Download as pptx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Balance Sheet Valix C1ValixDocument14 pagesBalance Sheet Valix C1Valixmaryqueenramos79% (24)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Chapter 3 Challenges in The Internal EnviromentsDocument5 pagesChapter 3 Challenges in The Internal EnviromentsBibi100% (3)

- DuPont PDFDocument5 pagesDuPont PDFMadhur100% (1)

- Behavioral FinanceDocument184 pagesBehavioral FinanceSatya ReddyNo ratings yet

- Resignation LetterDocument1 pageResignation LetterBibiNo ratings yet

- BbbaDocument5 pagesBbbaBibiNo ratings yet

- Graham PastillasDocument15 pagesGraham PastillasBibiNo ratings yet

- Module-5-DAVID, ERLYN A.Document4 pagesModule-5-DAVID, ERLYN A.BibiNo ratings yet

- Cultural Systems Around The GlobeDocument2 pagesCultural Systems Around The GlobeBibiNo ratings yet

- ErlynDocument2 pagesErlynBibiNo ratings yet

- BACC6/ ECC10 Final ExaminationDocument3 pagesBACC6/ ECC10 Final ExaminationBibiNo ratings yet

- Case Analysis FormatDocument2 pagesCase Analysis FormatBibiNo ratings yet

- 1차 문제은행 국제재무기초 이상휘Document50 pages1차 문제은행 국제재무기초 이상휘JunNo ratings yet

- FA2e Chapter12 Solutions ManualDocument78 pagesFA2e Chapter12 Solutions Manual齐瀚飞No ratings yet

- The Definitive Guide To Building A: Winning Forex Trading SystemDocument63 pagesThe Definitive Guide To Building A: Winning Forex Trading SystemStephen ShekwonuDuza HoSeaNo ratings yet

- Final Edition GuideDocument4 pagesFinal Edition GuideAlister MackinnonNo ratings yet

- Multiple Choice Problems 9Document15 pagesMultiple Choice Problems 9Dieter LudwigNo ratings yet

- Aicpa Draft-Inventory-Valuation-GuidanceDocument50 pagesAicpa Draft-Inventory-Valuation-GuidanceOmar OteroNo ratings yet

- A Practical Guide To KII: Key Investor InformationDocument2 pagesA Practical Guide To KII: Key Investor InformationAnt ThoNo ratings yet

- BFN 313-Financial Modelling and ForecastingDocument3 pagesBFN 313-Financial Modelling and ForecastingIsaack MohamedNo ratings yet

- International Finance PDFDocument339 pagesInternational Finance PDFcmukherjeeNo ratings yet

- ISE Internship Report-AIOUDocument102 pagesISE Internship Report-AIOUKomal ShujaatNo ratings yet

- Review FinalDocument10 pagesReview FinalNguyen Minh QuanNo ratings yet

- Final Exam: Derivatives and Risk ManagementDocument29 pagesFinal Exam: Derivatives and Risk ManagementTrang Nguyễn Hoàng LêNo ratings yet

- QUANT BooksDocument6 pagesQUANT Bookssukumar72100% (1)

- Corporate Finance Asia Edition (Solution Manual)Document3 pagesCorporate Finance Asia Edition (Solution Manual)Kinglam Tse20% (15)

- Lecture 11 - The Costs of ProductionDocument22 pagesLecture 11 - The Costs of ProductionMUHAMMAD 23125No ratings yet

- Ratio Analysis. A) Liquidity Ratio - 1) Current Ratio Current Asset Current LiabilityDocument6 pagesRatio Analysis. A) Liquidity Ratio - 1) Current Ratio Current Asset Current LiabilitysolomonNo ratings yet

- FA CIE 1 Zyra Shireen SheriffDocument7 pagesFA CIE 1 Zyra Shireen SheriffPoojith KumarNo ratings yet

- Cost of Capital2022Document39 pagesCost of Capital2022Yassin IslamNo ratings yet

- Amity School of Business Amity University Uttar Pradesh NoidaDocument15 pagesAmity School of Business Amity University Uttar Pradesh NoidaGautam TandonNo ratings yet

- Dec 2002 - AnsDocument14 pagesDec 2002 - AnsHubbak KhanNo ratings yet

- Valuation of BondsDocument7 pagesValuation of BondsHannah Louise Gutang PortilloNo ratings yet

- 5 - Intraday Pattern Practice SessionDocument12 pages5 - Intraday Pattern Practice SessioncollegetradingexchangeNo ratings yet

- ACT 410 Financial Statement Analysis: Week 2Document35 pagesACT 410 Financial Statement Analysis: Week 2zubaidzamanNo ratings yet

- R Aditya Rayhan Zanesty - 29223341 - Entrepreneurship 26Document41 pagesR Aditya Rayhan Zanesty - 29223341 - Entrepreneurship 26R. Aditya Rayhan ZanestyNo ratings yet

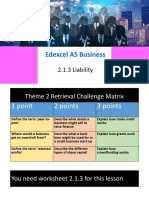

- 2.1.3 AS LiabilityDocument23 pages2.1.3 AS LiabilityEhtesham UmerNo ratings yet

- LaTeX Format For IEEE Journal SubmissionDocument1 pageLaTeX Format For IEEE Journal SubmissionJaydev RavalNo ratings yet

- Ch03 PPTDocument56 pagesCh03 PPTmuhammad AdeelNo ratings yet