Download as pptx, pdf, or txt

You might also like

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- Modes of Disbursements (ATA)Document44 pagesModes of Disbursements (ATA)Maria Julieta Stephanie Tacogue100% (2)

- MCQ On VAT Audit GuidelinesDocument3 pagesMCQ On VAT Audit GuidelinesVikash KumarNo ratings yet

- Lecture Notes On Process of TenderingDocument23 pagesLecture Notes On Process of TenderingArifNo ratings yet

- Advance Ruling Principle Under Income Tax Act 1961Document44 pagesAdvance Ruling Principle Under Income Tax Act 1961Zaheer UsmanNo ratings yet

- Procedure and Practical Approach in Dealing With Appeal Before Commissioner of Income Tax (Appeals)Document34 pagesProcedure and Practical Approach in Dealing With Appeal Before Commissioner of Income Tax (Appeals)mani712fcaNo ratings yet

- Maharashtra VAT Assessment AnalysisDocument6 pagesMaharashtra VAT Assessment AnalysisSagar TeliNo ratings yet

- Lecture Notes On Bidding ProcessDocument20 pagesLecture Notes On Bidding ProcessArifNo ratings yet

- Taxation 2 Power Point Part 2Document32 pagesTaxation 2 Power Point Part 2Vince Q. Matutina100% (1)

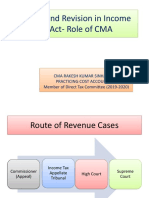

- CMA Rakesh Sinha 2Document25 pagesCMA Rakesh Sinha 2Subrata BindhaniNo ratings yet

- 8 CaroDocument45 pages8 CaroAnupam BaliNo ratings yet

- Important Notes On Assessment Procedure Under Income Tax Act-1961Document16 pagesImportant Notes On Assessment Procedure Under Income Tax Act-1961vip_85No ratings yet

- Assessment Procedure Model QnsDocument31 pagesAssessment Procedure Model QnsRitsikaGurramNo ratings yet

- Professional Ethics - , Accountancy For Lawyers and Bench-BarDocument27 pagesProfessional Ethics - , Accountancy For Lawyers and Bench-BarArpan Kamal100% (6)

- CIR v. Phil. Global Communications, IncDocument3 pagesCIR v. Phil. Global Communications, IncGain DeeNo ratings yet

- 19 Assessment Audit Recovery - TaxationDocument11 pages19 Assessment Audit Recovery - TaxationTayyaba YounasNo ratings yet

- 9 Assessment ProcedureDocument5 pages9 Assessment ProcedureHarry Singh ButtarNo ratings yet

- Notes 230604 181745 280Document2 pagesNotes 230604 181745 280Riya RajNo ratings yet

- Update On Taxpayers Rights Remedies VicMamalateoDocument53 pagesUpdate On Taxpayers Rights Remedies VicMamalateoNimpa PichayNo ratings yet

- Mutations CircularDocument4 pagesMutations CircularARUN SHOWRI ADVOCATENo ratings yet

- Income Tax - MidhunDocument19 pagesIncome Tax - MidhunmidhunNo ratings yet

- RA 9184 Slides (3) - Atty. TomDocument32 pagesRA 9184 Slides (3) - Atty. TomrickmortyNo ratings yet

- Arun Singh AssesmentDocument27 pagesArun Singh Assesmentdeepak singhNo ratings yet

- Wmec Cit (A) PPT 2023Document38 pagesWmec Cit (A) PPT 2023mani712fcaNo ratings yet

- Audit Documentation: Presented By: Mr. Francis H. VillaminDocument34 pagesAudit Documentation: Presented By: Mr. Francis H. VillaminnaddieNo ratings yet

- Assessment, Provisional Assessment & AuditDocument21 pagesAssessment, Provisional Assessment & AuditMithun BiswasNo ratings yet

- Professional Ethics', Accountancy For Lawyers and Bench-Bar RelationsDocument27 pagesProfessional Ethics', Accountancy For Lawyers and Bench-Bar RelationsSrinivasu YennetiNo ratings yet

- T.002 The Certification Process General Requirements - PDFDocument22 pagesT.002 The Certification Process General Requirements - PDFMuhamad FarikinNo ratings yet

- It Act - Part IiDocument249 pagesIt Act - Part IiKritika SinghNo ratings yet

- Appeal and Revision PDFDocument5 pagesAppeal and Revision PDFmonicaNo ratings yet

- 2020 Boiler Pressure Vessel CodeDocument61 pages2020 Boiler Pressure Vessel CodemohdfirdausNo ratings yet

- Overview of Companies (Auditor's Report) Order 2003Document45 pagesOverview of Companies (Auditor's Report) Order 2003Kshitiz JainNo ratings yet

- Draft Show Cause Notice-Ac/ Adc-CompetencyDocument2 pagesDraft Show Cause Notice-Ac/ Adc-Competencygolu.abhishek95No ratings yet

- All Forms Performancedata Fy2014 Qtr3Document1 pageAll Forms Performancedata Fy2014 Qtr3Ga AgNo ratings yet

- Tax - Sinhala Appeals PDFDocument38 pagesTax - Sinhala Appeals PDFIsuruNo ratings yet

- Npa RevisedDocument22 pagesNpa RevisedBalwinder Singh ABROLNo ratings yet

- Main Stages in Power Station ErectionDocument38 pagesMain Stages in Power Station ErectionSam75% (4)

- NpaDocument15 pagesNpaKaibalyaprasad MallickNo ratings yet

- List of Schedules For AuditDocument6 pagesList of Schedules For Auditapi-3705645100% (3)

- Assessment Singst by CA Ashok BatraDocument66 pagesAssessment Singst by CA Ashok BatraNahid ParweenNo ratings yet

- Assess Audit 22022018Document33 pagesAssess Audit 22022018Suresh Kumar YathirajuNo ratings yet

- C ' C - A C D: Itizens Harter Ssessment Ollection EpartmentDocument20 pagesC ' C - A C D: Itizens Harter Ssessment Ollection EpartmentpaupermNo ratings yet

- Authority For Advance RulingDocument9 pagesAuthority For Advance RulingTreesa Mary RejiNo ratings yet

- Mar AdmLaw 6Document35 pagesMar AdmLaw 6Khairil AzmanNo ratings yet

- Procedures For Reopening After Temporary Closure Due To COVID-19Document6 pagesProcedures For Reopening After Temporary Closure Due To COVID-19Tony Garcia100% (4)

- CA Roopa NayakDocument40 pagesCA Roopa NayakAayushi AroraNo ratings yet

- 0182 00103546 03Document1 page0182 00103546 03Junaid MirNo ratings yet

- COA Circular 2019-002- Audit Jurisidiction of Relief and Write-OffDocument2 pagesCOA Circular 2019-002- Audit Jurisidiction of Relief and Write-OffMa Angelica Grace AbanNo ratings yet

- CIR Vs Phil. GlobalDocument3 pagesCIR Vs Phil. GlobalPiaNo ratings yet

- Nirc Local Taxation Real Property Taxation Prescriptive Period: AssessmentDocument2 pagesNirc Local Taxation Real Property Taxation Prescriptive Period: AssessmentJovie Hernandez-MiraplesNo ratings yet

- Fundamentals of Bookkeeping: Ucpb Savings Bank Operations DivisionDocument71 pagesFundamentals of Bookkeeping: Ucpb Savings Bank Operations DivisionJames ToNo ratings yet

- Survey DrydockDocument20 pagesSurvey DrydockHarshad Tallur100% (3)

- Navigating Black Money (TaxDocument28 pagesNavigating Black Money (Taxaliciag4342No ratings yet

- Model Policies and Procedures for Not-for-Profit OrganizationsFrom EverandModel Policies and Procedures for Not-for-Profit OrganizationsNo ratings yet

- Wiley Practitioner's Guide to GAAS 2023: Covering All SASs, SSAEs, SSARSs, and InterpretationsFrom EverandWiley Practitioner's Guide to GAAS 2023: Covering All SASs, SSAEs, SSARSs, and InterpretationsNo ratings yet

- Customs Act, 1962 - FA'17 - Sec 25-43Document24 pagesCustoms Act, 1962 - FA'17 - Sec 25-43Vikash KumarNo ratings yet

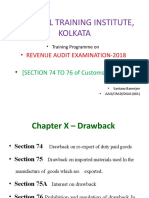

- Regional Training Institute, Kolkata: - Revenue Audit Examination-2018Document17 pagesRegional Training Institute, Kolkata: - Revenue Audit Examination-2018Vikash KumarNo ratings yet

- Multiple Choice QuestionDocument6 pagesMultiple Choice QuestionVikash KumarNo ratings yet

- List of ContentsDocument7 pagesList of ContentsVikash KumarNo ratings yet

- Need For Electricity Act 2003Document1 pageNeed For Electricity Act 2003Vikash KumarNo ratings yet

- Indian Contract Act - 1872 - NewDocument23 pagesIndian Contract Act - 1872 - NewVikash KumarNo ratings yet

- Overview - Administrative Functions: August 2016Document35 pagesOverview - Administrative Functions: August 2016Vikash KumarNo ratings yet

- Step by Step Process AssessmentDocument14 pagesStep by Step Process AssessmentVikash KumarNo ratings yet

- Public Procurement BillDocument4 pagesPublic Procurement BillVikash KumarNo ratings yet