NPS

NPS

You might also like

- Land of Snow WorksheetDocument7 pagesLand of Snow WorksheetSatish Bhadani83% (12)

- Comptroller & Auditor General's Manual of Standing Orders (Audit)Document53 pagesComptroller & Auditor General's Manual of Standing Orders (Audit)Ashutosh Anil Vishnoi100% (1)

- Arrear Demand Write OffDocument45 pagesArrear Demand Write OffSatish Bhadani100% (1)

- CCS-Pension-Rules 2021-EnglishDocument111 pagesCCS-Pension-Rules 2021-EnglishRohit Mishra100% (1)

- 9.man The Living MachineDocument11 pages9.man The Living MachineSatish Bhadani100% (1)

- 56SAM - Swift MT103 - 202 DOA GM INTERTRADEDocument22 pages56SAM - Swift MT103 - 202 DOA GM INTERTRADEPink AppleNo ratings yet

- National Pension Scheme (NPS) Guidelines FY 2019-20Document21 pagesNational Pension Scheme (NPS) Guidelines FY 2019-20harrishNo ratings yet

- Nps Note and MCQDocument37 pagesNps Note and MCQRSMENNo ratings yet

- The General Provident Fund (Central Service) Rules, 1960Document40 pagesThe General Provident Fund (Central Service) Rules, 1960Maddela Ravi kumarNo ratings yet

- MACP SchemeDocument15 pagesMACP SchemevkjajoriaNo ratings yet

- National Pension System FAQs GeneralDocument8 pagesNational Pension System FAQs GeneralvrknraoNo ratings yet

- Ta RulesDocument25 pagesTa RulesMohit JoonNo ratings yet

- CCS Conduct RulesDocument33 pagesCCS Conduct RulesnnreddiNo ratings yet

- "Joining Time": A. Cases in Which Joining Time Is AdmissibleDocument24 pages"Joining Time": A. Cases in Which Joining Time Is Admissiblesanu edacheriNo ratings yet

- LTC PDFDocument11 pagesLTC PDFMagesssNo ratings yet

- CCS (Conduct) Rules - Session 4.1 & 4.2Document26 pagesCCS (Conduct) Rules - Session 4.1 & 4.2pgtenglishNo ratings yet

- New Incentive PLI RPLI Structure 07.04.23Document7 pagesNew Incentive PLI RPLI Structure 07.04.23duvaNo ratings yet

- LTC RulesDocument30 pagesLTC RulesmeetsatyajeeNo ratings yet

- On GFRDocument23 pagesOn GFRSuvadip PalNo ratings yet

- DPC Guidelines PDFDocument5 pagesDPC Guidelines PDFAmit KumarNo ratings yet

- Procurement of Goods & Services Through Government E-Marketplace (GeM) - Central Government Employees NewsDocument2 pagesProcurement of Goods & Services Through Government E-Marketplace (GeM) - Central Government Employees NewsbimlapalNo ratings yet

- CCS Conduct - 1964Document7 pagesCCS Conduct - 1964suresh sureshNo ratings yet

- F.R - Pay Fixarions-IiDocument38 pagesF.R - Pay Fixarions-IimurapakasrinivasNo ratings yet

- Goods and Service Contracts Through Government E-Marketplace (Gem)Document24 pagesGoods and Service Contracts Through Government E-Marketplace (Gem)Ranjeet SinghNo ratings yet

- CCS (Leave) RulesDocument53 pagesCCS (Leave) Rulespoojasikka196380% (5)

- GPF (General Provident Fund) Rules, 1960 and Contributory Provident FundDocument9 pagesGPF (General Provident Fund) Rules, 1960 and Contributory Provident FundFinance AdministrationNo ratings yet

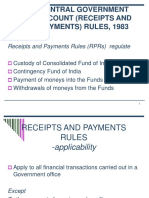

- Central Government Account (Receipts and Payments) Rules, 1983Document21 pagesCentral Government Account (Receipts and Payments) Rules, 1983Deepak Kumar PandaNo ratings yet

- Travelling AllowanceDocument12 pagesTravelling AllowanceManoj SharmaNo ratings yet

- Delegation of Financial Power RULES, 1978Document42 pagesDelegation of Financial Power RULES, 1978Manoj Kumar SainiNo ratings yet

- New Pension Scheme in Comparison To Old Pension SchemeDocument29 pagesNew Pension Scheme in Comparison To Old Pension SchemenavtejpvsNo ratings yet

- LTC RulesDocument33 pagesLTC RulesExam Preparation Coaching ClassesNo ratings yet

- LTC RulesDocument34 pagesLTC Rulessunilhanda33_4382901No ratings yet

- CCS (Pensions Rule) 2021 BookDocument234 pagesCCS (Pensions Rule) 2021 BookSIDDHARTH DATTA100% (1)

- DWP 2020Document30 pagesDWP 2020ravisingh85No ratings yet

- Swaminathan PublicationDocument4 pagesSwaminathan PublicationRishabh DevNo ratings yet

- Kisan Vikas Patra Scheme: Prepared By: Jagdish Chosala Instructor, PTC VadodaraDocument9 pagesKisan Vikas Patra Scheme: Prepared By: Jagdish Chosala Instructor, PTC Vadodarabhanupalavarapu100% (1)

- DFPR1978 PDFDocument76 pagesDFPR1978 PDFricki2010No ratings yet

- Leave RulesDocument10 pagesLeave Rulesdinesh005No ratings yet

- Module On Pay Fixation 1Document14 pagesModule On Pay Fixation 1Adepu Venkata Ramana50% (2)

- CCS (Conduct) Rules, 1964 - From Website of DoPT As On 07.01.2019Document185 pagesCCS (Conduct) Rules, 1964 - From Website of DoPT As On 07.01.2019अजय चौधरी100% (1)

- General Provident Fund Rules PDFDocument65 pagesGeneral Provident Fund Rules PDFMuhammad ImranNo ratings yet

- MACPS (Modified Oct. 2012)Document86 pagesMACPS (Modified Oct. 2012)Aparajita GhoshNo ratings yet

- CCS (Pension) Rules, 1972Document28 pagesCCS (Pension) Rules, 1972saritaNo ratings yet

- Commutation of Pension - Some Question and Answers On Retirement Benefits - Pensioners PortalDocument3 pagesCommutation of Pension - Some Question and Answers On Retirement Benefits - Pensioners PortalTvs ReddyNo ratings yet

- DFPRDocument10 pagesDFPRVish indianNo ratings yet

- "Joining Time": A. Cases in Which Joining Time Is AdmissibleDocument24 pages"Joining Time": A. Cases in Which Joining Time Is Admissiblevijaygarge59100% (1)

- KSR 3Document9 pagesKSR 3abhivnairNo ratings yet

- Ccs Cca Rules 1965Document18 pagesCcs Cca Rules 1965himanshuNo ratings yet

- CCS (Cca) - FaqDocument71 pagesCCS (Cca) - FaqHarshDivakarNo ratings yet

- Mnop 220412Document22 pagesMnop 220412ajoy2barNo ratings yet

- Fundamental RulesDocument41 pagesFundamental Rulesmrraee4729No ratings yet

- India - Fundamental RulesDocument15 pagesIndia - Fundamental RulesKyaw Zin Htet100% (2)

- Chapter 08 Revised Maintenance - of - Service - BooksDocument14 pagesChapter 08 Revised Maintenance - of - Service - BooksSrigouri ChigateriNo ratings yet

- Workshop On Defence Procurement Manual 2009wksp2-AnjulaDocument42 pagesWorkshop On Defence Procurement Manual 2009wksp2-Anjulaersachinpachori0% (1)

- 06 Temp Service 21-AppendixDocument3 pages06 Temp Service 21-Appendixnew besesdNo ratings yet

- Swamys Manual On Office Procedure For Central Government Offices PDFDocument5 pagesSwamys Manual On Office Procedure For Central Government Offices PDFSureshJeevan0% (2)

- NPS PPT - HDFC BankDocument17 pagesNPS PPT - HDFC BankPankaj Kothari100% (1)

- National Pension System For Corporates - PresentationDocument10 pagesNational Pension System For Corporates - PresentationSudeep KulkarniNo ratings yet

- NPS-HDFC-Frequently Asked QuestionsDocument7 pagesNPS-HDFC-Frequently Asked QuestionsSudip MukhopadhyayNo ratings yet

- Post Office Surjit PDFDocument7 pagesPost Office Surjit PDFPawan SharmaNo ratings yet

- FAQ NPS-Corp ModelDocument13 pagesFAQ NPS-Corp Modeljamjam75No ratings yet

- The New National Pension SchemeDocument2 pagesThe New National Pension Schemegurudev001No ratings yet

- New Pension Scheme UpdatedDocument5 pagesNew Pension Scheme UpdatedBhawnaSharmaNo ratings yet

- Direct Tax Code: Capital Gains Tax On Sale of Residential PropertyDocument5 pagesDirect Tax Code: Capital Gains Tax On Sale of Residential Propertykarthikeyan.mohandossNo ratings yet

- Penalty and ProsecutionsDocument50 pagesPenalty and ProsecutionsSatish BhadaniNo ratings yet

- Income Tax Authority: Chapter-Xiii (Section 116 To 138)Document46 pagesIncome Tax Authority: Chapter-Xiii (Section 116 To 138)Satish BhadaniNo ratings yet

- Civics Class VIII - Chapter-3Document24 pagesCivics Class VIII - Chapter-3Satish BhadaniNo ratings yet

- Civics Class VIII - Chapter-1Document30 pagesCivics Class VIII - Chapter-1Satish BhadaniNo ratings yet

- AppealDocument28 pagesAppealSatish BhadaniNo ratings yet

- Income From Other SourcesDocument29 pagesIncome From Other SourcesSatish BhadaniNo ratings yet

- Female Foeticide and Child LabourDocument9 pagesFemale Foeticide and Child LabourSatish BhadaniNo ratings yet

- Court Fees Act, 1870.Document18 pagesCourt Fees Act, 1870.Satish BhadaniNo ratings yet

- 12.weather WorksheetDocument10 pages12.weather WorksheetSatish BhadaniNo ratings yet

- 13.pollution WorksheetDocument7 pages13.pollution WorksheetSatish BhadaniNo ratings yet

- 3.saftey 1. Fill in The BlanksDocument6 pages3.saftey 1. Fill in The BlanksSatish BhadaniNo ratings yet

- 11.light Sound and ForceDocument7 pages11.light Sound and ForceSatish Bhadani100% (1)

- 14.our Earth and Its NeighboursDocument8 pages14.our Earth and Its NeighboursSatish BhadaniNo ratings yet

- Birds-Food and MoreDocument7 pagesBirds-Food and MoreSatish BhadaniNo ratings yet

- Living and Non-Living ThingsDocument7 pagesLiving and Non-Living ThingsSatish BhadaniNo ratings yet

- Revocations Irc 501c3 Determinations 01292021Document40 pagesRevocations Irc 501c3 Determinations 01292021Bertha McGalliard PenceNo ratings yet

- This Study Resource Was: Quiz On Receivable FinancingDocument3 pagesThis Study Resource Was: Quiz On Receivable FinancingKez MaxNo ratings yet

- Modified Pag-Ibig Ii Enrollment FormDocument2 pagesModified Pag-Ibig Ii Enrollment FormJazziel Fortaliza100% (1)

- New Swot RetailDocument11 pagesNew Swot RetailijustyadavNo ratings yet

- Promo Mechs - 2022 McDo NUP MSMT FINALDocument14 pagesPromo Mechs - 2022 McDo NUP MSMT FINALFrank PasuntingNo ratings yet

- Jio Invoice 290323Document2 pagesJio Invoice 290323Deepak KiniNo ratings yet

- Eighteenth Edition, Global Edition: Customer Value-Driven Marketing Strategy: Creating Value For Target CustomersDocument41 pagesEighteenth Edition, Global Edition: Customer Value-Driven Marketing Strategy: Creating Value For Target CustomersIrene Elfrida SNo ratings yet

- Back-to-Back Letters of CreditDocument12 pagesBack-to-Back Letters of CreditSudershan ThaibaNo ratings yet

- Gauhati University - Exam Form Payment Receipt PDFDocument2 pagesGauhati University - Exam Form Payment Receipt PDFMuktadur RahmanNo ratings yet

- Cost Concepts and ClassificationsDocument6 pagesCost Concepts and ClassificationsNailiah MacakilingNo ratings yet

- 1701Q Quarterly Income Tax Return: For Individuals, Estates and TrustsDocument1 page1701Q Quarterly Income Tax Return: For Individuals, Estates and TrustsAshly MateoNo ratings yet

- YES Bank Annual Report 2014-15Document4 pagesYES Bank Annual Report 2014-15Nalini ChunchuNo ratings yet

- Financial Management For EntrepreneursDocument40 pagesFinancial Management For EntrepreneursHerald TheHorrorNo ratings yet

- 26.recent Changes in BankingDocument2 pages26.recent Changes in BankingVIKASH ARYANNo ratings yet

- Zomato LTD.: Investing Key To Compounding Long Term GrowthDocument5 pagesZomato LTD.: Investing Key To Compounding Long Term GrowthAvinash GollaNo ratings yet

- Cash To Accrual Basis of AccountingDocument6 pagesCash To Accrual Basis of AccountingChocobetternotNo ratings yet

- Registration Kenya Print Pack Sign Expo 19-21 Jan 2021Document4 pagesRegistration Kenya Print Pack Sign Expo 19-21 Jan 2021MAYANK CHHATWALNo ratings yet

- Advertising MCQDocument14 pagesAdvertising MCQArti Srivastava100% (1)

- Personal Finance 4th Edition Madura Test BankDocument18 pagesPersonal Finance 4th Edition Madura Test Bankkhuyenfrederickgjk8100% (29)

- Journal, T Accounts, WorksheetDocument10 pagesJournal, T Accounts, Worksheetkenneth coronelNo ratings yet

- Hybrid Approach To Corporate Sustainability Performance in Indonesia's Cement IndustryDocument21 pagesHybrid Approach To Corporate Sustainability Performance in Indonesia's Cement IndustryazzahraNo ratings yet

- Receivable Financing Sample ProblemDocument3 pagesReceivable Financing Sample ProblemKathleen FrondozoNo ratings yet

- Target Cost AnswersDocument6 pagesTarget Cost Answerspaul sagudaNo ratings yet

- Chapter 2 - Standardisation and Food Food LegislationDocument49 pagesChapter 2 - Standardisation and Food Food LegislationLam Thoại NguyễnNo ratings yet

- Chapter 3 Consumer MathematicsDocument36 pagesChapter 3 Consumer MathematicsHazmin NawiNo ratings yet

- ECONOMICSDocument2 pagesECONOMICSSuzui MasudaNo ratings yet

- IndianMiningLaws MMDRAct1957SubsequentAmendmentsDocument24 pagesIndianMiningLaws MMDRAct1957SubsequentAmendmentsSwiggly PandaNo ratings yet

- The Impact of Customer Services On Customer Satisfaction in The Food Industry: A Case Study of Mcdonald'SDocument15 pagesThe Impact of Customer Services On Customer Satisfaction in The Food Industry: A Case Study of Mcdonald'SMofy AllyNo ratings yet

- Chapter 6 - AnswersDocument22 pagesChapter 6 - Answersviva nazarenoNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Land of Snow WorksheetDocument7 pagesLand of Snow WorksheetSatish Bhadani83% (12)

- Comptroller & Auditor General's Manual of Standing Orders (Audit)Document53 pagesComptroller & Auditor General's Manual of Standing Orders (Audit)Ashutosh Anil Vishnoi100% (1)

- Arrear Demand Write OffDocument45 pagesArrear Demand Write OffSatish Bhadani100% (1)

- CCS-Pension-Rules 2021-EnglishDocument111 pagesCCS-Pension-Rules 2021-EnglishRohit Mishra100% (1)

- 9.man The Living MachineDocument11 pages9.man The Living MachineSatish Bhadani100% (1)

- 56SAM - Swift MT103 - 202 DOA GM INTERTRADEDocument22 pages56SAM - Swift MT103 - 202 DOA GM INTERTRADEPink AppleNo ratings yet

- National Pension Scheme (NPS) Guidelines FY 2019-20Document21 pagesNational Pension Scheme (NPS) Guidelines FY 2019-20harrishNo ratings yet

- Nps Note and MCQDocument37 pagesNps Note and MCQRSMENNo ratings yet

- The General Provident Fund (Central Service) Rules, 1960Document40 pagesThe General Provident Fund (Central Service) Rules, 1960Maddela Ravi kumarNo ratings yet

- MACP SchemeDocument15 pagesMACP SchemevkjajoriaNo ratings yet

- National Pension System FAQs GeneralDocument8 pagesNational Pension System FAQs GeneralvrknraoNo ratings yet

- Ta RulesDocument25 pagesTa RulesMohit JoonNo ratings yet

- CCS Conduct RulesDocument33 pagesCCS Conduct RulesnnreddiNo ratings yet

- "Joining Time": A. Cases in Which Joining Time Is AdmissibleDocument24 pages"Joining Time": A. Cases in Which Joining Time Is Admissiblesanu edacheriNo ratings yet

- LTC PDFDocument11 pagesLTC PDFMagesssNo ratings yet

- CCS (Conduct) Rules - Session 4.1 & 4.2Document26 pagesCCS (Conduct) Rules - Session 4.1 & 4.2pgtenglishNo ratings yet

- New Incentive PLI RPLI Structure 07.04.23Document7 pagesNew Incentive PLI RPLI Structure 07.04.23duvaNo ratings yet

- LTC RulesDocument30 pagesLTC RulesmeetsatyajeeNo ratings yet

- On GFRDocument23 pagesOn GFRSuvadip PalNo ratings yet

- DPC Guidelines PDFDocument5 pagesDPC Guidelines PDFAmit KumarNo ratings yet

- Procurement of Goods & Services Through Government E-Marketplace (GeM) - Central Government Employees NewsDocument2 pagesProcurement of Goods & Services Through Government E-Marketplace (GeM) - Central Government Employees NewsbimlapalNo ratings yet

- CCS Conduct - 1964Document7 pagesCCS Conduct - 1964suresh sureshNo ratings yet

- F.R - Pay Fixarions-IiDocument38 pagesF.R - Pay Fixarions-IimurapakasrinivasNo ratings yet

- Goods and Service Contracts Through Government E-Marketplace (Gem)Document24 pagesGoods and Service Contracts Through Government E-Marketplace (Gem)Ranjeet SinghNo ratings yet

- CCS (Leave) RulesDocument53 pagesCCS (Leave) Rulespoojasikka196380% (5)

- GPF (General Provident Fund) Rules, 1960 and Contributory Provident FundDocument9 pagesGPF (General Provident Fund) Rules, 1960 and Contributory Provident FundFinance AdministrationNo ratings yet

- Central Government Account (Receipts and Payments) Rules, 1983Document21 pagesCentral Government Account (Receipts and Payments) Rules, 1983Deepak Kumar PandaNo ratings yet

- Travelling AllowanceDocument12 pagesTravelling AllowanceManoj SharmaNo ratings yet

- Delegation of Financial Power RULES, 1978Document42 pagesDelegation of Financial Power RULES, 1978Manoj Kumar SainiNo ratings yet

- New Pension Scheme in Comparison To Old Pension SchemeDocument29 pagesNew Pension Scheme in Comparison To Old Pension SchemenavtejpvsNo ratings yet

- LTC RulesDocument33 pagesLTC RulesExam Preparation Coaching ClassesNo ratings yet

- LTC RulesDocument34 pagesLTC Rulessunilhanda33_4382901No ratings yet

- CCS (Pensions Rule) 2021 BookDocument234 pagesCCS (Pensions Rule) 2021 BookSIDDHARTH DATTA100% (1)

- DWP 2020Document30 pagesDWP 2020ravisingh85No ratings yet

- Swaminathan PublicationDocument4 pagesSwaminathan PublicationRishabh DevNo ratings yet

- Kisan Vikas Patra Scheme: Prepared By: Jagdish Chosala Instructor, PTC VadodaraDocument9 pagesKisan Vikas Patra Scheme: Prepared By: Jagdish Chosala Instructor, PTC Vadodarabhanupalavarapu100% (1)

- DFPR1978 PDFDocument76 pagesDFPR1978 PDFricki2010No ratings yet

- Leave RulesDocument10 pagesLeave Rulesdinesh005No ratings yet

- Module On Pay Fixation 1Document14 pagesModule On Pay Fixation 1Adepu Venkata Ramana50% (2)

- CCS (Conduct) Rules, 1964 - From Website of DoPT As On 07.01.2019Document185 pagesCCS (Conduct) Rules, 1964 - From Website of DoPT As On 07.01.2019अजय चौधरी100% (1)

- General Provident Fund Rules PDFDocument65 pagesGeneral Provident Fund Rules PDFMuhammad ImranNo ratings yet

- MACPS (Modified Oct. 2012)Document86 pagesMACPS (Modified Oct. 2012)Aparajita GhoshNo ratings yet

- CCS (Pension) Rules, 1972Document28 pagesCCS (Pension) Rules, 1972saritaNo ratings yet

- Commutation of Pension - Some Question and Answers On Retirement Benefits - Pensioners PortalDocument3 pagesCommutation of Pension - Some Question and Answers On Retirement Benefits - Pensioners PortalTvs ReddyNo ratings yet

- DFPRDocument10 pagesDFPRVish indianNo ratings yet

- "Joining Time": A. Cases in Which Joining Time Is AdmissibleDocument24 pages"Joining Time": A. Cases in Which Joining Time Is Admissiblevijaygarge59100% (1)

- KSR 3Document9 pagesKSR 3abhivnairNo ratings yet

- Ccs Cca Rules 1965Document18 pagesCcs Cca Rules 1965himanshuNo ratings yet

- CCS (Cca) - FaqDocument71 pagesCCS (Cca) - FaqHarshDivakarNo ratings yet

- Mnop 220412Document22 pagesMnop 220412ajoy2barNo ratings yet

- Fundamental RulesDocument41 pagesFundamental Rulesmrraee4729No ratings yet

- India - Fundamental RulesDocument15 pagesIndia - Fundamental RulesKyaw Zin Htet100% (2)

- Chapter 08 Revised Maintenance - of - Service - BooksDocument14 pagesChapter 08 Revised Maintenance - of - Service - BooksSrigouri ChigateriNo ratings yet

- Workshop On Defence Procurement Manual 2009wksp2-AnjulaDocument42 pagesWorkshop On Defence Procurement Manual 2009wksp2-Anjulaersachinpachori0% (1)

- 06 Temp Service 21-AppendixDocument3 pages06 Temp Service 21-Appendixnew besesdNo ratings yet

- Swamys Manual On Office Procedure For Central Government Offices PDFDocument5 pagesSwamys Manual On Office Procedure For Central Government Offices PDFSureshJeevan0% (2)

- NPS PPT - HDFC BankDocument17 pagesNPS PPT - HDFC BankPankaj Kothari100% (1)

- National Pension System For Corporates - PresentationDocument10 pagesNational Pension System For Corporates - PresentationSudeep KulkarniNo ratings yet

- NPS-HDFC-Frequently Asked QuestionsDocument7 pagesNPS-HDFC-Frequently Asked QuestionsSudip MukhopadhyayNo ratings yet

- Post Office Surjit PDFDocument7 pagesPost Office Surjit PDFPawan SharmaNo ratings yet

- FAQ NPS-Corp ModelDocument13 pagesFAQ NPS-Corp Modeljamjam75No ratings yet

- The New National Pension SchemeDocument2 pagesThe New National Pension Schemegurudev001No ratings yet

- New Pension Scheme UpdatedDocument5 pagesNew Pension Scheme UpdatedBhawnaSharmaNo ratings yet

- Direct Tax Code: Capital Gains Tax On Sale of Residential PropertyDocument5 pagesDirect Tax Code: Capital Gains Tax On Sale of Residential Propertykarthikeyan.mohandossNo ratings yet

- Penalty and ProsecutionsDocument50 pagesPenalty and ProsecutionsSatish BhadaniNo ratings yet

- Income Tax Authority: Chapter-Xiii (Section 116 To 138)Document46 pagesIncome Tax Authority: Chapter-Xiii (Section 116 To 138)Satish BhadaniNo ratings yet

- Civics Class VIII - Chapter-3Document24 pagesCivics Class VIII - Chapter-3Satish BhadaniNo ratings yet

- Civics Class VIII - Chapter-1Document30 pagesCivics Class VIII - Chapter-1Satish BhadaniNo ratings yet

- AppealDocument28 pagesAppealSatish BhadaniNo ratings yet

- Income From Other SourcesDocument29 pagesIncome From Other SourcesSatish BhadaniNo ratings yet

- Female Foeticide and Child LabourDocument9 pagesFemale Foeticide and Child LabourSatish BhadaniNo ratings yet

- Court Fees Act, 1870.Document18 pagesCourt Fees Act, 1870.Satish BhadaniNo ratings yet

- 12.weather WorksheetDocument10 pages12.weather WorksheetSatish BhadaniNo ratings yet

- 13.pollution WorksheetDocument7 pages13.pollution WorksheetSatish BhadaniNo ratings yet

- 3.saftey 1. Fill in The BlanksDocument6 pages3.saftey 1. Fill in The BlanksSatish BhadaniNo ratings yet

- 11.light Sound and ForceDocument7 pages11.light Sound and ForceSatish Bhadani100% (1)

- 14.our Earth and Its NeighboursDocument8 pages14.our Earth and Its NeighboursSatish BhadaniNo ratings yet

- Birds-Food and MoreDocument7 pagesBirds-Food and MoreSatish BhadaniNo ratings yet

- Living and Non-Living ThingsDocument7 pagesLiving and Non-Living ThingsSatish BhadaniNo ratings yet

- Revocations Irc 501c3 Determinations 01292021Document40 pagesRevocations Irc 501c3 Determinations 01292021Bertha McGalliard PenceNo ratings yet

- This Study Resource Was: Quiz On Receivable FinancingDocument3 pagesThis Study Resource Was: Quiz On Receivable FinancingKez MaxNo ratings yet

- Modified Pag-Ibig Ii Enrollment FormDocument2 pagesModified Pag-Ibig Ii Enrollment FormJazziel Fortaliza100% (1)

- New Swot RetailDocument11 pagesNew Swot RetailijustyadavNo ratings yet

- Promo Mechs - 2022 McDo NUP MSMT FINALDocument14 pagesPromo Mechs - 2022 McDo NUP MSMT FINALFrank PasuntingNo ratings yet

- Jio Invoice 290323Document2 pagesJio Invoice 290323Deepak KiniNo ratings yet

- Eighteenth Edition, Global Edition: Customer Value-Driven Marketing Strategy: Creating Value For Target CustomersDocument41 pagesEighteenth Edition, Global Edition: Customer Value-Driven Marketing Strategy: Creating Value For Target CustomersIrene Elfrida SNo ratings yet

- Back-to-Back Letters of CreditDocument12 pagesBack-to-Back Letters of CreditSudershan ThaibaNo ratings yet

- Gauhati University - Exam Form Payment Receipt PDFDocument2 pagesGauhati University - Exam Form Payment Receipt PDFMuktadur RahmanNo ratings yet

- Cost Concepts and ClassificationsDocument6 pagesCost Concepts and ClassificationsNailiah MacakilingNo ratings yet

- 1701Q Quarterly Income Tax Return: For Individuals, Estates and TrustsDocument1 page1701Q Quarterly Income Tax Return: For Individuals, Estates and TrustsAshly MateoNo ratings yet

- YES Bank Annual Report 2014-15Document4 pagesYES Bank Annual Report 2014-15Nalini ChunchuNo ratings yet

- Financial Management For EntrepreneursDocument40 pagesFinancial Management For EntrepreneursHerald TheHorrorNo ratings yet

- 26.recent Changes in BankingDocument2 pages26.recent Changes in BankingVIKASH ARYANNo ratings yet

- Zomato LTD.: Investing Key To Compounding Long Term GrowthDocument5 pagesZomato LTD.: Investing Key To Compounding Long Term GrowthAvinash GollaNo ratings yet

- Cash To Accrual Basis of AccountingDocument6 pagesCash To Accrual Basis of AccountingChocobetternotNo ratings yet

- Registration Kenya Print Pack Sign Expo 19-21 Jan 2021Document4 pagesRegistration Kenya Print Pack Sign Expo 19-21 Jan 2021MAYANK CHHATWALNo ratings yet

- Advertising MCQDocument14 pagesAdvertising MCQArti Srivastava100% (1)

- Personal Finance 4th Edition Madura Test BankDocument18 pagesPersonal Finance 4th Edition Madura Test Bankkhuyenfrederickgjk8100% (29)

- Journal, T Accounts, WorksheetDocument10 pagesJournal, T Accounts, Worksheetkenneth coronelNo ratings yet

- Hybrid Approach To Corporate Sustainability Performance in Indonesia's Cement IndustryDocument21 pagesHybrid Approach To Corporate Sustainability Performance in Indonesia's Cement IndustryazzahraNo ratings yet

- Receivable Financing Sample ProblemDocument3 pagesReceivable Financing Sample ProblemKathleen FrondozoNo ratings yet

- Target Cost AnswersDocument6 pagesTarget Cost Answerspaul sagudaNo ratings yet

- Chapter 2 - Standardisation and Food Food LegislationDocument49 pagesChapter 2 - Standardisation and Food Food LegislationLam Thoại NguyễnNo ratings yet

- Chapter 3 Consumer MathematicsDocument36 pagesChapter 3 Consumer MathematicsHazmin NawiNo ratings yet

- ECONOMICSDocument2 pagesECONOMICSSuzui MasudaNo ratings yet

- IndianMiningLaws MMDRAct1957SubsequentAmendmentsDocument24 pagesIndianMiningLaws MMDRAct1957SubsequentAmendmentsSwiggly PandaNo ratings yet

- The Impact of Customer Services On Customer Satisfaction in The Food Industry: A Case Study of Mcdonald'SDocument15 pagesThe Impact of Customer Services On Customer Satisfaction in The Food Industry: A Case Study of Mcdonald'SMofy AllyNo ratings yet

- Chapter 6 - AnswersDocument22 pagesChapter 6 - Answersviva nazarenoNo ratings yet