Download as pptx, pdf, or txt

You might also like

- Computerized Bookkeeping of Joseph Landscaping and Plant Store Business Case STUDENTDocument24 pagesComputerized Bookkeeping of Joseph Landscaping and Plant Store Business Case STUDENThello nasty100% (1)

- Test Bank 2 - Ia 3Document31 pagesTest Bank 2 - Ia 3Xiena100% (6)

- 000 MergedDocument134 pages000 Mergedhira malikNo ratings yet

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- Chapter 8Document14 pagesChapter 8Kanton FernandezNo ratings yet

- Review of The Accounting ProcessDocument17 pagesReview of The Accounting ProcessLucy UnNo ratings yet

- Account ReceivableDocument13 pagesAccount ReceivableAndrea FontiverosNo ratings yet

- Alternate Demonstration Problem MerchandisingDocument5 pagesAlternate Demonstration Problem MerchandisingmoNo ratings yet

- Answers and Solutions To Exercises PDFDocument22 pagesAnswers and Solutions To Exercises PDFshaira aimee diolata100% (1)

- SRCBAI ABM1 Q3M10 Merchandising Concern Part1Document14 pagesSRCBAI ABM1 Q3M10 Merchandising Concern Part1Jaye RuantoNo ratings yet

- Singapore Institute of Management: University of London Preliminary Exam 2020Document20 pagesSingapore Institute of Management: University of London Preliminary Exam 2020Kəmalə AslanzadəNo ratings yet

- Market Need Analysis Define The Market Need For The New BusinessDocument2 pagesMarket Need Analysis Define The Market Need For The New BusinessCarmela De Juan100% (3)

- Acc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)Document1 pageAcc 1 - Financial Accounting and Reporting QUIZ NO. 15 - Accounting Cycle of A Merchandising Business (Application)nicole bancoroNo ratings yet

- Accounting Principles: Level 3 Diploma in Credit Management Exemplar PaperDocument20 pagesAccounting Principles: Level 3 Diploma in Credit Management Exemplar PaperFarrukhsgNo ratings yet

- 1 Mgt5014 .Lec.3 Double Entry-2021 StaffDocument23 pages1 Mgt5014 .Lec.3 Double Entry-2021 StaffNeelez RaizNo ratings yet

- Lec Merchandising Perpetual PeriodicDocument8 pagesLec Merchandising Perpetual PeriodicAiddan Clark De JesusNo ratings yet

- Ac1 Reviewer FinalsDocument5 pagesAc1 Reviewer FinalsMark Christian BrlNo ratings yet

- Review Quiz Inter1Document9 pagesReview Quiz Inter1Vanessa vnssNo ratings yet

- Fabm2 - Statement of Comprehensive Income (Practice Problems) - Answer KeyDocument3 pagesFabm2 - Statement of Comprehensive Income (Practice Problems) - Answer KeyMounicha Ambayec100% (4)

- Fabm2 Statement of Comprehensive Income Practice Problems Answer KeyDocument3 pagesFabm2 Statement of Comprehensive Income Practice Problems Answer KeyMounicha Ambayec0% (1)

- Chapter 5 Exercises-Exercise BankDocument9 pagesChapter 5 Exercises-Exercise BankPATRICIUS ALAN WIRAYUDHA KUSUMNo ratings yet

- Incomplete RecordDocument30 pagesIncomplete RecordMuhammad TahaNo ratings yet

- The Direct MethodDocument15 pagesThe Direct MethodHacker SKNo ratings yet

- Credo CompanyDocument2 pagesCredo CompanyYan TagleNo ratings yet

- Account ReceivableDocument3 pagesAccount ReceivableLorence Patrick LapidezNo ratings yet

- Session 5b Cash Flow Statement: HI5020 Corporate AccountingDocument18 pagesSession 5b Cash Flow Statement: HI5020 Corporate AccountingFeku RamNo ratings yet

- Steps in The Accounting Process: Ans:1 Definition of Accounting. 1: The System of Recording and SummarizingDocument9 pagesSteps in The Accounting Process: Ans:1 Definition of Accounting. 1: The System of Recording and SummarizingshamagondalNo ratings yet

- EC 1 - Acctg Cycle Part 2 Sample ProblemsDocument1 pageEC 1 - Acctg Cycle Part 2 Sample ProblemsChelay EscarezNo ratings yet

- 2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Document8 pages2018-0232 Beldia, Pitchie Mae G. ACT142: Auditing and Assurance: Concepts and Application 1Melanie SamsonaNo ratings yet

- AFB Lecture 4 Completed DeckDocument41 pagesAFB Lecture 4 Completed DeckAzure Pear HaNo ratings yet

- Merchandising Operations Part1Document49 pagesMerchandising Operations Part1keith niduelanNo ratings yet

- Henri Emanuel Reforba - Learning Task #2Document6 pagesHenri Emanuel Reforba - Learning Task #2Rhea BernabeNo ratings yet

- Accounting For Merchandising BusinessDocument34 pagesAccounting For Merchandising BusinessErleNo ratings yet

- AccountingDocument5 pagesAccountingMarinie CabagbagNo ratings yet

- 08.12.2017 Activity - Acfunda LabDocument2 pages08.12.2017 Activity - Acfunda LabPatOcampoNo ratings yet

- bài tập errorDocument4 pagesbài tập errorHoàng Bảo TrâmNo ratings yet

- Acctg Merchandise Inventory and Cost of SalesDocument16 pagesAcctg Merchandise Inventory and Cost of SalesDaisy Marie A. Rosel100% (1)

- Statement of Profit or Loss For The Year Ended 31 March 2009Document1 pageStatement of Profit or Loss For The Year Ended 31 March 2009Plawan GhimireNo ratings yet

- Introduction To Accounting An Integrated Approach 6Th Edition Ainsworth Solutions Manual Full Chapter PDFDocument41 pagesIntroduction To Accounting An Integrated Approach 6Th Edition Ainsworth Solutions Manual Full Chapter PDFstevenwhitextsngyadmk100% (14)

- Adobe Scan Mar 31, 2023Document20 pagesAdobe Scan Mar 31, 2023Renalyn Ps MewagNo ratings yet

- Accounting For Merchandising BusinessDocument21 pagesAccounting For Merchandising BusinessJunel PlanosNo ratings yet

- Incomplete RecordsDocument51 pagesIncomplete RecordssoniaNo ratings yet

- Answers To Quick Tests: Unit 3.1: Income StatementsDocument7 pagesAnswers To Quick Tests: Unit 3.1: Income StatementsJaved MushtaqNo ratings yet

- FUNACC - Accounting Cycle of A Merchandising BusinessDocument12 pagesFUNACC - Accounting Cycle of A Merchandising BusinessSassy GirlNo ratings yet

- Audit SM CH 4 2022Document13 pagesAudit SM CH 4 2022andzie09876No ratings yet

- Final AccountsDocument17 pagesFinal AccountsVikash AgrawalNo ratings yet

- Accounting Cycle For Merchandising ConcernDocument30 pagesAccounting Cycle For Merchandising ConcernMary100% (2)

- Answers of Doubtful Accounts AssignmentDocument4 pagesAnswers of Doubtful Accounts AssignmentGee Lysa Pascua VilbarNo ratings yet

- Merchandising AccountingDocument6 pagesMerchandising AccountingchrstncstlljNo ratings yet

- Merch 1Document3 pagesMerch 1Angelica EcliseNo ratings yet

- AccountancyDocument16 pagesAccountancyevangiebalunsat9No ratings yet

- SOLETRADER ACCOUNTING Handout 2Document4 pagesSOLETRADER ACCOUNTING Handout 2DenishNo ratings yet

- (01B) Prelims Special Exam Answer KeyDocument8 pages(01B) Prelims Special Exam Answer KeyAngel Madelene BernardoNo ratings yet

- Practical Auditing by Empleo 2022 Chapter 4 Receivables Related RevenuesDocument55 pagesPractical Auditing by Empleo 2022 Chapter 4 Receivables Related RevenuesDarence IndayaNo ratings yet

- Akuntansi p5Document7 pagesAkuntansi p5Alche MistNo ratings yet

- Branch Accounting - ICMAIDocument51 pagesBranch Accounting - ICMAIdbNo ratings yet

- Acc Concepts PP QnsDocument9 pagesAcc Concepts PP Qnsmoots altNo ratings yet

- Assignment 2.2Document6 pagesAssignment 2.2GLEN JORDAN ANTONIONo ratings yet

- Inventory EstimationDocument4 pagesInventory EstimationEryn GabrielleNo ratings yet

- April-22 - Louise Peralta - 11 - FairnessDocument3 pagesApril-22 - Louise Peralta - 11 - FairnessLouise Joseph PeraltaNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- IAS - 7 Statement of Cash FlowsDocument29 pagesIAS - 7 Statement of Cash FlowsKəmalə AslanzadəNo ratings yet

- Chapter 7: Equity, Capital and Dividends: 7.1.1 AimsDocument12 pagesChapter 7: Equity, Capital and Dividends: 7.1.1 AimsKəmalə AslanzadəNo ratings yet

- Section B Answer Question 1 and Not More Than One Further Question From This Section. Question 1Document3 pagesSection B Answer Question 1 and Not More Than One Further Question From This Section. Question 1Kəmalə AslanzadəNo ratings yet

- Sample CIBIL Report - IndividualDocument63 pagesSample CIBIL Report - IndividualNeeraj DaultaniNo ratings yet

- Consumer Rights AASRAADocument17 pagesConsumer Rights AASRAASourav MandalNo ratings yet

- P Siva Sankar SBI Statement2Document15 pagesP Siva Sankar SBI Statement2pulapa umamaheswara raoNo ratings yet

- Ivi Farm Feasibility StudyDocument8 pagesIvi Farm Feasibility StudyEBENEZERNo ratings yet

- Assignment 2 Course: Cross Culture Management Class: Bba-6 Submitted To: Sir Faisal Sultan Submitted By: Mahnoor Hammad (11842) Khurram Tasleem (11972)Document14 pagesAssignment 2 Course: Cross Culture Management Class: Bba-6 Submitted To: Sir Faisal Sultan Submitted By: Mahnoor Hammad (11842) Khurram Tasleem (11972)muhammadsaadkhanNo ratings yet

- ErpDocument164 pagesErpMohamed Asif Ali HNo ratings yet

- Swot Anlaysis of Abdul Monem GroupDocument19 pagesSwot Anlaysis of Abdul Monem GroupIsrat Jahan JarinNo ratings yet

- Module 1 - Strategic Business AnalysisDocument17 pagesModule 1 - Strategic Business AnalysisPrime Johnson FelicianoNo ratings yet

- Preface: Guidelines For PPP ProjectsDocument48 pagesPreface: Guidelines For PPP ProjectsmanugeorgeNo ratings yet

- Taylor'S Laundry ServicesDocument2 pagesTaylor'S Laundry Servicesdrsravya reddyNo ratings yet

- Literature Review: The Effect of Online Shops On Consumer: Shopping SatisfactionDocument6 pagesLiterature Review: The Effect of Online Shops On Consumer: Shopping Satisfactionsamantha beatrice apinesNo ratings yet

- Chap 12Document23 pagesChap 12Maria SyNo ratings yet

- Chapter 6Document26 pagesChapter 6shaykh.faNo ratings yet

- Lista de Verificação de Prontidão ISO 45001 - 2018 - SafetyCultureDocument20 pagesLista de Verificação de Prontidão ISO 45001 - 2018 - SafetyCultureCleverson Santos QueirozNo ratings yet

- Vivy YusofDocument2 pagesVivy YusofNassim NoriqmalNo ratings yet

- Annex 1-6-Cooperative Productive Society Fowa EnglishDocument3 pagesAnnex 1-6-Cooperative Productive Society Fowa EnglishWikileaks2024No ratings yet

- FG Terms & ConditionsDocument9 pagesFG Terms & ConditionsF. A AhmedNo ratings yet

- Michael Porter - The EconomistDocument3 pagesMichael Porter - The EconomistDz KNo ratings yet

- A Study On Factors Affecting The Capitalization RateDocument13 pagesA Study On Factors Affecting The Capitalization Ratemtamilv100% (1)

- Name: Abhishek Kumar Employee ID: 162225: Fixed Compensation Variable Compensation Total Cash CompensationDocument3 pagesName: Abhishek Kumar Employee ID: 162225: Fixed Compensation Variable Compensation Total Cash CompensationManish KumarNo ratings yet

- DataDocument5 pagesDataXevivek PrajapatiNo ratings yet

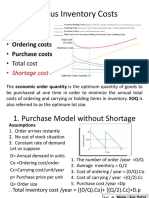

- Various Inventory Costs: - Holding / - Ordering Costs - Purchase Costs - Total CostDocument28 pagesVarious Inventory Costs: - Holding / - Ordering Costs - Purchase Costs - Total CostAditya Dashputre100% (2)

- # Short Cases - SCMDocument16 pages# Short Cases - SCMArthur AquamanNo ratings yet

- Foxconn Additional QuestionsDocument3 pagesFoxconn Additional QuestionsangelllNo ratings yet

- Diagnostics Apps Check 261110Document315 pagesDiagnostics Apps Check 261110Rohit Kumar VijNo ratings yet

- APPENDICES Hollowblocks FinalDocument13 pagesAPPENDICES Hollowblocks FinalJerriel MisolesNo ratings yet

- Executive Summary TechnicalDocument2 pagesExecutive Summary TechnicalSoma ShekarNo ratings yet

- Marginal CostingDocument9 pagesMarginal CostingJoydip DasguptaNo ratings yet

- History of Companies ActDocument5 pagesHistory of Companies ActAthisaya cgNo ratings yet