Download as ppt, pdf, or txt

You might also like

- Deed of Absolute SaleDocument3 pagesDeed of Absolute Saleramel4uNo ratings yet

- Ch08 Harrison 8e GE SM (Revised)Document102 pagesCh08 Harrison 8e GE SM (Revised)Muh BilalNo ratings yet

- Ch12 Harrison 8e GE SMDocument87 pagesCh12 Harrison 8e GE SMMuh BilalNo ratings yet

- Tiger Airways Case StudyDocument6 pagesTiger Airways Case StudyRiko Lam0% (1)

- Annex F WaiverDocument2 pagesAnnex F WaiverMaela Maala Mendoza82% (11)

- Parity PPPDocument42 pagesParity PPPDeus MalimaNo ratings yet

- International: Financial ManagementDocument45 pagesInternational: Financial ManagementOmary MsikuNo ratings yet

- Kc-Fin 315 - Chapter 5Document9 pagesKc-Fin 315 - Chapter 5Hoàng Trương MinhNo ratings yet

- 6 International Parity Relationships & Forecasting Foreign Exchange RatesDocument35 pages6 International Parity Relationships & Forecasting Foreign Exchange RatesRicha ChauhanNo ratings yet

- Module 6Document45 pagesModule 6Kamlesh VansjaliaNo ratings yet

- Exchange Rate DeterminationDocument43 pagesExchange Rate DeterminationAmit Sinha100% (1)

- International Parity Relationships & Forecasting Exchange RatesDocument33 pagesInternational Parity Relationships & Forecasting Exchange RatesKARISHMAATA2No ratings yet

- International Finance IF4 - FX MarketsDocument37 pagesInternational Finance IF4 - FX MarketsMariem StylesNo ratings yet

- Eun 9e International Financial Management PPT CH06 AccessibleDocument31 pagesEun 9e International Financial Management PPT CH06 AccessibleDao Dang Khoa FUG CTNo ratings yet

- Futures and Options On Foreign Exchange: International Financial ManagementDocument50 pagesFutures and Options On Foreign Exchange: International Financial ManagementvijiNo ratings yet

- International RiskDocument35 pagesInternational Riskmarjannaseri77No ratings yet

- If Jeff Medora CHP 07Document25 pagesIf Jeff Medora CHP 07Naoman ChNo ratings yet

- 7 Int Parity RelationshipDocument40 pages7 Int Parity RelationshipumangNo ratings yet

- Solutions Manual: Introducing Corporate Finance 2eDocument9 pagesSolutions Manual: Introducing Corporate Finance 2ePaul Sau HutaNo ratings yet

- The Forex MarketDocument22 pagesThe Forex MarketMrMoney ManNo ratings yet

- IFM8e ch07Document20 pagesIFM8e ch07adnanNo ratings yet

- DocDocument8 pagesDocAhmad RahhalNo ratings yet

- CH 7Document25 pagesCH 7Zuhaib SultanNo ratings yet

- Management of Economic Exposure: Chapter NineDocument25 pagesManagement of Economic Exposure: Chapter NineHu Jia QuenNo ratings yet

- Management of Economic Exposure: InternationalDocument28 pagesManagement of Economic Exposure: InternationalAnmol VigNo ratings yet

- Eun7e CH 009Document33 pagesEun7e CH 009Shruti AshokNo ratings yet

- 27 Managing International RisksDocument11 pages27 Managing International Risksddrechsler9No ratings yet

- Chap 005-Interest Rates and Bond ValuationDocument43 pagesChap 005-Interest Rates and Bond Valuationsarvenaz kamali matin100% (1)

- Exchange Rate DeterminationDocument29 pagesExchange Rate DeterminationChacha Donald Trump America waleNo ratings yet

- Multinational Accounting: Foreign Currency Transactions and Financial InstrumentsDocument44 pagesMultinational Accounting: Foreign Currency Transactions and Financial InstrumentsWidya PertiwiNo ratings yet

- Transaction Expoure - HalfDocument22 pagesTransaction Expoure - Halfvijay vighneshNo ratings yet

- Transaction Exposure Management - CompleteDocument52 pagesTransaction Exposure Management - Completevijay vighneshNo ratings yet

- International Arbitrage and Interest Rate ParityDocument20 pagesInternational Arbitrage and Interest Rate Parityjahirul munnaNo ratings yet

- Interest Rates and Bonds Chapter 7Document39 pagesInterest Rates and Bonds Chapter 7Rahul KhadkaNo ratings yet

- Chapter 17Document28 pagesChapter 17Talat_Gergawi_2786No ratings yet

- FOFch 17Document48 pagesFOFch 17ferahNo ratings yet

- CH 07 - International Arbitrage and IRPDocument31 pagesCH 07 - International Arbitrage and IRPRim RimNo ratings yet

- Multinational Financial ManagementDocument42 pagesMultinational Financial ManagementannafuentesNo ratings yet

- Interest Rate and Purchasing Power ParityDocument40 pagesInterest Rate and Purchasing Power ParityAntriksh GillNo ratings yet

- International ArbitrageDocument27 pagesInternational ArbitragehasnainNo ratings yet

- International Parity Relationships & Forecasting Exchange Rates - ShortDocument12 pagesInternational Parity Relationships & Forecasting Exchange Rates - ShortYoussef BrahmiNo ratings yet

- 12+Valuation+of+stock+and+bonds - โหมดความเข้ากันได้Document14 pages12+Valuation+of+stock+and+bonds - โหมดความเข้ากันได้NATCHA TANAPANJAPORNNo ratings yet

- CH19Document29 pagesCH19sajaabdullah195No ratings yet

- South Korean CaseDocument6 pagesSouth Korean CaseIqbal JoyNo ratings yet

- International FinanceDocument30 pagesInternational FinanceMyrna LaquitanNo ratings yet

- Chapter Review International Arbitrage and Interest Rate Parity International ArbitrageDocument9 pagesChapter Review International Arbitrage and Interest Rate Parity International ArbitrageWi SilalahiNo ratings yet

- Foreign ExchangeDocument15 pagesForeign ExchangeanshpaulNo ratings yet

- International Parity RelationshipsDocument45 pagesInternational Parity RelationshipsDr RizwanaNo ratings yet

- Interest Rate Parity (IRP)Document13 pagesInterest Rate Parity (IRP)Hiron Rafi100% (1)

- Unit III Future and Options On Foreign ExchangeDocument67 pagesUnit III Future and Options On Foreign ExchangeNeha ShelkeNo ratings yet

- Summary MKI Chapter 7Document5 pagesSummary MKI Chapter 7DeviNo ratings yet

- Lesson 3 - c7Document30 pagesLesson 3 - c7TRANG LÊ THỊ HẠNHNo ratings yet

- CH06Document52 pagesCH06Tasnova AalamNo ratings yet

- Econ TesterDocument2 pagesEcon TesterGrace RoqueNo ratings yet

- Fixed Income Securities: Lecture Note 3: Term Structure and Yield CurveDocument62 pagesFixed Income Securities: Lecture Note 3: Term Structure and Yield CurveKOTHAKAPU SANTOSH REDDYNo ratings yet

- The Time Value of Money: Fundamentals of Corporate FinanceDocument36 pagesThe Time Value of Money: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- IBF301 Ch006 2020Document38 pagesIBF301 Ch006 2020Giang PhanNo ratings yet

- 70-398 International Finance SPRING 2023: Prof. Serkan AkgucDocument29 pages70-398 International Finance SPRING 2023: Prof. Serkan AkgucAmiko GogitidzeNo ratings yet

- Chapter 7 - CompleteDocument20 pagesChapter 7 - Completemohsin razaNo ratings yet

- IBF301 Ch006Document37 pagesIBF301 Ch006vanossman904No ratings yet

- International Finance 5Document36 pagesInternational Finance 5Hu Jia QuenNo ratings yet

- Corporate Finance: Net Present ValueDocument31 pagesCorporate Finance: Net Present ValueMahfuzur RahmanNo ratings yet

- AccHor 7e CH 23Document24 pagesAccHor 7e CH 23Muh BilalNo ratings yet

- AccHor 7e CH 01Document32 pagesAccHor 7e CH 01Muh BilalNo ratings yet

- AccHor 7e CH 02Document28 pagesAccHor 7e CH 02Muh BilalNo ratings yet

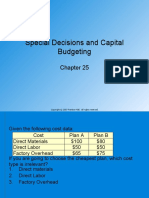

- AccHor 7e CH 25Document24 pagesAccHor 7e CH 25Muh BilalNo ratings yet

- AccHor 7e CH 14Document22 pagesAccHor 7e CH 14Muh BilalNo ratings yet

- AccHor 7e CH 21Document25 pagesAccHor 7e CH 21Muh BilalNo ratings yet

- AccHor 7e CH 22Document28 pagesAccHor 7e CH 22Muh BilalNo ratings yet

- AccHor 7e CH 19Document28 pagesAccHor 7e CH 19Muh BilalNo ratings yet

- AccHor 7e CH 18Document22 pagesAccHor 7e CH 18Muh BilalNo ratings yet

- AccHor 7e CH 17Document24 pagesAccHor 7e CH 17Muh BilalNo ratings yet

- Ch06 Harrison 8e GE SMDocument87 pagesCh06 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch07 Harrison 8e GE SMDocument87 pagesCh07 Harrison 8e GE SMMuh BilalNo ratings yet

- Risk Management: Fundamentals of Corporate FinanceDocument24 pagesRisk Management: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Ch05 Harrison 8e GE SMDocument73 pagesCh05 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch01 Harrison 8e GE SMDocument63 pagesCh01 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch03 Harrison 8e GE SMDocument113 pagesCh03 Harrison 8e GE SMMuh BilalNo ratings yet

- Ch04 Harrison 8e GE SMDocument73 pagesCh04 Harrison 8e GE SMMuh BilalNo ratings yet

- Chap 023Document19 pagesChap 023Muh BilalNo ratings yet

- Ch02 Harrison 8e GE SMDocument96 pagesCh02 Harrison 8e GE SMMuh BilalNo ratings yet

- Short-Term Financial Planning: Fundamentals of Corporate FinanceDocument26 pagesShort-Term Financial Planning: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Financial Statement Analysis: Fundamentals of Corporate FinanceDocument23 pagesFinancial Statement Analysis: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Long-Term Financial Planning: Fundamentals of Corporate FinanceDocument17 pagesLong-Term Financial Planning: Fundamentals of Corporate FinanceMuh BilalNo ratings yet

- Standards On Auditing and Its Usage in AuditingDocument5 pagesStandards On Auditing and Its Usage in Auditingbhagaban_fm8098No ratings yet

- Audit of Liabilities 1Document1 pageAudit of Liabilities 1Ricalyn E. SumpayNo ratings yet

- AJE Practice Problems - 2127759290Document2 pagesAJE Practice Problems - 2127759290Nichole Joy XielSera TanNo ratings yet

- 14 ConsignmentDocument8 pages14 ConsignmentangeelinaNo ratings yet

- 1) Enter Equity: $10,000.00 2) Enter % To Risk 3) Estimated No. of Pips To HoldDocument7 pages1) Enter Equity: $10,000.00 2) Enter % To Risk 3) Estimated No. of Pips To HoldHicham HasnaouiNo ratings yet

- Sell More With A Buyer Credit GuaranteeDocument2 pagesSell More With A Buyer Credit GuaranteeSalah AyoubiNo ratings yet

- Old-Line Firms in Auto Race: For PersonalDocument32 pagesOld-Line Firms in Auto Race: For PersonalstefanoNo ratings yet

- Global Venture Capital LandscapeDocument18 pagesGlobal Venture Capital LandscapeUlas CanakciNo ratings yet

- Far - Team PRTC 1stpb May 2023Document8 pagesFar - Team PRTC 1stpb May 2023Alexander IgotNo ratings yet

- MBA Questions I Year & II Year Safety ManagementDocument44 pagesMBA Questions I Year & II Year Safety Managementbabu1434100% (3)

- 260520231838-Bismillah Rice MillDocument5 pages260520231838-Bismillah Rice MillPranjal AgarwalNo ratings yet

- Industry Profile: CommodityDocument12 pagesIndustry Profile: CommoditySaidi ReddyNo ratings yet

- Document5 AMEX Dec 2013Document14 pagesDocument5 AMEX Dec 2013Daniel TaylorNo ratings yet

- Metrobank vs. Riverside MillsDocument18 pagesMetrobank vs. Riverside MillsStrawberryNo ratings yet

- (L) Chapter 5 Accounting Concepts - ConventionsDocument6 pages(L) Chapter 5 Accounting Concepts - ConventionsCHZE CHZI CHUAHNo ratings yet

- Kholipah & Suryandari (2019)Document14 pagesKholipah & Suryandari (2019)Riyandi JoshuaNo ratings yet

- Upstocx Demat-Account-Closure-Form PDFDocument1 pageUpstocx Demat-Account-Closure-Form PDFGautam DixitNo ratings yet

- Class 9 Economics The Story of Village PalampurDocument9 pagesClass 9 Economics The Story of Village PalampurSujitnkbps100% (3)

- Test Bank For Contemporary Engineering Economics 5th Edition by ParkDocument35 pagesTest Bank For Contemporary Engineering Economics 5th Edition by Parkalsikeamorosoe4cn7100% (52)

- Premium Breakup: MCA Paisa Bazaar HDFC Argo 4 Wheel WorldDocument3 pagesPremium Breakup: MCA Paisa Bazaar HDFC Argo 4 Wheel WorldrashmimNo ratings yet

- Bricks Bussines PlanDocument23 pagesBricks Bussines Plansirajt300No ratings yet

- Fabm 2: Quarter 3 - Module 1 The Statement of Financial Position (Elements, Forms and Its Classifications)Document23 pagesFabm 2: Quarter 3 - Module 1 The Statement of Financial Position (Elements, Forms and Its Classifications)Maria Nikka GarciaNo ratings yet

- Covenants Running With LandDocument27 pagesCovenants Running With LandDivyanshu GuptaNo ratings yet

- Companies Act, 2001 MauritiusDocument285 pagesCompanies Act, 2001 MauritiusJoydeep NtNo ratings yet

- Hon Elly Karuhanga UMCP PDFDocument4 pagesHon Elly Karuhanga UMCP PDFPeter BofinNo ratings yet

- Commrev CompilationDocument11 pagesCommrev CompilationAC SubijanoNo ratings yet

- Sources of Taxation LawDocument21 pagesSources of Taxation LawViola Ari PutriNo ratings yet