Download as ppt, pdf, or txt

You might also like

- 1 Accounting For Merchandising BusinessDocument23 pages1 Accounting For Merchandising BusinessKhay2 ManaliliDelaCruz100% (1)

- Acc 211 MidtermDocument8 pagesAcc 211 MidtermRinaldi Sinaga100% (2)

- BASIC ACCOUNTING ExamDocument4 pagesBASIC ACCOUNTING ExamKevinPaulMasmodiLaviňa60% (5)

- Sage X3 - User Guide - SE - Reports - Financial-US000Document173 pagesSage X3 - User Guide - SE - Reports - Financial-US000caplusinc100% (2)

- Job Order CostingDocument49 pagesJob Order CostingKuroko71% (7)

- VAT Transfer PostingDocument1 pageVAT Transfer PostingabbasxNo ratings yet

- ABC CorporationDocument6 pagesABC CorporationDemeke HeseboNo ratings yet

- Journal EntriesDocument55 pagesJournal Entriesmunna00016100% (1)

- Recording TransactionsDocument39 pagesRecording Transactionspranali suryawanshiNo ratings yet

- Accounting Cycle UpdatedDocument73 pagesAccounting Cycle UpdatedAce Maynard DiancoNo ratings yet

- Demo Lesson PlanDocument4 pagesDemo Lesson PlanJane Tanams100% (1)

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument13 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionMarielle Mae BurbosNo ratings yet

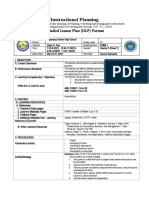

- Instructional Planning: Detailed Lesson Plan (DLP) FormatDocument5 pagesInstructional Planning: Detailed Lesson Plan (DLP) FormatDaisy PaoNo ratings yet

- Baking Tools and EquipmentDocument50 pagesBaking Tools and EquipmentKenichi KenNo ratings yet

- Chapter 4 - Types of Major AccountsDocument15 pagesChapter 4 - Types of Major AccountsApril GumiranNo ratings yet

- Quizzes - Chapter 4 - Types of Major Accounts.Document3 pagesQuizzes - Chapter 4 - Types of Major Accounts.Mechaella Shella Ningal ApolinarioNo ratings yet

- Iobz - Syllabus Financial Accounting 11Document2 pagesIobz - Syllabus Financial Accounting 11josemusi0% (1)

- Fundamentals of Accounting 1Document241 pagesFundamentals of Accounting 1kedge100% (2)

- Module 5. Methods of CookingDocument3 pagesModule 5. Methods of CookingGeboy AguilarNo ratings yet

- Lesson 1 (Baking Tools & Equipment)Document52 pagesLesson 1 (Baking Tools & Equipment)Shiela Mae GarciaNo ratings yet

- 4th Quarter Entrepreneurship FinalsDocument3 pages4th Quarter Entrepreneurship FinalsShen EugenioNo ratings yet

- CHAPTER 1 Introduction To AccountingDocument12 pagesCHAPTER 1 Introduction To Accountingrosendophil7No ratings yet

- Midterm - Financial Acctg & Reporting First Sem (Sy2021 2022) BDocument6 pagesMidterm - Financial Acctg & Reporting First Sem (Sy2021 2022) BLENNETH MONESNo ratings yet

- Chapter 2 Branches of Accounting and Users of Accounting InformationDocument14 pagesChapter 2 Branches of Accounting and Users of Accounting InformationAngellouiza MatampacNo ratings yet

- Chapter 13-CL and ContengenciesDocument12 pagesChapter 13-CL and ContengenciesPilly PhamNo ratings yet

- Accounting Training: Confidential PresentationDocument74 pagesAccounting Training: Confidential Presentationzee_iitNo ratings yet

- Accounting For non-CPADocument7 pagesAccounting For non-CPAJim OctavoNo ratings yet

- Bread and Pastry ProductionDocument51 pagesBread and Pastry ProductionPrincess Joy MoralesNo ratings yet

- On Line Class With 11 ABM Day1Document21 pagesOn Line Class With 11 ABM Day1Mirian De Ocampo100% (1)

- Baking Tools and EquipmentDocument72 pagesBaking Tools and EquipmentMelody NavoaNo ratings yet

- Short-Term Financial PlanningDocument64 pagesShort-Term Financial PlanningSheila Mae LaputNo ratings yet

- Financial Analysis and Reporting (Introduction)Document5 pagesFinancial Analysis and Reporting (Introduction)Mariadel Yrog-irog100% (1)

- 1 PartnershipDocument54 pages1 PartnershipShajidur RashidNo ratings yet

- Bread and Pastry Production NC Ii: Tarragona National High SchoolDocument54 pagesBread and Pastry Production NC Ii: Tarragona National High SchoolAl Lhea Bandayanon MoralesNo ratings yet

- Bsba - Bacc-1 - Midterm Exam - ADocument3 pagesBsba - Bacc-1 - Midterm Exam - AMechileNo ratings yet

- Quiz 5 Books of Accounts Without AnswerDocument5 pagesQuiz 5 Books of Accounts Without AnswerHello KittyNo ratings yet

- Chapter 7 The Accounting EquationDocument57 pagesChapter 7 The Accounting EquationCarmelaNo ratings yet

- Merchandising BusinessDocument31 pagesMerchandising BusinessAngelo ReyesNo ratings yet

- The Accounting Cycle - Service Business: Rodmarc P. Sanchez, J.DDocument41 pagesThe Accounting Cycle - Service Business: Rodmarc P. Sanchez, J.DDodgeSanchezNo ratings yet

- TLEBPP10 Q2 Mod4 Mixing Techniques Procedures and Types of Pastries v3Document29 pagesTLEBPP10 Q2 Mod4 Mixing Techniques Procedures and Types of Pastries v3Cherry Gelle DimaculanganNo ratings yet

- MERCHANDISING BUSINESS (Periodic Vs Perpetual)Document3 pagesMERCHANDISING BUSINESS (Periodic Vs Perpetual)Laurence Karl CurboNo ratings yet

- Module 1 Accountancy ProfessionDocument39 pagesModule 1 Accountancy ProfessionNicole ConcepcionNo ratings yet

- FABM1-LESSON-2 - Users of Accounting InformationDocument5 pagesFABM1-LESSON-2 - Users of Accounting InformationGheGhe AvilaNo ratings yet

- Acctg Project-2Document3 pagesAcctg Project-2Jania Lopez Amiuq CampilananNo ratings yet

- Special Journals Transactions Source DocumentsDocument11 pagesSpecial Journals Transactions Source DocumentsStpmTutorialClassNo ratings yet

- Introduction To Accounting: StructureDocument418 pagesIntroduction To Accounting: StructureRashadNo ratings yet

- Accounting Concepts and ConventionsDocument5 pagesAccounting Concepts and ConventionsAMIN BUHARI ABDUL KHADERNo ratings yet

- Fabm 1 Quiz TheoriesDocument4 pagesFabm 1 Quiz TheoriesJanafaye Krisha100% (1)

- FABM2 Module - 1Document3 pagesFABM2 Module - 1Jennifer NayveNo ratings yet

- FAR Course GuideDocument4 pagesFAR Course GuideMariel BombitaNo ratings yet

- Question 1: Completing The Accounting Cycle, Worksheet and FinancialDocument9 pagesQuestion 1: Completing The Accounting Cycle, Worksheet and FinancialĐanNguyễnNo ratings yet

- ACTG21C - Midterm ExamDocument8 pagesACTG21C - Midterm ExamJuanito TanamorNo ratings yet

- Chapter 4: Types of Major AccountsDocument3 pagesChapter 4: Types of Major AccountsShemara AlonzoNo ratings yet

- FABM11 IIIa 6Document3 pagesFABM11 IIIa 6Mary Grace Pagalan LadaranNo ratings yet

- Lecture in FUNAC 2Document84 pagesLecture in FUNAC 2Shaira Bloom RagonjanNo ratings yet

- ACCT101 - Prelim - THEORY (25 PTS)Document3 pagesACCT101 - Prelim - THEORY (25 PTS)Accounting 201100% (1)

- Financial Accounting Part IDocument18 pagesFinancial Accounting Part Idannydoly100% (1)

- Chqpte 1 7 Practice TestsDocument6 pagesChqpte 1 7 Practice TestsI IvaNo ratings yet

- Fabm2 Sce Week 6-8Document61 pagesFabm2 Sce Week 6-8mary rose aragonNo ratings yet

- GCT BKK NC3 (Lecture 2)Document5 pagesGCT BKK NC3 (Lecture 2)Layla ReksNo ratings yet

- Bsa 14c Cost Acctg Syllabus 2019-20 II LanenDocument14 pagesBsa 14c Cost Acctg Syllabus 2019-20 II LanenOfelia RagpaNo ratings yet

- Abm 11 Fundamentals of Accountancy Business and Management 1 Module 1Document145 pagesAbm 11 Fundamentals of Accountancy Business and Management 1 Module 1XiexieNo ratings yet

- AKN4509 Accounting Information SystemsDocument57 pagesAKN4509 Accounting Information SystemsAgnes Teoh Sook SianNo ratings yet

- Accounting Concepts and Accounting Equation DrillsDocument3 pagesAccounting Concepts and Accounting Equation Drillsken garciaNo ratings yet

- Lec 5Document56 pagesLec 5Sara Abdelrahim MakkawiNo ratings yet

- Steps: Fundamentals of AccountingDocument5 pagesSteps: Fundamentals of AccountingMikaela LacabaNo ratings yet

- Dwnload Full Accounting Volume 1 Canadian 9th Edition Horngren Solutions Manual PDFDocument36 pagesDwnload Full Accounting Volume 1 Canadian 9th Edition Horngren Solutions Manual PDFsynomocyeducable6pyb8k100% (20)

- Error Question 3Document4 pagesError Question 3Rimmy's BrainNo ratings yet

- Billable Item Class - 20190328 - 150942185Document14 pagesBillable Item Class - 20190328 - 150942185Taslim100% (1)

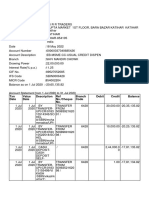

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument18 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceMrinal KumarNo ratings yet

- Unit 1 Audit of Property PLant and EquipmentDocument5 pagesUnit 1 Audit of Property PLant and EquipmentJustin SolanoNo ratings yet

- FAR-02 Retained EarningsDocument5 pagesFAR-02 Retained EarningsKim Cristian MaañoNo ratings yet

- Top Ten QuickBooks Tips and TricksDocument52 pagesTop Ten QuickBooks Tips and Tricksjaalcivar100% (2)

- Dave Chapter 9Document11 pagesDave Chapter 9Mark Dave SambranoNo ratings yet

- Adjusting Entries ActsDocument5 pagesAdjusting Entries ActsLori100% (1)

- Principles of Accounting - CASE NO. 4 - PC DEPOTDocument24 pagesPrinciples of Accounting - CASE NO. 4 - PC DEPOTlouie florentine Sanchez100% (1)

- Examination Question and Answers, Set B (Problem Solving), Chapter 2 - Analyzing TransactionsDocument4 pagesExamination Question and Answers, Set B (Problem Solving), Chapter 2 - Analyzing TransactionsJohn Carlos DoringoNo ratings yet

- Lecture 5 Cash BookDocument10 pagesLecture 5 Cash BookChaudhry F MasoodNo ratings yet

- ACL Commands User GuideDocument62 pagesACL Commands User GuiderobmathewNo ratings yet

- 2551Document2 pages2551Mariluz BeltranNo ratings yet

- ACC 311 Finals Answer KeyDocument11 pagesACC 311 Finals Answer KeyAnn GGNo ratings yet

- Merged 20240425 1313 RemoDocument4 pagesMerged 20240425 1313 Remodeep925211No ratings yet

- Boddoc LN B61a5Document203 pagesBoddoc LN B61a5koos_engelbrecht100% (1)

- Branch Accounting 1Document36 pagesBranch Accounting 1Efa Agus100% (3)

- Prelim Exam - Intermediate Accounting Part 1Document13 pagesPrelim Exam - Intermediate Accounting Part 1Vincent AbellaNo ratings yet

- Accounting Nov 2017 MemoDocument14 pagesAccounting Nov 2017 Memokwanele andiswaNo ratings yet

- Goods and Services Tax (GST) : Complete Option 1 OR 2 OR 3 (Indicate One Choice With An X)Document2 pagesGoods and Services Tax (GST) : Complete Option 1 OR 2 OR 3 (Indicate One Choice With An X)rajkrishna03No ratings yet

- KTQT 2.8 3.2Document4 pagesKTQT 2.8 3.2Trần Thanh SơnNo ratings yet

- College Accounting 12th Edition Slater Test BankDocument36 pagesCollege Accounting 12th Edition Slater Test Bankotisphoebeajn100% (33)

- Fa1 Examiner's Report S21-A22Document6 pagesFa1 Examiner's Report S21-A22ArbazNo ratings yet