Download as ppt, pdf, or txt

You might also like

- Demolition Planning PDFDocument12 pagesDemolition Planning PDFimanbilly67% (3)

- Chap 007Document37 pagesChap 007AhsanNo ratings yet

- Variable Costing: A Tool For Management: Chapter SevenDocument37 pagesVariable Costing: A Tool For Management: Chapter SevenJavier TsangNo ratings yet

- Inventory Costing: Chapter NineDocument39 pagesInventory Costing: Chapter NineDio VinosaNo ratings yet

- Chap007 27102021 110417amDocument30 pagesChap007 27102021 110417amAzaz IftikharNo ratings yet

- Variable Costing: A Tool For Management: © 2010 The Mcgraw-Hill Companies, IncDocument30 pagesVariable Costing: A Tool For Management: © 2010 The Mcgraw-Hill Companies, IncInga ApseNo ratings yet

- Variable Costing: A Tool For ManagementDocument37 pagesVariable Costing: A Tool For ManagementumakantanayakNo ratings yet

- Variable Costing and Segment Reporting: Tools For ManagementDocument66 pagesVariable Costing and Segment Reporting: Tools For ManagementsofiaNo ratings yet

- Variable Costing: A Tool For Management: Chapter SevenDocument40 pagesVariable Costing: A Tool For Management: Chapter SevenFitzmore Peters100% (1)

- Variable Costing - PPT - 20231130 - 092302 - 0000Document43 pagesVariable Costing - PPT - 20231130 - 092302 - 00002230356No ratings yet

- Variable Costing: A Tool For ManagementDocument37 pagesVariable Costing: A Tool For ManagementAsif Ahmed AnikNo ratings yet

- Variable Costing and Segment Reporting: Tools For ManagementDocument68 pagesVariable Costing and Segment Reporting: Tools For ManagementAqsa KhanNo ratings yet

- 11 Edition: Mcgraw Hill/IrwinDocument9 pages11 Edition: Mcgraw Hill/Irwinakash10107No ratings yet

- 11 Edition: Mcgraw-Hill/IrwinDocument93 pages11 Edition: Mcgraw-Hill/IrwinrisaNo ratings yet

- VariableDocument44 pagesVariablethareendaNo ratings yet

- Chapter 02Document47 pagesChapter 02Fadumo ZahraNo ratings yet

- Chapter - 6 - Variable Costing and Segment Tools For ManagementDocument66 pagesChapter - 6 - Variable Costing and Segment Tools For Managementshamsirarefin275285No ratings yet

- Varince AnalysisDocument79 pagesVarince Analysisarshad mNo ratings yet

- Dasar Akmen 4 - Variable Costing and Full CostingDocument42 pagesDasar Akmen 4 - Variable Costing and Full CostingDiandra OlivianiNo ratings yet

- Variable Costing: A Tool For Management: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Document79 pagesVariable Costing: A Tool For Management: Garrison, Noreen, Brewer, Cheng & Yuen Mcgraw-Hill Education (Asia)Chincel G. ANINo ratings yet

- 8.31 - Standard CostingDocument109 pages8.31 - Standard CostingBhosx Kim100% (1)

- Cost Behavior: Analysis and Use: Chapter FiveDocument62 pagesCost Behavior: Analysis and Use: Chapter FiveJenny ManaladNo ratings yet

- Standard Costing PDFDocument143 pagesStandard Costing PDFYsabelle VillavicencioNo ratings yet

- Cost Concepts and BehaviorsDocument41 pagesCost Concepts and BehaviorslongphungspNo ratings yet

- Standard Costs and Operating Performance MeasuresDocument70 pagesStandard Costs and Operating Performance MeasuresdianaNo ratings yet

- Chapter 2editDocument33 pagesChapter 2editCherry SeasonNo ratings yet

- Cost Behavior: Analysis and Use: Chapter FiveDocument60 pagesCost Behavior: Analysis and Use: Chapter Fiveayesha125865No ratings yet

- Cost Terms and ClassificationsDocument53 pagesCost Terms and ClassificationsMd. Fahim Faysal Sumon 191-11-763No ratings yet

- Standard CostDocument16 pagesStandard CostRozibul BasarNo ratings yet

- Cost Concepts & ClassificationDocument65 pagesCost Concepts & ClassificationPrio DebnathNo ratings yet

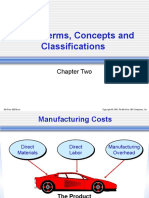

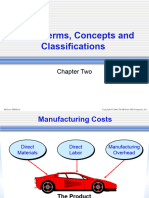

- Cost Terms, Concepts and Classifications: Chapter TwoDocument270 pagesCost Terms, Concepts and Classifications: Chapter TwoDania Al-ȜbadiNo ratings yet

- Standard Costs and The Balanced Scorecard: Mcgraw-Hill/IrwinDocument41 pagesStandard Costs and The Balanced Scorecard: Mcgraw-Hill/IrwinShamittaaNo ratings yet

- Standard Costs and The Balanced Scorecard: Mcgraw-Hill/IrwinDocument101 pagesStandard Costs and The Balanced Scorecard: Mcgraw-Hill/IrwinSyed Ijlal HaiderNo ratings yet

- Syndicate 2 Accounting CasesDocument28 pagesSyndicate 2 Accounting CasesKrishna RaiNo ratings yet

- Chap004 7e EditedDocument47 pagesChap004 7e EditedfarahNo ratings yet

- Costs Terms, Concepts and Classifications: Chapter TwoDocument78 pagesCosts Terms, Concepts and Classifications: Chapter Twosaka haiNo ratings yet

- Process Costing: Mcgraw-Hill/IrwinDocument46 pagesProcess Costing: Mcgraw-Hill/IrwinRoberto NinoNo ratings yet

- SChap3. Job-Order CostingDocument12 pagesSChap3. Job-Order Costinglao porphengNo ratings yet

- Standard Cost & VarianceDocument26 pagesStandard Cost & VarianceWaqar AhmadNo ratings yet

- An Organization - . .: Managing Resources, Activities, and PeopleDocument35 pagesAn Organization - . .: Managing Resources, Activities, and PeopleAyush RajoriyaNo ratings yet

- Analisa Biaya 8 Process CostingDocument74 pagesAnalisa Biaya 8 Process CostingBrian HuangNo ratings yet

- ABC Analysis HandoutsDocument11 pagesABC Analysis HandoutsTushar DuaNo ratings yet

- Costs Terms, Concepts and Classifications: Chapter TwoDocument80 pagesCosts Terms, Concepts and Classifications: Chapter TwoNoor ShinwariNo ratings yet

- DMMR Standard CostingDocument80 pagesDMMR Standard CostingArmanul HaqueNo ratings yet

- Cost Terms, Concepts and Classifications: Chapter TwoDocument46 pagesCost Terms, Concepts and Classifications: Chapter Twomusic lover PHNo ratings yet

- Bab 2 - Perilaku BiayaDocument40 pagesBab 2 - Perilaku BiayaAndy ReynaldyyNo ratings yet

- Bab 2 - Perilaku BiayaDocument40 pagesBab 2 - Perilaku BiayaAndy ReynaldyyNo ratings yet

- Variance AnalysisDocument66 pagesVariance AnalysisSyed Adnan HossainNo ratings yet

- Variance Analysis-Reading MaterialsDocument66 pagesVariance Analysis-Reading MaterialsSM RaselNo ratings yet

- Mcgraw-Hill/Irwin © 2006 The Mcgraw-Hill Companies, Inc., All Rights ReservedDocument24 pagesMcgraw-Hill/Irwin © 2006 The Mcgraw-Hill Companies, Inc., All Rights ReservedHard workerNo ratings yet

- Process CostingDocument76 pagesProcess CostingAnonymous Lz2qH7No ratings yet

- 11 Edition: Mcgraw-Hill/IrwinDocument56 pages11 Edition: Mcgraw-Hill/IrwinmanahilNo ratings yet

- Hms 02Document64 pagesHms 02JavierNo ratings yet

- Costs Terms, Concepts and Classifications: Chapter TwoDocument66 pagesCosts Terms, Concepts and Classifications: Chapter TwoRabbi RahmanNo ratings yet

- Lec 6Document41 pagesLec 6Nidus PhrykeNo ratings yet

- Chapter 2 Cost Terms Concepts and ClassificationsDocument55 pagesChapter 2 Cost Terms Concepts and ClassificationsJasia MustafaNo ratings yet

- Dokumen - Tips Managerial Accounting Garrison Noreen Brewer Chapter 04Document76 pagesDokumen - Tips Managerial Accounting Garrison Noreen Brewer Chapter 04Arghya BiswasNo ratings yet

- Systems Design: Activity Based Costing: Mcgraw-Hill /irwinDocument55 pagesSystems Design: Activity Based Costing: Mcgraw-Hill /irwinXu FengNo ratings yet

- Chap 02 NotesDocument67 pagesChap 02 NotesNancy HineyNo ratings yet

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageFrom EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageRating: 5 out of 5 stars5/5 (1)

- Module # Topics 4: Unit 4Document15 pagesModule # Topics 4: Unit 4ANNA MARY GINTORONo ratings yet

- Response Letter Reuse Energy - FOMB - PRDE RFPv2Document3 pagesResponse Letter Reuse Energy - FOMB - PRDE RFPv2Metro Puerto RicoNo ratings yet

- Securities QP1Document5 pagesSecurities QP1Max PayneNo ratings yet

- Company Far160Document15 pagesCompany Far160Nur Anis AqilahNo ratings yet

- External Refurbishment Process For Repairable Spares With Serial Number IntegrationDocument11 pagesExternal Refurbishment Process For Repairable Spares With Serial Number IntegrationibrahimNo ratings yet

- SKU # Category Brand: KR20200614 Transportation Not AddedDocument6 pagesSKU # Category Brand: KR20200614 Transportation Not AddedTanmay DasNo ratings yet

- DTF 802Document2 pagesDTF 802Peter R MantiaNo ratings yet

- Business MeetingsDocument32 pagesBusiness Meetingsk225195 Laiba FatimaNo ratings yet

- Ideal+Solution+ +DA+Case+Study+PPT+1Document10 pagesIdeal+Solution+ +DA+Case+Study+PPT+1Abha JainNo ratings yet

- 2023 Summary of Fines To Be CollectedDocument2 pages2023 Summary of Fines To Be Collectedivannavarro230No ratings yet

- Asasah Islamic Micro FinanceDocument34 pagesAsasah Islamic Micro FinanceAlHuda Centre of Islamic Banking & Economics (CIBE)No ratings yet

- Orbit Exchange A Catalyst For Change in Crypto Sports BettingDocument2 pagesOrbit Exchange A Catalyst For Change in Crypto Sports Bettingsportsbettingexchange23No ratings yet

- Capital BudgetingDocument53 pagesCapital Budgeting88ak07No ratings yet

- MBA ProjectDocument72 pagesMBA ProjectBalaji Rao N79% (19)

- Ama Aia - Tax01-Final Exam-Casilla 2nd Sem Ay 2021-2022Document9 pagesAma Aia - Tax01-Final Exam-Casilla 2nd Sem Ay 2021-2022Meg CruzNo ratings yet

- Trio Tech - Oracle Fusion Technical +OIC Course - NewDocument7 pagesTrio Tech - Oracle Fusion Technical +OIC Course - NewssbhattoraNo ratings yet

- 114 Pitney Bowes Model M Postage MeterDocument7 pages114 Pitney Bowes Model M Postage Meterinbox9999No ratings yet

- More Exercises On Theoretical FrameworkDocument9 pagesMore Exercises On Theoretical FrameworkCyrus SantosNo ratings yet

- VA Vol 41 No 3 May June 2013Document31 pagesVA Vol 41 No 3 May June 2013jer galvinNo ratings yet

- Questions For Competitive Markets Type I: True/False Question (Give A Brief Explanation)Document3 pagesQuestions For Competitive Markets Type I: True/False Question (Give A Brief Explanation)Hạnh Đỗ Thị ThanhNo ratings yet

- Golden S Intellectual Property Valuation Case Law CompendiumDocument709 pagesGolden S Intellectual Property Valuation Case Law CompendiumIlya BazaleevNo ratings yet

- MCQ in Engineering Management Part 3 Engineering Board ExamDocument17 pagesMCQ in Engineering Management Part 3 Engineering Board ExamTRICKS MASTERNo ratings yet

- Providence Lawsuit Over Social MediaDocument66 pagesProvidence Lawsuit Over Social MediaNBC 10 WJARNo ratings yet

- Zillow Inc: Form 8-KDocument15 pagesZillow Inc: Form 8-KJohn CookNo ratings yet

- Project HSE TimelineDocument1 pageProject HSE TimelineAri PrastyantoNo ratings yet

- SCM630 - Basic Warehouse MGMTDocument29 pagesSCM630 - Basic Warehouse MGMTKumar Shreshtha100% (1)

- Yes We Hack S.A.S. - General Conditions of Use - 01/25/2023 - Page 1 of 23Document23 pagesYes We Hack S.A.S. - General Conditions of Use - 01/25/2023 - Page 1 of 23reza maulidinNo ratings yet

- 2023-05-25 Calvert County TimesDocument40 pages2023-05-25 Calvert County TimesSouthern Maryland OnlineNo ratings yet

- Technology's Impact On Sales Big DataDocument3 pagesTechnology's Impact On Sales Big DataFardeen LeoNo ratings yet