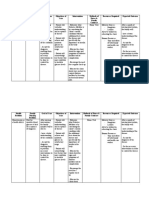

Various Investment Categories

Various Investment Categories

You might also like

- Gone With The Wind ScriptDocument71 pagesGone With The Wind ScriptRafael Aleman0% (1)

- Filipino: Ikalawang Markahan - Modyul 13Document23 pagesFilipino: Ikalawang Markahan - Modyul 13Libert Moore Omambat Betita100% (2)

- Commentary of Nussbaum's Compassion and TerrorDocument3 pagesCommentary of Nussbaum's Compassion and TerrorJacob Clift100% (1)

- Investmentalternatives 090320222238 Phpapp02Document16 pagesInvestmentalternatives 090320222238 Phpapp02sarathyy09No ratings yet

- Mutual Funds: PRENTENED BY:-Sher Singh Pradeep KumarDocument18 pagesMutual Funds: PRENTENED BY:-Sher Singh Pradeep Kumarsherrysingh44No ratings yet

- InvestmentDocument5 pagesInvestmentDen Mark AlbayNo ratings yet

- Investment Alternatives - Negotiable and Non-Negotiable InstrumentsDocument7 pagesInvestment Alternatives - Negotiable and Non-Negotiable InstrumentsAvinash KumarNo ratings yet

- Investment Alternatives - Negotiable and Non-Negotiable InstrumentsDocument7 pagesInvestment Alternatives - Negotiable and Non-Negotiable InstrumentsAvinash Kumar100% (1)

- Capital Market: Unit-IDocument17 pagesCapital Market: Unit-IChristine Joy RozanoNo ratings yet

- Mutual Funds: BY: Adneya Audhi Roll: 12304Document20 pagesMutual Funds: BY: Adneya Audhi Roll: 12304Adneya AudhiNo ratings yet

- Investment Law EvolutionDocument39 pagesInvestment Law EvolutionAdarsh RanjanNo ratings yet

- Unit I Supplementary Info Investment AvenuesDocument17 pagesUnit I Supplementary Info Investment AvenuesAmit RoyNo ratings yet

- Unit 4: Investment VehiclesDocument29 pagesUnit 4: Investment Vehiclesworld4meNo ratings yet

- Mutual Funds: Presented By: Group 3 Arnab Moitra Manish Banga Mohit Kapoor Shersingh Bagel Stuti Sethi Sumit DuaDocument32 pagesMutual Funds: Presented By: Group 3 Arnab Moitra Manish Banga Mohit Kapoor Shersingh Bagel Stuti Sethi Sumit DuaMohit KapoorNo ratings yet

- S. S. Dempo College of Commerce and Economics: Banking Isa-2Document20 pagesS. S. Dempo College of Commerce and Economics: Banking Isa-2Karthikeyan MishraNo ratings yet

- Portfolio Management and Investment Alternatives: Shruti ChavarkarDocument17 pagesPortfolio Management and Investment Alternatives: Shruti ChavarkarShrikant SabatNo ratings yet

- Security Analysis and Portfolio Management: UNIT-1Document51 pagesSecurity Analysis and Portfolio Management: UNIT-1Sudha PanneerselvamNo ratings yet

- Benefits of Investment ProductsDocument3 pagesBenefits of Investment ProductsabhishekNo ratings yet

- Report On Investment OptionsDocument8 pagesReport On Investment OptionsParth Ladda100% (1)

- Investment Avenues AssignmentDocument8 pagesInvestment Avenues Assignmentfaisalk95No ratings yet

- Presentation FinDocument24 pagesPresentation FinSagrika SagarNo ratings yet

- INVESTMENTDocument63 pagesINVESTMENTetiNo ratings yet

- Name-Gurpreet Kaur SECTION - R1813 ROLL NO.-B27 Assignment Of-Pfp Submitted To-Mr - Vikas AnandDocument7 pagesName-Gurpreet Kaur SECTION - R1813 ROLL NO.-B27 Assignment Of-Pfp Submitted To-Mr - Vikas AnandPari SiddiqueNo ratings yet

- Loan Against Securities MeaningDocument6 pagesLoan Against Securities MeaningPratik LahotiNo ratings yet

- 3-Notes On Non Banking Products-Part 1Document27 pages3-Notes On Non Banking Products-Part 1Kirti GiyamalaniNo ratings yet

- Mutual Funds in IndiaDocument111 pagesMutual Funds in IndiaJigar JainNo ratings yet

- Mutual FundDocument11 pagesMutual FundAnkush KochharNo ratings yet

- Investment AlternativesDocument19 pagesInvestment AlternativesJagrityTalwarNo ratings yet

- Allied Services - 7Document9 pagesAllied Services - 7asaSNo ratings yet

- Mutual Funds: Prepared by - Pratik MananiDocument29 pagesMutual Funds: Prepared by - Pratik MananimananipratikNo ratings yet

- FEIA 2&5m Question With AnswerDocument5 pagesFEIA 2&5m Question With Answerprashanthuddar6No ratings yet

- Investments - Meaning, Objectives, Features and Various AlternativesDocument4 pagesInvestments - Meaning, Objectives, Features and Various AlternativesKOUJI N. MARQUEZNo ratings yet

- Objective of The Study of Mutual FundsDocument18 pagesObjective of The Study of Mutual FundsdusuuttungNo ratings yet

- Investment Avenues:: Chapter No.2Document12 pagesInvestment Avenues:: Chapter No.2rajaniNo ratings yet

- Mutual Fund - An Introduction: Project Report Submitted by Team B" Name Enrolment Number Roll Number Assigned in MSOPDocument32 pagesMutual Fund - An Introduction: Project Report Submitted by Team B" Name Enrolment Number Roll Number Assigned in MSOPbholagangster1No ratings yet

- Mutual FundsDocument43 pagesMutual FundsAnkur PandeyNo ratings yet

- Types of InvestmentsDocument8 pagesTypes of InvestmentsAnirudh VictorNo ratings yet

- 3.debt - BasicsDocument17 pages3.debt - BasicsDebjani SinghaNo ratings yet

- IM - Unit-3Document25 pagesIM - Unit-3Maddi NikhithaNo ratings yet

- LFS DetailDocument21 pagesLFS DetailChetan LaddhaNo ratings yet

- Assignment FINALDocument7 pagesAssignment FINALPavan HosalliNo ratings yet

- Ca1 Financial MarketsDocument12 pagesCa1 Financial MarketsKartik ChaturvediNo ratings yet

- AbsharDocument23 pagesAbsharAbsharNo ratings yet

- NSDL Update - September 2014 PDFDocument8 pagesNSDL Update - September 2014 PDFveatla2745No ratings yet

- Mutual FundsDocument10 pagesMutual Fundsaltthrowaway747No ratings yet

- Depository Service AND MUTUAL FUNDSDocument40 pagesDepository Service AND MUTUAL FUNDSDasharath Raj UrsNo ratings yet

- Investment Avenues (Securities) in PakistanDocument7 pagesInvestment Avenues (Securities) in PakistanPolite Charm100% (1)

- Task 8 RajatDocument20 pagesTask 8 RajatTeja MullapudiNo ratings yet

- Concept and Role of Mutual FundDocument8 pagesConcept and Role of Mutual FundKhushbu ThakurNo ratings yet

- Financial ManagementDocument13 pagesFinancial ManagementSunny KesarwaniNo ratings yet

- Mutual FundDocument20 pagesMutual FundRupesh KekadeNo ratings yet

- Presented By:-Deepika Sahu Sonika PandeyDocument30 pagesPresented By:-Deepika Sahu Sonika PandeySonika MishraNo ratings yet

- FMM Investment Basics NotesDocument8 pagesFMM Investment Basics NotesBhavesh RajpootNo ratings yet

- Questions and Answers Capital IQDocument28 pagesQuestions and Answers Capital IQrishifiib08100% (1)

- Financial Assets AreDocument5 pagesFinancial Assets AreAllen Immanuel RNo ratings yet

- Mutual FundsDocument91 pagesMutual Fundssanjeev151No ratings yet

- Investing Made Easy: Finding the Right Opportunities for YouFrom EverandInvesting Made Easy: Finding the Right Opportunities for YouNo ratings yet

- Equity Investment for CFA level 1: CFA level 1, #2From EverandEquity Investment for CFA level 1: CFA level 1, #2Rating: 5 out of 5 stars5/5 (1)

- Dividend Investing: Passive Income and Growth Investing for BeginnersFrom EverandDividend Investing: Passive Income and Growth Investing for BeginnersNo ratings yet

- Investing Demystified: A Beginner's Guide to Building Wealth in the Stock MarketFrom EverandInvesting Demystified: A Beginner's Guide to Building Wealth in the Stock MarketNo ratings yet

- Indian Mutual funds for Beginners: A Basic Guide for Beginners to Learn About Mutual Funds in IndiaFrom EverandIndian Mutual funds for Beginners: A Basic Guide for Beginners to Learn About Mutual Funds in IndiaRating: 3.5 out of 5 stars3.5/5 (8)

- FNCPDocument3 pagesFNCPFatima Ysabelle Marie RuizNo ratings yet

- SAP 1 - Law - BCR Answer Key - (24-10-2021)Document13 pagesSAP 1 - Law - BCR Answer Key - (24-10-2021)PradeepNo ratings yet

- Grammar Handbook Parts of SpeechDocument29 pagesGrammar Handbook Parts of SpeechClayton OgilvyNo ratings yet

- Needs Assessment SurveyDocument2 pagesNeeds Assessment SurveyPatrick SanchezNo ratings yet

- ASISC Rules and Regulations For Literary EventsDocument6 pagesASISC Rules and Regulations For Literary EventsSahil PahanNo ratings yet

- Rights of Women in Prison: Addressing Gender IssuesDocument39 pagesRights of Women in Prison: Addressing Gender IssuesUtkarsh JoshiNo ratings yet

- Cost Accounting Quiz No 1docx PDF FreeDocument5 pagesCost Accounting Quiz No 1docx PDF FreeDeryl GalveNo ratings yet

- Estate Tax Problems 2Document5 pagesEstate Tax Problems 2howaanNo ratings yet

- Lexington County School District One LawsuitDocument17 pagesLexington County School District One LawsuitMayra ParrillaNo ratings yet

- Cybernetic GovernanceDocument3 pagesCybernetic Governancesuhajanan16No ratings yet

- Informal Le!er e Mail Template Client Business Email Normal EmailDocument1 pageInformal Le!er e Mail Template Client Business Email Normal EmailJean-Pierre MwananshikuNo ratings yet

- AAMU WDC Alumni Chapter Newsletter - Jan 2011Document16 pagesAAMU WDC Alumni Chapter Newsletter - Jan 2011AAMUAlumniTweetNo ratings yet

- Pseudo Code ExamplesDocument4 pagesPseudo Code ExamplesViji RamNo ratings yet

- Texas v. JohnsonDocument6 pagesTexas v. JohnsonjonnesjogieNo ratings yet

- Factors Affecting Decision 4Document3 pagesFactors Affecting Decision 4p.sankaranarayananNo ratings yet

- Capital District 2022 Dcon Award WinnersDocument3 pagesCapital District 2022 Dcon Award Winnersapi-95653109No ratings yet

- View Invoice - ReceiptDocument1 pageView Invoice - ReceiptashadbolajiNo ratings yet

- GEOG AssignmentDocument14 pagesGEOG AssignmentMuhammad HamzaNo ratings yet

- Inventory Is Considered To Be One of The Most Important Assets of A BusinessDocument3 pagesInventory Is Considered To Be One of The Most Important Assets of A Businesselaiza armeroNo ratings yet

- Rafi Peer Theater Workshop Strategic PlanDocument11 pagesRafi Peer Theater Workshop Strategic PlanRafiq JafferNo ratings yet

- Vedanta Limited Cairn Oil & Gas: Integrated Field Plan Execution Services in Satellite Fields in Rj-On 90/1 BLOCKDocument23 pagesVedanta Limited Cairn Oil & Gas: Integrated Field Plan Execution Services in Satellite Fields in Rj-On 90/1 BLOCKPRAKASH PANDEYNo ratings yet

- Template - Tender Management ProcessDocument9 pagesTemplate - Tender Management ProcessGryswolf0% (1)

- 0025 A (4) C Lawis ST Dela Paz Antipolo June 2, 2022: Business Plan Scallion (Spring Onion) SaladsDocument7 pages0025 A (4) C Lawis ST Dela Paz Antipolo June 2, 2022: Business Plan Scallion (Spring Onion) SaladsCarol Maina100% (1)

- 7nonf ErosianmythDocument255 pages7nonf ErosianmythvivekpatelbiiNo ratings yet

- đề 15Document7 pagesđề 15Thuphuong LeNo ratings yet

- Annales School of History: Its Origins, Development and ContributionsDocument8 pagesAnnales School of History: Its Origins, Development and ContributionsKanchi AgarwalNo ratings yet

- BSP CampDocument7 pagesBSP CampArleneTalledoNo ratings yet

Download as pptx, pdf, or txt

You might also like

- Gone With The Wind ScriptDocument71 pagesGone With The Wind ScriptRafael Aleman0% (1)

- Filipino: Ikalawang Markahan - Modyul 13Document23 pagesFilipino: Ikalawang Markahan - Modyul 13Libert Moore Omambat Betita100% (2)

- Commentary of Nussbaum's Compassion and TerrorDocument3 pagesCommentary of Nussbaum's Compassion and TerrorJacob Clift100% (1)

- Investmentalternatives 090320222238 Phpapp02Document16 pagesInvestmentalternatives 090320222238 Phpapp02sarathyy09No ratings yet

- Mutual Funds: PRENTENED BY:-Sher Singh Pradeep KumarDocument18 pagesMutual Funds: PRENTENED BY:-Sher Singh Pradeep Kumarsherrysingh44No ratings yet

- InvestmentDocument5 pagesInvestmentDen Mark AlbayNo ratings yet

- Investment Alternatives - Negotiable and Non-Negotiable InstrumentsDocument7 pagesInvestment Alternatives - Negotiable and Non-Negotiable InstrumentsAvinash KumarNo ratings yet

- Investment Alternatives - Negotiable and Non-Negotiable InstrumentsDocument7 pagesInvestment Alternatives - Negotiable and Non-Negotiable InstrumentsAvinash Kumar100% (1)

- Capital Market: Unit-IDocument17 pagesCapital Market: Unit-IChristine Joy RozanoNo ratings yet

- Mutual Funds: BY: Adneya Audhi Roll: 12304Document20 pagesMutual Funds: BY: Adneya Audhi Roll: 12304Adneya AudhiNo ratings yet

- Investment Law EvolutionDocument39 pagesInvestment Law EvolutionAdarsh RanjanNo ratings yet

- Unit I Supplementary Info Investment AvenuesDocument17 pagesUnit I Supplementary Info Investment AvenuesAmit RoyNo ratings yet

- Unit 4: Investment VehiclesDocument29 pagesUnit 4: Investment Vehiclesworld4meNo ratings yet

- Mutual Funds: Presented By: Group 3 Arnab Moitra Manish Banga Mohit Kapoor Shersingh Bagel Stuti Sethi Sumit DuaDocument32 pagesMutual Funds: Presented By: Group 3 Arnab Moitra Manish Banga Mohit Kapoor Shersingh Bagel Stuti Sethi Sumit DuaMohit KapoorNo ratings yet

- S. S. Dempo College of Commerce and Economics: Banking Isa-2Document20 pagesS. S. Dempo College of Commerce and Economics: Banking Isa-2Karthikeyan MishraNo ratings yet

- Portfolio Management and Investment Alternatives: Shruti ChavarkarDocument17 pagesPortfolio Management and Investment Alternatives: Shruti ChavarkarShrikant SabatNo ratings yet

- Security Analysis and Portfolio Management: UNIT-1Document51 pagesSecurity Analysis and Portfolio Management: UNIT-1Sudha PanneerselvamNo ratings yet

- Benefits of Investment ProductsDocument3 pagesBenefits of Investment ProductsabhishekNo ratings yet

- Report On Investment OptionsDocument8 pagesReport On Investment OptionsParth Ladda100% (1)

- Investment Avenues AssignmentDocument8 pagesInvestment Avenues Assignmentfaisalk95No ratings yet

- Presentation FinDocument24 pagesPresentation FinSagrika SagarNo ratings yet

- INVESTMENTDocument63 pagesINVESTMENTetiNo ratings yet

- Name-Gurpreet Kaur SECTION - R1813 ROLL NO.-B27 Assignment Of-Pfp Submitted To-Mr - Vikas AnandDocument7 pagesName-Gurpreet Kaur SECTION - R1813 ROLL NO.-B27 Assignment Of-Pfp Submitted To-Mr - Vikas AnandPari SiddiqueNo ratings yet

- Loan Against Securities MeaningDocument6 pagesLoan Against Securities MeaningPratik LahotiNo ratings yet

- 3-Notes On Non Banking Products-Part 1Document27 pages3-Notes On Non Banking Products-Part 1Kirti GiyamalaniNo ratings yet

- Mutual Funds in IndiaDocument111 pagesMutual Funds in IndiaJigar JainNo ratings yet

- Mutual FundDocument11 pagesMutual FundAnkush KochharNo ratings yet

- Investment AlternativesDocument19 pagesInvestment AlternativesJagrityTalwarNo ratings yet

- Allied Services - 7Document9 pagesAllied Services - 7asaSNo ratings yet

- Mutual Funds: Prepared by - Pratik MananiDocument29 pagesMutual Funds: Prepared by - Pratik MananimananipratikNo ratings yet

- FEIA 2&5m Question With AnswerDocument5 pagesFEIA 2&5m Question With Answerprashanthuddar6No ratings yet

- Investments - Meaning, Objectives, Features and Various AlternativesDocument4 pagesInvestments - Meaning, Objectives, Features and Various AlternativesKOUJI N. MARQUEZNo ratings yet

- Objective of The Study of Mutual FundsDocument18 pagesObjective of The Study of Mutual FundsdusuuttungNo ratings yet

- Investment Avenues:: Chapter No.2Document12 pagesInvestment Avenues:: Chapter No.2rajaniNo ratings yet

- Mutual Fund - An Introduction: Project Report Submitted by Team B" Name Enrolment Number Roll Number Assigned in MSOPDocument32 pagesMutual Fund - An Introduction: Project Report Submitted by Team B" Name Enrolment Number Roll Number Assigned in MSOPbholagangster1No ratings yet

- Mutual FundsDocument43 pagesMutual FundsAnkur PandeyNo ratings yet

- Types of InvestmentsDocument8 pagesTypes of InvestmentsAnirudh VictorNo ratings yet

- 3.debt - BasicsDocument17 pages3.debt - BasicsDebjani SinghaNo ratings yet

- IM - Unit-3Document25 pagesIM - Unit-3Maddi NikhithaNo ratings yet

- LFS DetailDocument21 pagesLFS DetailChetan LaddhaNo ratings yet

- Assignment FINALDocument7 pagesAssignment FINALPavan HosalliNo ratings yet

- Ca1 Financial MarketsDocument12 pagesCa1 Financial MarketsKartik ChaturvediNo ratings yet

- AbsharDocument23 pagesAbsharAbsharNo ratings yet

- NSDL Update - September 2014 PDFDocument8 pagesNSDL Update - September 2014 PDFveatla2745No ratings yet

- Mutual FundsDocument10 pagesMutual Fundsaltthrowaway747No ratings yet

- Depository Service AND MUTUAL FUNDSDocument40 pagesDepository Service AND MUTUAL FUNDSDasharath Raj UrsNo ratings yet

- Investment Avenues (Securities) in PakistanDocument7 pagesInvestment Avenues (Securities) in PakistanPolite Charm100% (1)

- Task 8 RajatDocument20 pagesTask 8 RajatTeja MullapudiNo ratings yet

- Concept and Role of Mutual FundDocument8 pagesConcept and Role of Mutual FundKhushbu ThakurNo ratings yet

- Financial ManagementDocument13 pagesFinancial ManagementSunny KesarwaniNo ratings yet

- Mutual FundDocument20 pagesMutual FundRupesh KekadeNo ratings yet

- Presented By:-Deepika Sahu Sonika PandeyDocument30 pagesPresented By:-Deepika Sahu Sonika PandeySonika MishraNo ratings yet

- FMM Investment Basics NotesDocument8 pagesFMM Investment Basics NotesBhavesh RajpootNo ratings yet

- Questions and Answers Capital IQDocument28 pagesQuestions and Answers Capital IQrishifiib08100% (1)

- Financial Assets AreDocument5 pagesFinancial Assets AreAllen Immanuel RNo ratings yet

- Mutual FundsDocument91 pagesMutual Fundssanjeev151No ratings yet

- Investing Made Easy: Finding the Right Opportunities for YouFrom EverandInvesting Made Easy: Finding the Right Opportunities for YouNo ratings yet

- Equity Investment for CFA level 1: CFA level 1, #2From EverandEquity Investment for CFA level 1: CFA level 1, #2Rating: 5 out of 5 stars5/5 (1)

- Dividend Investing: Passive Income and Growth Investing for BeginnersFrom EverandDividend Investing: Passive Income and Growth Investing for BeginnersNo ratings yet

- Investing Demystified: A Beginner's Guide to Building Wealth in the Stock MarketFrom EverandInvesting Demystified: A Beginner's Guide to Building Wealth in the Stock MarketNo ratings yet

- Indian Mutual funds for Beginners: A Basic Guide for Beginners to Learn About Mutual Funds in IndiaFrom EverandIndian Mutual funds for Beginners: A Basic Guide for Beginners to Learn About Mutual Funds in IndiaRating: 3.5 out of 5 stars3.5/5 (8)

- FNCPDocument3 pagesFNCPFatima Ysabelle Marie RuizNo ratings yet

- SAP 1 - Law - BCR Answer Key - (24-10-2021)Document13 pagesSAP 1 - Law - BCR Answer Key - (24-10-2021)PradeepNo ratings yet

- Grammar Handbook Parts of SpeechDocument29 pagesGrammar Handbook Parts of SpeechClayton OgilvyNo ratings yet

- Needs Assessment SurveyDocument2 pagesNeeds Assessment SurveyPatrick SanchezNo ratings yet

- ASISC Rules and Regulations For Literary EventsDocument6 pagesASISC Rules and Regulations For Literary EventsSahil PahanNo ratings yet

- Rights of Women in Prison: Addressing Gender IssuesDocument39 pagesRights of Women in Prison: Addressing Gender IssuesUtkarsh JoshiNo ratings yet

- Cost Accounting Quiz No 1docx PDF FreeDocument5 pagesCost Accounting Quiz No 1docx PDF FreeDeryl GalveNo ratings yet

- Estate Tax Problems 2Document5 pagesEstate Tax Problems 2howaanNo ratings yet

- Lexington County School District One LawsuitDocument17 pagesLexington County School District One LawsuitMayra ParrillaNo ratings yet

- Cybernetic GovernanceDocument3 pagesCybernetic Governancesuhajanan16No ratings yet

- Informal Le!er e Mail Template Client Business Email Normal EmailDocument1 pageInformal Le!er e Mail Template Client Business Email Normal EmailJean-Pierre MwananshikuNo ratings yet

- AAMU WDC Alumni Chapter Newsletter - Jan 2011Document16 pagesAAMU WDC Alumni Chapter Newsletter - Jan 2011AAMUAlumniTweetNo ratings yet

- Pseudo Code ExamplesDocument4 pagesPseudo Code ExamplesViji RamNo ratings yet

- Texas v. JohnsonDocument6 pagesTexas v. JohnsonjonnesjogieNo ratings yet

- Factors Affecting Decision 4Document3 pagesFactors Affecting Decision 4p.sankaranarayananNo ratings yet

- Capital District 2022 Dcon Award WinnersDocument3 pagesCapital District 2022 Dcon Award Winnersapi-95653109No ratings yet

- View Invoice - ReceiptDocument1 pageView Invoice - ReceiptashadbolajiNo ratings yet

- GEOG AssignmentDocument14 pagesGEOG AssignmentMuhammad HamzaNo ratings yet

- Inventory Is Considered To Be One of The Most Important Assets of A BusinessDocument3 pagesInventory Is Considered To Be One of The Most Important Assets of A Businesselaiza armeroNo ratings yet

- Rafi Peer Theater Workshop Strategic PlanDocument11 pagesRafi Peer Theater Workshop Strategic PlanRafiq JafferNo ratings yet

- Vedanta Limited Cairn Oil & Gas: Integrated Field Plan Execution Services in Satellite Fields in Rj-On 90/1 BLOCKDocument23 pagesVedanta Limited Cairn Oil & Gas: Integrated Field Plan Execution Services in Satellite Fields in Rj-On 90/1 BLOCKPRAKASH PANDEYNo ratings yet

- Template - Tender Management ProcessDocument9 pagesTemplate - Tender Management ProcessGryswolf0% (1)

- 0025 A (4) C Lawis ST Dela Paz Antipolo June 2, 2022: Business Plan Scallion (Spring Onion) SaladsDocument7 pages0025 A (4) C Lawis ST Dela Paz Antipolo June 2, 2022: Business Plan Scallion (Spring Onion) SaladsCarol Maina100% (1)

- 7nonf ErosianmythDocument255 pages7nonf ErosianmythvivekpatelbiiNo ratings yet

- đề 15Document7 pagesđề 15Thuphuong LeNo ratings yet

- Annales School of History: Its Origins, Development and ContributionsDocument8 pagesAnnales School of History: Its Origins, Development and ContributionsKanchi AgarwalNo ratings yet

- BSP CampDocument7 pagesBSP CampArleneTalledoNo ratings yet