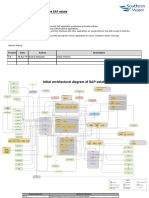

Obtain An Understanding of The Customer's Key Business Processes Define The Client's Organization Structure in SAP Based On Those Business Processes

Obtain An Understanding of The Customer's Key Business Processes Define The Client's Organization Structure in SAP Based On Those Business Processes

You might also like

- Stern Strategy EssentialsDocument121 pagesStern Strategy Essentialssatya324100% (3)

- Case Submission - Stone Container Corporation (A) ' Group VIIIDocument5 pagesCase Submission - Stone Container Corporation (A) ' Group VIIIGURNEET KAURNo ratings yet

- Implementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesFrom EverandImplementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesNo ratings yet

- Revenue Recognition: With SAP S/4HANA Cloud in The Context of IFRS15/ASC606Document35 pagesRevenue Recognition: With SAP S/4HANA Cloud in The Context of IFRS15/ASC606m_casavecchiaNo ratings yet

- Final Exam Financial MarketsDocument9 pagesFinal Exam Financial MarketsLorielyn Mae SalcedoNo ratings yet

- Union Gaming Feasibility StudyDocument51 pagesUnion Gaming Feasibility StudyAnn DwyerNo ratings yet

- GM Andean Accounts Payable Workshop v1 April09Document18 pagesGM Andean Accounts Payable Workshop v1 April09Subbireddy ChintapalliNo ratings yet

- Sap Finance OverviewDocument45 pagesSap Finance Overviewprat05No ratings yet

- Introduction To SAPDocument60 pagesIntroduction To SAPAnonymous aX3l06L5eNo ratings yet

- SAP OverviewDocument36 pagesSAP OverviewsivakumarNo ratings yet

- Introduction To ERPDocument24 pagesIntroduction To ERPAbdul WahabNo ratings yet

- Evaluated Receipt Settlement Sap PDFDocument2 pagesEvaluated Receipt Settlement Sap PDFTim0% (2)

- Lockbox BAI2 Layout With SAPDocument14 pagesLockbox BAI2 Layout With SAPMafia333No ratings yet

- Truebell - Fin - Ap - Config - Account PayableDocument49 pagesTruebell - Fin - Ap - Config - Account PayableRajesh ChowdaryNo ratings yet

- Sap Fi S4 Hana Asset Accounting Part 1Document6 pagesSap Fi S4 Hana Asset Accounting Part 1NASEER ULLAHNo ratings yet

- Day1 - Introduction To SAP FICODocument37 pagesDay1 - Introduction To SAP FICOankitavengNo ratings yet

- HSPL Fi 06 House Bank v1.0Document18 pagesHSPL Fi 06 House Bank v1.0Naveen KumarNo ratings yet

- Business Processes Master List Financial Accounting & ControllingDocument21 pagesBusiness Processes Master List Financial Accounting & ControllingPrathamesh ParkerNo ratings yet

- Chapter 29 SAP Databse Tables-1Document20 pagesChapter 29 SAP Databse Tables-1zachary kehoeNo ratings yet

- Sapbrainsonline Com Help FSCM Module Tutorials HTMLDocument8 pagesSapbrainsonline Com Help FSCM Module Tutorials HTMLCarlos CasañoNo ratings yet

- SAP CO CookbookDocument129 pagesSAP CO CookbookMisbah FatimaNo ratings yet

- SRI RUDRAM With MeaningDocument73 pagesSRI RUDRAM With Meaningsreelatha1No ratings yet

- AC206 Parallel Valuation and Financial Reporting: Local Law - IAS (IFRS) / US-GAAP?Document6 pagesAC206 Parallel Valuation and Financial Reporting: Local Law - IAS (IFRS) / US-GAAP?mhku1No ratings yet

- 2016 05 Spring Catalog SAP-PRESS DOWNLOAD PDFDocument32 pages2016 05 Spring Catalog SAP-PRESS DOWNLOAD PDFVitlenNo ratings yet

- Standard SAP Business Process Flow DiagramDocument1 pageStandard SAP Business Process Flow DiagramAjay KumarNo ratings yet

- Table Name: Description Important FieldsDocument5 pagesTable Name: Description Important FieldsJyotiraditya Banerjee100% (1)

- Sap - PDF Catalogue s4Document25 pagesSap - PDF Catalogue s4razatsaxena0% (2)

- Fi-Co SAP Systems Application and Products in Data ProcessingDocument295 pagesFi-Co SAP Systems Application and Products in Data ProcessingPrabhakarNo ratings yet

- SAP CO ECC 6.0 Bootcamp - Day 5Document104 pagesSAP CO ECC 6.0 Bootcamp - Day 5dcanohNo ratings yet

- SAp Testing Part 5Document11 pagesSAp Testing Part 5RajaNo ratings yet

- Fdocuments - in Sap Overview PP PC IntegrationDocument84 pagesFdocuments - in Sap Overview PP PC IntegrationHimanshu SinghNo ratings yet

- SAP Bootcamp Quiz SDDocument47 pagesSAP Bootcamp Quiz SDBeverly GordonNo ratings yet

- Simple Finance - The Convergence of The GL Account and The Cost ElementDocument12 pagesSimple Finance - The Convergence of The GL Account and The Cost Elementjoseph davidNo ratings yet

- Ivend Retail Integration With SapDocument21 pagesIvend Retail Integration With SapniteshNo ratings yet

- BP OP ENTPR S4HANA1909 06 Process-Steps EN USDocument816 pagesBP OP ENTPR S4HANA1909 06 Process-Steps EN USBiji RoyNo ratings yet

- An SAP Consultant - ABAP - Step by Step Tutorial On Smart Forms - Template NodeDocument9 pagesAn SAP Consultant - ABAP - Step by Step Tutorial On Smart Forms - Template NodearunNo ratings yet

- S 4 HanaDocument51 pagesS 4 Hanamannadas206No ratings yet

- SAP Workflow Introduction For PresentationDocument40 pagesSAP Workflow Introduction For PresentationanantdaNo ratings yet

- Inbound Data Flow in SAP Retail EnvironmentDocument3 pagesInbound Data Flow in SAP Retail EnvironmentEklavya BansalNo ratings yet

- Vendor Invoice Booking-MIRODocument5 pagesVendor Invoice Booking-MIROAMIT SAWANTNo ratings yet

- Leveraging S4 AI ML Capabilities 1689177179Document79 pagesLeveraging S4 AI ML Capabilities 1689177179nagarajuNo ratings yet

- Sap Fico Portfolio - Monisha DemarkDocument245 pagesSap Fico Portfolio - Monisha Demarknandhinikrish306No ratings yet

- 011000358700000031292010EDocument74 pages011000358700000031292010Erameshdv9No ratings yet

- Sap Fico Interview QuestionsDocument357 pagesSap Fico Interview QuestionsMohamed Azouggarh100% (1)

- Sap TablesDocument29 pagesSap TablesTest100% (1)

- SAP ERP Solution: FICO-Reconciliation ToolDocument21 pagesSAP ERP Solution: FICO-Reconciliation ToolViivekcanandu MethriNo ratings yet

- JVA-TRN - FI109 - Joint Venture Accounting v1.1Document83 pagesJVA-TRN - FI109 - Joint Venture Accounting v1.1James Anderson Luna SilvaNo ratings yet

- SAP OverviewDocument20 pagesSAP OverviewMarkup QpicNo ratings yet

- SAP FI Ecc X s4Document14 pagesSAP FI Ecc X s4fzankNo ratings yet

- Sap Financial Supply Chain Management (FSCM) : System & Technology Model Finance SSC June 2019Document20 pagesSap Financial Supply Chain Management (FSCM) : System & Technology Model Finance SSC June 2019fadliNo ratings yet

- New Asset AccountingDocument19 pagesNew Asset AccountingShruti ChapraNo ratings yet

- Sap Ariba Create SourcingDocument18 pagesSap Ariba Create SourcingS M SHEKAR AND CONo ratings yet

- Intro ERP Using GBI Slides FI en v2.01Document25 pagesIntro ERP Using GBI Slides FI en v2.01shobhit1980inNo ratings yet

- Hana Sidecar Kuleuven PDFDocument51 pagesHana Sidecar Kuleuven PDFPaul DeleuzeNo ratings yet

- SAP Discovery - Initial Architectural Diagram of SAP Estate v1.0Document3 pagesSAP Discovery - Initial Architectural Diagram of SAP Estate v1.0PulkKit SharMaNo ratings yet

- S4HANA OP 1511 Learning Journey BetaDocument9 pagesS4HANA OP 1511 Learning Journey BetaJorge Santillan0% (1)

- Sales Area: S / 4 HANA ContentDocument34 pagesSales Area: S / 4 HANA ContentEnrique Israel Flores ZúñigaNo ratings yet

- Creating GL AccountsDocument19 pagesCreating GL AccountsJyotiraditya BanerjeeNo ratings yet

- Accrual Engine: Solution Management FinancialsDocument32 pagesAccrual Engine: Solution Management FinancialsateeqbajwaNo ratings yet

- ISU TablesDocument1 pageISU TablesrajusampathiraoNo ratings yet

- Procurement ProcessDocument32 pagesProcurement ProcessAnkit GoyalNo ratings yet

- Building A Tax Calculation ApplicationDocument11 pagesBuilding A Tax Calculation ApplicationMartin De LeoNo ratings yet

- Tender FormDocument7 pagesTender Formaharish_iitkNo ratings yet

- Museums As Participants in The Market Game: The Political and Economic Context of The Functioning of The MuseumsDocument19 pagesMuseums As Participants in The Market Game: The Political and Economic Context of The Functioning of The MuseumsMika FungoNo ratings yet

- Session 18 Securitization of Loans and Other AssetsDocument13 pagesSession 18 Securitization of Loans and Other AssetsNeena TomyNo ratings yet

- 10000027146Document47 pages10000027146Chapter 11 DocketsNo ratings yet

- Payment of Bonus Act, 1965 & The Rules: ChecklistDocument2 pagesPayment of Bonus Act, 1965 & The Rules: ChecklistparavindNo ratings yet

- Taxation - UP 2008Document163 pagesTaxation - UP 2008Martoni SaliendraNo ratings yet

- Audit - Isa 500Document6 pagesAudit - Isa 500Imran AsgharNo ratings yet

- PPDocument9 pagesPPEmmylouCasanovaNo ratings yet

- Brochure-Future and Option Trading StrategiesDocument6 pagesBrochure-Future and Option Trading StrategiesfnopulseNo ratings yet

- Project Report On Air IndiaDocument33 pagesProject Report On Air IndiaHitesh MoreNo ratings yet

- Relative VolumeDocument13 pagesRelative Volumevishnuvardhanreddy4uNo ratings yet

- Chapter5 InflationTaxDocument17 pagesChapter5 InflationTaxadamNo ratings yet

- Model SOP 2018Document354 pagesModel SOP 2018Lakshmi VishwanathanNo ratings yet

- DPR Format SipbDocument6 pagesDPR Format SipbNet PlaZaNo ratings yet

- WoolworthsGroupLimited HubParliamentStationPtyLtd TI 100000001488833 INV438272Document2 pagesWoolworthsGroupLimited HubParliamentStationPtyLtd TI 100000001488833 INV438272Axel TuohyNo ratings yet

- Financial Analysis Report OGDCLDocument16 pagesFinancial Analysis Report OGDCLRaza SohailNo ratings yet

- الفروقات المؤقتة ومحاسبة الضريبة المؤجلة في الشركات الفردية وفق النظام المحاسبي الماليDocument18 pagesالفروقات المؤقتة ومحاسبة الضريبة المؤجلة في الشركات الفردية وفق النظام المحاسبي الماليRime KessiraNo ratings yet

- 20 Venture Capital Advantages and DisadvantagesDocument9 pages20 Venture Capital Advantages and DisadvantagesFrancis BellidoNo ratings yet

- Gasbill 5568246016 202112 20211228191312Document1 pageGasbill 5568246016 202112 20211228191312ahmedNo ratings yet

- Expanding Branches of Commercial Bank ofDocument5 pagesExpanding Branches of Commercial Bank ofsi labNo ratings yet

- Econ 1042 Macroeconomics 2 Sem 1 2007 Final Examination Draft CDocument12 pagesEcon 1042 Macroeconomics 2 Sem 1 2007 Final Examination Draft CDoong YeeJiun0% (1)

- Warren Buffet BiographyDocument8 pagesWarren Buffet BiographyMark allenNo ratings yet

- Api 2201Document13 pagesApi 2201Cesar Kv RangelNo ratings yet

- Assignment 3, International Banking Shafiqullah, Reg No, Su-17-01-021-001, Bba 8th.Document5 pagesAssignment 3, International Banking Shafiqullah, Reg No, Su-17-01-021-001, Bba 8th.Shafiq UllahNo ratings yet

- 111 Test Bank For Cost Management Measuring Monitoring and Motivating Performance 2nd EditionDocument28 pages111 Test Bank For Cost Management Measuring Monitoring and Motivating Performance 2nd EditionEbook free100% (1)

- Aa1 3 2024Document39 pagesAa1 3 2024esratbithikaNo ratings yet

Download as ppt, pdf, or txt

You might also like

- Stern Strategy EssentialsDocument121 pagesStern Strategy Essentialssatya324100% (3)

- Case Submission - Stone Container Corporation (A) ' Group VIIIDocument5 pagesCase Submission - Stone Container Corporation (A) ' Group VIIIGURNEET KAURNo ratings yet

- Implementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesFrom EverandImplementing Integrated Business Planning: A Guide Exemplified With Process Context and SAP IBP Use CasesNo ratings yet

- Revenue Recognition: With SAP S/4HANA Cloud in The Context of IFRS15/ASC606Document35 pagesRevenue Recognition: With SAP S/4HANA Cloud in The Context of IFRS15/ASC606m_casavecchiaNo ratings yet

- Final Exam Financial MarketsDocument9 pagesFinal Exam Financial MarketsLorielyn Mae SalcedoNo ratings yet

- Union Gaming Feasibility StudyDocument51 pagesUnion Gaming Feasibility StudyAnn DwyerNo ratings yet

- GM Andean Accounts Payable Workshop v1 April09Document18 pagesGM Andean Accounts Payable Workshop v1 April09Subbireddy ChintapalliNo ratings yet

- Sap Finance OverviewDocument45 pagesSap Finance Overviewprat05No ratings yet

- Introduction To SAPDocument60 pagesIntroduction To SAPAnonymous aX3l06L5eNo ratings yet

- SAP OverviewDocument36 pagesSAP OverviewsivakumarNo ratings yet

- Introduction To ERPDocument24 pagesIntroduction To ERPAbdul WahabNo ratings yet

- Evaluated Receipt Settlement Sap PDFDocument2 pagesEvaluated Receipt Settlement Sap PDFTim0% (2)

- Lockbox BAI2 Layout With SAPDocument14 pagesLockbox BAI2 Layout With SAPMafia333No ratings yet

- Truebell - Fin - Ap - Config - Account PayableDocument49 pagesTruebell - Fin - Ap - Config - Account PayableRajesh ChowdaryNo ratings yet

- Sap Fi S4 Hana Asset Accounting Part 1Document6 pagesSap Fi S4 Hana Asset Accounting Part 1NASEER ULLAHNo ratings yet

- Day1 - Introduction To SAP FICODocument37 pagesDay1 - Introduction To SAP FICOankitavengNo ratings yet

- HSPL Fi 06 House Bank v1.0Document18 pagesHSPL Fi 06 House Bank v1.0Naveen KumarNo ratings yet

- Business Processes Master List Financial Accounting & ControllingDocument21 pagesBusiness Processes Master List Financial Accounting & ControllingPrathamesh ParkerNo ratings yet

- Chapter 29 SAP Databse Tables-1Document20 pagesChapter 29 SAP Databse Tables-1zachary kehoeNo ratings yet

- Sapbrainsonline Com Help FSCM Module Tutorials HTMLDocument8 pagesSapbrainsonline Com Help FSCM Module Tutorials HTMLCarlos CasañoNo ratings yet

- SAP CO CookbookDocument129 pagesSAP CO CookbookMisbah FatimaNo ratings yet

- SRI RUDRAM With MeaningDocument73 pagesSRI RUDRAM With Meaningsreelatha1No ratings yet

- AC206 Parallel Valuation and Financial Reporting: Local Law - IAS (IFRS) / US-GAAP?Document6 pagesAC206 Parallel Valuation and Financial Reporting: Local Law - IAS (IFRS) / US-GAAP?mhku1No ratings yet

- 2016 05 Spring Catalog SAP-PRESS DOWNLOAD PDFDocument32 pages2016 05 Spring Catalog SAP-PRESS DOWNLOAD PDFVitlenNo ratings yet

- Standard SAP Business Process Flow DiagramDocument1 pageStandard SAP Business Process Flow DiagramAjay KumarNo ratings yet

- Table Name: Description Important FieldsDocument5 pagesTable Name: Description Important FieldsJyotiraditya Banerjee100% (1)

- Sap - PDF Catalogue s4Document25 pagesSap - PDF Catalogue s4razatsaxena0% (2)

- Fi-Co SAP Systems Application and Products in Data ProcessingDocument295 pagesFi-Co SAP Systems Application and Products in Data ProcessingPrabhakarNo ratings yet

- SAP CO ECC 6.0 Bootcamp - Day 5Document104 pagesSAP CO ECC 6.0 Bootcamp - Day 5dcanohNo ratings yet

- SAp Testing Part 5Document11 pagesSAp Testing Part 5RajaNo ratings yet

- Fdocuments - in Sap Overview PP PC IntegrationDocument84 pagesFdocuments - in Sap Overview PP PC IntegrationHimanshu SinghNo ratings yet

- SAP Bootcamp Quiz SDDocument47 pagesSAP Bootcamp Quiz SDBeverly GordonNo ratings yet

- Simple Finance - The Convergence of The GL Account and The Cost ElementDocument12 pagesSimple Finance - The Convergence of The GL Account and The Cost Elementjoseph davidNo ratings yet

- Ivend Retail Integration With SapDocument21 pagesIvend Retail Integration With SapniteshNo ratings yet

- BP OP ENTPR S4HANA1909 06 Process-Steps EN USDocument816 pagesBP OP ENTPR S4HANA1909 06 Process-Steps EN USBiji RoyNo ratings yet

- An SAP Consultant - ABAP - Step by Step Tutorial On Smart Forms - Template NodeDocument9 pagesAn SAP Consultant - ABAP - Step by Step Tutorial On Smart Forms - Template NodearunNo ratings yet

- S 4 HanaDocument51 pagesS 4 Hanamannadas206No ratings yet

- SAP Workflow Introduction For PresentationDocument40 pagesSAP Workflow Introduction For PresentationanantdaNo ratings yet

- Inbound Data Flow in SAP Retail EnvironmentDocument3 pagesInbound Data Flow in SAP Retail EnvironmentEklavya BansalNo ratings yet

- Vendor Invoice Booking-MIRODocument5 pagesVendor Invoice Booking-MIROAMIT SAWANTNo ratings yet

- Leveraging S4 AI ML Capabilities 1689177179Document79 pagesLeveraging S4 AI ML Capabilities 1689177179nagarajuNo ratings yet

- Sap Fico Portfolio - Monisha DemarkDocument245 pagesSap Fico Portfolio - Monisha Demarknandhinikrish306No ratings yet

- 011000358700000031292010EDocument74 pages011000358700000031292010Erameshdv9No ratings yet

- Sap Fico Interview QuestionsDocument357 pagesSap Fico Interview QuestionsMohamed Azouggarh100% (1)

- Sap TablesDocument29 pagesSap TablesTest100% (1)

- SAP ERP Solution: FICO-Reconciliation ToolDocument21 pagesSAP ERP Solution: FICO-Reconciliation ToolViivekcanandu MethriNo ratings yet

- JVA-TRN - FI109 - Joint Venture Accounting v1.1Document83 pagesJVA-TRN - FI109 - Joint Venture Accounting v1.1James Anderson Luna SilvaNo ratings yet

- SAP OverviewDocument20 pagesSAP OverviewMarkup QpicNo ratings yet

- SAP FI Ecc X s4Document14 pagesSAP FI Ecc X s4fzankNo ratings yet

- Sap Financial Supply Chain Management (FSCM) : System & Technology Model Finance SSC June 2019Document20 pagesSap Financial Supply Chain Management (FSCM) : System & Technology Model Finance SSC June 2019fadliNo ratings yet

- New Asset AccountingDocument19 pagesNew Asset AccountingShruti ChapraNo ratings yet

- Sap Ariba Create SourcingDocument18 pagesSap Ariba Create SourcingS M SHEKAR AND CONo ratings yet

- Intro ERP Using GBI Slides FI en v2.01Document25 pagesIntro ERP Using GBI Slides FI en v2.01shobhit1980inNo ratings yet

- Hana Sidecar Kuleuven PDFDocument51 pagesHana Sidecar Kuleuven PDFPaul DeleuzeNo ratings yet

- SAP Discovery - Initial Architectural Diagram of SAP Estate v1.0Document3 pagesSAP Discovery - Initial Architectural Diagram of SAP Estate v1.0PulkKit SharMaNo ratings yet

- S4HANA OP 1511 Learning Journey BetaDocument9 pagesS4HANA OP 1511 Learning Journey BetaJorge Santillan0% (1)

- Sales Area: S / 4 HANA ContentDocument34 pagesSales Area: S / 4 HANA ContentEnrique Israel Flores ZúñigaNo ratings yet

- Creating GL AccountsDocument19 pagesCreating GL AccountsJyotiraditya BanerjeeNo ratings yet

- Accrual Engine: Solution Management FinancialsDocument32 pagesAccrual Engine: Solution Management FinancialsateeqbajwaNo ratings yet

- ISU TablesDocument1 pageISU TablesrajusampathiraoNo ratings yet

- Procurement ProcessDocument32 pagesProcurement ProcessAnkit GoyalNo ratings yet

- Building A Tax Calculation ApplicationDocument11 pagesBuilding A Tax Calculation ApplicationMartin De LeoNo ratings yet

- Tender FormDocument7 pagesTender Formaharish_iitkNo ratings yet

- Museums As Participants in The Market Game: The Political and Economic Context of The Functioning of The MuseumsDocument19 pagesMuseums As Participants in The Market Game: The Political and Economic Context of The Functioning of The MuseumsMika FungoNo ratings yet

- Session 18 Securitization of Loans and Other AssetsDocument13 pagesSession 18 Securitization of Loans and Other AssetsNeena TomyNo ratings yet

- 10000027146Document47 pages10000027146Chapter 11 DocketsNo ratings yet

- Payment of Bonus Act, 1965 & The Rules: ChecklistDocument2 pagesPayment of Bonus Act, 1965 & The Rules: ChecklistparavindNo ratings yet

- Taxation - UP 2008Document163 pagesTaxation - UP 2008Martoni SaliendraNo ratings yet

- Audit - Isa 500Document6 pagesAudit - Isa 500Imran AsgharNo ratings yet

- PPDocument9 pagesPPEmmylouCasanovaNo ratings yet

- Brochure-Future and Option Trading StrategiesDocument6 pagesBrochure-Future and Option Trading StrategiesfnopulseNo ratings yet

- Project Report On Air IndiaDocument33 pagesProject Report On Air IndiaHitesh MoreNo ratings yet

- Relative VolumeDocument13 pagesRelative Volumevishnuvardhanreddy4uNo ratings yet

- Chapter5 InflationTaxDocument17 pagesChapter5 InflationTaxadamNo ratings yet

- Model SOP 2018Document354 pagesModel SOP 2018Lakshmi VishwanathanNo ratings yet

- DPR Format SipbDocument6 pagesDPR Format SipbNet PlaZaNo ratings yet

- WoolworthsGroupLimited HubParliamentStationPtyLtd TI 100000001488833 INV438272Document2 pagesWoolworthsGroupLimited HubParliamentStationPtyLtd TI 100000001488833 INV438272Axel TuohyNo ratings yet

- Financial Analysis Report OGDCLDocument16 pagesFinancial Analysis Report OGDCLRaza SohailNo ratings yet

- الفروقات المؤقتة ومحاسبة الضريبة المؤجلة في الشركات الفردية وفق النظام المحاسبي الماليDocument18 pagesالفروقات المؤقتة ومحاسبة الضريبة المؤجلة في الشركات الفردية وفق النظام المحاسبي الماليRime KessiraNo ratings yet

- 20 Venture Capital Advantages and DisadvantagesDocument9 pages20 Venture Capital Advantages and DisadvantagesFrancis BellidoNo ratings yet

- Gasbill 5568246016 202112 20211228191312Document1 pageGasbill 5568246016 202112 20211228191312ahmedNo ratings yet

- Expanding Branches of Commercial Bank ofDocument5 pagesExpanding Branches of Commercial Bank ofsi labNo ratings yet

- Econ 1042 Macroeconomics 2 Sem 1 2007 Final Examination Draft CDocument12 pagesEcon 1042 Macroeconomics 2 Sem 1 2007 Final Examination Draft CDoong YeeJiun0% (1)

- Warren Buffet BiographyDocument8 pagesWarren Buffet BiographyMark allenNo ratings yet

- Api 2201Document13 pagesApi 2201Cesar Kv RangelNo ratings yet

- Assignment 3, International Banking Shafiqullah, Reg No, Su-17-01-021-001, Bba 8th.Document5 pagesAssignment 3, International Banking Shafiqullah, Reg No, Su-17-01-021-001, Bba 8th.Shafiq UllahNo ratings yet

- 111 Test Bank For Cost Management Measuring Monitoring and Motivating Performance 2nd EditionDocument28 pages111 Test Bank For Cost Management Measuring Monitoring and Motivating Performance 2nd EditionEbook free100% (1)

- Aa1 3 2024Document39 pagesAa1 3 2024esratbithikaNo ratings yet