ACCA F3 CH#10: Accruals and Prepayments Notes

ACCA F3 CH#10: Accruals and Prepayments Notes

You might also like

- Inv Visanet EspanaDocument1 pageInv Visanet Espanakingmonarchy306No ratings yet

- Look Inside Exam Kit Acca Managing Costs and FinanceDocument9 pagesLook Inside Exam Kit Acca Managing Costs and FinanceMobile Mentor100% (1)

- Jessica Alexopoulos Bank StatDocument5 pagesJessica Alexopoulos Bank StatSailing SecretaryNo ratings yet

- TAX BRIEFING-NEW RegistrantsDocument57 pagesTAX BRIEFING-NEW RegistrantsPcl Nueva Vizcaya100% (3)

- Level 3 Costing & MA Text Update June 2021pdfDocument125 pagesLevel 3 Costing & MA Text Update June 2021pdfAmi KayNo ratings yet

- CIMA Practice QnsDocument261 pagesCIMA Practice QnsInnocent Won AberNo ratings yet

- Cash BudgetDocument2 pagesCash BudgetSenthil Kumar0% (1)

- F2 Past Papers and Answers Taha PopatiaDocument320 pagesF2 Past Papers and Answers Taha PopatiaBELONG TO VIRGIN MARYNo ratings yet

- Ajio FL91371963 1568487594186Document1 pageAjio FL91371963 1568487594186Akshay JhawarNo ratings yet

- MA1 BPP Kit (2016) CompletedDocument113 pagesMA1 BPP Kit (2016) CompletedAbdul Wasay AlsyedNo ratings yet

- K-A-K Accruals & Prepayments QuestionsDocument3 pagesK-A-K Accruals & Prepayments QuestionsUmer Farooq0% (1)

- Chapter 6 ACCA F3Document12 pagesChapter 6 ACCA F3siksha100% (1)

- PM January 2021 Lecture 4 Worked Examples Questions (Drury (2012), P. 451, 17.17)Document6 pagesPM January 2021 Lecture 4 Worked Examples Questions (Drury (2012), P. 451, 17.17)KAY PHINE NGNo ratings yet

- Acca F5 Mock Exem QuestionsDocument16 pagesAcca F5 Mock Exem QuestionsGeo DonNo ratings yet

- Ma2 Specimen j14Document16 pagesMa2 Specimen j14talha100% (3)

- Management AccountingDocument223 pagesManagement Accountingcyrus100% (2)

- T1 - Tutorial MaDocument10 pagesT1 - Tutorial Matylee970% (1)

- JB Limited Is A Small Specialist Manufacturer of Electronic ComponentsDocument2 pagesJB Limited Is A Small Specialist Manufacturer of Electronic ComponentsAmit PandeyNo ratings yet

- ACCA F5 Linear Programming RevisionDocument4 pagesACCA F5 Linear Programming RevisionZoe ChimNo ratings yet

- Paper T10 Managing Finances: Sample Multiple Choice Questions - June 2009Document174 pagesPaper T10 Managing Finances: Sample Multiple Choice Questions - June 2009Khánh LyNo ratings yet

- CH 10 Accruals and PrepaymentsDocument8 pagesCH 10 Accruals and PrepaymentsBuntheaNo ratings yet

- ACCA F3 CH#10: Accruals and Prepayments Practice NotesDocument13 pagesACCA F3 CH#10: Accruals and Prepayments Practice NotesMuhammad AzamNo ratings yet

- Past Papers - Partnership ChangesDocument10 pagesPast Papers - Partnership ChangesFarhan JehangirNo ratings yet

- Answer 1 - Cost of CapitalDocument2 pagesAnswer 1 - Cost of Capitaljeganrajraj100% (1)

- Functional BudgetsDocument12 pagesFunctional Budgetsarjun sachdev100% (1)

- Test of Labour Overheads and Absorption and Marginal CostingDocument4 pagesTest of Labour Overheads and Absorption and Marginal CostingzairaNo ratings yet

- Absorption and Margin CostingDocument8 pagesAbsorption and Margin CostingIshfaq AhmadNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesDocument40 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesMuhammad AzamNo ratings yet

- Chap 1 - Inventory Valuation (Questions)Document4 pagesChap 1 - Inventory Valuation (Questions)90 SHAMAZNo ratings yet

- Orchid LimitedDocument3 pagesOrchid LimitedANo ratings yet

- Budget AnswersDocument6 pagesBudget AnswersSushant MaskeyNo ratings yet

- Chapter 15 From Textbook T.S. Grewal (2018) For Class 11 ACCOUNTANCYDocument59 pagesChapter 15 From Textbook T.S. Grewal (2018) For Class 11 ACCOUNTANCYvkbm42100% (2)

- Lesson 3: Linear ProgrammingDocument31 pagesLesson 3: Linear ProgrammingYi WeiNo ratings yet

- IAS 2 Summary-MergedDocument19 pagesIAS 2 Summary-MergedShameel IrshadNo ratings yet

- Chapter 14-Ch. 14-Cash Flow Estimation 11-13.El-Bigbee Bottling CompanyDocument1 pageChapter 14-Ch. 14-Cash Flow Estimation 11-13.El-Bigbee Bottling CompanyRajib DahalNo ratings yet

- Chapter 18 ACCA F3Document6 pagesChapter 18 ACCA F3sikshaNo ratings yet

- Manufacturing-Accounts Teaching GuideDocument26 pagesManufacturing-Accounts Teaching GuidekimringineNo ratings yet

- Chapter 17 - Control AccountsDocument17 pagesChapter 17 - Control Accountsshemida75% (4)

- 9706 Y16 SP 3Document10 pages9706 Y16 SP 3Wi Mae RiNo ratings yet

- FA Consolidation Test - Questions S20-A21 PDFDocument16 pagesFA Consolidation Test - Questions S20-A21 PDFAlpha MpofuNo ratings yet

- Acca f2 Management Accountant Topicwise Past PapersDocument44 pagesAcca f2 Management Accountant Topicwise Past PapersIkram Naguib100% (2)

- MA2 CGA Sept'11 ExamDocument21 pagesMA2 CGA Sept'11 ExamumgilkinNo ratings yet

- Cost Sheet QuestionsDocument5 pagesCost Sheet QuestionsDrimit GhosalNo ratings yet

- 11 Accruals and PrepaymentsDocument1 page11 Accruals and PrepaymentsNadia AhmedNo ratings yet

- F2 Past Paper - Ans06-2004Document10 pagesF2 Past Paper - Ans06-2004ArsalanACCANo ratings yet

- Fma Past Papers 1Document23 pagesFma Past Papers 1Fatuma Coco BuddaflyNo ratings yet

- CAF 1 IA Autumn 2020Document5 pagesCAF 1 IA Autumn 2020Qasim Hafeez KhokharNo ratings yet

- Limiting Factors & Linear ProgrammingDocument8 pagesLimiting Factors & Linear ProgrammingMohammad Faizan Farooq Qadri AttariNo ratings yet

- Answer Key Accounting Paper 2 Term 3 Form 4Document8 pagesAnswer Key Accounting Paper 2 Term 3 Form 4Aejaz MohamedNo ratings yet

- Practice Questions For Ias 16Document6 pagesPractice Questions For Ias 16Uman Imran,56No ratings yet

- Notes On Inventory ValuationDocument7 pagesNotes On Inventory ValuationNouman Mujahid100% (2)

- 7 2006 Dec QDocument6 pages7 2006 Dec Qapi-19836745No ratings yet

- 01 Accruals and Prepayments TestDocument13 pages01 Accruals and Prepayments TestThomas Kong Ying Li100% (1)

- BOOK LIST 2021 - 2022 Grade IX Compulsory SubjectsDocument2 pagesBOOK LIST 2021 - 2022 Grade IX Compulsory SubjectsaslamNo ratings yet

- Solutions To Text Book Exercises: Non-Trading ConcernsDocument12 pagesSolutions To Text Book Exercises: Non-Trading ConcernsM JEEVARATHNAM NAIDUNo ratings yet

- Chapter # 1: Accounting For Incomplete Records (Single Entry)Document24 pagesChapter # 1: Accounting For Incomplete Records (Single Entry)Umar Zahid100% (1)

- Chapter 21Document4 pagesChapter 21Rahila RafiqNo ratings yet

- Accounting Problem Book 2011 PDFDocument103 pagesAccounting Problem Book 2011 PDFViệt Đức Lê67% (3)

- Chapter 9 Marginal Costing and Absorption CostingDocument7 pagesChapter 9 Marginal Costing and Absorption CostingLinyVatNo ratings yet

- Irrecoverable Debts ReviewDocument11 pagesIrrecoverable Debts ReviewThidarothNo ratings yet

- FA 2 Practice Test Set 3Document13 pagesFA 2 Practice Test Set 3Chhour Thalika0% (1)

- Acct101-3 - (Your Name)Document9 pagesAcct101-3 - (Your Name)Vedanshi BihaniNo ratings yet

- Accruals and PrepaymentsDocument28 pagesAccruals and Prepaymentsvpq7qcwszyNo ratings yet

- Accruals & Prepayment-1Document3 pagesAccruals & Prepayment-1Kopanang LeokanaNo ratings yet

- ACCA F3 CH#10: Accruals and Prepayments Practice NotesDocument13 pagesACCA F3 CH#10: Accruals and Prepayments Practice NotesMuhammad AzamNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesDocument40 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesMuhammad AzamNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts Practice NotesDocument11 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts Practice NotesMuhammad AzamNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts Practice NotesDocument3 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts Practice NotesMuhammad AzamNo ratings yet

- Income Taxation DrillsDocument10 pagesIncome Taxation DrillsResty VillaroelNo ratings yet

- RealmeDocument1 pageRealmePíyûshGuptaNo ratings yet

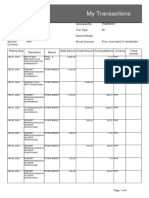

- My Transactions PDFDocument6 pagesMy Transactions PDFgeorgina woelkeNo ratings yet

- Samsung Fest Amazonpay Offer TNCDocument3 pagesSamsung Fest Amazonpay Offer TNCmaheshNo ratings yet

- Form 173 Score Report Form PDFDocument3 pagesForm 173 Score Report Form PDFbarneylovesbagelsNo ratings yet

- Oman Income TaxDocument84 pagesOman Income TaxsoumenNo ratings yet

- Statement 16 02Document2 pagesStatement 16 02kerembonov761No ratings yet

- ATX MYS - Examinable Documents Guidance Notes - 2020 0ct-2021sept - FINALDocument3 pagesATX MYS - Examinable Documents Guidance Notes - 2020 0ct-2021sept - FINALAmy LauNo ratings yet

- Subramani PayslipDocument2 pagesSubramani PayslipMr. HarshaNo ratings yet

- ICCT Colleges Foundation, Inc.: - Activity / AssignmentDocument2 pagesICCT Colleges Foundation, Inc.: - Activity / AssignmentDamayan XeroxanNo ratings yet

- Life Long Gas Stove Bill InvoiceDocument1 pageLife Long Gas Stove Bill Invoicesreenivas100% (1)

- Tasco: Fosma Maritime Institute & Research OrganisationDocument2 pagesTasco: Fosma Maritime Institute & Research OrganisationRahul GuptaNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument16 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancevedhasai198No ratings yet

- 2nd QuarterDocument112 pages2nd QuarterRodnel MonceraNo ratings yet

- 2017 TXN - TXT 2 - PDF - BitcoinDocument4 pages2017 TXN - TXT 2 - PDF - BitcoinDaniel NaeNo ratings yet

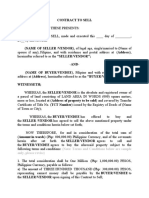

- Contract To Sell: (Note: Terms and Conditions Below Are Sample Only, Please Revise)Document3 pagesContract To Sell: (Note: Terms and Conditions Below Are Sample Only, Please Revise)JANNNo ratings yet

- MBBcurrent 014075169296 2023-10-31Document2 pagesMBBcurrent 014075169296 2023-10-31zulapimasiranNo ratings yet

- Division - Alabang Supermarket v. City Government of MuntinlupaDocument8 pagesDivision - Alabang Supermarket v. City Government of MuntinlupaPaul Joshua SubaNo ratings yet

- Taxation E211 2017 12 4ED - RDocument95 pagesTaxation E211 2017 12 4ED - RSaid Safa TurabiNo ratings yet

- Evolution of Taxation in The PhilippinesDocument10 pagesEvolution of Taxation in The PhilippinesCarlos Baul David100% (1)

- Account Statement From 20 Apr 2022 To 4 May 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 20 Apr 2022 To 4 May 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRajkumar GopalanNo ratings yet

- Debit CardDocument3 pagesDebit CardNeelofar AzeemNo ratings yet

- Primerica Debt ResolutionDocument0 pagesPrimerica Debt ResolutionDesmon FlonnoryNo ratings yet

- Diamond 3:10 PDFDocument1 pageDiamond 3:10 PDFChris LeeNo ratings yet

- TADAT Field Guide - 2019 (Approved - FINAL MASTER COPY)Document198 pagesTADAT Field Guide - 2019 (Approved - FINAL MASTER COPY)Maarten De ZeeuwNo ratings yet

- Jordan InvoiceDocument2 pagesJordan InvoiceKrishna Beriwal0% (1)

Download as pptx, pdf, or txt

You might also like

- Inv Visanet EspanaDocument1 pageInv Visanet Espanakingmonarchy306No ratings yet

- Look Inside Exam Kit Acca Managing Costs and FinanceDocument9 pagesLook Inside Exam Kit Acca Managing Costs and FinanceMobile Mentor100% (1)

- Jessica Alexopoulos Bank StatDocument5 pagesJessica Alexopoulos Bank StatSailing SecretaryNo ratings yet

- TAX BRIEFING-NEW RegistrantsDocument57 pagesTAX BRIEFING-NEW RegistrantsPcl Nueva Vizcaya100% (3)

- Level 3 Costing & MA Text Update June 2021pdfDocument125 pagesLevel 3 Costing & MA Text Update June 2021pdfAmi KayNo ratings yet

- CIMA Practice QnsDocument261 pagesCIMA Practice QnsInnocent Won AberNo ratings yet

- Cash BudgetDocument2 pagesCash BudgetSenthil Kumar0% (1)

- F2 Past Papers and Answers Taha PopatiaDocument320 pagesF2 Past Papers and Answers Taha PopatiaBELONG TO VIRGIN MARYNo ratings yet

- Ajio FL91371963 1568487594186Document1 pageAjio FL91371963 1568487594186Akshay JhawarNo ratings yet

- MA1 BPP Kit (2016) CompletedDocument113 pagesMA1 BPP Kit (2016) CompletedAbdul Wasay AlsyedNo ratings yet

- K-A-K Accruals & Prepayments QuestionsDocument3 pagesK-A-K Accruals & Prepayments QuestionsUmer Farooq0% (1)

- Chapter 6 ACCA F3Document12 pagesChapter 6 ACCA F3siksha100% (1)

- PM January 2021 Lecture 4 Worked Examples Questions (Drury (2012), P. 451, 17.17)Document6 pagesPM January 2021 Lecture 4 Worked Examples Questions (Drury (2012), P. 451, 17.17)KAY PHINE NGNo ratings yet

- Acca F5 Mock Exem QuestionsDocument16 pagesAcca F5 Mock Exem QuestionsGeo DonNo ratings yet

- Ma2 Specimen j14Document16 pagesMa2 Specimen j14talha100% (3)

- Management AccountingDocument223 pagesManagement Accountingcyrus100% (2)

- T1 - Tutorial MaDocument10 pagesT1 - Tutorial Matylee970% (1)

- JB Limited Is A Small Specialist Manufacturer of Electronic ComponentsDocument2 pagesJB Limited Is A Small Specialist Manufacturer of Electronic ComponentsAmit PandeyNo ratings yet

- ACCA F5 Linear Programming RevisionDocument4 pagesACCA F5 Linear Programming RevisionZoe ChimNo ratings yet

- Paper T10 Managing Finances: Sample Multiple Choice Questions - June 2009Document174 pagesPaper T10 Managing Finances: Sample Multiple Choice Questions - June 2009Khánh LyNo ratings yet

- CH 10 Accruals and PrepaymentsDocument8 pagesCH 10 Accruals and PrepaymentsBuntheaNo ratings yet

- ACCA F3 CH#10: Accruals and Prepayments Practice NotesDocument13 pagesACCA F3 CH#10: Accruals and Prepayments Practice NotesMuhammad AzamNo ratings yet

- Past Papers - Partnership ChangesDocument10 pagesPast Papers - Partnership ChangesFarhan JehangirNo ratings yet

- Answer 1 - Cost of CapitalDocument2 pagesAnswer 1 - Cost of Capitaljeganrajraj100% (1)

- Functional BudgetsDocument12 pagesFunctional Budgetsarjun sachdev100% (1)

- Test of Labour Overheads and Absorption and Marginal CostingDocument4 pagesTest of Labour Overheads and Absorption and Marginal CostingzairaNo ratings yet

- Absorption and Margin CostingDocument8 pagesAbsorption and Margin CostingIshfaq AhmadNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesDocument40 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesMuhammad AzamNo ratings yet

- Chap 1 - Inventory Valuation (Questions)Document4 pagesChap 1 - Inventory Valuation (Questions)90 SHAMAZNo ratings yet

- Orchid LimitedDocument3 pagesOrchid LimitedANo ratings yet

- Budget AnswersDocument6 pagesBudget AnswersSushant MaskeyNo ratings yet

- Chapter 15 From Textbook T.S. Grewal (2018) For Class 11 ACCOUNTANCYDocument59 pagesChapter 15 From Textbook T.S. Grewal (2018) For Class 11 ACCOUNTANCYvkbm42100% (2)

- Lesson 3: Linear ProgrammingDocument31 pagesLesson 3: Linear ProgrammingYi WeiNo ratings yet

- IAS 2 Summary-MergedDocument19 pagesIAS 2 Summary-MergedShameel IrshadNo ratings yet

- Chapter 14-Ch. 14-Cash Flow Estimation 11-13.El-Bigbee Bottling CompanyDocument1 pageChapter 14-Ch. 14-Cash Flow Estimation 11-13.El-Bigbee Bottling CompanyRajib DahalNo ratings yet

- Chapter 18 ACCA F3Document6 pagesChapter 18 ACCA F3sikshaNo ratings yet

- Manufacturing-Accounts Teaching GuideDocument26 pagesManufacturing-Accounts Teaching GuidekimringineNo ratings yet

- Chapter 17 - Control AccountsDocument17 pagesChapter 17 - Control Accountsshemida75% (4)

- 9706 Y16 SP 3Document10 pages9706 Y16 SP 3Wi Mae RiNo ratings yet

- FA Consolidation Test - Questions S20-A21 PDFDocument16 pagesFA Consolidation Test - Questions S20-A21 PDFAlpha MpofuNo ratings yet

- Acca f2 Management Accountant Topicwise Past PapersDocument44 pagesAcca f2 Management Accountant Topicwise Past PapersIkram Naguib100% (2)

- MA2 CGA Sept'11 ExamDocument21 pagesMA2 CGA Sept'11 ExamumgilkinNo ratings yet

- Cost Sheet QuestionsDocument5 pagesCost Sheet QuestionsDrimit GhosalNo ratings yet

- 11 Accruals and PrepaymentsDocument1 page11 Accruals and PrepaymentsNadia AhmedNo ratings yet

- F2 Past Paper - Ans06-2004Document10 pagesF2 Past Paper - Ans06-2004ArsalanACCANo ratings yet

- Fma Past Papers 1Document23 pagesFma Past Papers 1Fatuma Coco BuddaflyNo ratings yet

- CAF 1 IA Autumn 2020Document5 pagesCAF 1 IA Autumn 2020Qasim Hafeez KhokharNo ratings yet

- Limiting Factors & Linear ProgrammingDocument8 pagesLimiting Factors & Linear ProgrammingMohammad Faizan Farooq Qadri AttariNo ratings yet

- Answer Key Accounting Paper 2 Term 3 Form 4Document8 pagesAnswer Key Accounting Paper 2 Term 3 Form 4Aejaz MohamedNo ratings yet

- Practice Questions For Ias 16Document6 pagesPractice Questions For Ias 16Uman Imran,56No ratings yet

- Notes On Inventory ValuationDocument7 pagesNotes On Inventory ValuationNouman Mujahid100% (2)

- 7 2006 Dec QDocument6 pages7 2006 Dec Qapi-19836745No ratings yet

- 01 Accruals and Prepayments TestDocument13 pages01 Accruals and Prepayments TestThomas Kong Ying Li100% (1)

- BOOK LIST 2021 - 2022 Grade IX Compulsory SubjectsDocument2 pagesBOOK LIST 2021 - 2022 Grade IX Compulsory SubjectsaslamNo ratings yet

- Solutions To Text Book Exercises: Non-Trading ConcernsDocument12 pagesSolutions To Text Book Exercises: Non-Trading ConcernsM JEEVARATHNAM NAIDUNo ratings yet

- Chapter # 1: Accounting For Incomplete Records (Single Entry)Document24 pagesChapter # 1: Accounting For Incomplete Records (Single Entry)Umar Zahid100% (1)

- Chapter 21Document4 pagesChapter 21Rahila RafiqNo ratings yet

- Accounting Problem Book 2011 PDFDocument103 pagesAccounting Problem Book 2011 PDFViệt Đức Lê67% (3)

- Chapter 9 Marginal Costing and Absorption CostingDocument7 pagesChapter 9 Marginal Costing and Absorption CostingLinyVatNo ratings yet

- Irrecoverable Debts ReviewDocument11 pagesIrrecoverable Debts ReviewThidarothNo ratings yet

- FA 2 Practice Test Set 3Document13 pagesFA 2 Practice Test Set 3Chhour Thalika0% (1)

- Acct101-3 - (Your Name)Document9 pagesAcct101-3 - (Your Name)Vedanshi BihaniNo ratings yet

- Accruals and PrepaymentsDocument28 pagesAccruals and Prepaymentsvpq7qcwszyNo ratings yet

- Accruals & Prepayment-1Document3 pagesAccruals & Prepayment-1Kopanang LeokanaNo ratings yet

- ACCA F3 CH#10: Accruals and Prepayments Practice NotesDocument13 pagesACCA F3 CH#10: Accruals and Prepayments Practice NotesMuhammad AzamNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesDocument40 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts NotesMuhammad AzamNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts Practice NotesDocument11 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts Practice NotesMuhammad AzamNo ratings yet

- ACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts Practice NotesDocument3 pagesACCA F3 CH#5: Sale Returns, Purchases Returns, Discounts Practice NotesMuhammad AzamNo ratings yet

- Income Taxation DrillsDocument10 pagesIncome Taxation DrillsResty VillaroelNo ratings yet

- RealmeDocument1 pageRealmePíyûshGuptaNo ratings yet

- My Transactions PDFDocument6 pagesMy Transactions PDFgeorgina woelkeNo ratings yet

- Samsung Fest Amazonpay Offer TNCDocument3 pagesSamsung Fest Amazonpay Offer TNCmaheshNo ratings yet

- Form 173 Score Report Form PDFDocument3 pagesForm 173 Score Report Form PDFbarneylovesbagelsNo ratings yet

- Oman Income TaxDocument84 pagesOman Income TaxsoumenNo ratings yet

- Statement 16 02Document2 pagesStatement 16 02kerembonov761No ratings yet

- ATX MYS - Examinable Documents Guidance Notes - 2020 0ct-2021sept - FINALDocument3 pagesATX MYS - Examinable Documents Guidance Notes - 2020 0ct-2021sept - FINALAmy LauNo ratings yet

- Subramani PayslipDocument2 pagesSubramani PayslipMr. HarshaNo ratings yet

- ICCT Colleges Foundation, Inc.: - Activity / AssignmentDocument2 pagesICCT Colleges Foundation, Inc.: - Activity / AssignmentDamayan XeroxanNo ratings yet

- Life Long Gas Stove Bill InvoiceDocument1 pageLife Long Gas Stove Bill Invoicesreenivas100% (1)

- Tasco: Fosma Maritime Institute & Research OrganisationDocument2 pagesTasco: Fosma Maritime Institute & Research OrganisationRahul GuptaNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument16 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancevedhasai198No ratings yet

- 2nd QuarterDocument112 pages2nd QuarterRodnel MonceraNo ratings yet

- 2017 TXN - TXT 2 - PDF - BitcoinDocument4 pages2017 TXN - TXT 2 - PDF - BitcoinDaniel NaeNo ratings yet

- Contract To Sell: (Note: Terms and Conditions Below Are Sample Only, Please Revise)Document3 pagesContract To Sell: (Note: Terms and Conditions Below Are Sample Only, Please Revise)JANNNo ratings yet

- MBBcurrent 014075169296 2023-10-31Document2 pagesMBBcurrent 014075169296 2023-10-31zulapimasiranNo ratings yet

- Division - Alabang Supermarket v. City Government of MuntinlupaDocument8 pagesDivision - Alabang Supermarket v. City Government of MuntinlupaPaul Joshua SubaNo ratings yet

- Taxation E211 2017 12 4ED - RDocument95 pagesTaxation E211 2017 12 4ED - RSaid Safa TurabiNo ratings yet

- Evolution of Taxation in The PhilippinesDocument10 pagesEvolution of Taxation in The PhilippinesCarlos Baul David100% (1)

- Account Statement From 20 Apr 2022 To 4 May 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 20 Apr 2022 To 4 May 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRajkumar GopalanNo ratings yet

- Debit CardDocument3 pagesDebit CardNeelofar AzeemNo ratings yet

- Primerica Debt ResolutionDocument0 pagesPrimerica Debt ResolutionDesmon FlonnoryNo ratings yet

- Diamond 3:10 PDFDocument1 pageDiamond 3:10 PDFChris LeeNo ratings yet

- TADAT Field Guide - 2019 (Approved - FINAL MASTER COPY)Document198 pagesTADAT Field Guide - 2019 (Approved - FINAL MASTER COPY)Maarten De ZeeuwNo ratings yet

- Jordan InvoiceDocument2 pagesJordan InvoiceKrishna Beriwal0% (1)