Perfect Competition: Slides by John F. Hall

Perfect Competition: Slides by John F. Hall

You might also like

- MorningstarDocument13 pagesMorningstargigiNo ratings yet

- A level Economics Revision: Cheeky Revision ShortcutsFrom EverandA level Economics Revision: Cheeky Revision ShortcutsRating: 3 out of 5 stars3/5 (1)

- Asian Paints Corporate StrategyDocument82 pagesAsian Paints Corporate StrategyGULSHANKUMARVERMA60% (5)

- Perfect CompetitionDocument17 pagesPerfect CompetitionBrian KissingerNo ratings yet

- Eco Chapter 4 NotesBy Shashikiran SirDocument17 pagesEco Chapter 4 NotesBy Shashikiran Sirashoknandi156No ratings yet

- Monopoly and Imperfect CompetitionDocument57 pagesMonopoly and Imperfect Competitionmohammed zeinNo ratings yet

- Market Structure and Perfect Competitive FirmDocument30 pagesMarket Structure and Perfect Competitive Firmmetc860100% (1)

- Chapter - MonopolyDocument13 pagesChapter - Monopolyanamika.sharmaNo ratings yet

- 5-7 - Market Structures and EfficiencyDocument83 pages5-7 - Market Structures and EfficiencySamiyah Irfan 2023243No ratings yet

- ECO10004 - Week 6Document8 pagesECO10004 - Week 6Kiệt Văn Ngọc TuấnNo ratings yet

- Market Competition Actual1123Document27 pagesMarket Competition Actual1123oshimo.tokuNo ratings yet

- Monopoly and Imperfect Competition: Slides by John F. HallDocument47 pagesMonopoly and Imperfect Competition: Slides by John F. Hallneha2227100% (1)

- Imperfect Competition and Output Decision: Presented By: Ananya Sengupta Deepak Nanda Kush RaiDocument23 pagesImperfect Competition and Output Decision: Presented By: Ananya Sengupta Deepak Nanda Kush RaiDeepak NandaNo ratings yet

- Chap 11Document68 pagesChap 11Ayesh DinukaNo ratings yet

- Chapter 6 Market StructureDocument36 pagesChapter 6 Market StructureChen Yee KhooNo ratings yet

- Pricing and Output Decisions:: Monopolistic Competition and OligopolyDocument44 pagesPricing and Output Decisions:: Monopolistic Competition and OligopolyAimen KhanNo ratings yet

- Perfect Competition Short RunDocument20 pagesPerfect Competition Short RunM Bilal KhanNo ratings yet

- Lecture 5 - Monopolistic CompetitionDocument49 pagesLecture 5 - Monopolistic Competitionsandeepsingaria.2325No ratings yet

- Perfect Competition in Short RunDocument20 pagesPerfect Competition in Short RunViraja GuruNo ratings yet

- 4.1market Structures - PERFECT COMPETITIONDocument21 pages4.1market Structures - PERFECT COMPETITIONVanessa CanoogNo ratings yet

- Presented by Ananya Sengupta Deepak Nanda Kush RaiDocument26 pagesPresented by Ananya Sengupta Deepak Nanda Kush RaiDeepak NandaNo ratings yet

- EconomicsDocument22 pagesEconomicsdipu jaiswalNo ratings yet

- Market Structures and Price-Output DeterminationDocument40 pagesMarket Structures and Price-Output DeterminationHartin StylesNo ratings yet

- 2024 Term 2 ECON Activities - MGDocument37 pages2024 Term 2 ECON Activities - MGketyeemihleNo ratings yet

- ECO113 L-16 Market Structures (Monoply 1) PPTDocument20 pagesECO113 L-16 Market Structures (Monoply 1) PPTlakshay sharmaNo ratings yet

- Chapter 5 LovewellDocument31 pagesChapter 5 Lovewellintisharakib9No ratings yet

- Supply and Demand: Slides by John F. HallDocument60 pagesSupply and Demand: Slides by John F. HallArief TAnkziNo ratings yet

- Chapters 7 9Document17 pagesChapters 7 9directo549No ratings yet

- Micro II 1Document10 pagesMicro II 1Gena DuresaNo ratings yet

- Bruechap 008Document32 pagesBruechap 008Rainier MendozaNo ratings yet

- Market StructureDocument81 pagesMarket StructuresuryaabhimaniNo ratings yet

- MonopolyDocument50 pagesMonopolyVishwa Srikanth100% (1)

- 1 5 Market StructureDocument24 pages1 5 Market StructureBMPatelNo ratings yet

- Oligopolycharacteristics 090925201939 Phpapp01Document16 pagesOligopolycharacteristics 090925201939 Phpapp01gunu_f1No ratings yet

- Economics Unit 4Document10 pagesEconomics Unit 4dhadhi payaleNo ratings yet

- MonopolyDocument33 pagesMonopolyRUPABH BHARTINo ratings yet

- MonopolyDocument38 pagesMonopolyanu nitiNo ratings yet

- Between Monopoly and Perfect CompetitionDocument23 pagesBetween Monopoly and Perfect CompetitionAmlan SenguptaNo ratings yet

- Freshman Eco Unit 5Document16 pagesFreshman Eco Unit 5Khant Si ThuNo ratings yet

- MarketDocument22 pagesMarketAaditya GuptaNo ratings yet

- Theories of The FirmDocument14 pagesTheories of The FirmRudjun TapalNo ratings yet

- Chapter-07 Market Structure & PricingDocument28 pagesChapter-07 Market Structure & PricingsubarnabiswasNo ratings yet

- Chapter 8 MEDocument61 pagesChapter 8 MEHaryadi WidodoNo ratings yet

- 08 Market 01 PCDocument58 pages08 Market 01 PCBhaskar KondaNo ratings yet

- Lecture 10 & 11 - Monopolistic Competition & OligopolyDocument62 pagesLecture 10 & 11 - Monopolistic Competition & Oligopolyvillaverdev01No ratings yet

- Monopolistc Competition 3Document10 pagesMonopolistc Competition 3Abid SunnyNo ratings yet

- Lecture 3.2 - Perfect CompetitionDocument13 pagesLecture 3.2 - Perfect CompetitionLakmal SilvaNo ratings yet

- Oligopoly (RF)Document37 pagesOligopoly (RF)riya nawasNo ratings yet

- Oligopoly (RF)Document37 pagesOligopoly (RF)faizy24No ratings yet

- Chapter Two: Demand and SupplyDocument71 pagesChapter Two: Demand and Supplykasech mogesNo ratings yet

- 06 MonopolyDocument20 pages06 MonopolyManisha GoraiNo ratings yet

- Economics 1110: Topic 6Document62 pagesEconomics 1110: Topic 6mahesh kumaraNo ratings yet

- Market StructuresDocument36 pagesMarket StructuresSolovastru MihaelaNo ratings yet

- MonopolyDocument17 pagesMonopolydestinyebeku01No ratings yet

- Chapter 11Document14 pagesChapter 11Rajveer SinghNo ratings yet

- The Firm and Market StructuresDocument36 pagesThe Firm and Market StructuresPrince Agrawal100% (1)

- OligopolyDocument43 pagesOligopolyPankaj Dogra75% (4)

- 1monopolistic CompetitionDocument9 pages1monopolistic CompetitionRaj AdakNo ratings yet

- Perfect Competition ADocument67 pagesPerfect Competition APeter MastersNo ratings yet

- Lessons From The Successful InvestorFrom EverandLessons From The Successful InvestorRating: 4.5 out of 5 stars4.5/5 (5)

- The Well-Timed Strategy (Review and Analysis of Navarro's Book)From EverandThe Well-Timed Strategy (Review and Analysis of Navarro's Book)No ratings yet

- Vertical and Horizontal Strategy in SCMDocument22 pagesVertical and Horizontal Strategy in SCMShivendu ShekharNo ratings yet

- Imc Research PlanDocument5 pagesImc Research Planapi-348222896No ratings yet

- LIC S Jeevan Rekha 512N211V01Document4 pagesLIC S Jeevan Rekha 512N211V01Ramu448No ratings yet

- Reference Back Bay Sim ReportDocument2 pagesReference Back Bay Sim Reportrjhajharia1997No ratings yet

- Principle of Accounts School Based Assessment SBADocument27 pagesPrinciple of Accounts School Based Assessment SBAAlexia MorganNo ratings yet

- BankMobile Full Fee Schedules PDFDocument2 pagesBankMobile Full Fee Schedules PDFminipower50No ratings yet

- Answer Costs of Al Shaheer Corporation Going PublicDocument3 pagesAnswer Costs of Al Shaheer Corporation Going PublicSyed Saqlain Raza JafriNo ratings yet

- MotorUX PitchDocument14 pagesMotorUX PitchBramhananda ReddyNo ratings yet

- Health Financing Strategy Period 2016-2025 - EN - Copy 1Document47 pagesHealth Financing Strategy Period 2016-2025 - EN - Copy 1Indah ShofiyahNo ratings yet

- MSD - Sales Budgeting & Forecasting 1Document25 pagesMSD - Sales Budgeting & Forecasting 1Sajith PrasangaNo ratings yet

- Diagnostic Test: Question TextDocument60 pagesDiagnostic Test: Question TextpankajmadhavNo ratings yet

- QuestionnairesDocument3 pagesQuestionnairesshahidjappaNo ratings yet

- CH 12 PracticeDocument6 pagesCH 12 PracticeAli Abdullah Al-Saffar100% (1)

- PIACOS, Giana Valerie W. Branches of Economics: Econ 1 - 6:30-7:30 MWF Bs Architecture 5Document1 pagePIACOS, Giana Valerie W. Branches of Economics: Econ 1 - 6:30-7:30 MWF Bs Architecture 5Valeria PNo ratings yet

- Internal Trade Testing - 1 (Direct Questions)Document9 pagesInternal Trade Testing - 1 (Direct Questions)Saahil LedwaniNo ratings yet

- CostDocument161 pagesCostMae Namoc67% (6)

- The Profitless PCDocument12 pagesThe Profitless PCSuchita SuryanarayananNo ratings yet

- Purchasing and Materials ManagementDocument73 pagesPurchasing and Materials ManagementShivamitra ChiruthaniNo ratings yet

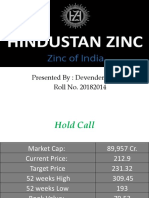

- Hindustan ZincDocument8 pagesHindustan ZincDevender SharmaNo ratings yet

- Tender Types Accepted During Sale Transaction 2Document38 pagesTender Types Accepted During Sale Transaction 2abhaykanodia1No ratings yet

- 17206Document17 pages17206ashaNo ratings yet

- CoaseDocument20 pagesCoasepwalker_25100% (1)

- Channel Roles in A Dynamic Marketplace at Bec DomsDocument7 pagesChannel Roles in A Dynamic Marketplace at Bec DomsBabasab Patil (Karrisatte)No ratings yet

- Chapter 22 - SBC - Share Apprecaition Right - Group 9Document26 pagesChapter 22 - SBC - Share Apprecaition Right - Group 9Margarethe GatdulaNo ratings yet

- LSO - Operating EnvironmentsDocument10 pagesLSO - Operating Environmentsdozza56No ratings yet

- AU12-FM-Midterm QuizDocument6 pagesAU12-FM-Midterm QuizHan Nguyen GiaNo ratings yet

- Royal Dutch Shell Group - 2005 Case StudyDocument21 pagesRoyal Dutch Shell Group - 2005 Case StudyManatosa MenataNo ratings yet

- Investment Objective: Fund Fact Sheet As of September 2020Document2 pagesInvestment Objective: Fund Fact Sheet As of September 2020Neil MijaresNo ratings yet

Download as ppt, pdf, or txt

You might also like

- MorningstarDocument13 pagesMorningstargigiNo ratings yet

- A level Economics Revision: Cheeky Revision ShortcutsFrom EverandA level Economics Revision: Cheeky Revision ShortcutsRating: 3 out of 5 stars3/5 (1)

- Asian Paints Corporate StrategyDocument82 pagesAsian Paints Corporate StrategyGULSHANKUMARVERMA60% (5)

- Perfect CompetitionDocument17 pagesPerfect CompetitionBrian KissingerNo ratings yet

- Eco Chapter 4 NotesBy Shashikiran SirDocument17 pagesEco Chapter 4 NotesBy Shashikiran Sirashoknandi156No ratings yet

- Monopoly and Imperfect CompetitionDocument57 pagesMonopoly and Imperfect Competitionmohammed zeinNo ratings yet

- Market Structure and Perfect Competitive FirmDocument30 pagesMarket Structure and Perfect Competitive Firmmetc860100% (1)

- Chapter - MonopolyDocument13 pagesChapter - Monopolyanamika.sharmaNo ratings yet

- 5-7 - Market Structures and EfficiencyDocument83 pages5-7 - Market Structures and EfficiencySamiyah Irfan 2023243No ratings yet

- ECO10004 - Week 6Document8 pagesECO10004 - Week 6Kiệt Văn Ngọc TuấnNo ratings yet

- Market Competition Actual1123Document27 pagesMarket Competition Actual1123oshimo.tokuNo ratings yet

- Monopoly and Imperfect Competition: Slides by John F. HallDocument47 pagesMonopoly and Imperfect Competition: Slides by John F. Hallneha2227100% (1)

- Imperfect Competition and Output Decision: Presented By: Ananya Sengupta Deepak Nanda Kush RaiDocument23 pagesImperfect Competition and Output Decision: Presented By: Ananya Sengupta Deepak Nanda Kush RaiDeepak NandaNo ratings yet

- Chap 11Document68 pagesChap 11Ayesh DinukaNo ratings yet

- Chapter 6 Market StructureDocument36 pagesChapter 6 Market StructureChen Yee KhooNo ratings yet

- Pricing and Output Decisions:: Monopolistic Competition and OligopolyDocument44 pagesPricing and Output Decisions:: Monopolistic Competition and OligopolyAimen KhanNo ratings yet

- Perfect Competition Short RunDocument20 pagesPerfect Competition Short RunM Bilal KhanNo ratings yet

- Lecture 5 - Monopolistic CompetitionDocument49 pagesLecture 5 - Monopolistic Competitionsandeepsingaria.2325No ratings yet

- Perfect Competition in Short RunDocument20 pagesPerfect Competition in Short RunViraja GuruNo ratings yet

- 4.1market Structures - PERFECT COMPETITIONDocument21 pages4.1market Structures - PERFECT COMPETITIONVanessa CanoogNo ratings yet

- Presented by Ananya Sengupta Deepak Nanda Kush RaiDocument26 pagesPresented by Ananya Sengupta Deepak Nanda Kush RaiDeepak NandaNo ratings yet

- EconomicsDocument22 pagesEconomicsdipu jaiswalNo ratings yet

- Market Structures and Price-Output DeterminationDocument40 pagesMarket Structures and Price-Output DeterminationHartin StylesNo ratings yet

- 2024 Term 2 ECON Activities - MGDocument37 pages2024 Term 2 ECON Activities - MGketyeemihleNo ratings yet

- ECO113 L-16 Market Structures (Monoply 1) PPTDocument20 pagesECO113 L-16 Market Structures (Monoply 1) PPTlakshay sharmaNo ratings yet

- Chapter 5 LovewellDocument31 pagesChapter 5 Lovewellintisharakib9No ratings yet

- Supply and Demand: Slides by John F. HallDocument60 pagesSupply and Demand: Slides by John F. HallArief TAnkziNo ratings yet

- Chapters 7 9Document17 pagesChapters 7 9directo549No ratings yet

- Micro II 1Document10 pagesMicro II 1Gena DuresaNo ratings yet

- Bruechap 008Document32 pagesBruechap 008Rainier MendozaNo ratings yet

- Market StructureDocument81 pagesMarket StructuresuryaabhimaniNo ratings yet

- MonopolyDocument50 pagesMonopolyVishwa Srikanth100% (1)

- 1 5 Market StructureDocument24 pages1 5 Market StructureBMPatelNo ratings yet

- Oligopolycharacteristics 090925201939 Phpapp01Document16 pagesOligopolycharacteristics 090925201939 Phpapp01gunu_f1No ratings yet

- Economics Unit 4Document10 pagesEconomics Unit 4dhadhi payaleNo ratings yet

- MonopolyDocument33 pagesMonopolyRUPABH BHARTINo ratings yet

- MonopolyDocument38 pagesMonopolyanu nitiNo ratings yet

- Between Monopoly and Perfect CompetitionDocument23 pagesBetween Monopoly and Perfect CompetitionAmlan SenguptaNo ratings yet

- Freshman Eco Unit 5Document16 pagesFreshman Eco Unit 5Khant Si ThuNo ratings yet

- MarketDocument22 pagesMarketAaditya GuptaNo ratings yet

- Theories of The FirmDocument14 pagesTheories of The FirmRudjun TapalNo ratings yet

- Chapter-07 Market Structure & PricingDocument28 pagesChapter-07 Market Structure & PricingsubarnabiswasNo ratings yet

- Chapter 8 MEDocument61 pagesChapter 8 MEHaryadi WidodoNo ratings yet

- 08 Market 01 PCDocument58 pages08 Market 01 PCBhaskar KondaNo ratings yet

- Lecture 10 & 11 - Monopolistic Competition & OligopolyDocument62 pagesLecture 10 & 11 - Monopolistic Competition & Oligopolyvillaverdev01No ratings yet

- Monopolistc Competition 3Document10 pagesMonopolistc Competition 3Abid SunnyNo ratings yet

- Lecture 3.2 - Perfect CompetitionDocument13 pagesLecture 3.2 - Perfect CompetitionLakmal SilvaNo ratings yet

- Oligopoly (RF)Document37 pagesOligopoly (RF)riya nawasNo ratings yet

- Oligopoly (RF)Document37 pagesOligopoly (RF)faizy24No ratings yet

- Chapter Two: Demand and SupplyDocument71 pagesChapter Two: Demand and Supplykasech mogesNo ratings yet

- 06 MonopolyDocument20 pages06 MonopolyManisha GoraiNo ratings yet

- Economics 1110: Topic 6Document62 pagesEconomics 1110: Topic 6mahesh kumaraNo ratings yet

- Market StructuresDocument36 pagesMarket StructuresSolovastru MihaelaNo ratings yet

- MonopolyDocument17 pagesMonopolydestinyebeku01No ratings yet

- Chapter 11Document14 pagesChapter 11Rajveer SinghNo ratings yet

- The Firm and Market StructuresDocument36 pagesThe Firm and Market StructuresPrince Agrawal100% (1)

- OligopolyDocument43 pagesOligopolyPankaj Dogra75% (4)

- 1monopolistic CompetitionDocument9 pages1monopolistic CompetitionRaj AdakNo ratings yet

- Perfect Competition ADocument67 pagesPerfect Competition APeter MastersNo ratings yet

- Lessons From The Successful InvestorFrom EverandLessons From The Successful InvestorRating: 4.5 out of 5 stars4.5/5 (5)

- The Well-Timed Strategy (Review and Analysis of Navarro's Book)From EverandThe Well-Timed Strategy (Review and Analysis of Navarro's Book)No ratings yet

- Vertical and Horizontal Strategy in SCMDocument22 pagesVertical and Horizontal Strategy in SCMShivendu ShekharNo ratings yet

- Imc Research PlanDocument5 pagesImc Research Planapi-348222896No ratings yet

- LIC S Jeevan Rekha 512N211V01Document4 pagesLIC S Jeevan Rekha 512N211V01Ramu448No ratings yet

- Reference Back Bay Sim ReportDocument2 pagesReference Back Bay Sim Reportrjhajharia1997No ratings yet

- Principle of Accounts School Based Assessment SBADocument27 pagesPrinciple of Accounts School Based Assessment SBAAlexia MorganNo ratings yet

- BankMobile Full Fee Schedules PDFDocument2 pagesBankMobile Full Fee Schedules PDFminipower50No ratings yet

- Answer Costs of Al Shaheer Corporation Going PublicDocument3 pagesAnswer Costs of Al Shaheer Corporation Going PublicSyed Saqlain Raza JafriNo ratings yet

- MotorUX PitchDocument14 pagesMotorUX PitchBramhananda ReddyNo ratings yet

- Health Financing Strategy Period 2016-2025 - EN - Copy 1Document47 pagesHealth Financing Strategy Period 2016-2025 - EN - Copy 1Indah ShofiyahNo ratings yet

- MSD - Sales Budgeting & Forecasting 1Document25 pagesMSD - Sales Budgeting & Forecasting 1Sajith PrasangaNo ratings yet

- Diagnostic Test: Question TextDocument60 pagesDiagnostic Test: Question TextpankajmadhavNo ratings yet

- QuestionnairesDocument3 pagesQuestionnairesshahidjappaNo ratings yet

- CH 12 PracticeDocument6 pagesCH 12 PracticeAli Abdullah Al-Saffar100% (1)

- PIACOS, Giana Valerie W. Branches of Economics: Econ 1 - 6:30-7:30 MWF Bs Architecture 5Document1 pagePIACOS, Giana Valerie W. Branches of Economics: Econ 1 - 6:30-7:30 MWF Bs Architecture 5Valeria PNo ratings yet

- Internal Trade Testing - 1 (Direct Questions)Document9 pagesInternal Trade Testing - 1 (Direct Questions)Saahil LedwaniNo ratings yet

- CostDocument161 pagesCostMae Namoc67% (6)

- The Profitless PCDocument12 pagesThe Profitless PCSuchita SuryanarayananNo ratings yet

- Purchasing and Materials ManagementDocument73 pagesPurchasing and Materials ManagementShivamitra ChiruthaniNo ratings yet

- Hindustan ZincDocument8 pagesHindustan ZincDevender SharmaNo ratings yet

- Tender Types Accepted During Sale Transaction 2Document38 pagesTender Types Accepted During Sale Transaction 2abhaykanodia1No ratings yet

- 17206Document17 pages17206ashaNo ratings yet

- CoaseDocument20 pagesCoasepwalker_25100% (1)

- Channel Roles in A Dynamic Marketplace at Bec DomsDocument7 pagesChannel Roles in A Dynamic Marketplace at Bec DomsBabasab Patil (Karrisatte)No ratings yet

- Chapter 22 - SBC - Share Apprecaition Right - Group 9Document26 pagesChapter 22 - SBC - Share Apprecaition Right - Group 9Margarethe GatdulaNo ratings yet

- LSO - Operating EnvironmentsDocument10 pagesLSO - Operating Environmentsdozza56No ratings yet

- AU12-FM-Midterm QuizDocument6 pagesAU12-FM-Midterm QuizHan Nguyen GiaNo ratings yet

- Royal Dutch Shell Group - 2005 Case StudyDocument21 pagesRoyal Dutch Shell Group - 2005 Case StudyManatosa MenataNo ratings yet

- Investment Objective: Fund Fact Sheet As of September 2020Document2 pagesInvestment Objective: Fund Fact Sheet As of September 2020Neil MijaresNo ratings yet