Composition Scheme: - Dhwani Mainkar

Composition Scheme: - Dhwani Mainkar

You might also like

- 2013 REG Last Minute Study Notes (Bonus)Document47 pages2013 REG Last Minute Study Notes (Bonus)olegscherbina100% (3)

- How To Open A Pharmacy in PakistanDocument7 pagesHow To Open A Pharmacy in PakistanGulzar Ahmad Rawn73% (15)

- CombinepdfDocument129 pagesCombinepdfMary Jane G. FACERONDANo ratings yet

- Process of IPO in IndiaDocument4 pagesProcess of IPO in IndiaBasappaSarkarNo ratings yet

- GST Composition SchemeDocument2 pagesGST Composition SchemeVikram AruchamyNo ratings yet

- Sales Tax System in IndiaDocument7 pagesSales Tax System in IndiaKarthi_docNo ratings yet

- A Brief On VAT (Value Added Tax)Document8 pagesA Brief On VAT (Value Added Tax)San Deep SharmaNo ratings yet

- Tax On CorporationsDocument6 pagesTax On CorporationsJumen Gamaru TamayoNo ratings yet

- Final Withholding Tax FWT and CapitalDocument40 pagesFinal Withholding Tax FWT and CapitalEdna PostreNo ratings yet

- Composition Scheme GSTDocument3 pagesComposition Scheme GSTUttiya BasuNo ratings yet

- FAQ-Composition SchemeDocument2 pagesFAQ-Composition SchemeSejal GuptaNo ratings yet

- Bombay PicklesDocument8 pagesBombay PicklesSuyash NigotiaNo ratings yet

- Final Withholding Tax FWT and CapitalDocument39 pagesFinal Withholding Tax FWT and CapitalJessa HerreraNo ratings yet

- Q. What Is Value Added Tax (VAT) ?Document8 pagesQ. What Is Value Added Tax (VAT) ?Akhilesh SinghNo ratings yet

- Sikkim VatDocument9 pagesSikkim VatAnjali Angel ThakurNo ratings yet

- Sales Tax & VATDocument30 pagesSales Tax & VATAnonymous sfAOc3TKNo ratings yet

- Income Tax - Chap 07Document6 pagesIncome Tax - Chap 07ZainioNo ratings yet

- Taxation 2012 1Document44 pagesTaxation 2012 1mudassarNo ratings yet

- Lemon Law Q & ADocument25 pagesLemon Law Q & ADanzen Bueno Imus100% (1)

- Dfinal - Allow DeductionsDocument76 pagesDfinal - Allow DeductionsRexell DepalacNo ratings yet

- Value Added Tax Part 2Document14 pagesValue Added Tax Part 2Catherine LicudoNo ratings yet

- Vat IndiaDocument3 pagesVat IndiarajailayaNo ratings yet

- Module 4 Optional Tax Rate For Self EmployedDocument7 pagesModule 4 Optional Tax Rate For Self EmployedJam HailNo ratings yet

- SEBI - GuidelinesDocument38 pagesSEBI - GuidelinesBalajiNo ratings yet

- Chapter 17Document10 pagesChapter 17Neriza maningasNo ratings yet

- Automotive Sales, Use & Lease Tax Guide: September 2019Document16 pagesAutomotive Sales, Use & Lease Tax Guide: September 2019student_physicianNo ratings yet

- VAT RulesDocument11 pagesVAT RulesamrkiplNo ratings yet

- 59rinl Rural Dealership Scheme RevDocument8 pages59rinl Rural Dealership Scheme RevKedhareesh KNo ratings yet

- Jaral Traders: Bid Specific Addition Terms and ConditionsDocument6 pagesJaral Traders: Bid Specific Addition Terms and ConditionsSushant DuttaNo ratings yet

- WR Farmer's Market Vendor RulesDocument3 pagesWR Farmer's Market Vendor RulesgarnetstreetNo ratings yet

- Training Savings Plans From ScratchDocument36 pagesTraining Savings Plans From ScratchScribdTranslationsNo ratings yet

- Sales TaxDocument9 pagesSales Taxmay leeNo ratings yet

- Background: Read The History of Fairtrade Labelling InternationallyDocument8 pagesBackground: Read The History of Fairtrade Labelling Internationallysreekan2No ratings yet

- MSJG Income Tax Chapter 3 NotesDocument3 pagesMSJG Income Tax Chapter 3 NotesMar Sean Jan GabiosaNo ratings yet

- VTL301 Trade Licence Guidance NotesDocument2 pagesVTL301 Trade Licence Guidance Notesjamesgoodridge4No ratings yet

- UniLOAD DISTRIBUTOR2Document2 pagesUniLOAD DISTRIBUTOR2sh33nrastaNo ratings yet

- UntitledDocument8 pagesUntitledsuyash dugarNo ratings yet

- Module 5 Philippine Income Taxation CorporationDocument63 pagesModule 5 Philippine Income Taxation CorporationFlameNo ratings yet

- Part 3Document4 pagesPart 3Cahaya HaniNo ratings yet

- M10 Introduction To Business Taxation StudentsDocument33 pagesM10 Introduction To Business Taxation StudentsTokis SabaNo ratings yet

- CHAPTER 5 Corporate Income Taxation Regular Corporations ModuleDocument10 pagesCHAPTER 5 Corporate Income Taxation Regular Corporations ModuleShane Mark CabiasaNo ratings yet

- What Are Rates of Tax Under VAT?Document14 pagesWhat Are Rates of Tax Under VAT?api-3762419100% (2)

- Business Tax SummaryDocument10 pagesBusiness Tax SummaryJohn Raymond MarzanNo ratings yet

- HPBL Liquor Sales Policy 2017-1829032017185129Document12 pagesHPBL Liquor Sales Policy 2017-1829032017185129anilNo ratings yet

- SEBI Takeover Regulation 2011Document9 pagesSEBI Takeover Regulation 2011Himanshu AggarwalNo ratings yet

- Distributorship Agreement: 1. Appointment and Scope of The AgreementDocument8 pagesDistributorship Agreement: 1. Appointment and Scope of The AgreementAhmed AwnNo ratings yet

- Procedure To Be Followed For Delhi Value Added TaxDocument6 pagesProcedure To Be Followed For Delhi Value Added TaxChirag MalhotraNo ratings yet

- BCH 601 SM12Document10 pagesBCH 601 SM12technical analysisNo ratings yet

- VAT 11th-Edn-2012Document3,438 pagesVAT 11th-Edn-2012kommurisatishgstNo ratings yet

- IMFLDocument17 pagesIMFLSubhashish NandaNo ratings yet

- Phase 2Document7 pagesPhase 2saidmahamoud2001No ratings yet

- Business Law & Practice - Course SummaryDocument40 pagesBusiness Law & Practice - Course SummaryPolina KriulinaNo ratings yet

- Other Percentage TaxesDocument40 pagesOther Percentage TaxesKay Hanalee Villanueva NorioNo ratings yet

- TAXATION Ver 2Document3 pagesTAXATION Ver 2coleenllb_usaNo ratings yet

- Taxation PDFDocument55 pagesTaxation PDFHumphrey OdchigueNo ratings yet

- TAX Percentage TaxDocument19 pagesTAX Percentage TaxkmabcdeNo ratings yet

- Transfer From Normal Dealer To Compounding DealerDocument1 pageTransfer From Normal Dealer To Compounding DealerShivanand yadavNo ratings yet

- Business Taxation: Rex B. Banggawan, Cpa, MbaDocument50 pagesBusiness Taxation: Rex B. Banggawan, Cpa, MbaAllyson VillalobosNo ratings yet

- Request Form - R-Multi Ref Plan - v7.3Document3 pagesRequest Form - R-Multi Ref Plan - v7.3Vimal SinghNo ratings yet

- Pricing of Agricultural Goods - Neha Sharma, B053Document5 pagesPricing of Agricultural Goods - Neha Sharma, B053Neha SharmaNo ratings yet

- Quiz - Mvat: - Ms. Dhwani MainkarDocument4 pagesQuiz - Mvat: - Ms. Dhwani MainkarNeha SharmaNo ratings yet

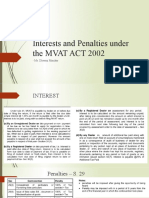

- Interests and Penalties Under The MVAT ACT 2002: - Ms. Dhwani MainkarDocument3 pagesInterests and Penalties Under The MVAT ACT 2002: - Ms. Dhwani MainkarNeha SharmaNo ratings yet

- Family Law Conjugal RightsDocument6 pagesFamily Law Conjugal RightsNeha Sharma100% (1)

- Wealth Taxes in India: - Ms. Dhwani MainkarDocument12 pagesWealth Taxes in India: - Ms. Dhwani MainkarNeha Sharma100% (1)

- Section 3 4 and 5 - CSTDocument4 pagesSection 3 4 and 5 - CSTNeha SharmaNo ratings yet

- Sales Tax Authorities: - Ms. Dhwani MainkarDocument8 pagesSales Tax Authorities: - Ms. Dhwani MainkarNeha SharmaNo ratings yet

- Request For Arbitration (Draft)Document9 pagesRequest For Arbitration (Draft)Neha SharmaNo ratings yet

- 8101 - Contract 2 - Semester 8Document5 pages8101 - Contract 2 - Semester 8Neha SharmaNo ratings yet

- IEUK Clyde & Co Work Sample Instructions 2021Document18 pagesIEUK Clyde & Co Work Sample Instructions 2021Neha SharmaNo ratings yet

- Declaration & Payment of Dividend Declaration & Payment of Dividend Declaration & Payment of DividendDocument4 pagesDeclaration & Payment of Dividend Declaration & Payment of Dividend Declaration & Payment of DividendNeha SharmaNo ratings yet

- MCQs On Contract IIDocument26 pagesMCQs On Contract IINeha Sharma100% (1)

- Business Audit - MVATDocument10 pagesBusiness Audit - MVATNeha SharmaNo ratings yet

- AJAD 2013 10 1 6tripathiDocument21 pagesAJAD 2013 10 1 6tripathiNeha SharmaNo ratings yet

- Price Distortions in Indian Agriculture 2017Document128 pagesPrice Distortions in Indian Agriculture 2017Neha SharmaNo ratings yet

- Registration Under MVATDocument16 pagesRegistration Under MVATNeha SharmaNo ratings yet

- Muslim Marriage and Divorce Act: Laws of Trinidad and TobagoDocument44 pagesMuslim Marriage and Divorce Act: Laws of Trinidad and TobagoNeha SharmaNo ratings yet

- Thermal AnalysisDocument8 pagesThermal AnalysisSURESH100% (1)

- The Functionalist's View On Family (Sociology)Document9 pagesThe Functionalist's View On Family (Sociology)Donique GrahamNo ratings yet

- Production & Operation Management - POM PDFDocument4 pagesProduction & Operation Management - POM PDFHiren Kotadia0% (2)

- Case StudyDocument14 pagesCase Studyapi-663318600No ratings yet

- European Steel and Alloy Grades: Gx8Crni12 (1.4107)Document2 pagesEuropean Steel and Alloy Grades: Gx8Crni12 (1.4107)farshid KarpasandNo ratings yet

- 1083ch8 2 PDFDocument19 pages1083ch8 2 PDFMateusz SynowieckiNo ratings yet

- Inner Circle Trader - Progressive Risk ReductionDocument2 pagesInner Circle Trader - Progressive Risk ReductionSteve Smith100% (1)

- Annotated Bibliography MLADocument2 pagesAnnotated Bibliography MLARick CookNo ratings yet

- College Adjustment Scale (CAS)Document7 pagesCollege Adjustment Scale (CAS)Bianca CarmenNo ratings yet

- Sana AfzalDocument5 pagesSana AfzalMishi BajwaNo ratings yet

- Home Learning Environment ECE 17Document11 pagesHome Learning Environment ECE 17Sheeva AbenidoNo ratings yet

- HSE Aviation-Helideck-Operations-Inspection-GuideDocument22 pagesHSE Aviation-Helideck-Operations-Inspection-GuidePierre CarvalhoNo ratings yet

- Legal Advisory April 2022Document24 pagesLegal Advisory April 2022PLTCOL EDGARDO C RIVERANo ratings yet

- CMAM Training PPT 2018 - 0Document57 pagesCMAM Training PPT 2018 - 0cabdinuux32100% (1)

- 1 PDFDocument103 pages1 PDF123qweNo ratings yet

- Supply Chain Management - Pgfa1941Document9 pagesSupply Chain Management - Pgfa1941Ravina SinghNo ratings yet

- Hysteretic Relative Permeability EffectsDocument8 pagesHysteretic Relative Permeability Effectshfdshy12No ratings yet

- DS - Online PD Spot Tester - Liona - BAUR - En-GbDocument4 pagesDS - Online PD Spot Tester - Liona - BAUR - En-GbEngineering CWSBNo ratings yet

- J. Konvitz - Don't Waste A Crisis 2020-04-20Document48 pagesJ. Konvitz - Don't Waste A Crisis 2020-04-20Fondapol100% (1)

- The Winners and Losers of GlobalizationDocument7 pagesThe Winners and Losers of GlobalizationRalucutsaNo ratings yet

- TheologyDocument4 pagesTheologyLovely Platon CantosNo ratings yet

- Republic of The Philippines Municipality of DiffunDocument3 pagesRepublic of The Philippines Municipality of DiffunKrisna Criselda SimbreNo ratings yet

- S1-TITAN Overview BrochureDocument8 pagesS1-TITAN Overview BrochureFedeNo ratings yet

- Analisis Efektivitas Biaya Kombinasi Obat Antihipertensi Pada Pasien Rawat Inap Di Rsud Dr. Soekardjo TasikmalayaDocument10 pagesAnalisis Efektivitas Biaya Kombinasi Obat Antihipertensi Pada Pasien Rawat Inap Di Rsud Dr. Soekardjo TasikmalayaEmiNo ratings yet

- Pre-Extraction Records in Edentulous Patients - A Literature ReviewDocument6 pagesPre-Extraction Records in Edentulous Patients - A Literature ReviewMaywiNo ratings yet

- Drone UnfinishedDocument10 pagesDrone UnfinishedLance Kelly ManlangitNo ratings yet

- Paediatrica Indonesiana: Original ArticleDocument8 pagesPaediatrica Indonesiana: Original ArticleNuaimatul Hani'ahNo ratings yet

- Session-3 (Color Codind and Splicing)Document17 pagesSession-3 (Color Codind and Splicing)Muhammad Ameer SabriNo ratings yet

- 990-736 ABL80 FLEX Service ManualDocument409 pages990-736 ABL80 FLEX Service ManualIsmael MorinigoNo ratings yet

- Design, Calculation and Simulation 3 Dof Capacitive Force SensorDocument5 pagesDesign, Calculation and Simulation 3 Dof Capacitive Force SensorLaNo ratings yet

Download as pptx, pdf, or txt

You might also like

- 2013 REG Last Minute Study Notes (Bonus)Document47 pages2013 REG Last Minute Study Notes (Bonus)olegscherbina100% (3)

- How To Open A Pharmacy in PakistanDocument7 pagesHow To Open A Pharmacy in PakistanGulzar Ahmad Rawn73% (15)

- CombinepdfDocument129 pagesCombinepdfMary Jane G. FACERONDANo ratings yet

- Process of IPO in IndiaDocument4 pagesProcess of IPO in IndiaBasappaSarkarNo ratings yet

- GST Composition SchemeDocument2 pagesGST Composition SchemeVikram AruchamyNo ratings yet

- Sales Tax System in IndiaDocument7 pagesSales Tax System in IndiaKarthi_docNo ratings yet

- A Brief On VAT (Value Added Tax)Document8 pagesA Brief On VAT (Value Added Tax)San Deep SharmaNo ratings yet

- Tax On CorporationsDocument6 pagesTax On CorporationsJumen Gamaru TamayoNo ratings yet

- Final Withholding Tax FWT and CapitalDocument40 pagesFinal Withholding Tax FWT and CapitalEdna PostreNo ratings yet

- Composition Scheme GSTDocument3 pagesComposition Scheme GSTUttiya BasuNo ratings yet

- FAQ-Composition SchemeDocument2 pagesFAQ-Composition SchemeSejal GuptaNo ratings yet

- Bombay PicklesDocument8 pagesBombay PicklesSuyash NigotiaNo ratings yet

- Final Withholding Tax FWT and CapitalDocument39 pagesFinal Withholding Tax FWT and CapitalJessa HerreraNo ratings yet

- Q. What Is Value Added Tax (VAT) ?Document8 pagesQ. What Is Value Added Tax (VAT) ?Akhilesh SinghNo ratings yet

- Sikkim VatDocument9 pagesSikkim VatAnjali Angel ThakurNo ratings yet

- Sales Tax & VATDocument30 pagesSales Tax & VATAnonymous sfAOc3TKNo ratings yet

- Income Tax - Chap 07Document6 pagesIncome Tax - Chap 07ZainioNo ratings yet

- Taxation 2012 1Document44 pagesTaxation 2012 1mudassarNo ratings yet

- Lemon Law Q & ADocument25 pagesLemon Law Q & ADanzen Bueno Imus100% (1)

- Dfinal - Allow DeductionsDocument76 pagesDfinal - Allow DeductionsRexell DepalacNo ratings yet

- Value Added Tax Part 2Document14 pagesValue Added Tax Part 2Catherine LicudoNo ratings yet

- Vat IndiaDocument3 pagesVat IndiarajailayaNo ratings yet

- Module 4 Optional Tax Rate For Self EmployedDocument7 pagesModule 4 Optional Tax Rate For Self EmployedJam HailNo ratings yet

- SEBI - GuidelinesDocument38 pagesSEBI - GuidelinesBalajiNo ratings yet

- Chapter 17Document10 pagesChapter 17Neriza maningasNo ratings yet

- Automotive Sales, Use & Lease Tax Guide: September 2019Document16 pagesAutomotive Sales, Use & Lease Tax Guide: September 2019student_physicianNo ratings yet

- VAT RulesDocument11 pagesVAT RulesamrkiplNo ratings yet

- 59rinl Rural Dealership Scheme RevDocument8 pages59rinl Rural Dealership Scheme RevKedhareesh KNo ratings yet

- Jaral Traders: Bid Specific Addition Terms and ConditionsDocument6 pagesJaral Traders: Bid Specific Addition Terms and ConditionsSushant DuttaNo ratings yet

- WR Farmer's Market Vendor RulesDocument3 pagesWR Farmer's Market Vendor RulesgarnetstreetNo ratings yet

- Training Savings Plans From ScratchDocument36 pagesTraining Savings Plans From ScratchScribdTranslationsNo ratings yet

- Sales TaxDocument9 pagesSales Taxmay leeNo ratings yet

- Background: Read The History of Fairtrade Labelling InternationallyDocument8 pagesBackground: Read The History of Fairtrade Labelling Internationallysreekan2No ratings yet

- MSJG Income Tax Chapter 3 NotesDocument3 pagesMSJG Income Tax Chapter 3 NotesMar Sean Jan GabiosaNo ratings yet

- VTL301 Trade Licence Guidance NotesDocument2 pagesVTL301 Trade Licence Guidance Notesjamesgoodridge4No ratings yet

- UniLOAD DISTRIBUTOR2Document2 pagesUniLOAD DISTRIBUTOR2sh33nrastaNo ratings yet

- UntitledDocument8 pagesUntitledsuyash dugarNo ratings yet

- Module 5 Philippine Income Taxation CorporationDocument63 pagesModule 5 Philippine Income Taxation CorporationFlameNo ratings yet

- Part 3Document4 pagesPart 3Cahaya HaniNo ratings yet

- M10 Introduction To Business Taxation StudentsDocument33 pagesM10 Introduction To Business Taxation StudentsTokis SabaNo ratings yet

- CHAPTER 5 Corporate Income Taxation Regular Corporations ModuleDocument10 pagesCHAPTER 5 Corporate Income Taxation Regular Corporations ModuleShane Mark CabiasaNo ratings yet

- What Are Rates of Tax Under VAT?Document14 pagesWhat Are Rates of Tax Under VAT?api-3762419100% (2)

- Business Tax SummaryDocument10 pagesBusiness Tax SummaryJohn Raymond MarzanNo ratings yet

- HPBL Liquor Sales Policy 2017-1829032017185129Document12 pagesHPBL Liquor Sales Policy 2017-1829032017185129anilNo ratings yet

- SEBI Takeover Regulation 2011Document9 pagesSEBI Takeover Regulation 2011Himanshu AggarwalNo ratings yet

- Distributorship Agreement: 1. Appointment and Scope of The AgreementDocument8 pagesDistributorship Agreement: 1. Appointment and Scope of The AgreementAhmed AwnNo ratings yet

- Procedure To Be Followed For Delhi Value Added TaxDocument6 pagesProcedure To Be Followed For Delhi Value Added TaxChirag MalhotraNo ratings yet

- BCH 601 SM12Document10 pagesBCH 601 SM12technical analysisNo ratings yet

- VAT 11th-Edn-2012Document3,438 pagesVAT 11th-Edn-2012kommurisatishgstNo ratings yet

- IMFLDocument17 pagesIMFLSubhashish NandaNo ratings yet

- Phase 2Document7 pagesPhase 2saidmahamoud2001No ratings yet

- Business Law & Practice - Course SummaryDocument40 pagesBusiness Law & Practice - Course SummaryPolina KriulinaNo ratings yet

- Other Percentage TaxesDocument40 pagesOther Percentage TaxesKay Hanalee Villanueva NorioNo ratings yet

- TAXATION Ver 2Document3 pagesTAXATION Ver 2coleenllb_usaNo ratings yet

- Taxation PDFDocument55 pagesTaxation PDFHumphrey OdchigueNo ratings yet

- TAX Percentage TaxDocument19 pagesTAX Percentage TaxkmabcdeNo ratings yet

- Transfer From Normal Dealer To Compounding DealerDocument1 pageTransfer From Normal Dealer To Compounding DealerShivanand yadavNo ratings yet

- Business Taxation: Rex B. Banggawan, Cpa, MbaDocument50 pagesBusiness Taxation: Rex B. Banggawan, Cpa, MbaAllyson VillalobosNo ratings yet

- Request Form - R-Multi Ref Plan - v7.3Document3 pagesRequest Form - R-Multi Ref Plan - v7.3Vimal SinghNo ratings yet

- Pricing of Agricultural Goods - Neha Sharma, B053Document5 pagesPricing of Agricultural Goods - Neha Sharma, B053Neha SharmaNo ratings yet

- Quiz - Mvat: - Ms. Dhwani MainkarDocument4 pagesQuiz - Mvat: - Ms. Dhwani MainkarNeha SharmaNo ratings yet

- Interests and Penalties Under The MVAT ACT 2002: - Ms. Dhwani MainkarDocument3 pagesInterests and Penalties Under The MVAT ACT 2002: - Ms. Dhwani MainkarNeha SharmaNo ratings yet

- Family Law Conjugal RightsDocument6 pagesFamily Law Conjugal RightsNeha Sharma100% (1)

- Wealth Taxes in India: - Ms. Dhwani MainkarDocument12 pagesWealth Taxes in India: - Ms. Dhwani MainkarNeha Sharma100% (1)

- Section 3 4 and 5 - CSTDocument4 pagesSection 3 4 and 5 - CSTNeha SharmaNo ratings yet

- Sales Tax Authorities: - Ms. Dhwani MainkarDocument8 pagesSales Tax Authorities: - Ms. Dhwani MainkarNeha SharmaNo ratings yet

- Request For Arbitration (Draft)Document9 pagesRequest For Arbitration (Draft)Neha SharmaNo ratings yet

- 8101 - Contract 2 - Semester 8Document5 pages8101 - Contract 2 - Semester 8Neha SharmaNo ratings yet

- IEUK Clyde & Co Work Sample Instructions 2021Document18 pagesIEUK Clyde & Co Work Sample Instructions 2021Neha SharmaNo ratings yet

- Declaration & Payment of Dividend Declaration & Payment of Dividend Declaration & Payment of DividendDocument4 pagesDeclaration & Payment of Dividend Declaration & Payment of Dividend Declaration & Payment of DividendNeha SharmaNo ratings yet

- MCQs On Contract IIDocument26 pagesMCQs On Contract IINeha Sharma100% (1)

- Business Audit - MVATDocument10 pagesBusiness Audit - MVATNeha SharmaNo ratings yet

- AJAD 2013 10 1 6tripathiDocument21 pagesAJAD 2013 10 1 6tripathiNeha SharmaNo ratings yet

- Price Distortions in Indian Agriculture 2017Document128 pagesPrice Distortions in Indian Agriculture 2017Neha SharmaNo ratings yet

- Registration Under MVATDocument16 pagesRegistration Under MVATNeha SharmaNo ratings yet

- Muslim Marriage and Divorce Act: Laws of Trinidad and TobagoDocument44 pagesMuslim Marriage and Divorce Act: Laws of Trinidad and TobagoNeha SharmaNo ratings yet

- Thermal AnalysisDocument8 pagesThermal AnalysisSURESH100% (1)

- The Functionalist's View On Family (Sociology)Document9 pagesThe Functionalist's View On Family (Sociology)Donique GrahamNo ratings yet

- Production & Operation Management - POM PDFDocument4 pagesProduction & Operation Management - POM PDFHiren Kotadia0% (2)

- Case StudyDocument14 pagesCase Studyapi-663318600No ratings yet

- European Steel and Alloy Grades: Gx8Crni12 (1.4107)Document2 pagesEuropean Steel and Alloy Grades: Gx8Crni12 (1.4107)farshid KarpasandNo ratings yet

- 1083ch8 2 PDFDocument19 pages1083ch8 2 PDFMateusz SynowieckiNo ratings yet

- Inner Circle Trader - Progressive Risk ReductionDocument2 pagesInner Circle Trader - Progressive Risk ReductionSteve Smith100% (1)

- Annotated Bibliography MLADocument2 pagesAnnotated Bibliography MLARick CookNo ratings yet

- College Adjustment Scale (CAS)Document7 pagesCollege Adjustment Scale (CAS)Bianca CarmenNo ratings yet

- Sana AfzalDocument5 pagesSana AfzalMishi BajwaNo ratings yet

- Home Learning Environment ECE 17Document11 pagesHome Learning Environment ECE 17Sheeva AbenidoNo ratings yet

- HSE Aviation-Helideck-Operations-Inspection-GuideDocument22 pagesHSE Aviation-Helideck-Operations-Inspection-GuidePierre CarvalhoNo ratings yet

- Legal Advisory April 2022Document24 pagesLegal Advisory April 2022PLTCOL EDGARDO C RIVERANo ratings yet

- CMAM Training PPT 2018 - 0Document57 pagesCMAM Training PPT 2018 - 0cabdinuux32100% (1)

- 1 PDFDocument103 pages1 PDF123qweNo ratings yet

- Supply Chain Management - Pgfa1941Document9 pagesSupply Chain Management - Pgfa1941Ravina SinghNo ratings yet

- Hysteretic Relative Permeability EffectsDocument8 pagesHysteretic Relative Permeability Effectshfdshy12No ratings yet

- DS - Online PD Spot Tester - Liona - BAUR - En-GbDocument4 pagesDS - Online PD Spot Tester - Liona - BAUR - En-GbEngineering CWSBNo ratings yet

- J. Konvitz - Don't Waste A Crisis 2020-04-20Document48 pagesJ. Konvitz - Don't Waste A Crisis 2020-04-20Fondapol100% (1)

- The Winners and Losers of GlobalizationDocument7 pagesThe Winners and Losers of GlobalizationRalucutsaNo ratings yet

- TheologyDocument4 pagesTheologyLovely Platon CantosNo ratings yet

- Republic of The Philippines Municipality of DiffunDocument3 pagesRepublic of The Philippines Municipality of DiffunKrisna Criselda SimbreNo ratings yet

- S1-TITAN Overview BrochureDocument8 pagesS1-TITAN Overview BrochureFedeNo ratings yet

- Analisis Efektivitas Biaya Kombinasi Obat Antihipertensi Pada Pasien Rawat Inap Di Rsud Dr. Soekardjo TasikmalayaDocument10 pagesAnalisis Efektivitas Biaya Kombinasi Obat Antihipertensi Pada Pasien Rawat Inap Di Rsud Dr. Soekardjo TasikmalayaEmiNo ratings yet

- Pre-Extraction Records in Edentulous Patients - A Literature ReviewDocument6 pagesPre-Extraction Records in Edentulous Patients - A Literature ReviewMaywiNo ratings yet

- Drone UnfinishedDocument10 pagesDrone UnfinishedLance Kelly ManlangitNo ratings yet

- Paediatrica Indonesiana: Original ArticleDocument8 pagesPaediatrica Indonesiana: Original ArticleNuaimatul Hani'ahNo ratings yet

- Session-3 (Color Codind and Splicing)Document17 pagesSession-3 (Color Codind and Splicing)Muhammad Ameer SabriNo ratings yet

- 990-736 ABL80 FLEX Service ManualDocument409 pages990-736 ABL80 FLEX Service ManualIsmael MorinigoNo ratings yet

- Design, Calculation and Simulation 3 Dof Capacitive Force SensorDocument5 pagesDesign, Calculation and Simulation 3 Dof Capacitive Force SensorLaNo ratings yet