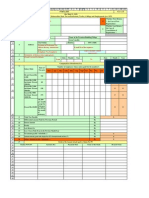

Earn Pay-Outs: Sales Goals Bonus Earnings Goals Bonus

Earn Pay-Outs: Sales Goals Bonus Earnings Goals Bonus

You might also like

- A1.2 Roic TreeDocument9 pagesA1.2 Roic TreemonemNo ratings yet

- MT103 Netkom Solutions LTDDocument2 pagesMT103 Netkom Solutions LTDrasool mehrjoo100% (3)

- ATH Technologies: Case-3 Strategic ImplementationDocument8 pagesATH Technologies: Case-3 Strategic ImplementationSumit RajNo ratings yet

- Group6 - Vyaderm PharmaceuticalsDocument7 pagesGroup6 - Vyaderm PharmaceuticalsVaishak AnilNo ratings yet

- Cloudstrat Case StudyDocument10 pagesCloudstrat Case StudyAbhirami PromodNo ratings yet

- Case Submission-EA DBSTDocument9 pagesCase Submission-EA DBSTUjjwal Bhardwaj100% (1)

- Solutions To Chapters 7 and 8 Problem SetsDocument21 pagesSolutions To Chapters 7 and 8 Problem SetsMuhammad Hasnain100% (1)

- 520 Greenlawn Commercial Questions f12 PDFDocument1 page520 Greenlawn Commercial Questions f12 PDFAshish Kothari0% (2)

- Mayes 8e CH05 SolutionsDocument36 pagesMayes 8e CH05 SolutionsRamez AhmedNo ratings yet

- (Case Study) 2.3.-Knowlton+Roberts+II+ - ADocument8 pages(Case Study) 2.3.-Knowlton+Roberts+II+ - AAyesha AwanNo ratings yet

- Session 9 Case Discussion Immulogic Pharmaceutical CorporationDocument32 pagesSession 9 Case Discussion Immulogic Pharmaceutical CorporationK RameshNo ratings yet

- Macro OB Case QuestionsDocument4 pagesMacro OB Case Questionsrock sinhaNo ratings yet

- Sephora Direct-Hannah Mcarthy 550 - PortfolioDocument6 pagesSephora Direct-Hannah Mcarthy 550 - Portfoliovenom_ftwNo ratings yet

- Immulogic Pharmaceutical CorporationDocument3 pagesImmulogic Pharmaceutical Corporationmiguel50% (2)

- Eastman Kodak CompanyDocument9 pagesEastman Kodak CompanyArveen KaurNo ratings yet

- Form IiibDocument2 pagesForm Iiibvishnucnk25% (4)

- ATH Technologies TemplateDocument2 pagesATH Technologies TemplateamitNo ratings yet

- GE Health Care Case: Executive SummaryDocument4 pagesGE Health Care Case: Executive SummarykpraneethkNo ratings yet

- Answering Questions For GiveIndia Case StudyDocument2 pagesAnswering Questions For GiveIndia Case StudyAryanshi Dubey0% (2)

- CVS CaseDocument4 pagesCVS CaseSayeed AhmadNo ratings yet

- Gilette B Case AssignmentDocument3 pagesGilette B Case AssignmentRajeev NairNo ratings yet

- Case Analysis Landmark FacilityDocument25 pagesCase Analysis Landmark Facilitystark100% (1)

- Exercise 1 SolnDocument2 pagesExercise 1 Solndarinjohson0% (2)

- Shobhit Saxena - CSTR - Assignment IDocument4 pagesShobhit Saxena - CSTR - Assignment IShobhit SaxenaNo ratings yet

- Sec-A - Group 8 - SecureNowDocument7 pagesSec-A - Group 8 - SecureNowPuneet GargNo ratings yet

- Sealed Air Corporation's Leveraged RecapitalizationDocument7 pagesSealed Air Corporation's Leveraged RecapitalizationKumarNo ratings yet

- Performance Management at NIM - Case AnalysisDocument10 pagesPerformance Management at NIM - Case Analysistr07109250% (2)

- 02 The Three Faces of Consumer PromotionsDocument21 pages02 The Three Faces of Consumer PromotionshiteshthaparNo ratings yet

- PGP MAJVCG 2019-20 S3 Unrelated Diversification PDFDocument22 pagesPGP MAJVCG 2019-20 S3 Unrelated Diversification PDFBschool caseNo ratings yet

- Case Study (Midtown Medical Centre)Document3 pagesCase Study (Midtown Medical Centre)Sarmad AminNo ratings yet

- Sealed AirDocument7 pagesSealed AirAnju BabuNo ratings yet

- 08 BrainardCaseAssignmentDocument2 pages08 BrainardCaseAssignmentZainabNo ratings yet

- Q1. How Did The Understanding of Customer Behavior Help With Its Marketing Strategy?Document3 pagesQ1. How Did The Understanding of Customer Behavior Help With Its Marketing Strategy?Pulkit LalwaniNo ratings yet

- Krispy Naturals Case WriteupDocument13 pagesKrispy Naturals Case WriteupVivek Anandan100% (3)

- Gillette Dry IdeaDocument5 pagesGillette Dry IdeaAnirudh PrasadNo ratings yet

- Online Marketing at Big Skinny: Submitted by Group - 6Document2 pagesOnline Marketing at Big Skinny: Submitted by Group - 6Saumadeep GuharayNo ratings yet

- CMA Individual Assignment Manu M EPGPKC06054Document6 pagesCMA Individual Assignment Manu M EPGPKC06054CH NAIRNo ratings yet

- Eye Care System: Case Study On: The Aravind Eye Hospital, India: in Service For SightDocument6 pagesEye Care System: Case Study On: The Aravind Eye Hospital, India: in Service For Sightshruthin100% (1)

- Sealed Air CorporationDocument7 pagesSealed Air CorporationMeenal MalhotraNo ratings yet

- Balanced Scorecard Used in Reliance Life InsuranceDocument6 pagesBalanced Scorecard Used in Reliance Life Insurancemoumitapainibs0% (1)

- Section D - OSD - Group 5Document6 pagesSection D - OSD - Group 5Chidananda PuriNo ratings yet

- 6 Habits of Merely Effective NegotiatorsDocument3 pages6 Habits of Merely Effective NegotiatorsAAMOD KHARB PGP 2018-20 BatchNo ratings yet

- Ingersol RandDocument3 pagesIngersol RandBitan RoyNo ratings yet

- Case Study NordstromDocument2 pagesCase Study Nordstromcavargas11100% (1)

- House of TataDocument36 pagesHouse of TataHarsh Bhardwaj0% (1)

- Good Morning Cereal - Dimensioning Challenge Case 010621Document12 pagesGood Morning Cereal - Dimensioning Challenge Case 010621Tushar SoniNo ratings yet

- MSI Case 1 V.0Document10 pagesMSI Case 1 V.0Dipanjan SenguptaNo ratings yet

- Impairing The Microsoft - Nokia PairingDocument54 pagesImpairing The Microsoft - Nokia Pairingjk kumarNo ratings yet

- Maruti Suzuki Financial Ratios, Dupont AnalysisDocument12 pagesMaruti Suzuki Financial Ratios, Dupont Analysismayankparkhi100% (1)

- Boots Hair Care Sales Promotion Case Study AnalysisDocument11 pagesBoots Hair Care Sales Promotion Case Study Analysispritish chadhaNo ratings yet

- Case 9Document1 pageCase 9Aditya KulashriNo ratings yet

- Age Experience in SF Overall Work Ex Region Positives NegativesDocument6 pagesAge Experience in SF Overall Work Ex Region Positives NegativesireneNo ratings yet

- Bharti Airtel in AfricaDocument3 pagesBharti Airtel in AfricaNishan Shetty100% (1)

- Wrightline Inc. Case Study: Group-6Document6 pagesWrightline Inc. Case Study: Group-6sili coreNo ratings yet

- Samantha Seetaram IENG3003 Assignment1Document15 pagesSamantha Seetaram IENG3003 Assignment1Samantha SeetaramNo ratings yet

- Case Study 2: Sustainability of Ikea GroupDocument3 pagesCase Study 2: Sustainability of Ikea Groupneha reddyNo ratings yet

- Investment Banking: Individual Assignment 2Document5 pagesInvestment Banking: Individual Assignment 2Aakash Ladha100% (3)

- Natureview Farm SolutionsDocument5 pagesNatureview Farm SolutionsRamona ElenaNo ratings yet

- Bunge SA V Nidera BV - Group C - UpDocument9 pagesBunge SA V Nidera BV - Group C - UpPraveen KumarNo ratings yet

- B2BDocument3 pagesB2BHarishNo ratings yet

- ATH Tech Case QuestionsDocument2 pagesATH Tech Case QuestionsSANJAY BHATTACHARYANo ratings yet

- A1.2 Roic TreeDocument9 pagesA1.2 Roic Treesara_AlQuwaifliNo ratings yet

- The Walt Disney CompanyDocument8 pagesThe Walt Disney CompanyUjjwal BhardwajNo ratings yet

- Sugar & Spice: Strategic Position Defensibility Operations Strategy PGPBL02 Term 3 - Group 3Document9 pagesSugar & Spice: Strategic Position Defensibility Operations Strategy PGPBL02 Term 3 - Group 3Ujjwal BhardwajNo ratings yet

- MBM-Precise Case SolutionDocument7 pagesMBM-Precise Case SolutionUjjwal BhardwajNo ratings yet

- MBM Case 2 - Kunst 1600Document4 pagesMBM Case 2 - Kunst 1600Ujjwal BhardwajNo ratings yet

- IndiaMART Solution - MBMDocument4 pagesIndiaMART Solution - MBMUjjwal BhardwajNo ratings yet

- MBM Case 1 - PVTDocument3 pagesMBM Case 1 - PVTUjjwal BhardwajNo ratings yet

- CVS Case - OSDocument11 pagesCVS Case - OSUjjwal Bhardwaj100% (1)

- Kindle Fire: Amazon's Heated Battle For The Tablet Market: DBST: Case# 4Document24 pagesKindle Fire: Amazon's Heated Battle For The Tablet Market: DBST: Case# 4Ujjwal BhardwajNo ratings yet

- Comparative Study Between Private Sector Banks and Public Sector BanksDocument60 pagesComparative Study Between Private Sector Banks and Public Sector BanksAsħîŞĥLøÝå100% (1)

- Mechanics Lien Handout Pitkin County CODocument5 pagesMechanics Lien Handout Pitkin County COanon_166387457No ratings yet

- A Critical Analysis On The Project Appraisal & Management of Project in BangladeshDocument42 pagesA Critical Analysis On The Project Appraisal & Management of Project in Bangladesharcrussel100% (2)

- Flipkart Walmart Deal and Its Affect On EconomyDocument2 pagesFlipkart Walmart Deal and Its Affect On EconomyajNo ratings yet

- Persons Competent To Transfer (S. 7)Document4 pagesPersons Competent To Transfer (S. 7)Saurabh RajNo ratings yet

- Notes From The 2004 Wesco Annual Meeting: May 5, 2004 Pasadena, CA by Whitney TilsonDocument24 pagesNotes From The 2004 Wesco Annual Meeting: May 5, 2004 Pasadena, CA by Whitney Tilsonshadysbr0kenNo ratings yet

- Capital Budgeting QuestionsDocument3 pagesCapital Budgeting QuestionsTAYYABA AMJAD L1F16MBAM0221100% (1)

- What Is Capital Gains Tax On Real EstateDocument51 pagesWhat Is Capital Gains Tax On Real EstatePrateik RyukiNo ratings yet

- PPSC Lecturer Recruitment 2015 Math Mcqs For Lecturer Test 2015Document7 pagesPPSC Lecturer Recruitment 2015 Math Mcqs For Lecturer Test 2015ALI ASGHERNo ratings yet

- Mason Bankruptcy PetitionDocument195 pagesMason Bankruptcy PetitionLansingStateJournalNo ratings yet

- Banking Law NotesDocument8 pagesBanking Law NotesGeetika DhamaNo ratings yet

- 21231IIEDDocument102 pages21231IIEDAmany ElagawyNo ratings yet

- The Following Is Last Month's Contribution Format Income StatementDocument22 pagesThe Following Is Last Month's Contribution Format Income StatementWilliam DC RiveraNo ratings yet

- CH 4.palepu - Jw.caDocument14 pagesCH 4.palepu - Jw.caazizah auliyatusshoffyNo ratings yet

- Chapter 8 Exclusions From Gross IncomeDocument4 pagesChapter 8 Exclusions From Gross IncomeMary Jane PabroaNo ratings yet

- 23.01.10-Vetoquinol PR1 2023 CalendarDocument1 page23.01.10-Vetoquinol PR1 2023 CalendarMayNo ratings yet

- 01.2 - Attached - Agency Action Plan and Status of Implementation 04122016Document8 pages01.2 - Attached - Agency Action Plan and Status of Implementation 04122016Kim Patrick VictoriaNo ratings yet

- Chapter 5: Analysis Financial Statements: Financial Mix RatioDocument22 pagesChapter 5: Analysis Financial Statements: Financial Mix RatioBOSS I4N TVNo ratings yet

- PP Process A Financial Sale Transaction 290812Document42 pagesPP Process A Financial Sale Transaction 290812Richard ZawNo ratings yet

- Hadi Ka DachaDocument55 pagesHadi Ka DachaVijay TendolkarNo ratings yet

- RECELL Repigmentation Underwhelms: Avita Medical (AVH)Document2 pagesRECELL Repigmentation Underwhelms: Avita Medical (AVH)Muhammad ImranNo ratings yet

- Strategic Management Assientment 2013 BMGTDocument7 pagesStrategic Management Assientment 2013 BMGTmulat belaynehNo ratings yet

- Statement of Axis Account No:914010048627688 For The Period (From: 20-12-2020 To: 18-01-2021)Document2 pagesStatement of Axis Account No:914010048627688 For The Period (From: 20-12-2020 To: 18-01-2021)karanNo ratings yet

- Operational PlanDocument3 pagesOperational PlanFaisal Bashir Cheema0% (1)

- SAP Fixed AssetsDocument45 pagesSAP Fixed Assetsrohitmandhania80% (5)

- Chap 13 - ProblemsDocument5 pagesChap 13 - ProblemsBuenaventura, Lara Jane T.No ratings yet

- PGP-IBM Batch 2010-12 With 2011-13 PlacementDocument27 pagesPGP-IBM Batch 2010-12 With 2011-13 Placementsenjaliya11No ratings yet

- Guidelines For BUDGET PreparationDocument8 pagesGuidelines For BUDGET Preparationsheer2_98No ratings yet

Download as pptx, pdf, or txt

You might also like

- A1.2 Roic TreeDocument9 pagesA1.2 Roic TreemonemNo ratings yet

- MT103 Netkom Solutions LTDDocument2 pagesMT103 Netkom Solutions LTDrasool mehrjoo100% (3)

- ATH Technologies: Case-3 Strategic ImplementationDocument8 pagesATH Technologies: Case-3 Strategic ImplementationSumit RajNo ratings yet

- Group6 - Vyaderm PharmaceuticalsDocument7 pagesGroup6 - Vyaderm PharmaceuticalsVaishak AnilNo ratings yet

- Cloudstrat Case StudyDocument10 pagesCloudstrat Case StudyAbhirami PromodNo ratings yet

- Case Submission-EA DBSTDocument9 pagesCase Submission-EA DBSTUjjwal Bhardwaj100% (1)

- Solutions To Chapters 7 and 8 Problem SetsDocument21 pagesSolutions To Chapters 7 and 8 Problem SetsMuhammad Hasnain100% (1)

- 520 Greenlawn Commercial Questions f12 PDFDocument1 page520 Greenlawn Commercial Questions f12 PDFAshish Kothari0% (2)

- Mayes 8e CH05 SolutionsDocument36 pagesMayes 8e CH05 SolutionsRamez AhmedNo ratings yet

- (Case Study) 2.3.-Knowlton+Roberts+II+ - ADocument8 pages(Case Study) 2.3.-Knowlton+Roberts+II+ - AAyesha AwanNo ratings yet

- Session 9 Case Discussion Immulogic Pharmaceutical CorporationDocument32 pagesSession 9 Case Discussion Immulogic Pharmaceutical CorporationK RameshNo ratings yet

- Macro OB Case QuestionsDocument4 pagesMacro OB Case Questionsrock sinhaNo ratings yet

- Sephora Direct-Hannah Mcarthy 550 - PortfolioDocument6 pagesSephora Direct-Hannah Mcarthy 550 - Portfoliovenom_ftwNo ratings yet

- Immulogic Pharmaceutical CorporationDocument3 pagesImmulogic Pharmaceutical Corporationmiguel50% (2)

- Eastman Kodak CompanyDocument9 pagesEastman Kodak CompanyArveen KaurNo ratings yet

- Form IiibDocument2 pagesForm Iiibvishnucnk25% (4)

- ATH Technologies TemplateDocument2 pagesATH Technologies TemplateamitNo ratings yet

- GE Health Care Case: Executive SummaryDocument4 pagesGE Health Care Case: Executive SummarykpraneethkNo ratings yet

- Answering Questions For GiveIndia Case StudyDocument2 pagesAnswering Questions For GiveIndia Case StudyAryanshi Dubey0% (2)

- CVS CaseDocument4 pagesCVS CaseSayeed AhmadNo ratings yet

- Gilette B Case AssignmentDocument3 pagesGilette B Case AssignmentRajeev NairNo ratings yet

- Case Analysis Landmark FacilityDocument25 pagesCase Analysis Landmark Facilitystark100% (1)

- Exercise 1 SolnDocument2 pagesExercise 1 Solndarinjohson0% (2)

- Shobhit Saxena - CSTR - Assignment IDocument4 pagesShobhit Saxena - CSTR - Assignment IShobhit SaxenaNo ratings yet

- Sec-A - Group 8 - SecureNowDocument7 pagesSec-A - Group 8 - SecureNowPuneet GargNo ratings yet

- Sealed Air Corporation's Leveraged RecapitalizationDocument7 pagesSealed Air Corporation's Leveraged RecapitalizationKumarNo ratings yet

- Performance Management at NIM - Case AnalysisDocument10 pagesPerformance Management at NIM - Case Analysistr07109250% (2)

- 02 The Three Faces of Consumer PromotionsDocument21 pages02 The Three Faces of Consumer PromotionshiteshthaparNo ratings yet

- PGP MAJVCG 2019-20 S3 Unrelated Diversification PDFDocument22 pagesPGP MAJVCG 2019-20 S3 Unrelated Diversification PDFBschool caseNo ratings yet

- Case Study (Midtown Medical Centre)Document3 pagesCase Study (Midtown Medical Centre)Sarmad AminNo ratings yet

- Sealed AirDocument7 pagesSealed AirAnju BabuNo ratings yet

- 08 BrainardCaseAssignmentDocument2 pages08 BrainardCaseAssignmentZainabNo ratings yet

- Q1. How Did The Understanding of Customer Behavior Help With Its Marketing Strategy?Document3 pagesQ1. How Did The Understanding of Customer Behavior Help With Its Marketing Strategy?Pulkit LalwaniNo ratings yet

- Krispy Naturals Case WriteupDocument13 pagesKrispy Naturals Case WriteupVivek Anandan100% (3)

- Gillette Dry IdeaDocument5 pagesGillette Dry IdeaAnirudh PrasadNo ratings yet

- Online Marketing at Big Skinny: Submitted by Group - 6Document2 pagesOnline Marketing at Big Skinny: Submitted by Group - 6Saumadeep GuharayNo ratings yet

- CMA Individual Assignment Manu M EPGPKC06054Document6 pagesCMA Individual Assignment Manu M EPGPKC06054CH NAIRNo ratings yet

- Eye Care System: Case Study On: The Aravind Eye Hospital, India: in Service For SightDocument6 pagesEye Care System: Case Study On: The Aravind Eye Hospital, India: in Service For Sightshruthin100% (1)

- Sealed Air CorporationDocument7 pagesSealed Air CorporationMeenal MalhotraNo ratings yet

- Balanced Scorecard Used in Reliance Life InsuranceDocument6 pagesBalanced Scorecard Used in Reliance Life Insurancemoumitapainibs0% (1)

- Section D - OSD - Group 5Document6 pagesSection D - OSD - Group 5Chidananda PuriNo ratings yet

- 6 Habits of Merely Effective NegotiatorsDocument3 pages6 Habits of Merely Effective NegotiatorsAAMOD KHARB PGP 2018-20 BatchNo ratings yet

- Ingersol RandDocument3 pagesIngersol RandBitan RoyNo ratings yet

- Case Study NordstromDocument2 pagesCase Study Nordstromcavargas11100% (1)

- House of TataDocument36 pagesHouse of TataHarsh Bhardwaj0% (1)

- Good Morning Cereal - Dimensioning Challenge Case 010621Document12 pagesGood Morning Cereal - Dimensioning Challenge Case 010621Tushar SoniNo ratings yet

- MSI Case 1 V.0Document10 pagesMSI Case 1 V.0Dipanjan SenguptaNo ratings yet

- Impairing The Microsoft - Nokia PairingDocument54 pagesImpairing The Microsoft - Nokia Pairingjk kumarNo ratings yet

- Maruti Suzuki Financial Ratios, Dupont AnalysisDocument12 pagesMaruti Suzuki Financial Ratios, Dupont Analysismayankparkhi100% (1)

- Boots Hair Care Sales Promotion Case Study AnalysisDocument11 pagesBoots Hair Care Sales Promotion Case Study Analysispritish chadhaNo ratings yet

- Case 9Document1 pageCase 9Aditya KulashriNo ratings yet

- Age Experience in SF Overall Work Ex Region Positives NegativesDocument6 pagesAge Experience in SF Overall Work Ex Region Positives NegativesireneNo ratings yet

- Bharti Airtel in AfricaDocument3 pagesBharti Airtel in AfricaNishan Shetty100% (1)

- Wrightline Inc. Case Study: Group-6Document6 pagesWrightline Inc. Case Study: Group-6sili coreNo ratings yet

- Samantha Seetaram IENG3003 Assignment1Document15 pagesSamantha Seetaram IENG3003 Assignment1Samantha SeetaramNo ratings yet

- Case Study 2: Sustainability of Ikea GroupDocument3 pagesCase Study 2: Sustainability of Ikea Groupneha reddyNo ratings yet

- Investment Banking: Individual Assignment 2Document5 pagesInvestment Banking: Individual Assignment 2Aakash Ladha100% (3)

- Natureview Farm SolutionsDocument5 pagesNatureview Farm SolutionsRamona ElenaNo ratings yet

- Bunge SA V Nidera BV - Group C - UpDocument9 pagesBunge SA V Nidera BV - Group C - UpPraveen KumarNo ratings yet

- B2BDocument3 pagesB2BHarishNo ratings yet

- ATH Tech Case QuestionsDocument2 pagesATH Tech Case QuestionsSANJAY BHATTACHARYANo ratings yet

- A1.2 Roic TreeDocument9 pagesA1.2 Roic Treesara_AlQuwaifliNo ratings yet

- The Walt Disney CompanyDocument8 pagesThe Walt Disney CompanyUjjwal BhardwajNo ratings yet

- Sugar & Spice: Strategic Position Defensibility Operations Strategy PGPBL02 Term 3 - Group 3Document9 pagesSugar & Spice: Strategic Position Defensibility Operations Strategy PGPBL02 Term 3 - Group 3Ujjwal BhardwajNo ratings yet

- MBM-Precise Case SolutionDocument7 pagesMBM-Precise Case SolutionUjjwal BhardwajNo ratings yet

- MBM Case 2 - Kunst 1600Document4 pagesMBM Case 2 - Kunst 1600Ujjwal BhardwajNo ratings yet

- IndiaMART Solution - MBMDocument4 pagesIndiaMART Solution - MBMUjjwal BhardwajNo ratings yet

- MBM Case 1 - PVTDocument3 pagesMBM Case 1 - PVTUjjwal BhardwajNo ratings yet

- CVS Case - OSDocument11 pagesCVS Case - OSUjjwal Bhardwaj100% (1)

- Kindle Fire: Amazon's Heated Battle For The Tablet Market: DBST: Case# 4Document24 pagesKindle Fire: Amazon's Heated Battle For The Tablet Market: DBST: Case# 4Ujjwal BhardwajNo ratings yet

- Comparative Study Between Private Sector Banks and Public Sector BanksDocument60 pagesComparative Study Between Private Sector Banks and Public Sector BanksAsħîŞĥLøÝå100% (1)

- Mechanics Lien Handout Pitkin County CODocument5 pagesMechanics Lien Handout Pitkin County COanon_166387457No ratings yet

- A Critical Analysis On The Project Appraisal & Management of Project in BangladeshDocument42 pagesA Critical Analysis On The Project Appraisal & Management of Project in Bangladesharcrussel100% (2)

- Flipkart Walmart Deal and Its Affect On EconomyDocument2 pagesFlipkart Walmart Deal and Its Affect On EconomyajNo ratings yet

- Persons Competent To Transfer (S. 7)Document4 pagesPersons Competent To Transfer (S. 7)Saurabh RajNo ratings yet

- Notes From The 2004 Wesco Annual Meeting: May 5, 2004 Pasadena, CA by Whitney TilsonDocument24 pagesNotes From The 2004 Wesco Annual Meeting: May 5, 2004 Pasadena, CA by Whitney Tilsonshadysbr0kenNo ratings yet

- Capital Budgeting QuestionsDocument3 pagesCapital Budgeting QuestionsTAYYABA AMJAD L1F16MBAM0221100% (1)

- What Is Capital Gains Tax On Real EstateDocument51 pagesWhat Is Capital Gains Tax On Real EstatePrateik RyukiNo ratings yet

- PPSC Lecturer Recruitment 2015 Math Mcqs For Lecturer Test 2015Document7 pagesPPSC Lecturer Recruitment 2015 Math Mcqs For Lecturer Test 2015ALI ASGHERNo ratings yet

- Mason Bankruptcy PetitionDocument195 pagesMason Bankruptcy PetitionLansingStateJournalNo ratings yet

- Banking Law NotesDocument8 pagesBanking Law NotesGeetika DhamaNo ratings yet

- 21231IIEDDocument102 pages21231IIEDAmany ElagawyNo ratings yet

- The Following Is Last Month's Contribution Format Income StatementDocument22 pagesThe Following Is Last Month's Contribution Format Income StatementWilliam DC RiveraNo ratings yet

- CH 4.palepu - Jw.caDocument14 pagesCH 4.palepu - Jw.caazizah auliyatusshoffyNo ratings yet

- Chapter 8 Exclusions From Gross IncomeDocument4 pagesChapter 8 Exclusions From Gross IncomeMary Jane PabroaNo ratings yet

- 23.01.10-Vetoquinol PR1 2023 CalendarDocument1 page23.01.10-Vetoquinol PR1 2023 CalendarMayNo ratings yet

- 01.2 - Attached - Agency Action Plan and Status of Implementation 04122016Document8 pages01.2 - Attached - Agency Action Plan and Status of Implementation 04122016Kim Patrick VictoriaNo ratings yet

- Chapter 5: Analysis Financial Statements: Financial Mix RatioDocument22 pagesChapter 5: Analysis Financial Statements: Financial Mix RatioBOSS I4N TVNo ratings yet

- PP Process A Financial Sale Transaction 290812Document42 pagesPP Process A Financial Sale Transaction 290812Richard ZawNo ratings yet

- Hadi Ka DachaDocument55 pagesHadi Ka DachaVijay TendolkarNo ratings yet

- RECELL Repigmentation Underwhelms: Avita Medical (AVH)Document2 pagesRECELL Repigmentation Underwhelms: Avita Medical (AVH)Muhammad ImranNo ratings yet

- Strategic Management Assientment 2013 BMGTDocument7 pagesStrategic Management Assientment 2013 BMGTmulat belaynehNo ratings yet

- Statement of Axis Account No:914010048627688 For The Period (From: 20-12-2020 To: 18-01-2021)Document2 pagesStatement of Axis Account No:914010048627688 For The Period (From: 20-12-2020 To: 18-01-2021)karanNo ratings yet

- Operational PlanDocument3 pagesOperational PlanFaisal Bashir Cheema0% (1)

- SAP Fixed AssetsDocument45 pagesSAP Fixed Assetsrohitmandhania80% (5)

- Chap 13 - ProblemsDocument5 pagesChap 13 - ProblemsBuenaventura, Lara Jane T.No ratings yet

- PGP-IBM Batch 2010-12 With 2011-13 PlacementDocument27 pagesPGP-IBM Batch 2010-12 With 2011-13 Placementsenjaliya11No ratings yet

- Guidelines For BUDGET PreparationDocument8 pagesGuidelines For BUDGET Preparationsheer2_98No ratings yet