Download as ppt, pdf, or txt

You might also like

- Bank Management and Financial Services 8e - Peter S. Rose, Sylvia C. HudginsDocument310 pagesBank Management and Financial Services 8e - Peter S. Rose, Sylvia C. HudginsTF67% (9)

- Consumer 3451467296Document10 pagesConsumer 3451467296Wayne DuncanNo ratings yet

- Hard Money LendingDocument16 pagesHard Money Lendingnikhilraheja100% (1)

- Leveraging Fintech To Disrupt Cross-Border Remittance ServicesDocument15 pagesLeveraging Fintech To Disrupt Cross-Border Remittance ServicesAbhi SangwanNo ratings yet

- Unified Payments Interface (UPI)Document14 pagesUnified Payments Interface (UPI)VivekNo ratings yet

- Basics of BankingDocument167 pagesBasics of BankingTed CuteTedNo ratings yet

- Overview of Changing Financial ServicesDocument14 pagesOverview of Changing Financial ServicesNazmul H. PalashNo ratings yet

- Chap-17-Lending Policies and ProceduresDocument30 pagesChap-17-Lending Policies and ProceduresNazmul H. PalashNo ratings yet

- Windsor Crescent Dental IMDocument21 pagesWindsor Crescent Dental IMzdx4627ks9No ratings yet

- HSBC's Mortgage Lending DecisionDocument22 pagesHSBC's Mortgage Lending Decisionbestchi19No ratings yet

- Chapter 4 - Consumer CreditDocument35 pagesChapter 4 - Consumer CredithaziqNo ratings yet

- Cac Prelim ReviewerDocument3 pagesCac Prelim ReviewerAnna Lyssa BatasNo ratings yet

- Analysis On The Basis of 7 Ps and SwotDocument28 pagesAnalysis On The Basis of 7 Ps and Swotvedanshjain100% (3)

- Sheam. Bank Management.-1Document121 pagesSheam. Bank Management.-1SM SheamNo ratings yet

- Relationship O Cer - Micro Segment: Closes: July 8, 2021Document4 pagesRelationship O Cer - Micro Segment: Closes: July 8, 2021joanmubzNo ratings yet

- Chapter 3 Eng VersionDocument26 pagesChapter 3 Eng VersionThảo NguyễnNo ratings yet

- Chapter One: An Overview of Banks and The Financial-Services SectorDocument13 pagesChapter One: An Overview of Banks and The Financial-Services SectorMohamed A. TawfikNo ratings yet

- Credit Explained Leaflet 2005Document24 pagesCredit Explained Leaflet 2005ericagen53No ratings yet

- E-Banking Applications On Different BanksDocument24 pagesE-Banking Applications On Different BanksSalman JaganiNo ratings yet

- AIB PresentationDocument11 pagesAIB Presentationy942kjmdb4No ratings yet

- Updated Chap 3Document67 pagesUpdated Chap 3Đoàn Trần Ngọc AnhNo ratings yet

- Are You Creditworthy?: What Are Special Accessing Entities?Document2 pagesAre You Creditworthy?: What Are Special Accessing Entities?Allyzza MarieNo ratings yet

- Debt Recovery O Cer: Closes: July 8, 2021Document4 pagesDebt Recovery O Cer: Closes: July 8, 2021joanmubzNo ratings yet

- Busfin ReviewerDocument4 pagesBusfin ReviewerjeonsnobNo ratings yet

- Product Booklet TImes UDocument12 pagesProduct Booklet TImes UmwendaflaviushilelmutembeiNo ratings yet

- Private Real Estate Financing OverviewDocument13 pagesPrivate Real Estate Financing OverviewJoseph McDonald100% (1)

- Chapter 09 Risk Management: Asset-Backed Securities, Loan Sales, Credit Standbys, and Credit DerivativesDocument33 pagesChapter 09 Risk Management: Asset-Backed Securities, Loan Sales, Credit Standbys, and Credit DerivativesNway Moe Saung100% (2)

- Overdraft: Important NoticeDocument2 pagesOverdraft: Important NoticeAdegboyega Moses SegunNo ratings yet

- Chapter 01 Overview of Bank ManagementDocument26 pagesChapter 01 Overview of Bank Managementtrungngoan02No ratings yet

- Consumer Credit 2021Document2 pagesConsumer Credit 2021Finn KevinNo ratings yet

- Credit Report Analysis Sample - ClientDocument10 pagesCredit Report Analysis Sample - ClientvanezzajorlyanneNo ratings yet

- Your Credit Score: What It Means To You As A Prospective Home BuyerDocument5 pagesYour Credit Score: What It Means To You As A Prospective Home BuyerRyan5Cents100% (2)

- Welcome To : Reports, Scores & HistoriesDocument41 pagesWelcome To : Reports, Scores & HistoriesOne RochaNo ratings yet

- Fintech 6Document30 pagesFintech 6Taaran ReddyNo ratings yet

- Credit & Collection FirmDocument17 pagesCredit & Collection FirmJACA, John Lloyd B.No ratings yet

- Islamic Banking and FinanceDocument14 pagesIslamic Banking and FinanceMr AnonymousNo ratings yet

- Credit Analysis cccccccDocument220 pagesCredit Analysis cccccccsiinqeecreditNo ratings yet

- The Bank: Banking For AllDocument20 pagesThe Bank: Banking For AllYaswanth ChilukuriNo ratings yet

- Cred Risk (07-9 Alternate)Document61 pagesCred Risk (07-9 Alternate)Farrukh JunaidNo ratings yet

- The Skys The Limit Credit Repair GuideDocument5 pagesThe Skys The Limit Credit Repair GuideCarolNo ratings yet

- Credit Analysis CccccccDocument220 pagesCredit Analysis CccccccsiinqeecreditNo ratings yet

- AJDFI - Principles of Credit - PPP - 16nov2012Document51 pagesAJDFI - Principles of Credit - PPP - 16nov2012Fretchie SenielNo ratings yet

- Ask Icas Webinar Series: Funding Business Recovery and ExpansionDocument38 pagesAsk Icas Webinar Series: Funding Business Recovery and ExpansionAhsan IqbalNo ratings yet

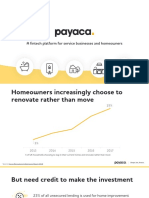

- A Fintech Platform For Service Businesses and HomeownersDocument23 pagesA Fintech Platform For Service Businesses and HomeownersEly PNo ratings yet

- Cash Loan - Home Credit PhilippinesDocument1 pageCash Loan - Home Credit PhilippinesbeshstopNo ratings yet

- Module1 - Introduction To CreditDocument24 pagesModule1 - Introduction To CreditXoxo NiggaNo ratings yet

- Credit Repair Made E-Z PDFDocument140 pagesCredit Repair Made E-Z PDFWill CrawfordNo ratings yet

- Overview of BankingDocument24 pagesOverview of BankingKRZ. Arpon Root HackerNo ratings yet

- Credit & Collection FirmDocument18 pagesCredit & Collection FirmJACA, John Lloyd B.No ratings yet

- Vidalia Information Kit 2Document2 pagesVidalia Information Kit 2Rich Mhar ManguiatNo ratings yet

- BANKING Report2Document18 pagesBANKING Report2Ryan Dave GarciaNo ratings yet

- Chapter Thirteen: Managing Nondeposit LiabilitiesDocument22 pagesChapter Thirteen: Managing Nondeposit Liabilitiessridevi gopalakrishnanNo ratings yet

- ED29&30 EntrepDevDocument15 pagesED29&30 EntrepDevChetanya RajpalNo ratings yet

- Bank Recap & Reforms 2018Document18 pagesBank Recap & Reforms 2018alakshendraNo ratings yet

- Business Loans The Easy WayDocument1 pageBusiness Loans The Easy WayOjo TimmyNo ratings yet

- All About Credit Reports - Rev2Document8 pagesAll About Credit Reports - Rev2kabNo ratings yet

- CFAB. Commercial Banks - Chapter 5 - Consumer LoansDocument36 pagesCFAB. Commercial Banks - Chapter 5 - Consumer LoansViet Ha HoangNo ratings yet

- Dizon Banking ReviewerDocument82 pagesDizon Banking ReviewerAldrinCruiseNo ratings yet

- Credit Analysis and Distress Prediction: Adelia Rizkarunissa Arief Gust Kintan ImandaDocument4 pagesCredit Analysis and Distress Prediction: Adelia Rizkarunissa Arief Gust Kintan Imandanaega nuguNo ratings yet

- Module 3 Debt ManagementDocument33 pagesModule 3 Debt ManagementJane BañaresNo ratings yet

- Safari - Jun 5, 2019 at 9:49 PMDocument1 pageSafari - Jun 5, 2019 at 9:49 PMamir.jahed50No ratings yet

- Credit Risk Management: How to Avoid Lending Disasters and Maximize EarningsFrom EverandCredit Risk Management: How to Avoid Lending Disasters and Maximize EarningsNo ratings yet

- Plastic Money: Presented By: Ramandeep Kaur & Mba 4 Sem. 90512234158Document30 pagesPlastic Money: Presented By: Ramandeep Kaur & Mba 4 Sem. 90512234158ramandeeprinkyNo ratings yet

- Personal Finance and Planning: Skill Enhancement Course (SEC)Document29 pagesPersonal Finance and Planning: Skill Enhancement Course (SEC)Babita DeviNo ratings yet

- Fin368: Credit Management: Bank FinancingDocument46 pagesFin368: Credit Management: Bank FinancingHAIKAL9996No ratings yet

- BES 221 (PART I - Midterm Module)Document13 pagesBES 221 (PART I - Midterm Module)Maria Victoria IgcasNo ratings yet

- 05 GP CG Lesson01Document18 pages05 GP CG Lesson01VIKRANT VIKALNo ratings yet

- 1582368021812resume Yamini PDFDocument7 pages1582368021812resume Yamini PDFAaron JoshuaNo ratings yet

- Negotiable Instruments Act 1881Document40 pagesNegotiable Instruments Act 1881Tanvir PrantoNo ratings yet

- Literature Review On Financial Performance of BanksDocument4 pagesLiterature Review On Financial Performance of BanksafdtzvbexNo ratings yet

- 6.5 Present and Future Value of A Continuous Income StreamDocument3 pages6.5 Present and Future Value of A Continuous Income StreamPoppycortanaNo ratings yet

- Your Young Persons Account StatementDocument2 pagesYour Young Persons Account Statementabdi100% (1)

- 1910dsycp 11600Document2 pages1910dsycp 11600brandiwinde41No ratings yet

- Elife Services - Account Number:068811482: 01 Feb 2022 To 31 Aug 2022 Due Date by 31 Aug 2022 784-1989-4749595-2Document3 pagesElife Services - Account Number:068811482: 01 Feb 2022 To 31 Aug 2022 Due Date by 31 Aug 2022 784-1989-4749595-2mohamed elmakhzniNo ratings yet

- Confirmation File of LudhianaDocument19 pagesConfirmation File of LudhianaforestrangerNo ratings yet

- Math Test Chapter 1Document3 pagesMath Test Chapter 1jleodennisNo ratings yet

- ACCOUNTING VOCABULARY IN ENGLISH - EstudianteDocument3 pagesACCOUNTING VOCABULARY IN ENGLISH - EstudianteoswaldoNo ratings yet

- RFBT DRILL 3 (Special Laws)Document12 pagesRFBT DRILL 3 (Special Laws)ROMAR A. PIGANo ratings yet

- Topic 6 (1) - Banking InstitutionsDocument41 pagesTopic 6 (1) - Banking InstitutionsHirosha VejianNo ratings yet

- Twitter5 23 19 PDFDocument36 pagesTwitter5 23 19 PDFIttarrimi Haku Fazzaril Madāra100% (1)

- Study Report On Impact of Privatization On Banking Sector by Kartik MishraDocument96 pagesStudy Report On Impact of Privatization On Banking Sector by Kartik MishraManojNo ratings yet

- Chapter 6 Share CapitalsDocument5 pagesChapter 6 Share CapitalsShreya AgarwalNo ratings yet

- Customer Relationship Management in SbiDocument29 pagesCustomer Relationship Management in SbitanvishahtaashaNo ratings yet

- Ping An Bank - Annual Report 2020Document302 pagesPing An Bank - Annual Report 2020LutfilNo ratings yet

- Doa 250m DLC 6+2 - With Upfront Fee (3) - 5Document17 pagesDoa 250m DLC 6+2 - With Upfront Fee (3) - 5MANOJ VIJAYANNo ratings yet

- Presentation On: Project FinanceDocument80 pagesPresentation On: Project FinanceSachinNo ratings yet

- Birkisnhaw ING - Bank - Case - StudyDocument19 pagesBirkisnhaw ING - Bank - Case - StudyVicente MirandaNo ratings yet

- Operations 12122017 12032018Document2 pagesOperations 12122017 12032018Mohamed ElankoudNo ratings yet

- Extras de Cont / Account StatementDocument4 pagesExtras de Cont / Account StatementAdelina VeringaNo ratings yet

- MyTW Bill 900032858649 21 02 2022Document5 pagesMyTW Bill 900032858649 21 02 2022avelik ukNo ratings yet