Download as pptx, pdf, or txt

You might also like

- Chapter 4Document8 pagesChapter 4Châu Ánh ViNo ratings yet

- Variable and Absorption CostingDocument38 pagesVariable and Absorption CostingstarlightNo ratings yet

- Accounting For Materials: I. Opening Prayer III. Overview of The Topic IV. Discussion II. AnnouncementsDocument38 pagesAccounting For Materials: I. Opening Prayer III. Overview of The Topic IV. Discussion II. AnnouncementsJasmin ToqueNo ratings yet

- Famba 8e - SM - Mod 02 - 040220 1Document25 pagesFamba 8e - SM - Mod 02 - 040220 1Shady Mohsen MikhealNo ratings yet

- Quiz 1 & 2 (Far)Document26 pagesQuiz 1 & 2 (Far)Leane MarcoletaNo ratings yet

- Theory of Production CostDocument17 pagesTheory of Production CostDherya AgarwalNo ratings yet

- Transaction Process System AisDocument3 pagesTransaction Process System AisGem BaguinonNo ratings yet

- Report OnSolve Failing To Plan Is Planning To FailDocument19 pagesReport OnSolve Failing To Plan Is Planning To FailibrahimNo ratings yet

- Hybrid Work PresentationDocument12 pagesHybrid Work PresentationomarmanskopNo ratings yet

- Predetermined Overhead RatesDocument16 pagesPredetermined Overhead RatesjangjangNo ratings yet

- Meyer and Allen Model of Organizational CommitmentDocument3 pagesMeyer and Allen Model of Organizational CommitmentVia11No ratings yet

- Answer To Chapter 5 - Introduction To EthicsDocument1 pageAnswer To Chapter 5 - Introduction To EthicsFaith MarasiganNo ratings yet

- Introduction-Business LawDocument12 pagesIntroduction-Business LawAmirul Hakim Nor AzmanNo ratings yet

- Case Studies - PlanningDocument9 pagesCase Studies - PlanningVraj GamingNo ratings yet

- Cost Concepts and ClassificationsDocument15 pagesCost Concepts and ClassificationsMae Ann KongNo ratings yet

- Notes in Business Laws and RegulationsDocument10 pagesNotes in Business Laws and RegulationsZie TanNo ratings yet

- IFE MatrixDocument2 pagesIFE MatrixGraciella Tiffany100% (1)

- Revenue Memorandum Order No. 10-2021: Bureau of Internal RevenueDocument5 pagesRevenue Memorandum Order No. 10-2021: Bureau of Internal RevenueEarl PatrickNo ratings yet

- The Philippine Financial System (Revised 2020) PDFDocument1 pageThe Philippine Financial System (Revised 2020) PDFearlanthonyNo ratings yet

- Non Current Assets EssayDocument9 pagesNon Current Assets Essaystorky05600% (1)

- MODCOS2 Business CaseDocument8 pagesMODCOS2 Business CaseLou Brad IgnacioNo ratings yet

- Chapter 1 Governance - Ballada-MergedDocument94 pagesChapter 1 Governance - Ballada-MergedUnnamed homosapienNo ratings yet

- ACCCOB3Document87 pagesACCCOB3Lexy SungaNo ratings yet

- Actreg1 Notes 4Document33 pagesActreg1 Notes 4nuggsNo ratings yet

- Overview of The Financial SystemDocument63 pagesOverview of The Financial Systemhabiba ahmed100% (1)

- Actreg1 Notes 3Document33 pagesActreg1 Notes 3nuggsNo ratings yet

- Kinney 8e - CH 06Document19 pagesKinney 8e - CH 06Ashik Uz ZamanNo ratings yet

- Shareholders' EquityDocument6 pagesShareholders' EquityralphalonzoNo ratings yet

- Deductions From Gross EstateDocument16 pagesDeductions From Gross EstateJebeth RiveraNo ratings yet

- Module 03 - Income Tax ConceptsDocument29 pagesModule 03 - Income Tax ConceptsTrixie OnglaoNo ratings yet

- Planning As FunctionDocument11 pagesPlanning As Functionsonu_saisNo ratings yet

- Chapter 4 Reviewer Law 2 7Document6 pagesChapter 4 Reviewer Law 2 7Hannamae Baygan100% (1)

- RA No. 11976 - Ease of Paying Taxes ActDocument22 pagesRA No. 11976 - Ease of Paying Taxes ActAnostasia NemusNo ratings yet

- ACYFAR2 SyllabusDocument6 pagesACYFAR2 SyllabusCharlene Ashley CuNo ratings yet

- Chapter 1 With Quick CheckDocument48 pagesChapter 1 With Quick CheckSigit AryantoNo ratings yet

- Omnibus Investment CodeDocument7 pagesOmnibus Investment CodeKimmee LeeNo ratings yet

- Segment Reporting Decentralized Operations and Responsibility Accounting SystemDocument34 pagesSegment Reporting Decentralized Operations and Responsibility Accounting SystemalliahnahNo ratings yet

- Variable and Absorption CostingDocument3 pagesVariable and Absorption CostingAreeb Baqai100% (1)

- Module 6 FINP1 Financial ManagementDocument28 pagesModule 6 FINP1 Financial ManagementChristine Jane LumocsoNo ratings yet

- Best Brew CorporationDocument4 pagesBest Brew CorporationIsabella GimaoNo ratings yet

- Notes On Corporate Liquidation PDFDocument16 pagesNotes On Corporate Liquidation PDFFernando III PerezNo ratings yet

- 2 Inventory Cost Flow Intermediate Accounting ReviewerDocument3 pages2 Inventory Cost Flow Intermediate Accounting ReviewerDalia ElarabyNo ratings yet

- Lesson 1 - Cost Accounting - Overview of Cost AccountingDocument282 pagesLesson 1 - Cost Accounting - Overview of Cost AccountingMama MiyaNo ratings yet

- Petitioner vs. vs. Respondents R.C. Domingo Jr. & AssociatesDocument8 pagesPetitioner vs. vs. Respondents R.C. Domingo Jr. & AssociatesChristine Ang CaminadeNo ratings yet

- Kinney 8e - CH 09Document17 pagesKinney 8e - CH 09Ashik Uz ZamanNo ratings yet

- Economics-1 BALLB-207: Unit 3: MonopolyDocument23 pagesEconomics-1 BALLB-207: Unit 3: MonopolyAnonymousNo ratings yet

- Absorption and Variable CostingDocument15 pagesAbsorption and Variable CostingApril Pearl VenezuelaNo ratings yet

- Strategic Tax Management - Week 3Document14 pagesStrategic Tax Management - Week 3Arman DalisayNo ratings yet

- DAY 1 Part 1 Fundamental Principles of Taxation StudentsDocument5 pagesDAY 1 Part 1 Fundamental Principles of Taxation StudentsMary Chrisdel Obinque GarciaNo ratings yet

- Quiz-10 2Document13 pagesQuiz-10 2Yasmin Abdul WahabNo ratings yet

- Preference of CreditsDocument9 pagesPreference of CreditsJovy Balangue MacadaegNo ratings yet

- Financial InstrumentsDocument4 pagesFinancial Instrumentsbad geniusNo ratings yet

- The Planning FunctionDocument14 pagesThe Planning FunctionXaĦid WaqarNo ratings yet

- Module 2 Cost Behavior - Scatter & High-LowDocument37 pagesModule 2 Cost Behavior - Scatter & High-LowColeng RiveraNo ratings yet

- Ethical Dilemma Case StudyDocument1 pageEthical Dilemma Case StudyeshaalNo ratings yet

- Financial Accounting and Reporting - Property, Plant and EquipmentDocument7 pagesFinancial Accounting and Reporting - Property, Plant and EquipmentLuisitoNo ratings yet

- Prelims FBTDocument38 pagesPrelims FBTApril Joy ObedozaNo ratings yet

- Regulatory Framework and Legal Issues in Business Activity 1Document4 pagesRegulatory Framework and Legal Issues in Business Activity 1x xNo ratings yet

- Accounting QuestionsDocument8 pagesAccounting QuestionsHuryaNo ratings yet

- CSE - Newly Enacted Laws Environmental ProtectionDocument7 pagesCSE - Newly Enacted Laws Environmental ProtectionVienna Corrine Quijano AbucejoNo ratings yet

- Win Ballada, 2021 Basic Financial Accounting and Reporting (Made Easy)Document608 pagesWin Ballada, 2021 Basic Financial Accounting and Reporting (Made Easy)krishia jainneNo ratings yet

- College of Accountancy: Mary The Queen College (Pampanga), IncDocument3 pagesCollege of Accountancy: Mary The Queen College (Pampanga), IncPoison IvyNo ratings yet

- Chapter 3Document40 pagesChapter 3Korubel Asegdew YimenuNo ratings yet

- Accounting Rate of ReturnDocument7 pagesAccounting Rate of ReturnMahesh RaoNo ratings yet

- Financial Accounting Waec PDFDocument5 pagesFinancial Accounting Waec PDFAndrew Tandoh100% (1)

- About FRSC and PIC: A Chairman and MembersDocument2 pagesAbout FRSC and PIC: A Chairman and MembersChristian PerezNo ratings yet

- Ican Annual Report 2006 07Document52 pagesIcan Annual Report 2006 07casarokarNo ratings yet

- Accounting Concepts Conventions and Principles NotesDocument21 pagesAccounting Concepts Conventions and Principles Notesvarshika GunasekeranNo ratings yet

- ACN202-Lesson PlanDocument26 pagesACN202-Lesson PlanMaher Neger AneyNo ratings yet

- The Effects of Time Budget Pressure and Risk of Error On Auditor PerformanceDocument32 pagesThe Effects of Time Budget Pressure and Risk of Error On Auditor PerformanceLarasNo ratings yet

- Accounting: Definition, Scope, Nature, Objectives Accounting DefinedDocument3 pagesAccounting: Definition, Scope, Nature, Objectives Accounting DefinedDeuter AbusoNo ratings yet

- SAP FICO ProcessesDocument21 pagesSAP FICO ProcessesGaurav Tipnis0% (1)

- Page 206: EX. 4.3:: Problem Solving: Chapter 4Document3 pagesPage 206: EX. 4.3:: Problem Solving: Chapter 4Rebecca AntoniosNo ratings yet

- FI Sep 2018 PDFDocument19 pagesFI Sep 2018 PDFsheeraz ali khuhroNo ratings yet

- Full Download Solution Manual For Core Concepts of Accounting Raiborn 2nd Edition PDF Full ChapterDocument34 pagesFull Download Solution Manual For Core Concepts of Accounting Raiborn 2nd Edition PDF Full Chapterhebraizelathyos6cae100% (24)

- AEG-evidence From SingaporeDocument13 pagesAEG-evidence From SingaporeSiti Arbaiyah AhmadNo ratings yet

- House Bank Configuration AmanDocument12 pagesHouse Bank Configuration AmanAman Verma0% (1)

- Outline - PIPFADocument60 pagesOutline - PIPFAijazaslam999No ratings yet

- FA - MCQ'sDocument8 pagesFA - MCQ'sAshika JayaweeraNo ratings yet

- IAS 1 FInancial Reporting - HandoutDocument19 pagesIAS 1 FInancial Reporting - HandoutInnocent escoNo ratings yet

- Accounting StandardsDocument3 pagesAccounting StandardsLeslie CortesNo ratings yet

- IPSAS 17. Property-Plant - EquipmentDocument28 pagesIPSAS 17. Property-Plant - EquipmentKibromWeldegiyorgisNo ratings yet

- Testbank: Applying Ifrs Standards 4eDocument11 pagesTestbank: Applying Ifrs Standards 4eSyed Bilal AliNo ratings yet

- Dwnload Full Fundamental Accounting Principles Canadian Canadian 14th Edition Larson Solutions Manual PDFDocument36 pagesDwnload Full Fundamental Accounting Principles Canadian Canadian 14th Edition Larson Solutions Manual PDFexiguity.siroc.r1zj100% (11)

- Introductory AccountingDocument8 pagesIntroductory AccountingLIM HUI NI STUDENTNo ratings yet

- MBAB 5P01 - Chapter 1Document3 pagesMBAB 5P01 - Chapter 1Priya MehtaNo ratings yet

- Chap 1 Test BankDocument22 pagesChap 1 Test BankMike SerafinoNo ratings yet

- Ysch Oolg Ist.c Om: Principles of Accounts General ObjectivesDocument6 pagesYsch Oolg Ist.c Om: Principles of Accounts General ObjectivesGabriel UdokangNo ratings yet

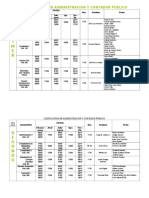

- P R I M E R: Licenciatura en Administración Y Contador PúblicoDocument7 pagesP R I M E R: Licenciatura en Administración Y Contador PúblicomatiasNo ratings yet