiz 3Document4 pagesCost Accounting Quiz 3Tayyaba KhalidNo ratings yet

- Lecture 8 - Exercises - QuestionDocument3 pagesLecture 8 - Exercises - QuestionIsyraf Hatim Mohd TamizamNo ratings yet

- Firda Arfianti - 2301949596 - LA53 - ACCT7141 - Accounting Information System and Internal ControlDocument6 pagesFirda Arfianti - 2301949596 - LA53 - ACCT7141 - Accounting Information System and Internal Controlfirda arfiantiNo ratings yet

- Comprehensive Master Budget Accounting 2302 Professor Norma JacobsDocument5 pagesComprehensive Master Budget Accounting 2302 Professor Norma JacobsOmar Gibson0% (1)

- Tugas Kelompok Ke-3 (Minggu 7/ Sesi 13) : Weighted-Average Method - Periodic InventoryDocument10 pagesTugas Kelompok Ke-3 (Minggu 7/ Sesi 13) : Weighted-Average Method - Periodic Inventoryliissylvia100% (2)

- CA01 VariableCostingFDocument114 pagesCA01 VariableCostingFVenise Balia33% (3)

- Ma2 Specimen j14Document16 pagesMa2 Specimen j14talha100% (3)

- AkuntansiDocument4 pagesAkuntansiNadilla NurNo ratings yet

- Ilovepdf MergedDocument9 pagesIlovepdf MergedGARTMiawNo ratings yet

- Modul Lab. Akuntansi Manajemen I 2019 - 2020 V1.1Document29 pagesModul Lab. Akuntansi Manajemen I 2019 - 2020 V1.1Felix HarryyantoNo ratings yet

- BINUS University: GuidanceDocument6 pagesBINUS University: Guidance079 Fadhil Muhammad Rafi'No ratings yet

- Tugas Kelompok Ke-3 Week 8: Flexible BudgetDocument4 pagesTugas Kelompok Ke-3 Week 8: Flexible BudgetNadilla NurNo ratings yet

- Tugas Sesi 7Document5 pagesTugas Sesi 7mutmainnahNo ratings yet

- 1621 Acct6174 Tabe TK1-W3-S4-R1 Team1Document11 pages1621 Acct6174 Tabe TK1-W3-S4-R1 Team1Raisul Ma'arif100% (1)

- Chapter-4-Solved-Problems (Cost Accounting)Document31 pagesChapter-4-Solved-Problems (Cost Accounting)Zainab GamalNo ratings yet

- CH 10 SMDocument17 pagesCH 10 SMapi-267019092No ratings yet

- Latihan 2 DiazDocument6 pagesLatihan 2 DiazDiaz Hesron Deo SimorangkirNo ratings yet

- Management AccountingDocument42 pagesManagement AccountingaamritaaNo ratings yet

- Animal Gear Company Makes Two Pet Carriers The Cat Allac andDocument2 pagesAnimal Gear Company Makes Two Pet Carriers The Cat Allac andAmit PandeyNo ratings yet

- BINUS University: Question 1 of 5 (Point 15%)Document5 pagesBINUS University: Question 1 of 5 (Point 15%)FirdaNo ratings yet

- The Wood Spirits Company Produces Two Products Turpentine and MethanolDocument1 pageThe Wood Spirits Company Produces Two Products Turpentine and MethanolAmit PandeyNo ratings yet

- Solution P 9-17Document3 pagesSolution P 9-17Thanawat PHURISIRUNGROJNo ratings yet

- Tugas Personal Ke-1 Week 2: Soal 1Document14 pagesTugas Personal Ke-1 Week 2: Soal 1meifangNo ratings yet

- تابع فصل ادارة المخزونDocument1 pageتابع فصل ادارة المخزونAhmed El KhateebNo ratings yet

- Chapter 3Document6 pagesChapter 3Pauline Keith Paz ManuelNo ratings yet

- Chapter 4Document52 pagesChapter 4XI MIPA 1 BILLY SURYAJAYANo ratings yet

- Sesi 9 & 10 Praktikum - SharedDocument9 pagesSesi 9 & 10 Praktikum - SharedDian Permata SariNo ratings yet

- Alpha BetaDocument13 pagesAlpha BetaJoel Christian MascariñaNo ratings yet

- Corporate FinanceDocument5 pagesCorporate FinancejahidkhanNo ratings yet

- Lira Consulting, Sa Adjusting Entry May 31, 2017: TotalDocument10 pagesLira Consulting, Sa Adjusting Entry May 31, 2017: TotalAngellamndaNo ratings yet

- Persediaan (Penilaian Tambahan/Additional Valuation) : Lower of Cost or Net Realizable ValueDocument4 pagesPersediaan (Penilaian Tambahan/Additional Valuation) : Lower of Cost or Net Realizable Valuemuhammad raflyNo ratings yet

- Solutions To Review Exam Papers 1 To 3Document171 pagesSolutions To Review Exam Papers 1 To 3Roi NyanNo ratings yet

- ABC ExerciseDocument3 pagesABC ExerciseRijal DinNo ratings yet

- BINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Document5 pagesBINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Martha Wulan TumangkengNo ratings yet

- Tugas AkbiDocument44 pagesTugas AkbiLafidan Rizata FebiolaNo ratings yet

- Assignment No.2 206Document5 pagesAssignment No.2 206Halimah SheikhNo ratings yet

- Assume The FollowingDocument3 pagesAssume The FollowingElliot RichardNo ratings yet

- Unit 7 - Wiley Plus ExamplesDocument14 pagesUnit 7 - Wiley Plus ExamplesMohammed Al DhaheriNo ratings yet

- Soal AKMDocument4 pagesSoal AKMIlham Syukrillah0% (1)

- Lembar Kerja Komputer Ukk Tina Nur Aisyah Xii Ak 1 25Document30 pagesLembar Kerja Komputer Ukk Tina Nur Aisyah Xii Ak 1 25RizalJalilPujaKesumaNo ratings yet

- ch03 Part3Document6 pagesch03 Part3Sergio HoffmanNo ratings yet

- Prescott Manufacturing Evaluates The Performance of Its Production Managers Based On A Variety of FactorsDocument3 pagesPrescott Manufacturing Evaluates The Performance of Its Production Managers Based On A Variety of FactorsElliot RichardNo ratings yet

- Soal Akuntansi KeuanganDocument4 pagesSoal Akuntansi Keuanganekaeva03No ratings yet

- Activity Preparing Journal EntriesDocument5 pagesActivity Preparing Journal EntriesJomir Kimberly DomingoNo ratings yet

- Prevention Costs: Appraisal Costs: Internal Failure Costs: External Failure CostsDocument35 pagesPrevention Costs: Appraisal Costs: Internal Failure Costs: External Failure CostsRaniaNo ratings yet

- Akdas Brief Dan SelfDocument18 pagesAkdas Brief Dan SelfAwun Sukma100% (1)

- Mock Test 201 KeyDocument12 pagesMock Test 201 Keydengdeng2211No ratings yet

- BAB 16 v2Document10 pagesBAB 16 v2rahmat lubisNo ratings yet

- Cost Accounting Chapter 2 Assignment #5Document4 pagesCost Accounting Chapter 2 Assignment #5Tawan Vihokratana100% (1)

- Ms Excel FinanceDocument17 pagesMs Excel FinanceNickolas GilbertNo ratings yet

- Questions Part2 Srikant and Datar TextbookDocument5 pagesQuestions Part2 Srikant and Datar TextbookUmar SyakirinNo ratings yet

- Mind Map Job Order CostingDocument1 pageMind Map Job Order CostingAndhika Bella PrawitasariNo ratings yet

- Lecture 6.1-General Cost Classifications (Problem 1)Document3 pagesLecture 6.1-General Cost Classifications (Problem 1)Nazmul-Hassan Sumon100% (4)

- By - Product Problem Solving - AsifDocument4 pagesBy - Product Problem Solving - AsifJafa AbnNo ratings yet

- Andreas B. IntermediateDocument4 pagesAndreas B. IntermediateAndreasNo ratings yet

- Tgs Kelompok Ganda Kasus 3Document18 pagesTgs Kelompok Ganda Kasus 3GARTMiawNo ratings yet

- .Archivetemp6 - Cost Accounting (Old & New Syllabus)Document2 pages.Archivetemp6 - Cost Accounting (Old & New Syllabus)aneebaNo ratings yet

- Mishal Mustafa BTA111 Prof. WuDocument2 pagesMishal Mustafa BTA111 Prof. WuMishalm96No ratings yet

- TerDocument7 pagesTerShalsa ByllaNo ratings yet

- Chapter 2 - Cost terms - CLC - handout.pptxDocument61 pagesChapter 2 - Cost terms - CLC - handout.pptxHoàng Bảo TrâmNo ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument38 pagesProcess Costing and Hybrid Product-Costing SystemsZia UddinNo ratings yet

- Artikel Bisnis 1Document3 pagesArtikel Bisnis 1Harisvan To SevenNo ratings yet

- Part C Raw Rakon, HtsDocument4 pagesPart C Raw Rakon, HtsHarisvan To SevenNo ratings yet

- The Foods and Beverages Merchants in Jabodetabek Lost Their Income Until RP 200 BillionDocument3 pagesThe Foods and Beverages Merchants in Jabodetabek Lost Their Income Until RP 200 BillionHarisvan To SevenNo ratings yet

- Perkapalan: Carriage of Goods by Sea ActDocument17 pagesPerkapalan: Carriage of Goods by Sea ActHarisvan To SevenNo ratings yet

- Zona 1 2 3 4 Oi Matriks Biaya (Cid) 1 Zone 1 2 2 1 3 2 4 3 DD 4 Matriks Exp Zone 1 2 Zone 1 2 3 4 1 1 2 2 3 3 4 4 DD DD Ed BD 1 2 1 2 3 4 DD DD Ed BDDocument2 pagesZona 1 2 3 4 Oi Matriks Biaya (Cid) 1 Zone 1 2 2 1 3 2 4 3 DD 4 Matriks Exp Zone 1 2 Zone 1 2 3 4 1 1 2 2 3 3 4 4 DD DD Ed BD 1 2 1 2 3 4 DD DD Ed BDHarisvan To SevenNo ratings yet

- Explosives Which Can Be Carried Only in Cargo Aircraft: Explosiv eDocument5 pagesExplosives Which Can Be Carried Only in Cargo Aircraft: Explosiv eHarisvan To SevenNo ratings yet

- Dangerous Goods Regulation 6-10 SlideDocument5 pagesDangerous Goods Regulation 6-10 SlideHarisvan To SevenNo ratings yet

- Dangerous Goods Regulation 1-5 SlideDocument5 pagesDangerous Goods Regulation 1-5 SlideHarisvan To SevenNo ratings yet

- O Classificati N: Instructor: TAYFOURDocument136 pagesO Classificati N: Instructor: TAYFOURyudha manurungNo ratings yet

- Omnichannel DistributionDocument24 pagesOmnichannel DistributionHarisvan To SevenNo ratings yet

- Practical Account 01 Es QuDocument718 pagesPractical Account 01 Es QuMozahar Sujon100% (1)

- Chapter 2 - Correction of Errors PDFDocument12 pagesChapter 2 - Correction of Errors PDFRonald90% (10)

- ACC 577 Quiz Week 2Document11 pagesACC 577 Quiz Week 2MaryNo ratings yet

- Republic of The Philippines Department of Education Public Technical - Vocational High SchoolsDocument34 pagesRepublic of The Philippines Department of Education Public Technical - Vocational High SchoolsKristel AcordonNo ratings yet

- Solution To Quiz 2Document4 pagesSolution To Quiz 2GianJoshuaDayritNo ratings yet

- Relevant Costing ReviewerDocument4 pagesRelevant Costing Reviewerdaniellejueco1228No ratings yet

- Chapter3 - Costing Methods The Costing of Resource OutputsDocument27 pagesChapter3 - Costing Methods The Costing of Resource OutputsNetsanet Belay100% (1)

- Cost Accounting Hilton 13Document10 pagesCost Accounting Hilton 13Vin TenNo ratings yet

- Summative QuizDocument2 pagesSummative QuizVIRGIL KIT AUGUSTIN ABANILLANo ratings yet

- Ma Project FMCG-: Marico, Itc, Colgate, Unilever, Yili, PepsicoDocument12 pagesMa Project FMCG-: Marico, Itc, Colgate, Unilever, Yili, PepsicoJasneet BaidNo ratings yet

- CH 09Document69 pagesCH 09Navindra Jaggernauth100% (1)

- Final Dissertation Elearning Chitunha PDFDocument66 pagesFinal Dissertation Elearning Chitunha PDFLinos TichazorwaNo ratings yet

- CH 4Document72 pagesCH 4Chang Chan ChongNo ratings yet

- Material CostingDocument18 pagesMaterial CostingRaj KumarNo ratings yet

- Ne Malai - 7 - Exercise CalculationDocument30 pagesNe Malai - 7 - Exercise CalculationNemalai VitalNo ratings yet

- Test Bank Accounting 25th Editon Warren Chapter 22 BudgetingDocument94 pagesTest Bank Accounting 25th Editon Warren Chapter 22 BudgetingAngely May Jordan100% (1)

- Dispensers of California (Jeff)Document9 pagesDispensers of California (Jeff)Jeffery KaoNo ratings yet

- Chapter 13 - Gross Profit MethodDocument7 pagesChapter 13 - Gross Profit MethodLorence IbañezNo ratings yet

- Account For MaterialDocument25 pagesAccount For Materialshrestha.aryxnNo ratings yet

- CostConExercise - COGM & COGSDocument3 pagesCostConExercise - COGM & COGSLee Tarroza100% (1)

- Standard Costing - A LevelDocument3 pagesStandard Costing - A LevelMUSTHARI KHANNo ratings yet

- Compilation of Assignments in Cost AccountingDocument9 pagesCompilation of Assignments in Cost AccountingCaia VelazquezNo ratings yet

- Fifo Method and Debt Held As MaturityDocument3 pagesFifo Method and Debt Held As MaturitysninaricaNo ratings yet

- Management TheoryDocument63 pagesManagement TheoryFaisal Ibrahim100% (2)

- CHAPTER 2 - Partnership OperationsDocument10 pagesCHAPTER 2 - Partnership OperationsRominna Dela RuedaNo ratings yet

- Papers of Cost AccountingDocument8 pagesPapers of Cost AccountingTalha BukhariNo ratings yet

- Terminal Report Siosig Edited 02Document37 pagesTerminal Report Siosig Edited 02briandss123No ratings yet

Download as pptx, pdf, or txt

You might also like

- Volume 2 India Ver 141005 PDFDocument222 pagesVolume 2 India Ver 141005 PDFLittin Thankachan82% (17)

- Personal Assignment 4 Week 8: English ProfessionalDocument4 pagesPersonal Assignment 4 Week 8: English ProfessionalBonardo Raja Ishak StanggangNo ratings yet

- Cost Accounting Quiz 3Document4 pagesCost Accounting Quiz 3Tayyaba KhalidNo ratings yet

- Lecture 8 - Exercises - QuestionDocument3 pagesLecture 8 - Exercises - QuestionIsyraf Hatim Mohd TamizamNo ratings yet

- Firda Arfianti - 2301949596 - LA53 - ACCT7141 - Accounting Information System and Internal ControlDocument6 pagesFirda Arfianti - 2301949596 - LA53 - ACCT7141 - Accounting Information System and Internal Controlfirda arfiantiNo ratings yet

- Comprehensive Master Budget Accounting 2302 Professor Norma JacobsDocument5 pagesComprehensive Master Budget Accounting 2302 Professor Norma JacobsOmar Gibson0% (1)

- Tugas Kelompok Ke-3 (Minggu 7/ Sesi 13) : Weighted-Average Method - Periodic InventoryDocument10 pagesTugas Kelompok Ke-3 (Minggu 7/ Sesi 13) : Weighted-Average Method - Periodic Inventoryliissylvia100% (2)

- CA01 VariableCostingFDocument114 pagesCA01 VariableCostingFVenise Balia33% (3)

- Ma2 Specimen j14Document16 pagesMa2 Specimen j14talha100% (3)

- AkuntansiDocument4 pagesAkuntansiNadilla NurNo ratings yet

- Ilovepdf MergedDocument9 pagesIlovepdf MergedGARTMiawNo ratings yet

- Modul Lab. Akuntansi Manajemen I 2019 - 2020 V1.1Document29 pagesModul Lab. Akuntansi Manajemen I 2019 - 2020 V1.1Felix HarryyantoNo ratings yet

- BINUS University: GuidanceDocument6 pagesBINUS University: Guidance079 Fadhil Muhammad Rafi'No ratings yet

- Tugas Kelompok Ke-3 Week 8: Flexible BudgetDocument4 pagesTugas Kelompok Ke-3 Week 8: Flexible BudgetNadilla NurNo ratings yet

- Tugas Sesi 7Document5 pagesTugas Sesi 7mutmainnahNo ratings yet

- 1621 Acct6174 Tabe TK1-W3-S4-R1 Team1Document11 pages1621 Acct6174 Tabe TK1-W3-S4-R1 Team1Raisul Ma'arif100% (1)

- Chapter-4-Solved-Problems (Cost Accounting)Document31 pagesChapter-4-Solved-Problems (Cost Accounting)Zainab GamalNo ratings yet

- CH 10 SMDocument17 pagesCH 10 SMapi-267019092No ratings yet

- Latihan 2 DiazDocument6 pagesLatihan 2 DiazDiaz Hesron Deo SimorangkirNo ratings yet

- Management AccountingDocument42 pagesManagement AccountingaamritaaNo ratings yet

- Animal Gear Company Makes Two Pet Carriers The Cat Allac andDocument2 pagesAnimal Gear Company Makes Two Pet Carriers The Cat Allac andAmit PandeyNo ratings yet

- BINUS University: Question 1 of 5 (Point 15%)Document5 pagesBINUS University: Question 1 of 5 (Point 15%)FirdaNo ratings yet

- The Wood Spirits Company Produces Two Products Turpentine and MethanolDocument1 pageThe Wood Spirits Company Produces Two Products Turpentine and MethanolAmit PandeyNo ratings yet

- Solution P 9-17Document3 pagesSolution P 9-17Thanawat PHURISIRUNGROJNo ratings yet

- Tugas Personal Ke-1 Week 2: Soal 1Document14 pagesTugas Personal Ke-1 Week 2: Soal 1meifangNo ratings yet

- تابع فصل ادارة المخزونDocument1 pageتابع فصل ادارة المخزونAhmed El KhateebNo ratings yet

- Chapter 3Document6 pagesChapter 3Pauline Keith Paz ManuelNo ratings yet

- Chapter 4Document52 pagesChapter 4XI MIPA 1 BILLY SURYAJAYANo ratings yet

- Sesi 9 & 10 Praktikum - SharedDocument9 pagesSesi 9 & 10 Praktikum - SharedDian Permata SariNo ratings yet

- Alpha BetaDocument13 pagesAlpha BetaJoel Christian MascariñaNo ratings yet

- Corporate FinanceDocument5 pagesCorporate FinancejahidkhanNo ratings yet

- Lira Consulting, Sa Adjusting Entry May 31, 2017: TotalDocument10 pagesLira Consulting, Sa Adjusting Entry May 31, 2017: TotalAngellamndaNo ratings yet

- Persediaan (Penilaian Tambahan/Additional Valuation) : Lower of Cost or Net Realizable ValueDocument4 pagesPersediaan (Penilaian Tambahan/Additional Valuation) : Lower of Cost or Net Realizable Valuemuhammad raflyNo ratings yet

- Solutions To Review Exam Papers 1 To 3Document171 pagesSolutions To Review Exam Papers 1 To 3Roi NyanNo ratings yet

- ABC ExerciseDocument3 pagesABC ExerciseRijal DinNo ratings yet

- BINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Document5 pagesBINUS University: Undergraduate / Master / Doctoral ) International/Regular/Smart Program/Global Class )Martha Wulan TumangkengNo ratings yet

- Tugas AkbiDocument44 pagesTugas AkbiLafidan Rizata FebiolaNo ratings yet

- Assignment No.2 206Document5 pagesAssignment No.2 206Halimah SheikhNo ratings yet

- Assume The FollowingDocument3 pagesAssume The FollowingElliot RichardNo ratings yet

- Unit 7 - Wiley Plus ExamplesDocument14 pagesUnit 7 - Wiley Plus ExamplesMohammed Al DhaheriNo ratings yet

- Soal AKMDocument4 pagesSoal AKMIlham Syukrillah0% (1)

- Lembar Kerja Komputer Ukk Tina Nur Aisyah Xii Ak 1 25Document30 pagesLembar Kerja Komputer Ukk Tina Nur Aisyah Xii Ak 1 25RizalJalilPujaKesumaNo ratings yet

- ch03 Part3Document6 pagesch03 Part3Sergio HoffmanNo ratings yet

- Prescott Manufacturing Evaluates The Performance of Its Production Managers Based On A Variety of FactorsDocument3 pagesPrescott Manufacturing Evaluates The Performance of Its Production Managers Based On A Variety of FactorsElliot RichardNo ratings yet

- Soal Akuntansi KeuanganDocument4 pagesSoal Akuntansi Keuanganekaeva03No ratings yet

- Activity Preparing Journal EntriesDocument5 pagesActivity Preparing Journal EntriesJomir Kimberly DomingoNo ratings yet

- Prevention Costs: Appraisal Costs: Internal Failure Costs: External Failure CostsDocument35 pagesPrevention Costs: Appraisal Costs: Internal Failure Costs: External Failure CostsRaniaNo ratings yet

- Akdas Brief Dan SelfDocument18 pagesAkdas Brief Dan SelfAwun Sukma100% (1)

- Mock Test 201 KeyDocument12 pagesMock Test 201 Keydengdeng2211No ratings yet

- BAB 16 v2Document10 pagesBAB 16 v2rahmat lubisNo ratings yet

- Cost Accounting Chapter 2 Assignment #5Document4 pagesCost Accounting Chapter 2 Assignment #5Tawan Vihokratana100% (1)

- Ms Excel FinanceDocument17 pagesMs Excel FinanceNickolas GilbertNo ratings yet

- Questions Part2 Srikant and Datar TextbookDocument5 pagesQuestions Part2 Srikant and Datar TextbookUmar SyakirinNo ratings yet

- Mind Map Job Order CostingDocument1 pageMind Map Job Order CostingAndhika Bella PrawitasariNo ratings yet

- Lecture 6.1-General Cost Classifications (Problem 1)Document3 pagesLecture 6.1-General Cost Classifications (Problem 1)Nazmul-Hassan Sumon100% (4)

- By - Product Problem Solving - AsifDocument4 pagesBy - Product Problem Solving - AsifJafa AbnNo ratings yet

- Andreas B. IntermediateDocument4 pagesAndreas B. IntermediateAndreasNo ratings yet

- Tgs Kelompok Ganda Kasus 3Document18 pagesTgs Kelompok Ganda Kasus 3GARTMiawNo ratings yet

- .Archivetemp6 - Cost Accounting (Old & New Syllabus)Document2 pages.Archivetemp6 - Cost Accounting (Old & New Syllabus)aneebaNo ratings yet

- Mishal Mustafa BTA111 Prof. WuDocument2 pagesMishal Mustafa BTA111 Prof. WuMishalm96No ratings yet

- TerDocument7 pagesTerShalsa ByllaNo ratings yet

- Chapter 2 - Cost terms - CLC - handout.pptxDocument61 pagesChapter 2 - Cost terms - CLC - handout.pptxHoàng Bảo TrâmNo ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument38 pagesProcess Costing and Hybrid Product-Costing SystemsZia UddinNo ratings yet

- Artikel Bisnis 1Document3 pagesArtikel Bisnis 1Harisvan To SevenNo ratings yet

- Part C Raw Rakon, HtsDocument4 pagesPart C Raw Rakon, HtsHarisvan To SevenNo ratings yet

- The Foods and Beverages Merchants in Jabodetabek Lost Their Income Until RP 200 BillionDocument3 pagesThe Foods and Beverages Merchants in Jabodetabek Lost Their Income Until RP 200 BillionHarisvan To SevenNo ratings yet

- Perkapalan: Carriage of Goods by Sea ActDocument17 pagesPerkapalan: Carriage of Goods by Sea ActHarisvan To SevenNo ratings yet

- Zona 1 2 3 4 Oi Matriks Biaya (Cid) 1 Zone 1 2 2 1 3 2 4 3 DD 4 Matriks Exp Zone 1 2 Zone 1 2 3 4 1 1 2 2 3 3 4 4 DD DD Ed BD 1 2 1 2 3 4 DD DD Ed BDDocument2 pagesZona 1 2 3 4 Oi Matriks Biaya (Cid) 1 Zone 1 2 2 1 3 2 4 3 DD 4 Matriks Exp Zone 1 2 Zone 1 2 3 4 1 1 2 2 3 3 4 4 DD DD Ed BD 1 2 1 2 3 4 DD DD Ed BDHarisvan To SevenNo ratings yet

- Explosives Which Can Be Carried Only in Cargo Aircraft: Explosiv eDocument5 pagesExplosives Which Can Be Carried Only in Cargo Aircraft: Explosiv eHarisvan To SevenNo ratings yet

- Dangerous Goods Regulation 6-10 SlideDocument5 pagesDangerous Goods Regulation 6-10 SlideHarisvan To SevenNo ratings yet

- Dangerous Goods Regulation 1-5 SlideDocument5 pagesDangerous Goods Regulation 1-5 SlideHarisvan To SevenNo ratings yet

- O Classificati N: Instructor: TAYFOURDocument136 pagesO Classificati N: Instructor: TAYFOURyudha manurungNo ratings yet

- Omnichannel DistributionDocument24 pagesOmnichannel DistributionHarisvan To SevenNo ratings yet

- Practical Account 01 Es QuDocument718 pagesPractical Account 01 Es QuMozahar Sujon100% (1)

- Chapter 2 - Correction of Errors PDFDocument12 pagesChapter 2 - Correction of Errors PDFRonald90% (10)

- ACC 577 Quiz Week 2Document11 pagesACC 577 Quiz Week 2MaryNo ratings yet

- Republic of The Philippines Department of Education Public Technical - Vocational High SchoolsDocument34 pagesRepublic of The Philippines Department of Education Public Technical - Vocational High SchoolsKristel AcordonNo ratings yet

- Solution To Quiz 2Document4 pagesSolution To Quiz 2GianJoshuaDayritNo ratings yet

- Relevant Costing ReviewerDocument4 pagesRelevant Costing Reviewerdaniellejueco1228No ratings yet

- Chapter3 - Costing Methods The Costing of Resource OutputsDocument27 pagesChapter3 - Costing Methods The Costing of Resource OutputsNetsanet Belay100% (1)

- Cost Accounting Hilton 13Document10 pagesCost Accounting Hilton 13Vin TenNo ratings yet

- Summative QuizDocument2 pagesSummative QuizVIRGIL KIT AUGUSTIN ABANILLANo ratings yet

- Ma Project FMCG-: Marico, Itc, Colgate, Unilever, Yili, PepsicoDocument12 pagesMa Project FMCG-: Marico, Itc, Colgate, Unilever, Yili, PepsicoJasneet BaidNo ratings yet

- CH 09Document69 pagesCH 09Navindra Jaggernauth100% (1)

- Final Dissertation Elearning Chitunha PDFDocument66 pagesFinal Dissertation Elearning Chitunha PDFLinos TichazorwaNo ratings yet

- CH 4Document72 pagesCH 4Chang Chan ChongNo ratings yet

- Material CostingDocument18 pagesMaterial CostingRaj KumarNo ratings yet

- Ne Malai - 7 - Exercise CalculationDocument30 pagesNe Malai - 7 - Exercise CalculationNemalai VitalNo ratings yet

- Test Bank Accounting 25th Editon Warren Chapter 22 BudgetingDocument94 pagesTest Bank Accounting 25th Editon Warren Chapter 22 BudgetingAngely May Jordan100% (1)

- Dispensers of California (Jeff)Document9 pagesDispensers of California (Jeff)Jeffery KaoNo ratings yet

- Chapter 13 - Gross Profit MethodDocument7 pagesChapter 13 - Gross Profit MethodLorence IbañezNo ratings yet

- Account For MaterialDocument25 pagesAccount For Materialshrestha.aryxnNo ratings yet

- CostConExercise - COGM & COGSDocument3 pagesCostConExercise - COGM & COGSLee Tarroza100% (1)

- Standard Costing - A LevelDocument3 pagesStandard Costing - A LevelMUSTHARI KHANNo ratings yet

- Compilation of Assignments in Cost AccountingDocument9 pagesCompilation of Assignments in Cost AccountingCaia VelazquezNo ratings yet

- Fifo Method and Debt Held As MaturityDocument3 pagesFifo Method and Debt Held As MaturitysninaricaNo ratings yet

- Management TheoryDocument63 pagesManagement TheoryFaisal Ibrahim100% (2)

- CHAPTER 2 - Partnership OperationsDocument10 pagesCHAPTER 2 - Partnership OperationsRominna Dela RuedaNo ratings yet

- Papers of Cost AccountingDocument8 pagesPapers of Cost AccountingTalha BukhariNo ratings yet

- Terminal Report Siosig Edited 02Document37 pagesTerminal Report Siosig Edited 02briandss123No ratings yet