Download as pptx, pdf, or txt

You might also like

- TSLA Q4 2023 UpdateDocument32 pagesTSLA Q4 2023 UpdateSimon AlvarezNo ratings yet

- MFRS133-LECTURE NOTES 1-FAR570 For StudentsDocument20 pagesMFRS133-LECTURE NOTES 1-FAR570 For StudentsJICNo ratings yet

- Financial Accounting II - FARM FRESH BERHADDocument25 pagesFinancial Accounting II - FARM FRESH BERHADWOO YOKE MEINo ratings yet

- AA025 PYQ 2015 - 2014 (ANS) by SectionDocument4 pagesAA025 PYQ 2015 - 2014 (ANS) by Sectionnurauniatiqah49No ratings yet

- Dec2022 Acc117 Acc106 Test 1 QDocument6 pagesDec2022 Acc117 Acc106 Test 1 Qlailanurinsyirah abdulhalimNo ratings yet

- ANSWER PSPM AA025 0708 by SectionDocument6 pagesANSWER PSPM AA025 0708 by SectionRISNATUL UZMA HELMI RIZAL100% (1)

- Part 1Document1 pagePart 1wawanNo ratings yet

- A221 MC 5 - StudentDocument6 pagesA221 MC 5 - StudentNajihah RazakNo ratings yet

- (KMS1013) Assignment 2 by Group 19Document10 pages(KMS1013) Assignment 2 by Group 19Nur Sabrina AfiqahNo ratings yet

- Assignment RES452Document2 pagesAssignment RES452halili rozaniNo ratings yet

- Introduction of Impiana Hotels BerhadDocument2 pagesIntroduction of Impiana Hotels BerhadAlia NursyifaNo ratings yet

- Question PSPM AA015 1718 by SectionDocument9 pagesQuestion PSPM AA015 1718 by Sectionnur athirahNo ratings yet

- Company Law - Case Study 2Document7 pagesCompany Law - Case Study 2Diana Yong MeiChi100% (1)

- Diploma in Management: Matriculation No: Identity Card No.: Telephone No.: E-Mail: Learning CentreDocument8 pagesDiploma in Management: Matriculation No: Identity Card No.: Telephone No.: E-Mail: Learning CentreSobanah ChandranNo ratings yet

- Far AssignmentDocument51 pagesFar AssignmentshazNo ratings yet

- CC 1Document11 pagesCC 1谦谦君子No ratings yet

- Exercise Topic 4Document7 pagesExercise Topic 4jr ylvsNo ratings yet

- Accounting TranslationDocument3 pagesAccounting TranslationJoanne_Kely_8735No ratings yet

- Topic 1 Introduction To AccountingDocument30 pagesTopic 1 Introduction To AccountingShanti GunaNo ratings yet

- Nota Bab 3Document27 pagesNota Bab 3Shanti GunaNo ratings yet

- Financial Analysis Nestle Malaysia Berhad For The Year 2019 A) Liquidity RatiosDocument13 pagesFinancial Analysis Nestle Malaysia Berhad For The Year 2019 A) Liquidity RatiosRawan NaderNo ratings yet

- Answers AA015 - Chapter 8Document5 pagesAnswers AA015 - Chapter 8nur athirah100% (1)

- A191 Mini Case Ppe QuestionDocument4 pagesA191 Mini Case Ppe Questiondini sofiaNo ratings yet

- A181 Tutorial 2Document9 pagesA181 Tutorial 2Fatin Nur Aina Mohd Radzi33% (3)

- Akaun Perdagangan Dan Untung Rugi Serta Akaun Pengasingan Untung Rugi Bagi Bulan Berakhir 31 Mac 2019Document2 pagesAkaun Perdagangan Dan Untung Rugi Serta Akaun Pengasingan Untung Rugi Bagi Bulan Berakhir 31 Mac 2019anon_164677107100% (1)

- Case Study Assignment Eco415 ( (Macroeconomics)Document4 pagesCase Study Assignment Eco415 ( (Macroeconomics)Dayat HidayatNo ratings yet

- Q&A Section A AA025 - Lecturer EditionDocument40 pagesQ&A Section A AA025 - Lecturer EditionSyirleen Adlyna Othman100% (1)

- Assigment Account FullDocument16 pagesAssigment Account FullFaid AmmarNo ratings yet

- Group Project Presentation GROUP 4Document34 pagesGroup Project Presentation GROUP 4Meena SyadaNo ratings yet

- Universiti Teknologi Mara Final Examination: CourseDocument7 pagesUniversiti Teknologi Mara Final Examination: Coursemuhammad ali imranNo ratings yet

- Aa025 Tutorial Answer Topic 7 AcmcDocument28 pagesAa025 Tutorial Answer Topic 7 Acmccjeipin123No ratings yet

- MINI-CASE 3 Intangible Assets AnswerDocument5 pagesMINI-CASE 3 Intangible Assets Answeryu choongNo ratings yet

- Nota Pengantar Statistik Bab 2Document49 pagesNota Pengantar Statistik Bab 2s12617880% (5)

- Maf603 Test 1 Dec 2020 - QuestionDocument8 pagesMaf603 Test 1 Dec 2020 - QuestionSITI FATIMAH AZ-ZAHRA ABD WAHIDNo ratings yet

- Soalan Assignment Tax Bab 7 Sem 6Document9 pagesSoalan Assignment Tax Bab 7 Sem 6Vasant SriudomNo ratings yet

- Question PSPM AA015 1011 by QuestionDocument6 pagesQuestion PSPM AA015 1011 by Questionnur athirahNo ratings yet

- A211 MC 2 - StudentDocument6 pagesA211 MC 2 - StudentWon HaNo ratings yet

- MAF 551 - Exercise 2 - Answer Question 1 - Seri Melur Institution - Ridzuan Bin Saharun 2017700141Document3 pagesMAF 551 - Exercise 2 - Answer Question 1 - Seri Melur Institution - Ridzuan Bin Saharun 2017700141RIDZUAN SAHARUNNo ratings yet

- PBL Tax - Final-EditDocument23 pagesPBL Tax - Final-EditRE100% (1)

- Bbaw2103 Financial AccountingDocument15 pagesBbaw2103 Financial AccountingSimon RajNo ratings yet

- Topic 10 - Lecturer 2Document10 pagesTopic 10 - Lecturer 2Nuradriana09No ratings yet

- Akaun Lejar Bentuk LajurDocument4 pagesAkaun Lejar Bentuk LajurlolololNo ratings yet

- A191 Tutorial 2 - Proposed AnswerDocument13 pagesA191 Tutorial 2 - Proposed AnswerAiden Ying0% (1)

- FIN242 REPORT Group 3Document32 pagesFIN242 REPORT Group 3Izzat FarhanNo ratings yet

- Chapter 9 - The Monetary SystemDocument5 pagesChapter 9 - The Monetary SystemRay JohnsonNo ratings yet

- A143 Sqqs1013 Ga Group 10Document9 pagesA143 Sqqs1013 Ga Group 10Nurul Farhan IbrahimNo ratings yet

- The Malaysian Business Code of EthicsDocument2 pagesThe Malaysian Business Code of EthicsSyafika SuhaimiNo ratings yet

- Consumer BehaviourDocument7 pagesConsumer Behaviourmophat SabareNo ratings yet

- Journals Question 2 ProblemsDocument22 pagesJournals Question 2 ProblemsAzam YahyaNo ratings yet

- Teori PerakaunanDocument47 pagesTeori PerakaunannabielanicoNo ratings yet

- The Recording ProcessDocument30 pagesThe Recording ProcesssyuhadaNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument33 pagesFinancial Statements, Cash Flow, and TaxesAyame KusuragiNo ratings yet

- Assignment Pad101Document4 pagesAssignment Pad101NURUL IZZATI AHMAD FERDAUSNo ratings yet

- Tutorial 11 Preparation of Financial Statements (Q)Document6 pagesTutorial 11 Preparation of Financial Statements (Q)lious liiNo ratings yet

- Mini Case 4-Investment Property (Student) - A192Document2 pagesMini Case 4-Investment Property (Student) - A192Chee Mei JeeNo ratings yet

- Solution Far510 - Jun 2015Document8 pagesSolution Far510 - Jun 2015azila aliasNo ratings yet

- ECO 561 INTERNATIONAL MICROECONOMIC (Group Assignment Rafie, Redzuan & Helmie)Document8 pagesECO 561 INTERNATIONAL MICROECONOMIC (Group Assignment Rafie, Redzuan & Helmie)MOHD REDZUAN BIN A KARIM (MOH-NEGERISEMBILAN)No ratings yet

- 1.0 Introduction of The Organisation Power Root (M) Sdn. BHDDocument14 pages1.0 Introduction of The Organisation Power Root (M) Sdn. BHDchua khen leong100% (1)

- Buku Nota PertnershipDocument33 pagesBuku Nota PertnershipmaiNo ratings yet

- Basic Accounting Concept: Topic 2Document58 pagesBasic Accounting Concept: Topic 2WAN FATIN IZZATI BINTI WAN NOOR AMAN MoeNo ratings yet

- Basics of Financial AccountingDocument30 pagesBasics of Financial AccountingSAURABH PATELNo ratings yet

- Am015 Chapter 3Document5 pagesAm015 Chapter 3Shanti GunaNo ratings yet

- Topic 1 Introduction To AccountingDocument30 pagesTopic 1 Introduction To AccountingShanti GunaNo ratings yet

- Nota Bab 3Document27 pagesNota Bab 3Shanti GunaNo ratings yet

- Sambung Bab 2Document30 pagesSambung Bab 2Shanti GunaNo ratings yet

- Accounting TermsDocument5 pagesAccounting TermsShanti GunaNo ratings yet

- Bab 8 Notes and Latihan Form 3 PtsiDocument15 pagesBab 8 Notes and Latihan Form 3 PtsiShanti Guna0% (1)

- Kento MomotaDocument4 pagesKento MomotaShanti GunaNo ratings yet

- Smart Health PDS BI 20181221 (Revised)Document3 pagesSmart Health PDS BI 20181221 (Revised)Shanti GunaNo ratings yet

- Crystal Meadows: Statement of Cash Flows Grigorios KrousiarlisDocument14 pagesCrystal Meadows: Statement of Cash Flows Grigorios KrousiarlisevdokiaaakNo ratings yet

- Rehabilitation of Sick Units - Concept, Process and DevelopmentsDocument33 pagesRehabilitation of Sick Units - Concept, Process and DevelopmentsGurkreet SodhiNo ratings yet

- Balance Sheet ProvisionalDocument2 pagesBalance Sheet ProvisionalRaja AdhikariNo ratings yet

- Financial AccountingDocument10 pagesFinancial AccountingNumber ButNo ratings yet

- Module 5 - Intangible AssetsDocument8 pagesModule 5 - Intangible AssetsLui0% (2)

- Case 1 Buffett Report FIN 635Document2 pagesCase 1 Buffett Report FIN 635jack stauberNo ratings yet

- Handout 3 - Plant Assets, Natural Resources, and Intangible AssetsDocument81 pagesHandout 3 - Plant Assets, Natural Resources, and Intangible Assetsyoussef abdellatifNo ratings yet

- JPIA CUP With AnswersDocument2 pagesJPIA CUP With AnswersDawn Rei DangkiwNo ratings yet

- FABM2 Module 05 (Q1-W6)Document12 pagesFABM2 Module 05 (Q1-W6)Christian ZebuaNo ratings yet

- Financial Statement Analysis Group Exercise: InstructionsDocument1 pageFinancial Statement Analysis Group Exercise: InstructionsMARY ACOSTANo ratings yet

- Bangladesh Accounting Standard (BAS-1)Document8 pagesBangladesh Accounting Standard (BAS-1)Simon Haque91% (11)

- DaisyDocument6 pagesDaisystaraera.18No ratings yet

- CH 2 PPEDocument71 pagesCH 2 PPEhassen mustefaNo ratings yet

- FABM MID TERMS Exam PERFORMANCE TASKDocument3 pagesFABM MID TERMS Exam PERFORMANCE TASKRaymond RocoNo ratings yet

- SBI Securities IPO Note on- Bansal Wire Industries LimitedDocument8 pagesSBI Securities IPO Note on- Bansal Wire Industries Limitedmanitjainm21No ratings yet

- Aalto University Annual Report EnglishDocument57 pagesAalto University Annual Report EnglishMandau KristiantoNo ratings yet

- Week 2 - Accrual Accounting and The Income Statement PDFDocument50 pagesWeek 2 - Accrual Accounting and The Income Statement PDFHisham ShihabNo ratings yet

- PWC - Financial Reporting in The Oil and Gas IndustryDocument156 pagesPWC - Financial Reporting in The Oil and Gas Industryahsan57100% (2)

- Jimma UniversityDocument37 pagesJimma Universitymubarek oumerNo ratings yet

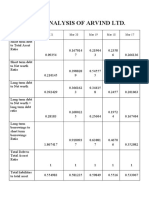

- Ratio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17Document10 pagesRatio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17simranNo ratings yet

- Sir Mac Book SolmanDocument10 pagesSir Mac Book SolmanJAY AUBREY PINEDANo ratings yet

- A Comparative Financial Analysis of Soft Drink IndustryDocument41 pagesA Comparative Financial Analysis of Soft Drink Industryvs1513100% (1)

- Introduction To Finance Lecture 1Document26 pagesIntroduction To Finance Lecture 1sestiliocharlesoremNo ratings yet

- Working Capital Operating Cycle, Profitability & LiquidityDocument5 pagesWorking Capital Operating Cycle, Profitability & LiquidityyngyaniNo ratings yet

- Iceland TaxDocument16 pagesIceland TaxRaja Ahmed HassanNo ratings yet

- Working Capital Finance in Food Processing IndustriesDocument13 pagesWorking Capital Finance in Food Processing IndustriesDurga Charan Pradhan50% (2)

- Basics of InvestmentDocument19 pagesBasics of InvestmentJohn DawsonNo ratings yet

- FR ConsolidationDocument31 pagesFR Consolidationvignesh_vikiNo ratings yet

- Case 1 New Signal Cable CompanyDocument6 pagesCase 1 New Signal Cable Companymilk teaNo ratings yet