Download as pptx, pdf, or txt

You might also like

- By Laws From HlurbDocument19 pagesBy Laws From HlurbPaul Verdida Pabillon80% (5)

- Forms of Business OrganizationsDocument27 pagesForms of Business OrganizationsArminda Villamin100% (1)

- United Beverages: Product Development Genius or One-Hit Wonder?Document35 pagesUnited Beverages: Product Development Genius or One-Hit Wonder?Paril ChhedaNo ratings yet

- Module 5 1Document6 pagesModule 5 1Manvendra Singh ShekhawatNo ratings yet

- Sole ProprietorshipDocument6 pagesSole ProprietorshipEron Roi Centina-gacutanNo ratings yet

- Business Units 2Document19 pagesBusiness Units 2mutasiga ericNo ratings yet

- Business LawDocument21 pagesBusiness LawUMAR FAROOQ TIPUNo ratings yet

- The Law of PartnershipDocument7 pagesThe Law of PartnershipAbu AsadNo ratings yet

- Business Forms 2Document7 pagesBusiness Forms 2Wamema joshuaNo ratings yet

- CH-2 Forms of Business Organizations (Notes)Document15 pagesCH-2 Forms of Business Organizations (Notes)Aryan PatelNo ratings yet

- Question: - Discuss Various Types of Business Organization?Document10 pagesQuestion: - Discuss Various Types of Business Organization?Hassan KhanNo ratings yet

- Company Law 2Document15 pagesCompany Law 2jonagoody9No ratings yet

- Advantages of A Sole ProprietorshipDocument4 pagesAdvantages of A Sole Proprietorshipdin shaNo ratings yet

- Business Organisation: BBA I SemDocument49 pagesBusiness Organisation: BBA I SemAnchal LuthraNo ratings yet

- Unit V Notes (Part I)Document15 pagesUnit V Notes (Part I)21EBKCS074PARULNo ratings yet

- Hand Out 8Document7 pagesHand Out 8abdool saheedNo ratings yet

- Forms of Business OrganisationDocument8 pagesForms of Business Organisationarvind123kumarNo ratings yet

- ch3 EntreDocument60 pagesch3 EntreeyoyoNo ratings yet

- AccountsDocument8 pagesAccountsAlveena UsmanNo ratings yet

- Forms of Tourism and Hospitality Business Ownership and FranchisingDocument27 pagesForms of Tourism and Hospitality Business Ownership and FranchisingJulie Mae Guanga Lpt100% (1)

- Forms of Business: Sole Proprietorship and PartnershipDocument17 pagesForms of Business: Sole Proprietorship and PartnershipTavleen KaurNo ratings yet

- IFA AssignmentDocument5 pagesIFA AssignmentAdnan JawedNo ratings yet

- Law PartnershipDocument6 pagesLaw PartnershipCyrelle MagpantayNo ratings yet

- Session 2 - Forms of Business OwnershipDocument18 pagesSession 2 - Forms of Business Ownershipruthykemunto111No ratings yet

- Chapter ThreeDocument27 pagesChapter Threekemelew AregaNo ratings yet

- Forms of Business OrganizationsDocument49 pagesForms of Business OrganizationsJooooooooNo ratings yet

- Lengua y Derecho IDocument56 pagesLengua y Derecho ICarolina BlancoNo ratings yet

- Chapter 2 Forms of Business Organisation NotesDocument14 pagesChapter 2 Forms of Business Organisation NotesLakshay DagarNo ratings yet

- Unit 2: Forms of Commercial Organizations: Meaning, Features, Merits and Limitations of The Following FormsDocument35 pagesUnit 2: Forms of Commercial Organizations: Meaning, Features, Merits and Limitations of The Following FormsYashAgarwalNo ratings yet

- Accounting For PartnershipDocument8 pagesAccounting For PartnershipsmlingwaNo ratings yet

- Lesson 2Document41 pagesLesson 2Ken Clausen CajayonNo ratings yet

- BL AssignmentDocument20 pagesBL AssignmentSheiryNo ratings yet

- Busl Assignment2 M.P.K SrihariDocument14 pagesBusl Assignment2 M.P.K Sriharimpk srihariNo ratings yet

- UCU 104 Lesson 6Document19 pagesUCU 104 Lesson 6Matt HeavenNo ratings yet

- Business Structures Notes 1Document6 pagesBusiness Structures Notes 1Nitin ChandraNo ratings yet

- Befa All UnitsDocument416 pagesBefa All UnitsFlash ActionNo ratings yet

- What Are The Types of Business Organization? Differentiate EachDocument3 pagesWhat Are The Types of Business Organization? Differentiate EachCarmelle BahadeNo ratings yet

- Forms of Business OrganizationDocument46 pagesForms of Business OrganizationAmanjot SachdevaNo ratings yet

- Unit No 2Document35 pagesUnit No 2awishNo ratings yet

- Forms of Business OrganizationDocument14 pagesForms of Business Organizationbhagyashreejana22No ratings yet

- Sole Proprietary: According To B.D. Wheeler, "The Sole Proprietorship Is That From of BusinessDocument12 pagesSole Proprietary: According To B.D. Wheeler, "The Sole Proprietorship Is That From of Businessapi-19729505No ratings yet

- 4 Forms of Business OrganizationsDocument30 pages4 Forms of Business Organizationsapi-2670235120% (1)

- Session 7Document10 pagesSession 7kalu kioNo ratings yet

- Business Ownership: Sole ProprietorshipDocument9 pagesBusiness Ownership: Sole ProprietorshipChristina RossettiNo ratings yet

- Chapter Three EnterpreneurshipDocument19 pagesChapter Three EnterpreneurshipSomanath BilihalNo ratings yet

- Introduction To PartnershipDocument22 pagesIntroduction To Partnershipgab mNo ratings yet

- FINAL Exam - Revision QuestionsDocument10 pagesFINAL Exam - Revision QuestionsĐào ĐăngNo ratings yet

- FINAL Exam Revision QuestionsDocument10 pagesFINAL Exam Revision QuestionsĐào ĐăngNo ratings yet

- Sole Proprietorship: Ownership PatternsDocument7 pagesSole Proprietorship: Ownership PatternsDeepak SharmaNo ratings yet

- Chapter 2Document16 pagesChapter 2Hayat Ali ShawNo ratings yet

- What Are The Basic Types of Business OrganizationsDocument3 pagesWhat Are The Basic Types of Business OrganizationsKyla Joy T. SanchezNo ratings yet

- Charter Separate Legal Entity Business Corporate Law Management Creditors Shareholders Labour Limited LiabilityDocument2 pagesCharter Separate Legal Entity Business Corporate Law Management Creditors Shareholders Labour Limited LiabilitymynoodleNo ratings yet

- Week 1 Session 1: Form of Business OrganizationDocument32 pagesWeek 1 Session 1: Form of Business OrganizationMyla D. DimayugaNo ratings yet

- Law in Enforcement Introduction To Financial ManagementDocument13 pagesLaw in Enforcement Introduction To Financial ManagementSamsuarPakasolangNo ratings yet

- Non-Corporate Business EntitiesDocument62 pagesNon-Corporate Business EntitiesTarunjeet Singh0% (3)

- Accounting 1 - Module 4Document41 pagesAccounting 1 - Module 4CATHNo ratings yet

- Corporate Law (Dba354)Document67 pagesCorporate Law (Dba354)Awini ShadrachNo ratings yet

- Commercial Law AssignmentDocument8 pagesCommercial Law AssignmentMemory ApiyoNo ratings yet

- Topic 11 Forms of Business Organisations TheoryDocument11 pagesTopic 11 Forms of Business Organisations TheoryKiasha WarnerNo ratings yet

- Your Personal Assets: Choose A Business StructureDocument10 pagesYour Personal Assets: Choose A Business StructureEds GarciaNo ratings yet

- The Advantages of Going From A Sole Proprietorship To A Limited PartnershipDocument5 pagesThe Advantages of Going From A Sole Proprietorship To A Limited PartnershipMaria Luz Clariza FonteloNo ratings yet

- Beerbal & Co Profile PDFDocument14 pagesBeerbal & Co Profile PDFIrshad murtazaNo ratings yet

- 1992 Friendly Societies Act 2012 EditionDocument233 pages1992 Friendly Societies Act 2012 EditionFuzzy_Wood_PersonNo ratings yet

- Hotel Invoice TemplateDocument1 pageHotel Invoice TemplatedeepakraaNo ratings yet

- 2020 NTP IP Chapter 3 4Document81 pages2020 NTP IP Chapter 3 4viet hoangNo ratings yet

- Wages and Time RecorDocument4 pagesWages and Time Recornurfitriana sandiniNo ratings yet

- HSBC Project ReportDocument66 pagesHSBC Project ReportSaurabh BudhirajaNo ratings yet

- RA 9520 Amended Cooperative CodeDocument29 pagesRA 9520 Amended Cooperative CodeLhui AquinoNo ratings yet

- Barangay Landican Annual Budget 2022Document25 pagesBarangay Landican Annual Budget 2022Maya AdovoNo ratings yet

- FABM 2 Financial AnalysisDocument67 pagesFABM 2 Financial Analysismary rose aragonNo ratings yet

- Financial Management Final Exam Solutions - F19401118 Jocelyn DarmawantyDocument11 pagesFinancial Management Final Exam Solutions - F19401118 Jocelyn DarmawantyJocelynNo ratings yet

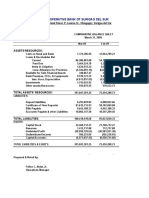

- Cooperative Bank of Surigao Del SurDocument4 pagesCooperative Bank of Surigao Del SurAnonymous iScW9lNo ratings yet

- TheEconomist 2023 04 08Document338 pagesTheEconomist 2023 04 08xuanzhou willNo ratings yet

- Dunning Notice 31 60Document2 pagesDunning Notice 31 60Laxmikant JoshiNo ratings yet

- D24174R104709Document11 pagesD24174R104709Nurul 'Ain0% (1)

- Vdocuments - MX Internship Report of Js Bank LTDDocument36 pagesVdocuments - MX Internship Report of Js Bank LTDShaikh JibranNo ratings yet

- 7110 s08 Ms 2Document8 pages7110 s08 Ms 2meelas123No ratings yet

- Clark Vs Sellner DigestDocument1 pageClark Vs Sellner Digestjim jim100% (1)

- Amazon: Name: Hammad Ahmed ACCA REG. NUMBER: 2427634Document20 pagesAmazon: Name: Hammad Ahmed ACCA REG. NUMBER: 2427634Hammad AhmedNo ratings yet

- Alipio Vs CADocument2 pagesAlipio Vs CASuiNo ratings yet

- Revision chung Tiếng AnhDocument4 pagesRevision chung Tiếng AnhVân Anh ĐặngNo ratings yet

- List of ShareholdersDocument1 pageList of ShareholderskaminiNo ratings yet

- Repayment of The First-Time Homebuyer CreditDocument1 pageRepayment of The First-Time Homebuyer CreditKate SchwartzNo ratings yet

- Order in The Matter of HBJ Capital Services Private Limited and HBJ Capital Ventures LLPDocument18 pagesOrder in The Matter of HBJ Capital Services Private Limited and HBJ Capital Ventures LLPShyam SunderNo ratings yet

- 2012 CombinedDocument195 pages2012 CombinedTamal Kishore AcharyaNo ratings yet

- Mohammad SaqibDocument1 pageMohammad SaqibMohammad SaqibNo ratings yet

- Profit Planning and BudgetingDocument9 pagesProfit Planning and BudgetingMaria Beatriz NavecisNo ratings yet

- 2016 Form1095CDocument1 page2016 Form1095CpatNo ratings yet

- Peregrine Powerpoint 2Document36 pagesPeregrine Powerpoint 2api-253241169No ratings yet