Download as ppt, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- MCS CertificateDocument1 pageMCS Certificatejessssan28No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Ch08 Harrison 8e GE SM (Revised)Document102 pagesCh08 Harrison 8e GE SM (Revised)Muh BilalNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Ch12 Harrison 8e GE SMDocument87 pagesCh12 Harrison 8e GE SMMuh BilalNo ratings yet

- AccHor 7e CH 02Document28 pagesAccHor 7e CH 02Muh BilalNo ratings yet

- AccHor 7e CH 01Document32 pagesAccHor 7e CH 01Muh BilalNo ratings yet

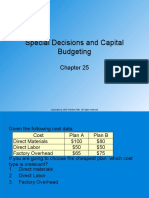

- AccHor 7e CH 25Document24 pagesAccHor 7e CH 25Muh BilalNo ratings yet

- AccHor 7e CH 22Document28 pagesAccHor 7e CH 22Muh BilalNo ratings yet

- AccHor 7e CH 23Document24 pagesAccHor 7e CH 23Muh BilalNo ratings yet

- AccHor 7e CH 21Document25 pagesAccHor 7e CH 21Muh BilalNo ratings yet

- AccHor 7e CH 17Document24 pagesAccHor 7e CH 17Muh BilalNo ratings yet

- Ch03 Harrison 8e GE SMDocument113 pagesCh03 Harrison 8e GE SMMuh BilalNo ratings yet

- AccHor 7e CH 19Document28 pagesAccHor 7e CH 19Muh BilalNo ratings yet

- Ch07 Harrison 8e GE SMDocument87 pagesCh07 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch06 Harrison 8e GE SMDocument87 pagesCh06 Harrison 8e GE SMMuh BilalNo ratings yet

- AccHor 7e CH 18Document22 pagesAccHor 7e CH 18Muh BilalNo ratings yet

- AccHor 7e CH 14Document22 pagesAccHor 7e CH 14Muh BilalNo ratings yet

- Ch05 Harrison 8e GE SMDocument73 pagesCh05 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch01 Harrison 8e GE SMDocument63 pagesCh01 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch04 Harrison 8e GE SMDocument73 pagesCh04 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch02 Harrison 8e GE SMDocument96 pagesCh02 Harrison 8e GE SMMuh BilalNo ratings yet

- Chap 023Document19 pagesChap 023Muh BilalNo ratings yet

- Risk Management: Fundamentals of Corporate FinanceDocument24 pagesRisk Management: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Chap 022Document23 pagesChap 022Muh BilalNo ratings yet

- Short-Term Financial Planning: Fundamentals of Corporate FinanceDocument26 pagesShort-Term Financial Planning: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Financial Statement Analysis: Fundamentals of Corporate FinanceDocument23 pagesFinancial Statement Analysis: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Long-Term Financial Planning: Fundamentals of Corporate FinanceDocument17 pagesLong-Term Financial Planning: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Parks Vs Province of TarlacDocument2 pagesParks Vs Province of TarlacTippy Dos Santos100% (2)

- The Public Assembly Act of 1985Document14 pagesThe Public Assembly Act of 1985Samn Pistola Cadley100% (1)

- AWS A5.11 Specification For Nickel and Nickel Alloy Welding Electrodes For Chielded Metal Arc Welding PDFDocument41 pagesAWS A5.11 Specification For Nickel and Nickel Alloy Welding Electrodes For Chielded Metal Arc Welding PDFcamilorodcoNo ratings yet

- (220009488) Contemporary Issue On Labour Law Reform in India An OverviewDocument30 pages(220009488) Contemporary Issue On Labour Law Reform in India An OverviewIshaan YadavNo ratings yet

- A Criticism On G H A Juynboll Perspectives About Mutawatir HadithDocument12 pagesA Criticism On G H A Juynboll Perspectives About Mutawatir HadithNacer BenrajebNo ratings yet

- MCQ Law On Sales - CompressDocument11 pagesMCQ Law On Sales - CompressShermaine VenturaNo ratings yet

- Medical Marijuana Facility ApplicationsDocument2 pagesMedical Marijuana Facility ApplicationsJackie SmithNo ratings yet

- Ayala-Corp-Investment-Proposal-Paper FinalDocument13 pagesAyala-Corp-Investment-Proposal-Paper FinalBOB MARLOWNo ratings yet

- Omega OM-CP-RTDTEMP2000Document5 pagesOmega OM-CP-RTDTEMP2000luis2006041380No ratings yet

- 9 Commercial StudiesDocument4 pages9 Commercial StudiesDeepram AbhiNo ratings yet

- PdfkenmoreDocument11 pagesPdfkenmoreJorge JaramilloNo ratings yet

- Class Exercise 1 PCF With AnswersDocument2 pagesClass Exercise 1 PCF With Answersgonzaleskyla277No ratings yet

- Lesson 14 - Judicial OrderDocument12 pagesLesson 14 - Judicial Orderdorindodo26maiNo ratings yet

- NSA Unclassified Report On PrismDocument11 pagesNSA Unclassified Report On PrismFrancisBerkman100% (1)

- Eligibility Test Cases - V3.0Document1 pageEligibility Test Cases - V3.0Shabbir ShamsudeenNo ratings yet

- SG NL 2015Document102 pagesSG NL 2015TC Carlos100% (1)

- Agra CasesDocument33 pagesAgra CasesMarielle Joyce G. AristonNo ratings yet

- Labor Law Social Legislation: Answers To Bar Examination QuestionsDocument108 pagesLabor Law Social Legislation: Answers To Bar Examination QuestionsJocelyn Baliwag-Alicmas Banganan BayubayNo ratings yet

- Classification of TaxesDocument5 pagesClassification of Taxesakanksha singhNo ratings yet

- Check in VoucherDocument1 pageCheck in VoucherKathleen PadillonNo ratings yet

- Quaid-e-Azam Muhammad Ali Jinnah's Vision of PakistanDocument9 pagesQuaid-e-Azam Muhammad Ali Jinnah's Vision of PakistanRizwan ShahNo ratings yet

- Freshmen Who Are Inactive - SAM CAM 8-2010Document2,329 pagesFreshmen Who Are Inactive - SAM CAM 8-2010xtracal12No ratings yet

- HR Policy Manual 24. Mobile and Telephone PolicyDocument2 pagesHR Policy Manual 24. Mobile and Telephone PolicyFaizan AhmedNo ratings yet

- Report PDFDocument2 pagesReport PDFJBStringerNo ratings yet

- Balnce Sheet Sam 3Document2 pagesBalnce Sheet Sam 3Samuel DebebeNo ratings yet

- Feds Vs AntifedsDocument3 pagesFeds Vs Antifedsapi-328061525No ratings yet

- Teves V Comelec FullDocument5 pagesTeves V Comelec FulljNo ratings yet

- Truth AboutDocument33 pagesTruth Aboutdigitaldiva360No ratings yet

- My 12/17/14 Complaint About Sydnee McElroy MD To The WV Board of Medicine and The Board's Next-Day ReplyDocument3 pagesMy 12/17/14 Complaint About Sydnee McElroy MD To The WV Board of Medicine and The Board's Next-Day ReplyPeter M. Heimlich0% (13)