Download as ppt, pdf, or txt

You might also like

- Ebook PDF Corporate Finance A Focused Approach 6th Edition PDFDocument29 pagesEbook PDF Corporate Finance A Focused Approach 6th Edition PDFjennifer.browne345100% (51)

- Wolfgang Keller at Konigsbrau-TAK CASE ANALYSISDocument3 pagesWolfgang Keller at Konigsbrau-TAK CASE ANALYSISArefeen Hridoy100% (11)

- Bill of Exchange and ChecksDocument8 pagesBill of Exchange and ChecksSmurf83% (18)

- Exam Practice Question Glori Fried Chicken Rima Puri v2 WZ AnswersDocument4 pagesExam Practice Question Glori Fried Chicken Rima Puri v2 WZ AnswersJœ œNo ratings yet

- Unit 4 - Contracts 2-1Document30 pagesUnit 4 - Contracts 2-1sarthak chughNo ratings yet

- COT Indicators - COT Indicator Suite For MetaTrader - MT4 - MT5Document1 pageCOT Indicators - COT Indicator Suite For MetaTrader - MT4 - MT5Shahbaz SyedNo ratings yet

- Car Park Shade QatarSat PDFDocument2 pagesCar Park Shade QatarSat PDFAnonymous 94TBTBRks0% (1)

- The Negotiable Instruments Act 1881Document119 pagesThe Negotiable Instruments Act 1881Sunayana GuptaNo ratings yet

- Banking Laws Pakistan Negotiable InstrumentsDocument57 pagesBanking Laws Pakistan Negotiable Instrumentsmzqace100% (8)

- Negotiable Instrument: Unit 3 Ms - Shruti MinochaDocument50 pagesNegotiable Instrument: Unit 3 Ms - Shruti MinochaAshutosh KumarNo ratings yet

- Cheque Paying and Collecting BankDocument5 pagesCheque Paying and Collecting BankSyed RedwanNo ratings yet

- Law of Negotiable Instrument (Law 416)Document8 pagesLaw of Negotiable Instrument (Law 416)Sarah M'dinNo ratings yet

- Chapter 4 LABDocument23 pagesChapter 4 LABVishvesh ShahNo ratings yet

- Promissory NotesDocument5 pagesPromissory NotesHimanshu DarganNo ratings yet

- Promissory Notes-Bills of Exchangeand ChequesDocument17 pagesPromissory Notes-Bills of Exchangeand Chequestheashu022No ratings yet

- Negotiable Instrument Act-1881: DR - Itishree MishraDocument23 pagesNegotiable Instrument Act-1881: DR - Itishree MishraAishwarya PriyadarshiniNo ratings yet

- Unit VII The Negotiable Instruments Act, 1881Document42 pagesUnit VII The Negotiable Instruments Act, 1881Neha GeorgeNo ratings yet

- BL-Synopsis - 9 (NI) (18 - 11 - 20)Document15 pagesBL-Synopsis - 9 (NI) (18 - 11 - 20)Erfan KhanNo ratings yet

- Negotiable Instrument Act: Amit BachhawatDocument11 pagesNegotiable Instrument Act: Amit BachhawatvaishnaviNo ratings yet

- THE Negotiable Instruments ACT, 1881Document55 pagesTHE Negotiable Instruments ACT, 1881Shradha PadhiNo ratings yet

- BPP Notes IV & V UnitDocument27 pagesBPP Notes IV & V UnitVasanthan PughazendhiNo ratings yet

- Negotiable InstrumentsDocument11 pagesNegotiable InstrumentsMahesh ChavanNo ratings yet

- Commercial Law NotesDocument30 pagesCommercial Law NotesPeter MNo ratings yet

- The Negotiable Instruments ActDocument30 pagesThe Negotiable Instruments ActYandex PrithuNo ratings yet

- Banking Law 1Document21 pagesBanking Law 1MAYANK GUPTANo ratings yet

- Promissory Notes, Bill of Exchange and ChequeDocument28 pagesPromissory Notes, Bill of Exchange and ChequeAadi saklechaNo ratings yet

- Negotiable Instruments Act 1881Document59 pagesNegotiable Instruments Act 1881vivekananda Roy100% (7)

- Group 5 Final Written Report-Legal FormsDocument34 pagesGroup 5 Final Written Report-Legal FormsFederico Dipay Jr.No ratings yet

- Negotiable Instruments ACTDocument19 pagesNegotiable Instruments ACTnaved_siddiquiNo ratings yet

- Negotiable InstrumentsDocument113 pagesNegotiable InstrumentsIsunni AroraNo ratings yet

- Law of Negotiable InstrumentsDocument26 pagesLaw of Negotiable InstrumentsMohammed Akbar KhanNo ratings yet

- Banking Laws & Operations: (Statutory Body Under An Act of Parliament)Document16 pagesBanking Laws & Operations: (Statutory Body Under An Act of Parliament)Vinu DNo ratings yet

- Promissory Notes, Bill of Exchange and ChequeDocument28 pagesPromissory Notes, Bill of Exchange and ChequeElsa ShaikhNo ratings yet

- Nego Finals ReviewerDocument22 pagesNego Finals ReviewerJay-ArhNo ratings yet

- Negotiable Instruments Act-1881Document37 pagesNegotiable Instruments Act-1881Md ToufikuzzamanNo ratings yet

- Negotiable Instrument: Promissory Note, Bill of Exchange, or Cheque Payable Either To Order or To The Bearer"Document5 pagesNegotiable Instrument: Promissory Note, Bill of Exchange, or Cheque Payable Either To Order or To The Bearer"Amandeep Singh Manku100% (1)

- NIL - Chapter 10 - ChecksDocument11 pagesNIL - Chapter 10 - ChecksElaine Dianne Laig SamonteNo ratings yet

- Assignment - 1Document13 pagesAssignment - 1Mohd shakeeb HashmiNo ratings yet

- Banking PresentationDocument21 pagesBanking Presentationpreetha1507mNo ratings yet

- PRTC Negotiable InstrumentsDocument171 pagesPRTC Negotiable InstrumentsSo min JeonNo ratings yet

- Negotiable Instrument Act, 1881Document24 pagesNegotiable Instrument Act, 1881siddharth devnaniNo ratings yet

- Commercial Law Atty. RondezDocument108 pagesCommercial Law Atty. RondezPaul Dean MarkNo ratings yet

- Nego Finals ReviewerDocument22 pagesNego Finals ReviewerAnna Katrina VistanNo ratings yet

- Bank Draft or Demand DraftDocument25 pagesBank Draft or Demand DraftTeja RaviNo ratings yet

- Business Law Question N AnswersDocument24 pagesBusiness Law Question N AnswersKalpita Chaudhari-Vartak100% (1)

- A059 Banking LawDocument11 pagesA059 Banking LawRajeev TekwaniNo ratings yet

- Negotiable Instruments Act: Learning and Knowledge Management CentreDocument62 pagesNegotiable Instruments Act: Learning and Knowledge Management CentrezidhichoraNo ratings yet

- Banker Customer Relationship & Negotiable InstrumentsDocument23 pagesBanker Customer Relationship & Negotiable InstrumentsMD KamalNo ratings yet

- Dishonour of Negotiable InstrumentsDocument6 pagesDishonour of Negotiable InstrumentsMukul BajajNo ratings yet

- THE Negotiable Instruments ACT, 1881Document54 pagesTHE Negotiable Instruments ACT, 1881Shradha PadhiNo ratings yet

- Evidence Midterm ReviewerDocument24 pagesEvidence Midterm Reviewercmv mendozaNo ratings yet

- Negotiable InstrumentsDocument46 pagesNegotiable InstrumentsNaina ParasharNo ratings yet

- Unit-4 Negotiable Instrument Act-1881Document3 pagesUnit-4 Negotiable Instrument Act-1881Vivek rathodNo ratings yet

- TPB - Module 4 - Reference MaterialDocument8 pagesTPB - Module 4 - Reference MaterialSupreethaNo ratings yet

- Negotiable Instrument Act 1881 SatishDocument22 pagesNegotiable Instrument Act 1881 SatishSatish VermaNo ratings yet

- 13th Week-Negotiable Instruments (Repaired)Document39 pages13th Week-Negotiable Instruments (Repaired)Muhammad WasifNo ratings yet

- Negotiable Instruments Law: Section 1. Form of Negotiable InstrumentDocument4 pagesNegotiable Instruments Law: Section 1. Form of Negotiable InstrumentJed CaraigNo ratings yet

- Negotiable Instruments Act, 1881Document23 pagesNegotiable Instruments Act, 1881Kansal Abhishek100% (1)

- Negotiable Instruments Laws Carlos Hilado Memorial State University Submitted By: Atty. Jul Davi P. SaezDocument26 pagesNegotiable Instruments Laws Carlos Hilado Memorial State University Submitted By: Atty. Jul Davi P. SaezJellie ElmerNo ratings yet

- Negotiable Instruments Act 1881Document47 pagesNegotiable Instruments Act 1881SupriyamathewNo ratings yet

- Businesslawunit3 180116172228Document32 pagesBusinesslawunit3 180116172228MansoorHayatAwanNo ratings yet

- Negotiable Instrument Act Full NotesDocument49 pagesNegotiable Instrument Act Full NotesHashir KhanNo ratings yet

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Revealed From A Top Realtor: The Fastest Way To Sell Properties Like Crazy In Real Estate - Even If You Are A Complete NewbieFrom EverandRevealed From A Top Realtor: The Fastest Way To Sell Properties Like Crazy In Real Estate - Even If You Are A Complete NewbieNo ratings yet

- ApplyBoard Invoice Template CanadaDocument2 pagesApplyBoard Invoice Template CanadasmangrishNo ratings yet

- Scan Aug 23, 2020 PDFDocument7 pagesScan Aug 23, 2020 PDFRgtdgcn c rydtNo ratings yet

- Consumer Awareness ProjectDocument30 pagesConsumer Awareness ProjectJNV_DVG38% (21)

- Ole Achieving Highly Effective WorkforceDocument8 pagesOle Achieving Highly Effective WorkforceDian PeshevNo ratings yet

- Process: A Generic ViewDocument13 pagesProcess: A Generic ViewHariNo ratings yet

- Documenting An Existing Api With SwaggerDocument11 pagesDocumenting An Existing Api With SwaggerJayampathi SamarasingheNo ratings yet

- Lesson 6 Evan S Dela RosaDocument6 pagesLesson 6 Evan S Dela RosaDyan Dela Rosa BuenafeNo ratings yet

- Force Majeure and Its Impact On Real Estate Leases PDFDocument9 pagesForce Majeure and Its Impact On Real Estate Leases PDFBharat BhushanNo ratings yet

- Introduction To Organisational Behaviour: Case of AmazonDocument6 pagesIntroduction To Organisational Behaviour: Case of AmazonMoumita RoyNo ratings yet

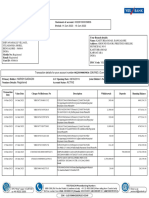

- Account Statement 14 Jun 2023-19 Jun 2023Document4 pagesAccount Statement 14 Jun 2023-19 Jun 2023propvisor real estateNo ratings yet

- Brief Prof Gitika KapoorDocument2 pagesBrief Prof Gitika KapoorNaman MaheshwariNo ratings yet

- Final ExamDocument6 pagesFinal ExamWan SawaNo ratings yet

- Order 2 Packing SlipDocument2 pagesOrder 2 Packing SlipArnav JoshiNo ratings yet

- Sap Tcodes: Logistics ExecutionDocument53 pagesSap Tcodes: Logistics ExecutionGabrielNo ratings yet

- AFAR Preboards MergedDocument112 pagesAFAR Preboards Mergedpajarillagavincent15No ratings yet

- Hospet Steels Limited, KoppalDocument21 pagesHospet Steels Limited, KoppalSagar GNo ratings yet

- Session 5 Customer Experience Journey MapDocument33 pagesSession 5 Customer Experience Journey Map曹旅瀚No ratings yet

- Concha V RubioDocument18 pagesConcha V RubiokamiruhyunNo ratings yet

- Customer Perception Towards Internet BankingDocument35 pagesCustomer Perception Towards Internet Bankingmajiclover90% (78)

- App Builder All SetDocument32 pagesApp Builder All SetArya50% (2)

- Educational Institutions: Santos, Sofia Anne PDocument11 pagesEducational Institutions: Santos, Sofia Anne PApril ManjaresNo ratings yet

- Pe Price DT.06.08.2020Document91 pagesPe Price DT.06.08.2020Akshat Engineers Private LimitedNo ratings yet

- TITAN (Watches) : Presented By: Shivangi Sharma Mba Specialization 2Nd SemDocument42 pagesTITAN (Watches) : Presented By: Shivangi Sharma Mba Specialization 2Nd SemShivangi SharmaNo ratings yet

- Disney Case DataDocument8 pagesDisney Case DataJustine Rachel YaoNo ratings yet

- Bank Recon TransmittalDocument3 pagesBank Recon TransmittalJessa Mariz Lecias CalimotNo ratings yet