Download as pptx, pdf, or txt

You might also like

- Case 1-2 - Vanguard International Growth FundDocument2 pagesCase 1-2 - Vanguard International Growth FundlauraNo ratings yet

- Articles of Incorporation OF TEKKKA, IncDocument5 pagesArticles of Incorporation OF TEKKKA, IncRandy AgotNo ratings yet

- 4.2 RACI Chart TJDocument1 page4.2 RACI Chart TJTapiwa JeyiNo ratings yet

- Prject Report Financial Statement of NestleDocument14 pagesPrject Report Financial Statement of NestleSumia Hoque NovaNo ratings yet

- A Guide For Testing and Diagnosis of OLTC and Case Study June 2020Document44 pagesA Guide For Testing and Diagnosis of OLTC and Case Study June 2020Ari100% (2)

- BA Outline - FinalDocument32 pagesBA Outline - FinalNathan Yost100% (1)

- Chap11 SolutionDocument29 pagesChap11 SolutionJustine Mark Soberano100% (1)

- Capital Budgeting: An Insight ToDocument26 pagesCapital Budgeting: An Insight Torjrahuljain100% (2)

- PC Sat Dist Concept GWGDocument12 pagesPC Sat Dist Concept GWGastorgad435No ratings yet

- mdw4-2 - CustomerDocument1 pagemdw4-2 - CustomerkrisnantoNo ratings yet

- Kiln Mechanics - (4.1) - ''Action Plan''Document5 pagesKiln Mechanics - (4.1) - ''Action Plan''Diego AlejandroNo ratings yet

- Lec 3 - My Research (1.5hr) PDFDocument20 pagesLec 3 - My Research (1.5hr) PDFVân Anh TrầnNo ratings yet

- mdw4-2 - PenjualanDocument1 pagemdw4-2 - PenjualankrisnantoNo ratings yet

- RaciDocument3 pagesRaciSreeranjPrakashNo ratings yet

- Competitive Value Train Analysis: BY: Section-ADocument7 pagesCompetitive Value Train Analysis: BY: Section-AAniketNo ratings yet

- Road Work For GSB, WMM & Bitumen Job QAPDocument2 pagesRoad Work For GSB, WMM & Bitumen Job QAPSasanka SekharNo ratings yet

- VX Multi Phasse TesterDocument8 pagesVX Multi Phasse TesterHassan ManzarNo ratings yet

- EE 508 Lect 18 Fall 2020Document32 pagesEE 508 Lect 18 Fall 2020Sai KiranNo ratings yet

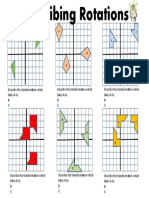

- Describing RotationDocument1 pageDescribing RotationJaneNo ratings yet

- Essential Graphs For AP MacroeconomicsDocument5 pagesEssential Graphs For AP MacroeconomicsDennis100% (1)

- Transcription 38 ARCHILUTH Les Sylvains PDFDocument2 pagesTranscription 38 ARCHILUTH Les Sylvains PDFRim LeymarieNo ratings yet

- ACO Fulbora Catalogue - 2015Document40 pagesACO Fulbora Catalogue - 2015dbrooksuttNo ratings yet

- Handout - ABC ClassificationDocument1 pageHandout - ABC ClassificationNoval MaulanaNo ratings yet

- Use Case: Statename State Nam E Statename StatenameDocument1 pageUse Case: Statename State Nam E Statename StatenameWAN NURULAIN ARIBAH BINTI WAN HASSANNo ratings yet

- Fault Detection of Power Transformer byDocument6 pagesFault Detection of Power Transformer bywaael abdulhassanNo ratings yet

- Symbol 3Document1 pageSymbol 3fredtranNo ratings yet

- GriffinC Resume 2010Document4 pagesGriffinC Resume 2010Simeon WheelerNo ratings yet

- (TK-006) Inspection Report For BandingDocument1 page(TK-006) Inspection Report For BandingMohammad FereidNo ratings yet

- MaammeDocument1 pageMaammeJussi-Pekka LajunenNo ratings yet

- Dynamic Resistance Measurement For Onload Tap ChangesDocument50 pagesDynamic Resistance Measurement For Onload Tap ChangesAhmed GhaniNo ratings yet

- EESA-R Skills RecordDocument1 pageEESA-R Skills RecordAmber Kat MillerNo ratings yet

- Notes: Conceptual Framework by Tashwita GuptaDocument21 pagesNotes: Conceptual Framework by Tashwita GuptaMensur Ćuprija100% (1)

- Numbers Sheet Name Numbers Table NameDocument34 pagesNumbers Sheet Name Numbers Table Namefilbert rozakNo ratings yet

- ControlDocument16 pagesControlAleia Coleen ORENSENo ratings yet

- حساب أحمال التبريد والتدفئةDocument44 pagesحساب أحمال التبريد والتدفئةAhmed SayedNo ratings yet

- AberdeeenDS-Well Intervention PC PDFDocument316 pagesAberdeeenDS-Well Intervention PC PDFHernán Ricardo Castillo Alarcón100% (2)

- Devoxx Microservices FinalDocument22 pagesDevoxx Microservices Finallcm3766lNo ratings yet

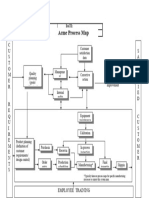

- App-A - Acme-Process-Map-1Document1 pageApp-A - Acme-Process-Map-1adamNo ratings yet

- Touring: Myrtle Beach Harley-Davidson Service Department Vehicle Maintenance ScheduleDocument1 pageTouring: Myrtle Beach Harley-Davidson Service Department Vehicle Maintenance ScheduleHenriqueNo ratings yet

- الأسواق السياحية PDFDocument11 pagesالأسواق السياحية PDFعمادالعزاويNo ratings yet

- You Can Practice Microcontroller Programming Easily Now!: Thursday, October 23, 2008Document16 pagesYou Can Practice Microcontroller Programming Easily Now!: Thursday, October 23, 2008Motaz HasnNo ratings yet

- Paper Decline Curve Analysis 1 (Najib)Document16 pagesPaper Decline Curve Analysis 1 (Najib)Ichsan Al Sabah LukmanNo ratings yet

- Lecture 3 (16th Jan, 2024)Document17 pagesLecture 3 (16th Jan, 2024)Harsh JainNo ratings yet

- @reception &: Challenges Quahty Gate# 1Document24 pages@reception &: Challenges Quahty Gate# 1Sneha SundarNo ratings yet

- InventorycountchecklistDocument3 pagesInventorycountchecklistsinra kongNo ratings yet

- Softails: Myrtle Beach Harley-Davidson Service Department Vehicle Maintenance ScheduleDocument1 pageSoftails: Myrtle Beach Harley-Davidson Service Department Vehicle Maintenance ScheduleHenriqueNo ratings yet

- Chapter-01-Figure-03 BUSI 2710Document1 pageChapter-01-Figure-03 BUSI 2710Mai KhanhNo ratings yet

- CKAD Curriculum V1.15.0 PDFDocument3 pagesCKAD Curriculum V1.15.0 PDFsamlalNo ratings yet

- Central and Inscribed Angles and Arcs-WorksheetDocument2 pagesCentral and Inscribed Angles and Arcs-WorksheetR Nov100% (1)

- Central and Inscribed Angles and Arcs-WorksheetDocument2 pagesCentral and Inscribed Angles and Arcs-WorksheetRyl TeraniaNo ratings yet

- Not For Reproduction: Operator's Manual Manual Del Operario Manuel de L'opérateurDocument28 pagesNot For Reproduction: Operator's Manual Manual Del Operario Manuel de L'opérateurmoisesNo ratings yet

- 22 17 04 23 10 38 44documentDocument4 pages22 17 04 23 10 38 44documentMarlboro RedNo ratings yet

- Vals BM (Op 69 Nº2)Document4 pagesVals BM (Op 69 Nº2)chonosaxNo ratings yet

- Triumph Maintenance Chart 6k Mile Service IntervalDocument1 pageTriumph Maintenance Chart 6k Mile Service IntervalalexNo ratings yet

- Dynas: Myrtle Beach Harley-Davidson Service Department Vehicle Maintenance ScheduleDocument2 pagesDynas: Myrtle Beach Harley-Davidson Service Department Vehicle Maintenance Schedulejaspal59No ratings yet

- c06c2db1 9e34 4cf3 9f3d D64e75b4cda7 JU OMR by AAPathshalaDocument1 pagec06c2db1 9e34 4cf3 9f3d D64e75b4cda7 JU OMR by AAPathshalaahnafisrakratim126No ratings yet

- Vidya Vikas Institute of Engineering & Technology: Blue BookDocument3 pagesVidya Vikas Institute of Engineering & Technology: Blue BookVarun H RNo ratings yet

- Form Function Test CableDocument1 pageForm Function Test Cablemuhammad attariqNo ratings yet

- Standard Highway Sign Border Specifications: A RadiusDocument7 pagesStandard Highway Sign Border Specifications: A Radiusapi-19757021No ratings yet

- Briggs Engine Owners Manual Model 12 277040tri - K - Hi1Document32 pagesBriggs Engine Owners Manual Model 12 277040tri - K - Hi1Willy Lozano GalindoNo ratings yet

- BoilerDocument1 pageBoileranilNo ratings yet

- Vespa SVC SchedDocument1 pageVespa SVC SchedLabrofskiNo ratings yet

- MA2 BPP Study TextDocument507 pagesMA2 BPP Study TextRavi Heeralall100% (1)

- Draft Rev.0 Copper Plating ReportDocument1 pageDraft Rev.0 Copper Plating ReportdekengNo ratings yet

- HKICPA QP Exam (Module A) Sep2004 Question PaperDocument7 pagesHKICPA QP Exam (Module A) Sep2004 Question Papercynthia tsuiNo ratings yet

- 568 - LLC Tax Return FormDocument7 pages568 - LLC Tax Return FormAndreana Dumpling WilliamsNo ratings yet

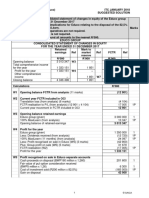

- ITC January 2018 Paper 2 Question 1 Part II Solution PDFDocument4 pagesITC January 2018 Paper 2 Question 1 Part II Solution PDFTinotenda MuroveNo ratings yet

- Simbol TradingDocument25 pagesSimbol TradingEmman ElagoNo ratings yet

- Ross's Top S: 5 Ealth Trade OpportunitiesDocument18 pagesRoss's Top S: 5 Ealth Trade OpportunitieswillNo ratings yet

- AlphaDocument18 pagesAlphaOrganic NutsNo ratings yet

- Z Accumulation/Z Income: Invesco ICVC Fund Range GuideDocument2 pagesZ Accumulation/Z Income: Invesco ICVC Fund Range GuideAaronNo ratings yet

- Introduction of PartnershipDocument22 pagesIntroduction of Partnershipmicaella pasionNo ratings yet

- Afar Review HandoutsDocument19 pagesAfar Review HandoutsAlisonNo ratings yet

- SRC HandoutDocument8 pagesSRC HandoutmangpatNo ratings yet

- Capital Structure Analysis of Hero HondaDocument8 pagesCapital Structure Analysis of Hero HondaHari ShankarNo ratings yet

- Textbook SolutionDocument61 pagesTextbook SolutionmmNo ratings yet

- Chapter 4 - Completing The Accounting CycleDocument59 pagesChapter 4 - Completing The Accounting CycleTâm Lê Hồ HồngNo ratings yet

- Tax Grant ThorntonDocument40 pagesTax Grant ThorntonMAYANK AGGARWALNo ratings yet

- Chapter 5 Accounting For Merchandising OperationsDocument15 pagesChapter 5 Accounting For Merchandising OperationsDecereen Pineda RodriguezaNo ratings yet

- Introduction: The Statement of Profit or LossDocument4 pagesIntroduction: The Statement of Profit or LossRonnel Villaceran SaysonNo ratings yet

- Deed of Assignment SharesDocument2 pagesDeed of Assignment SharesCora EleazarNo ratings yet

- Ledger FormatDocument1 pageLedger FormatPrecious Ruiz-zorillaNo ratings yet

- Burr Epstein Business Formation CompleteDocument15 pagesBurr Epstein Business Formation CompleteRyan KaltmanNo ratings yet

- Christopher Collins January Bank StatementDocument2 pagesChristopher Collins January Bank StatementJim Boaz100% (1)

- Finance Interview QuestionsDocument14 pagesFinance Interview QuestionsVivek SequeiraNo ratings yet

- Securities Market Exercise HVNHDocument8 pagesSecurities Market Exercise HVNHBánh Bèo KangNo ratings yet

- Comparison IFRS VASDocument43 pagesComparison IFRS VAStieuquan42100% (3)

- S4HANA1909 Availability Dependencies en XXDocument52 pagesS4HANA1909 Availability Dependencies en XXgobashaNo ratings yet

- Member Directory: April 2017Document15 pagesMember Directory: April 2017William WilliamsonNo ratings yet