Download as ppt, pdf, or txt

You might also like

- Business Feasibility Study Example of Table of ContentsDocument1 pageBusiness Feasibility Study Example of Table of ContentsShed100% (1)

- Am PDFDocument212 pagesAm PDFBrian Careel100% (1)

- 2020 Proteus Offshore, LLC Form 1065 Partnerships Tax Return - FilingDocument17 pages2020 Proteus Offshore, LLC Form 1065 Partnerships Tax Return - FilingPeter Kitchen100% (2)

- 45 CFDS Case Study Is Amazon A MonopolyDocument24 pages45 CFDS Case Study Is Amazon A MonopolyFahrayza RidzkyNo ratings yet

- Module 10 - SAVANT FrameworkDocument17 pagesModule 10 - SAVANT FrameworkAlice Wu100% (3)

- Fábio Luiz de Oliveira Rosa: Social EntrepreneurDocument26 pagesFábio Luiz de Oliveira Rosa: Social EntrepreneurAdam GonnermanNo ratings yet

- 250 High CPC Adsene Ad Network Lists-Technical24x7Document5 pages250 High CPC Adsene Ad Network Lists-Technical24x7Shubham Singh Mehra0% (1)

- Inventories: Student VersionDocument48 pagesInventories: Student VersionShahzad RashidNo ratings yet

- Job Order Costing: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityDocument78 pagesJob Order Costing: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityDiola QuilingNo ratings yet

- Receivables: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityDocument72 pagesReceivables: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityAlice WuNo ratings yet

- JOURNALIZINGDocument50 pagesJOURNALIZINGFely MaataNo ratings yet

- CH 6 Accounting For Merchandising Businesses 2 2Document68 pagesCH 6 Accounting For Merchandising Businesses 2 2CLarens MaraniNo ratings yet

- Accounting Systems: Student VersionDocument45 pagesAccounting Systems: Student VersionShahzad RashidNo ratings yet

- The Adjusting Process: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityDocument52 pagesThe Adjusting Process: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityJuan Dela CruzNo ratings yet

- 02 Analyzing TransactionsDocument56 pages02 Analyzing TransactionsIra CuñadoNo ratings yet

- CH 6 Accounting For Merchandising BusinessesDocument68 pagesCH 6 Accounting For Merchandising BusinessesSimbolon YehezkielNo ratings yet

- Analyzing Transactions: Student VersionDocument56 pagesAnalyzing Transactions: Student VersionTrần AnhNo ratings yet

- CH 1 Introduction To Accounting and BusinessDocument48 pagesCH 1 Introduction To Accounting and BusinessSimbolon YehezkielNo ratings yet

- WRD 24e LecturePPTs Ch01 SV FinalDocument45 pagesWRD 24e LecturePPTs Ch01 SV FinalArfini LestariNo ratings yet

- Completing The Accounting Cycle: Student VersionDocument49 pagesCompleting The Accounting Cycle: Student VersionTarek MadanatNo ratings yet

- CH 12 Accounting For Partnerships and Limited Liability CompaniesDocument54 pagesCH 12 Accounting For Partnerships and Limited Liability CompaniesRiza SyafrieNo ratings yet

- Absorption and Variable Costing, and Inventory Management: Cornerstones of Managerial Accounting, 4eDocument46 pagesAbsorption and Variable Costing, and Inventory Management: Cornerstones of Managerial Accounting, 4eFahad Dahir AbukarNo ratings yet

- Statement of Cash Flows: Student VersionDocument48 pagesStatement of Cash Flows: Student Versionjacks ocNo ratings yet

- Accounting For Merchandising BusinessesDocument132 pagesAccounting For Merchandising BusinessesAlice WuNo ratings yet

- Accounting Systems: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityDocument90 pagesAccounting Systems: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityAlice WuNo ratings yet

- Chapter 5 Worsheet 2Document89 pagesChapter 5 Worsheet 2kakaoNo ratings yet

- Absorption and Variable Costing, and Inventory ManagementDocument46 pagesAbsorption and Variable Costing, and Inventory Managementtira sundayNo ratings yet

- Job Order Costing: Cost Accounting Principles, 8eDocument17 pagesJob Order Costing: Cost Accounting Principles, 8eYan KimNo ratings yet

- Job Order Costing: Principles of Managerial AccountingDocument80 pagesJob Order Costing: Principles of Managerial AccountingLucy UnNo ratings yet

- The Adjusting Process: Student VersionDocument41 pagesThe Adjusting Process: Student VersionTarek MadanatNo ratings yet

- Financial Accounting - Chapter 8Document70 pagesFinancial Accounting - Chapter 8Hamza PagaNo ratings yet

- Analyzing Transactions: Student VersionDocument54 pagesAnalyzing Transactions: Student VersionTarek MadanatNo ratings yet

- Cornerstones: of Managerial Accounting, 5eDocument33 pagesCornerstones: of Managerial Accounting, 5eTasya AgustinaNo ratings yet

- Activity-Based Costing and Management: Managerial Accounting: The Cornerstone of Business Decisions, 4eDocument60 pagesActivity-Based Costing and Management: Managerial Accounting: The Cornerstone of Business Decisions, 4etira sundayNo ratings yet

- Performance Evaluation Using Variances From Standard Costs: BudgetingDocument82 pagesPerformance Evaluation Using Variances From Standard Costs: BudgetingfkarenNo ratings yet

- Cornerstones of Cost Management, 3E: Hansen/MowenDocument48 pagesCornerstones of Cost Management, 3E: Hansen/Mowenfauziah06No ratings yet

- Presentation FilesDocument41 pagesPresentation FilesShahzad RashidNo ratings yet

- Topic 6 Introduction To CostDocument34 pagesTopic 6 Introduction To CostChristopher De GuzmanNo ratings yet

- Financial Accounting - Chapter 11Document80 pagesFinancial Accounting - Chapter 11Hamza PagaNo ratings yet

- CH 8 Abs-Var Costing & Inv MNGTDocument21 pagesCH 8 Abs-Var Costing & Inv MNGTfifiNo ratings yet

- Cost Allocation and Activity-Based Costing: Principles of Managerial AccountingDocument64 pagesCost Allocation and Activity-Based Costing: Principles of Managerial AccountingLucy UnNo ratings yet

- Chapter 1Document45 pagesChapter 1harpadgeorgetaNo ratings yet

- Introduction To Cost AccountingDocument19 pagesIntroduction To Cost Accountingsophia chuaNo ratings yet

- Sarbanes-Oxley, Internal Control, and Cash: Student VersionDocument47 pagesSarbanes-Oxley, Internal Control, and Cash: Student VersionTarek MadanatNo ratings yet

- ACCT230 Ch7Document60 pagesACCT230 Ch7Said MohamedNo ratings yet

- Fraud Examination, 4E: Chapter 5: Recognizing The Symptoms of FraudDocument27 pagesFraud Examination, 4E: Chapter 5: Recognizing The Symptoms of FraudAudrey NathasyaNo ratings yet

- Financial Statement Fraud: Albrecht, Albrecht, Albrecht, ZimbelmanDocument34 pagesFinancial Statement Fraud: Albrecht, Albrecht, Albrecht, ZimbelmanZainab AlhashimNo ratings yet

- Ch32 presentationMEeDocument47 pagesCh32 presentationMEeAhmed GamalNo ratings yet

- Lean AccountingDocument42 pagesLean AccountingAmamore Lorenzana PlazaNo ratings yet

- Performance Evaluation For Decentralized Operations: Principles of Managerial AccountingDocument75 pagesPerformance Evaluation For Decentralized Operations: Principles of Managerial AccountingLucy UnNo ratings yet

- Process Cost Systems: Principles of Managerial AccountingDocument100 pagesProcess Cost Systems: Principles of Managerial AccountingLucy UnNo ratings yet

- Cost Management For Just-in-Time Environments: Principles of Managerial AccountingDocument74 pagesCost Management For Just-in-Time Environments: Principles of Managerial AccountingfkarenNo ratings yet

- International Financial Management Abridged 10 Edition: by Jeff MaduraDocument11 pagesInternational Financial Management Abridged 10 Edition: by Jeff MaduraHiếu Nhi TrịnhNo ratings yet

- Job Order Costing: Cost Accounting: Foundations and Evolutions, 8eDocument34 pagesJob Order Costing: Cost Accounting: Foundations and Evolutions, 8eFrl RizalNo ratings yet

- Semana 15 - Capitulo 24 Medición Del Costo de VidaDocument42 pagesSemana 15 - Capitulo 24 Medición Del Costo de Vidacarlosvasd8No ratings yet

- MA - 5e - PPT - CH 13 - SE SHORT RUN DECISION MAKING RELEVANT COSTINGDocument32 pagesMA - 5e - PPT - CH 13 - SE SHORT RUN DECISION MAKING RELEVANT COSTINGOksigeny GirlsNo ratings yet

- Flexible Budgets and Overhead AnalysisDocument33 pagesFlexible Budgets and Overhead AnalysisKyla RodriguezaNo ratings yet

- Cost Terminology and Cost Behaviors: Cost Accounting: Foundations & Evolutions, 8eDocument19 pagesCost Terminology and Cost Behaviors: Cost Accounting: Foundations & Evolutions, 8eMa Ac SitacaNo ratings yet

- Performance Evaluation Using Variances From Standard Costs: BudgetingDocument82 pagesPerformance Evaluation Using Variances From Standard Costs: BudgetingLucy UnNo ratings yet

- Managerail Accounting Variance Analysis 4 - 5e - PPT - Ch10 - STD CostDocument69 pagesManagerail Accounting Variance Analysis 4 - 5e - PPT - Ch10 - STD CostMahardhika KusumaNo ratings yet

- Strategic Leadership: Managing The Strategy-Making Process For Competitive AdvantageDocument34 pagesStrategic Leadership: Managing The Strategy-Making Process For Competitive AdvantageRohith NNo ratings yet

- W01. Ch01-PresentationDocument37 pagesW01. Ch01-Presentationtomec72872No ratings yet

- Raiborn Kinney On Joint CostsDocument18 pagesRaiborn Kinney On Joint CostsClrk RoxassNo ratings yet

- Lect 1BDocument32 pagesLect 1BjitenreddylawlbsNo ratings yet

- Financial Accounting - Chapter 2Document46 pagesFinancial Accounting - Chapter 2Hamza PagaNo ratings yet

- Standard Costing: A Managerial Control Tool: Cornerstones of Managerial Accounting, 6eDocument91 pagesStandard Costing: A Managerial Control Tool: Cornerstones of Managerial Accounting, 6esamuel tjandraNo ratings yet

- Selenium Testing Tools Interview Questions You'll Most Likely Be Asked: Second EditionFrom EverandSelenium Testing Tools Interview Questions You'll Most Likely Be Asked: Second EditionNo ratings yet

- Accounting For Merchandising BusinessesDocument132 pagesAccounting For Merchandising BusinessesAlice WuNo ratings yet

- Current Liabilities and Payroll: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityDocument85 pagesCurrent Liabilities and Payroll: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityAlice WuNo ratings yet

- Receivables: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityDocument72 pagesReceivables: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityAlice WuNo ratings yet

- Accounting Systems: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityDocument90 pagesAccounting Systems: Prepared By: C. Douglas Cloud Professor Emeritus of Accounting Pepperdine UniversityAlice WuNo ratings yet

- CH 7 Accounting For Issuance of Shares of Stocks 1Document80 pagesCH 7 Accounting For Issuance of Shares of Stocks 1Alice WuNo ratings yet

- Garrison CH06 AccessibleDocument74 pagesGarrison CH06 AccessibleAlice WuNo ratings yet

- Audit of PPE Comprehensive QuizzerDocument9 pagesAudit of PPE Comprehensive QuizzerAlice WuNo ratings yet

- Module 9 - Basic Principles of Tax PlanningDocument15 pagesModule 9 - Basic Principles of Tax PlanningAlice WuNo ratings yet

- Value Added Tax (VAT) : Sec. 105 To 115Document52 pagesValue Added Tax (VAT) : Sec. 105 To 115Alice WuNo ratings yet

- Problem On OPTDocument12 pagesProblem On OPTAlice Wu100% (1)

- Excel Solution For Admission by Investment and WithdrawalDocument7 pagesExcel Solution For Admission by Investment and WithdrawalAlice WuNo ratings yet

- BADVAC2X - MOD 1 Partnership FormationDocument4 pagesBADVAC2X - MOD 1 Partnership FormationAlice WuNo ratings yet

- Chapter 1 Aud TheoDocument37 pagesChapter 1 Aud TheoAlice WuNo ratings yet

- Forex StrategiesDocument5 pagesForex StrategiesumareemooserNo ratings yet

- Index NumbersDocument6 pagesIndex Numberskaziba stephenNo ratings yet

- Sample Agency AgreementDocument4 pagesSample Agency AgreementLuis F. BensimonNo ratings yet

- A Project On Whistle Blowing (Business Ethics)Document14 pagesA Project On Whistle Blowing (Business Ethics)Kiran moreNo ratings yet

- Starting A Bookkeeping Business1Document14 pagesStarting A Bookkeeping Business1Prisca Tembo100% (4)

- Prefill 2019Document2 pagesPrefill 2019Usama AshfaqNo ratings yet

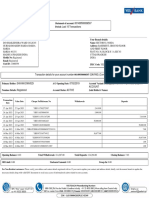

- Account Statement Last 10 TransactionsDocument2 pagesAccount Statement Last 10 TransactionsAshish kumarNo ratings yet

- Assessing The Effectiveness of Accounting Information Systems in The Era of COVID-19 Pandemic (Al-Okaily, 2021)Document19 pagesAssessing The Effectiveness of Accounting Information Systems in The Era of COVID-19 Pandemic (Al-Okaily, 2021)Will TannerNo ratings yet

- Chapter 1editedDocument13 pagesChapter 1editedMuktar jiboNo ratings yet

- Company Law - II "Intellectual Property Issues in Pharmaceutical Industries in Merger and Acquisition - A Critical Analysis"Document23 pagesCompany Law - II "Intellectual Property Issues in Pharmaceutical Industries in Merger and Acquisition - A Critical Analysis"devvrat garhwalNo ratings yet

- LL Material PDFDocument326 pagesLL Material PDFChintakayala SaikrishnaNo ratings yet

- Tds On Provison of Expenses (Tax Gls Open For Direct Manual Posting On 17.04.23 & 18.04.23 Only by Corporate Office) Urgent & Statuary ComplianceDocument1 pageTds On Provison of Expenses (Tax Gls Open For Direct Manual Posting On 17.04.23 & 18.04.23 Only by Corporate Office) Urgent & Statuary ComplianceArvind Kumar GuptaNo ratings yet

- Week 4Document41 pagesWeek 4flora tasiNo ratings yet

- 05 - Labour Law Trade UnionDocument3 pages05 - Labour Law Trade UnionBhavya RayalaNo ratings yet

- 06.17.2021-2021-List of ClientDocument14 pages06.17.2021-2021-List of ClientAntonio NoblezaNo ratings yet

- Amazon's Alexa Spaghetti StrategyDocument10 pagesAmazon's Alexa Spaghetti StrategyShubham SinghNo ratings yet

- Summary of The Secrets To Power Negotiating: by Roger Dawson Presented by Dan O WalkerDocument29 pagesSummary of The Secrets To Power Negotiating: by Roger Dawson Presented by Dan O WalkerEdy Suranta S MahaNo ratings yet

- MGT 162 Group Assignments 25Document20 pagesMGT 162 Group Assignments 25MUHAMMAD FAUZAN ABU BAKARNo ratings yet

- A Project Report ON: Youth Attraction in Bikano at BikanervalaDocument31 pagesA Project Report ON: Youth Attraction in Bikano at Bikanervalamanoj kumar Das67% (3)

- Module 4 - Notes ReceivableDocument22 pagesModule 4 - Notes ReceivableJennalyn S. GanalonNo ratings yet

- Study On Advertising Agency and Tourism Industry in NepalDocument5 pagesStudy On Advertising Agency and Tourism Industry in NepalSocial Science Journal for Advanced ResearchNo ratings yet

- IEM Bulletin October 2016Document52 pagesIEM Bulletin October 2016Zero123No ratings yet

- Younity's 3 Year Young Anniv Flash Sale PDFDocument1 pageYounity's 3 Year Young Anniv Flash Sale PDFIvy NinjaNo ratings yet

- AssessmentBrief 23.24BRM Oct2023Document10 pagesAssessmentBrief 23.24BRM Oct2023Prince ChibuezeNo ratings yet