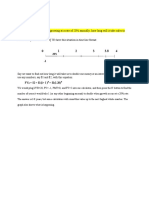

The Behavior Of Interest Rates: Group 9: 1/ Huỳnh Nguyễn Hạ Vy 2/ Đoàn Duy Khánh 3/ Nguyễn Đường Phương Ngọc

The Behavior Of Interest Rates: Group 9: 1/ Huỳnh Nguyễn Hạ Vy 2/ Đoàn Duy Khánh 3/ Nguyễn Đường Phương Ngọc

You might also like

- Microeconomics 13th Edition Parkin Solutions ManualDocument35 pagesMicroeconomics 13th Edition Parkin Solutions Manualbanediswontbd1pap100% (30)

- 14 x11 Financial Management BDocument10 pages14 x11 Financial Management Balexandro_novora639671% (14)

- Walmart's Financial Reporting AnalysisDocument30 pagesWalmart's Financial Reporting AnalysisRabab BI0% (1)

- Intermediate Accounting 1Document46 pagesIntermediate Accounting 1Jashi SiñelNo ratings yet

- Theories of Interest Rates DeterminationDocument9 pagesTheories of Interest Rates DeterminationSenelwa Anaya82% (11)

- A level Economics Revision: Cheeky Revision ShortcutsFrom EverandA level Economics Revision: Cheeky Revision ShortcutsRating: 3 out of 5 stars3/5 (1)

- Assessment of Cash Management in NIBDocument48 pagesAssessment of Cash Management in NIBEfrem Wondale100% (1)

- Internship Report Part2Document40 pagesInternship Report Part2ayshwarya sudheer100% (1)

- CAIA - Level II - Study GuideDocument117 pagesCAIA - Level II - Study GuideJeffrey Baker0% (1)

- Derivatives Project ReportDocument92 pagesDerivatives Project Reportkamdica83% (23)

- Money & Banking: Week 3: The Behavior of Interest RatesDocument33 pagesMoney & Banking: Week 3: The Behavior of Interest RatesAhmad RahhalNo ratings yet

- FINA3010 Lecture 4 (New) PDFDocument91 pagesFINA3010 Lecture 4 (New) PDFKoon Sing ChanNo ratings yet

- The Behavior of Interest Rates: Chap TerDocument9 pagesThe Behavior of Interest Rates: Chap TerHikmət RüstəmovNo ratings yet

- FI - M Lecture 4-Why Do Interest Rates Change - CompleteDocument50 pagesFI - M Lecture 4-Why Do Interest Rates Change - CompleteMoazzam ShahNo ratings yet

- The Behavior of Interest RatesDocument39 pagesThe Behavior of Interest RatesRhazes Zy100% (1)

- Lecture 3. ECON-4803.Document30 pagesLecture 3. ECON-4803.alveemss22No ratings yet

- Financial Markets and InstitutionsDocument72 pagesFinancial Markets and InstitutionsMarioNo ratings yet

- Lec 5 MBDocument42 pagesLec 5 MBjaags057No ratings yet

- Presented by Amir KhanDocument47 pagesPresented by Amir KhanSyed Arham MurtazaNo ratings yet

- Finals MonbankDocument3 pagesFinals MonbankJoniel AsasNo ratings yet

- The Behavior of Interest Rates: Cecchetti, Chapter 7Document41 pagesThe Behavior of Interest Rates: Cecchetti, Chapter 7Trúc Ly Cáp thịNo ratings yet

- Lecture 4: The Behaviour of Interest Rates: WealthDocument10 pagesLecture 4: The Behaviour of Interest Rates: WealthLeung Shing HeiNo ratings yet

- Classical Theory of Rate of InterestDocument5 pagesClassical Theory of Rate of InterestArshaanNo ratings yet

- Portfolio BalanceDocument43 pagesPortfolio BalanceBeyond TutoringNo ratings yet

- Assignment 4 - Liang Jia Ying (U2102926)Document4 pagesAssignment 4 - Liang Jia Ying (U2102926)U2102926 STUDENTNo ratings yet

- Chapter Preview: Why Do Interest Rates Change?Document6 pagesChapter Preview: Why Do Interest Rates Change?shahid faridNo ratings yet

- Keynesian Theory of Money and Interest (Note-This Lecture Is Compiled From The Book of Macroeconomics by L.N. DUTTA For Teaching Purpose Only)Document4 pagesKeynesian Theory of Money and Interest (Note-This Lecture Is Compiled From The Book of Macroeconomics by L.N. DUTTA For Teaching Purpose Only)Abhinandan MazumderNo ratings yet

- Money and Banking Week 1 CH 5Document5 pagesMoney and Banking Week 1 CH 5Pradipta NarendraNo ratings yet

- M&B Ch.5 A.2023Document4 pagesM&B Ch.5 A.2023Amgad ElshamyNo ratings yet

- Chapter 2 - DETERMINATION OF INTEREST RATESDocument36 pagesChapter 2 - DETERMINATION OF INTEREST RATES乙คckคrψ YTNo ratings yet

- Definition of Interest RateDocument6 pagesDefinition of Interest RatebishwajitNo ratings yet

- Finance 5Document11 pagesFinance 5namien koneNo ratings yet

- International Economics II Distance ModuleDocument94 pagesInternational Economics II Distance ModuleBereket Desalegn100% (1)

- Appendix 4 Option Pricing: Cash Flows On OptionsDocument10 pagesAppendix 4 Option Pricing: Cash Flows On Optionsapi-19731569No ratings yet

- Chap 5 ContDocument3 pagesChap 5 ContNa PhưnNo ratings yet

- Lecture No 2 Fundamentals of Financial Markets Interest RateDocument41 pagesLecture No 2 Fundamentals of Financial Markets Interest RateNimco CumarNo ratings yet

- COECA1 - Chapter 3 - Demand and SupplyDocument41 pagesCOECA1 - Chapter 3 - Demand and Supplybanathi nkosiNo ratings yet

- Lecture 6 Behavior of Interest RatesDocument33 pagesLecture 6 Behavior of Interest RatesAman Ullah BalochNo ratings yet

- 6 The Behavior of InterestrateDocument35 pages6 The Behavior of Interestrateyashasvipandey24682No ratings yet

- Chapter 5 Summary - Group 6Document10 pagesChapter 5 Summary - Group 6Phương Anh NguyễnNo ratings yet

- Sale of Government Bonds CB Sells Bonds To The Public and Gets Cash in Return SucksDocument55 pagesSale of Government Bonds CB Sells Bonds To The Public and Gets Cash in Return SucksDora IskandarNo ratings yet

- H#22 Theories of Interest RateDocument3 pagesH#22 Theories of Interest RateMd. Didarul AlamNo ratings yet

- Money, Interest Rates, and Exchange RatesDocument59 pagesMoney, Interest Rates, and Exchange RatesMømë Thãt ŸõûNo ratings yet

- 2 - Money Demand TheoriesDocument8 pages2 - Money Demand Theoriesmajmmallikarachchi.mallikarachchiNo ratings yet

- L 05-Keynessian Viewpoint of Quantity Theory of MoneyDocument8 pagesL 05-Keynessian Viewpoint of Quantity Theory of MoneyNorahNo ratings yet

- Chapter 2Document19 pagesChapter 2ebaaNo ratings yet

- Unit 3 - Monetary EconomicsDocument27 pagesUnit 3 - Monetary EconomicsDanielNo ratings yet

- Money, Interest Rates, and Exchange Rates (Lecture 7)Document8 pagesMoney, Interest Rates, and Exchange Rates (Lecture 7)nihadsamir2002No ratings yet

- City SemIV Regressive Expectation ModelDocument3 pagesCity SemIV Regressive Expectation ModelAmit EshoreNo ratings yet

- Macroeconomics 13th Edition Parkin Solutions ManualDocument35 pagesMacroeconomics 13th Edition Parkin Solutions Manualaraucariabesidesijd835100% (29)

- Financial Market-Lecture 2-2Document23 pagesFinancial Market-Lecture 2-2Krish ShettyNo ratings yet

- Chapter 3 (Unit 1)Document21 pagesChapter 3 (Unit 1)GiriNo ratings yet

- FIM Lecture V VI: Why Do Interest Rates Change?Document15 pagesFIM Lecture V VI: Why Do Interest Rates Change?Aniket GuptaNo ratings yet

- C4-Factors Affecting IRDocument24 pagesC4-Factors Affecting IRDuong Ha ThuyNo ratings yet

- Bond Is A Type of Financial SecurityDocument3 pagesBond Is A Type of Financial Securityjennifer leeNo ratings yet

- Chapter 6: Interest RatesDocument6 pagesChapter 6: Interest RateskafiNo ratings yet

- Chapter26 - Money Demand and Equilibrium Interest RateDocument15 pagesChapter26 - Money Demand and Equilibrium Interest Rateduygualsan1No ratings yet

- Money Demand, The Equilibrium Interest Rate, and Monetary PolicyDocument24 pagesMoney Demand, The Equilibrium Interest Rate, and Monetary PolicyAlmer Faishal WafiNo ratings yet

- Chapter 11 Money Demand and The Equilibrium Interest RateDocument12 pagesChapter 11 Money Demand and The Equilibrium Interest RateWard AlajlouniNo ratings yet

- Interest DefinitionDocument10 pagesInterest Definitionchechi_inNo ratings yet

- Dwnload Full Macroeconomics 13th Edition Parkin Solutions Manual PDFDocument35 pagesDwnload Full Macroeconomics 13th Edition Parkin Solutions Manual PDFelwoodbottifxus100% (12)

- Economics 330 (Kelly) Spring 2001 Answers To Practice Questions #1Document4 pagesEconomics 330 (Kelly) Spring 2001 Answers To Practice Questions #1Phương HàNo ratings yet

- Eco 531 - Chapter 4Document46 pagesEco 531 - Chapter 4Nurul Aina IzzatiNo ratings yet

- Interest RateDocument6 pagesInterest RatesruthipriyamaheshstoryloveNo ratings yet

- Theory of InterestDocument6 pagesTheory of Interestdivyayayadav11No ratings yet

- Avg 64Document1 pageAvg 64JPNo ratings yet

- Trading Game ReportDocument12 pagesTrading Game ReportNguyễn Đường Phương NgọcNo ratings yet

- TAICHINHCONGDocument1 pageTAICHINHCONGNguyễn Đường Phương NgọcNo ratings yet

- 1/ Why Do Banks Exist? DiscussDocument5 pages1/ Why Do Banks Exist? DiscussNguyễn Đường Phương NgọcNo ratings yet

- D. If A Company's Sales Are Growing at A Rate of 20% Annually, How Long Will It Take Sales To Double?Document3 pagesD. If A Company's Sales Are Growing at A Rate of 20% Annually, How Long Will It Take Sales To Double?Nguyễn Đường Phương NgọcNo ratings yet

- Working Capital ManagementDocument92 pagesWorking Capital ManagementJagadish Badi80% (5)

- Banc One Case My SolutionDocument5 pagesBanc One Case My SolutionБорче Шулески67% (3)

- Module 2Document41 pagesModule 2bhargaviNo ratings yet

- ATW September 2016 Investor PresentationDocument15 pagesATW September 2016 Investor PresentationHunterNo ratings yet

- Project RitesDocument72 pagesProject RitesSachin ChadhaNo ratings yet

- Using Financial Accounting Information The Alternative To Debits and Credits 10Th Edition Porter Solutions Manual Full Chapter PDFDocument21 pagesUsing Financial Accounting Information The Alternative To Debits and Credits 10Th Edition Porter Solutions Manual Full Chapter PDFchompdumetoseei5100% (10)

- Financial Statement Analysis - Pantaloon Retail IndiaDocument7 pagesFinancial Statement Analysis - Pantaloon Retail IndiaSupriyaThengdiNo ratings yet

- Laxmi PDFDocument68 pagesLaxmi PDFBharat Singh RathoreNo ratings yet

- Godrej Industries LimitedDocument8 pagesGodrej Industries LimitedJigarNo ratings yet

- Lending Rationale PDFDocument9 pagesLending Rationale PDFNancyNo ratings yet

- Credit Risk Management in BanksDocument19 pagesCredit Risk Management in BanksMahmudur RahmanNo ratings yet

- Tutorial 1: 1. What Is The Basic Functions of Financial Markets?Document6 pagesTutorial 1: 1. What Is The Basic Functions of Financial Markets?Ramsha ShafeelNo ratings yet

- BOJ Financial Sector Update - IMFDocument70 pagesBOJ Financial Sector Update - IMFVenkatesh RamaswamyNo ratings yet

- TestbankDocument33 pagesTestbankBhavneet Sachdeva100% (2)

- Islamic Mortgages in The UK 2020 A Definitive Guide 1Document35 pagesIslamic Mortgages in The UK 2020 A Definitive Guide 1Mahmoud SafaaNo ratings yet

- 16 BibliographyDocument10 pages16 BibliographytouffiqNo ratings yet

- CH 5.palepu - Jw.ca Ratio AnalysisDocument34 pagesCH 5.palepu - Jw.ca Ratio Analysiserza gunawanNo ratings yet

- Effect of Monetary Policy On Real Sector of NepalDocument6 pagesEffect of Monetary Policy On Real Sector of Nepalmr_vishalxpNo ratings yet

- GSE Reform and A Conspiracy of Silence Draft 1.3.1Document11 pagesGSE Reform and A Conspiracy of Silence Draft 1.3.1ny1davidNo ratings yet

- FSA QuestionsDocument1 pageFSA QuestionsNadeemNo ratings yet

- Highway InfrastructureDocument51 pagesHighway InfrastructureBiswarup GhoshNo ratings yet

- Liquidity Cascades - Newfound Research PDFDocument19 pagesLiquidity Cascades - Newfound Research PDFrwmortell3580No ratings yet

- Pestle and Banking IndustryDocument16 pagesPestle and Banking IndustryRegina Leona DeLos SantosNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Microeconomics 13th Edition Parkin Solutions ManualDocument35 pagesMicroeconomics 13th Edition Parkin Solutions Manualbanediswontbd1pap100% (30)

- 14 x11 Financial Management BDocument10 pages14 x11 Financial Management Balexandro_novora639671% (14)

- Walmart's Financial Reporting AnalysisDocument30 pagesWalmart's Financial Reporting AnalysisRabab BI0% (1)

- Intermediate Accounting 1Document46 pagesIntermediate Accounting 1Jashi SiñelNo ratings yet

- Theories of Interest Rates DeterminationDocument9 pagesTheories of Interest Rates DeterminationSenelwa Anaya82% (11)

- A level Economics Revision: Cheeky Revision ShortcutsFrom EverandA level Economics Revision: Cheeky Revision ShortcutsRating: 3 out of 5 stars3/5 (1)

- Assessment of Cash Management in NIBDocument48 pagesAssessment of Cash Management in NIBEfrem Wondale100% (1)

- Internship Report Part2Document40 pagesInternship Report Part2ayshwarya sudheer100% (1)

- CAIA - Level II - Study GuideDocument117 pagesCAIA - Level II - Study GuideJeffrey Baker0% (1)

- Derivatives Project ReportDocument92 pagesDerivatives Project Reportkamdica83% (23)

- Money & Banking: Week 3: The Behavior of Interest RatesDocument33 pagesMoney & Banking: Week 3: The Behavior of Interest RatesAhmad RahhalNo ratings yet

- FINA3010 Lecture 4 (New) PDFDocument91 pagesFINA3010 Lecture 4 (New) PDFKoon Sing ChanNo ratings yet

- The Behavior of Interest Rates: Chap TerDocument9 pagesThe Behavior of Interest Rates: Chap TerHikmət RüstəmovNo ratings yet

- FI - M Lecture 4-Why Do Interest Rates Change - CompleteDocument50 pagesFI - M Lecture 4-Why Do Interest Rates Change - CompleteMoazzam ShahNo ratings yet

- The Behavior of Interest RatesDocument39 pagesThe Behavior of Interest RatesRhazes Zy100% (1)

- Lecture 3. ECON-4803.Document30 pagesLecture 3. ECON-4803.alveemss22No ratings yet

- Financial Markets and InstitutionsDocument72 pagesFinancial Markets and InstitutionsMarioNo ratings yet

- Lec 5 MBDocument42 pagesLec 5 MBjaags057No ratings yet

- Presented by Amir KhanDocument47 pagesPresented by Amir KhanSyed Arham MurtazaNo ratings yet

- Finals MonbankDocument3 pagesFinals MonbankJoniel AsasNo ratings yet

- The Behavior of Interest Rates: Cecchetti, Chapter 7Document41 pagesThe Behavior of Interest Rates: Cecchetti, Chapter 7Trúc Ly Cáp thịNo ratings yet

- Lecture 4: The Behaviour of Interest Rates: WealthDocument10 pagesLecture 4: The Behaviour of Interest Rates: WealthLeung Shing HeiNo ratings yet

- Classical Theory of Rate of InterestDocument5 pagesClassical Theory of Rate of InterestArshaanNo ratings yet

- Portfolio BalanceDocument43 pagesPortfolio BalanceBeyond TutoringNo ratings yet

- Assignment 4 - Liang Jia Ying (U2102926)Document4 pagesAssignment 4 - Liang Jia Ying (U2102926)U2102926 STUDENTNo ratings yet

- Chapter Preview: Why Do Interest Rates Change?Document6 pagesChapter Preview: Why Do Interest Rates Change?shahid faridNo ratings yet

- Keynesian Theory of Money and Interest (Note-This Lecture Is Compiled From The Book of Macroeconomics by L.N. DUTTA For Teaching Purpose Only)Document4 pagesKeynesian Theory of Money and Interest (Note-This Lecture Is Compiled From The Book of Macroeconomics by L.N. DUTTA For Teaching Purpose Only)Abhinandan MazumderNo ratings yet

- Money and Banking Week 1 CH 5Document5 pagesMoney and Banking Week 1 CH 5Pradipta NarendraNo ratings yet

- M&B Ch.5 A.2023Document4 pagesM&B Ch.5 A.2023Amgad ElshamyNo ratings yet

- Chapter 2 - DETERMINATION OF INTEREST RATESDocument36 pagesChapter 2 - DETERMINATION OF INTEREST RATES乙คckคrψ YTNo ratings yet

- Definition of Interest RateDocument6 pagesDefinition of Interest RatebishwajitNo ratings yet

- Finance 5Document11 pagesFinance 5namien koneNo ratings yet

- International Economics II Distance ModuleDocument94 pagesInternational Economics II Distance ModuleBereket Desalegn100% (1)

- Appendix 4 Option Pricing: Cash Flows On OptionsDocument10 pagesAppendix 4 Option Pricing: Cash Flows On Optionsapi-19731569No ratings yet

- Chap 5 ContDocument3 pagesChap 5 ContNa PhưnNo ratings yet

- Lecture No 2 Fundamentals of Financial Markets Interest RateDocument41 pagesLecture No 2 Fundamentals of Financial Markets Interest RateNimco CumarNo ratings yet

- COECA1 - Chapter 3 - Demand and SupplyDocument41 pagesCOECA1 - Chapter 3 - Demand and Supplybanathi nkosiNo ratings yet

- Lecture 6 Behavior of Interest RatesDocument33 pagesLecture 6 Behavior of Interest RatesAman Ullah BalochNo ratings yet

- 6 The Behavior of InterestrateDocument35 pages6 The Behavior of Interestrateyashasvipandey24682No ratings yet

- Chapter 5 Summary - Group 6Document10 pagesChapter 5 Summary - Group 6Phương Anh NguyễnNo ratings yet

- Sale of Government Bonds CB Sells Bonds To The Public and Gets Cash in Return SucksDocument55 pagesSale of Government Bonds CB Sells Bonds To The Public and Gets Cash in Return SucksDora IskandarNo ratings yet

- H#22 Theories of Interest RateDocument3 pagesH#22 Theories of Interest RateMd. Didarul AlamNo ratings yet

- Money, Interest Rates, and Exchange RatesDocument59 pagesMoney, Interest Rates, and Exchange RatesMømë Thãt ŸõûNo ratings yet

- 2 - Money Demand TheoriesDocument8 pages2 - Money Demand Theoriesmajmmallikarachchi.mallikarachchiNo ratings yet

- L 05-Keynessian Viewpoint of Quantity Theory of MoneyDocument8 pagesL 05-Keynessian Viewpoint of Quantity Theory of MoneyNorahNo ratings yet

- Chapter 2Document19 pagesChapter 2ebaaNo ratings yet

- Unit 3 - Monetary EconomicsDocument27 pagesUnit 3 - Monetary EconomicsDanielNo ratings yet

- Money, Interest Rates, and Exchange Rates (Lecture 7)Document8 pagesMoney, Interest Rates, and Exchange Rates (Lecture 7)nihadsamir2002No ratings yet

- City SemIV Regressive Expectation ModelDocument3 pagesCity SemIV Regressive Expectation ModelAmit EshoreNo ratings yet

- Macroeconomics 13th Edition Parkin Solutions ManualDocument35 pagesMacroeconomics 13th Edition Parkin Solutions Manualaraucariabesidesijd835100% (29)

- Financial Market-Lecture 2-2Document23 pagesFinancial Market-Lecture 2-2Krish ShettyNo ratings yet

- Chapter 3 (Unit 1)Document21 pagesChapter 3 (Unit 1)GiriNo ratings yet

- FIM Lecture V VI: Why Do Interest Rates Change?Document15 pagesFIM Lecture V VI: Why Do Interest Rates Change?Aniket GuptaNo ratings yet

- C4-Factors Affecting IRDocument24 pagesC4-Factors Affecting IRDuong Ha ThuyNo ratings yet

- Bond Is A Type of Financial SecurityDocument3 pagesBond Is A Type of Financial Securityjennifer leeNo ratings yet

- Chapter 6: Interest RatesDocument6 pagesChapter 6: Interest RateskafiNo ratings yet

- Chapter26 - Money Demand and Equilibrium Interest RateDocument15 pagesChapter26 - Money Demand and Equilibrium Interest Rateduygualsan1No ratings yet

- Money Demand, The Equilibrium Interest Rate, and Monetary PolicyDocument24 pagesMoney Demand, The Equilibrium Interest Rate, and Monetary PolicyAlmer Faishal WafiNo ratings yet

- Chapter 11 Money Demand and The Equilibrium Interest RateDocument12 pagesChapter 11 Money Demand and The Equilibrium Interest RateWard AlajlouniNo ratings yet

- Interest DefinitionDocument10 pagesInterest Definitionchechi_inNo ratings yet

- Dwnload Full Macroeconomics 13th Edition Parkin Solutions Manual PDFDocument35 pagesDwnload Full Macroeconomics 13th Edition Parkin Solutions Manual PDFelwoodbottifxus100% (12)

- Economics 330 (Kelly) Spring 2001 Answers To Practice Questions #1Document4 pagesEconomics 330 (Kelly) Spring 2001 Answers To Practice Questions #1Phương HàNo ratings yet

- Eco 531 - Chapter 4Document46 pagesEco 531 - Chapter 4Nurul Aina IzzatiNo ratings yet

- Interest RateDocument6 pagesInterest RatesruthipriyamaheshstoryloveNo ratings yet

- Theory of InterestDocument6 pagesTheory of Interestdivyayayadav11No ratings yet

- Avg 64Document1 pageAvg 64JPNo ratings yet

- Trading Game ReportDocument12 pagesTrading Game ReportNguyễn Đường Phương NgọcNo ratings yet

- TAICHINHCONGDocument1 pageTAICHINHCONGNguyễn Đường Phương NgọcNo ratings yet

- 1/ Why Do Banks Exist? DiscussDocument5 pages1/ Why Do Banks Exist? DiscussNguyễn Đường Phương NgọcNo ratings yet

- D. If A Company's Sales Are Growing at A Rate of 20% Annually, How Long Will It Take Sales To Double?Document3 pagesD. If A Company's Sales Are Growing at A Rate of 20% Annually, How Long Will It Take Sales To Double?Nguyễn Đường Phương NgọcNo ratings yet

- Working Capital ManagementDocument92 pagesWorking Capital ManagementJagadish Badi80% (5)

- Banc One Case My SolutionDocument5 pagesBanc One Case My SolutionБорче Шулески67% (3)

- Module 2Document41 pagesModule 2bhargaviNo ratings yet

- ATW September 2016 Investor PresentationDocument15 pagesATW September 2016 Investor PresentationHunterNo ratings yet

- Project RitesDocument72 pagesProject RitesSachin ChadhaNo ratings yet

- Using Financial Accounting Information The Alternative To Debits and Credits 10Th Edition Porter Solutions Manual Full Chapter PDFDocument21 pagesUsing Financial Accounting Information The Alternative To Debits and Credits 10Th Edition Porter Solutions Manual Full Chapter PDFchompdumetoseei5100% (10)

- Financial Statement Analysis - Pantaloon Retail IndiaDocument7 pagesFinancial Statement Analysis - Pantaloon Retail IndiaSupriyaThengdiNo ratings yet

- Laxmi PDFDocument68 pagesLaxmi PDFBharat Singh RathoreNo ratings yet

- Godrej Industries LimitedDocument8 pagesGodrej Industries LimitedJigarNo ratings yet

- Lending Rationale PDFDocument9 pagesLending Rationale PDFNancyNo ratings yet

- Credit Risk Management in BanksDocument19 pagesCredit Risk Management in BanksMahmudur RahmanNo ratings yet

- Tutorial 1: 1. What Is The Basic Functions of Financial Markets?Document6 pagesTutorial 1: 1. What Is The Basic Functions of Financial Markets?Ramsha ShafeelNo ratings yet

- BOJ Financial Sector Update - IMFDocument70 pagesBOJ Financial Sector Update - IMFVenkatesh RamaswamyNo ratings yet

- TestbankDocument33 pagesTestbankBhavneet Sachdeva100% (2)

- Islamic Mortgages in The UK 2020 A Definitive Guide 1Document35 pagesIslamic Mortgages in The UK 2020 A Definitive Guide 1Mahmoud SafaaNo ratings yet

- 16 BibliographyDocument10 pages16 BibliographytouffiqNo ratings yet

- CH 5.palepu - Jw.ca Ratio AnalysisDocument34 pagesCH 5.palepu - Jw.ca Ratio Analysiserza gunawanNo ratings yet

- Effect of Monetary Policy On Real Sector of NepalDocument6 pagesEffect of Monetary Policy On Real Sector of Nepalmr_vishalxpNo ratings yet

- GSE Reform and A Conspiracy of Silence Draft 1.3.1Document11 pagesGSE Reform and A Conspiracy of Silence Draft 1.3.1ny1davidNo ratings yet

- FSA QuestionsDocument1 pageFSA QuestionsNadeemNo ratings yet

- Highway InfrastructureDocument51 pagesHighway InfrastructureBiswarup GhoshNo ratings yet

- Liquidity Cascades - Newfound Research PDFDocument19 pagesLiquidity Cascades - Newfound Research PDFrwmortell3580No ratings yet

- Pestle and Banking IndustryDocument16 pagesPestle and Banking IndustryRegina Leona DeLos SantosNo ratings yet