Download as ppt, pdf, or txt

You might also like

- 5CO01 - Assessment BriefDocument10 pages5CO01 - Assessment BriefEmmanuel KingsNo ratings yet

- Three Girls From BronzevilleDocument5 pagesThree Girls From BronzevilleOnPointRadio0% (1)

- Budget and Budgetary Control in Kesoram Cement Industries LTDDocument42 pagesBudget and Budgetary Control in Kesoram Cement Industries LTDglorydharmaraj100% (7)

- Functional and Activity - Based BudgetingDocument45 pagesFunctional and Activity - Based BudgetingJessa MartinezNo ratings yet

- Production Budgets: Understand Why Organizations Budget and The Processes They Use To Create BudgetsDocument74 pagesProduction Budgets: Understand Why Organizations Budget and The Processes They Use To Create BudgetsRoman AliNo ratings yet

- Chapter - 8 - Master BudgetingDocument92 pagesChapter - 8 - Master Budgetingshamsirarefin275285No ratings yet

- IPPTChap 008Document92 pagesIPPTChap 008AnasChihabNo ratings yet

- Chapter One Master BudgetingDocument89 pagesChapter One Master BudgetingFidelina CastroNo ratings yet

- Profit Planning: © 2010 The Mcgraw-Hill Companies, IncDocument64 pagesProfit Planning: © 2010 The Mcgraw-Hill Companies, IncSarmad TareenNo ratings yet

- Chap009 FB2101 1011B StudentDocument82 pagesChap009 FB2101 1011B StudentJavier TsangNo ratings yet

- Lecture Five Budget and Profit PlanningDocument104 pagesLecture Five Budget and Profit PlanningMohamed RashadNo ratings yet

- Profit Planning: Mcgraw-Hill /irwinDocument89 pagesProfit Planning: Mcgraw-Hill /irwinFariaFaryNo ratings yet

- GNB - 09 - 12e Profit PlanningDocument89 pagesGNB - 09 - 12e Profit PlanningAhmed Mostafa ElmowafyNo ratings yet

- Chapter 9 Garrison 13eDocument88 pagesChapter 9 Garrison 13efarhan MomenNo ratings yet

- Profit Planning: Chapter NineDocument89 pagesProfit Planning: Chapter NineanyrzahNo ratings yet

- Short-Term Financial Planning: The Basic Framework of BudgetingDocument8 pagesShort-Term Financial Planning: The Basic Framework of BudgetingDaphne PerezNo ratings yet

- Lesson 7Document103 pagesLesson 7henielh965No ratings yet

- Chap009Document82 pagesChap009Shimul HossainNo ratings yet

- Profit Planning: Mcgraw-Hill/IrwinDocument88 pagesProfit Planning: Mcgraw-Hill/IrwinRahamat UllahNo ratings yet

- Profit Planning: Mcgraw-Hill /irwinDocument89 pagesProfit Planning: Mcgraw-Hill /irwinXu FengNo ratings yet

- Management Accounting: Profit Planning / BudgetingDocument78 pagesManagement Accounting: Profit Planning / BudgetingMary R. R. PanesNo ratings yet

- Module 6 - Profit Planning (Budgeting)Document82 pagesModule 6 - Profit Planning (Budgeting)CristineNo ratings yet

- Profit Planning: Asic Framework of Budgeting AccountingDocument5 pagesProfit Planning: Asic Framework of Budgeting AccountingMichaela CruzNo ratings yet

- Operating and Financial Budgeting FinalDocument10 pagesOperating and Financial Budgeting FinalKharen SantosNo ratings yet

- Chapter 04Document9 pagesChapter 04Trang Lê Thị ThùyNo ratings yet

- ACT4105 - Class 05 06 07 (Printing)Document24 pagesACT4105 - Class 05 06 07 (Printing)Wong Siu CheongNo ratings yet

- BudgetingDocument12 pagesBudgetingSyeda Samia SultanaNo ratings yet

- ACT202 Chapter 8Document80 pagesACT202 Chapter 8arafkhan1623No ratings yet

- Unit 2 Budget and Budgetary Control - 8601574734764214Document82 pagesUnit 2 Budget and Budgetary Control - 8601574734764214Rhea Mae AmitNo ratings yet

- Kuliah 1 MANAGEMENT - CONTROL - SYSTEMS - 1Document24 pagesKuliah 1 MANAGEMENT - CONTROL - SYSTEMS - 1Ismail MuhammadNo ratings yet

- Operating and Financial Budgeting (Final)Document7 pagesOperating and Financial Budgeting (Final)Mica R.No ratings yet

- Learning Objective 1: Understand Why Organizations Budget and The Processes They Use To Create BudgetsDocument70 pagesLearning Objective 1: Understand Why Organizations Budget and The Processes They Use To Create BudgetsshivaniNo ratings yet

- FinmanDocument4 pagesFinmanMycah ManriqueNo ratings yet

- BudgetingDocument13 pagesBudgetingUditha Muthumala100% (1)

- Unit Budgeting: A Ro L OffDocument5 pagesUnit Budgeting: A Ro L OffNiranjan ChopadeNo ratings yet

- Budgeting Introduction PartDocument8 pagesBudgeting Introduction PartAvinash kashimNo ratings yet

- Budgeting ProcessDocument43 pagesBudgeting Processabhineet.jkaiNo ratings yet

- A222 - Topic 4 MacsDocument29 pagesA222 - Topic 4 MacsfiqNo ratings yet

- F2-12 Budgeting - Nature, Purpose and Behavioural AspectsDocument12 pagesF2-12 Budgeting - Nature, Purpose and Behavioural AspectsJaved ImranNo ratings yet

- Budget F MacDocument94 pagesBudget F MacAkshat ShuklaNo ratings yet

- Session 05 BudgetingDocument9 pagesSession 05 BudgetingalirajayNo ratings yet

- VI. Budgeting and Financial ForecastingDocument39 pagesVI. Budgeting and Financial ForecastingJemNo ratings yet

- FS Notes Budgetary Control & MiscellaneousDocument8 pagesFS Notes Budgetary Control & MiscellaneousMuditNo ratings yet

- Budget and Budgetary ControlDocument10 pagesBudget and Budgetary Controlzeebee17No ratings yet

- AKMEN Pertm 4, 5Document127 pagesAKMEN Pertm 4, 5UJI TESTNo ratings yet

- Budget & Budgetary Control - Sem-IDocument37 pagesBudget & Budgetary Control - Sem-Ishital_vyas19870% (1)

- Profit Planning or Budgeting: Control Is The Use of Budget To Control A Firm's ActivitiesDocument30 pagesProfit Planning or Budgeting: Control Is The Use of Budget To Control A Firm's ActivitiesRaven Dumlao OllerNo ratings yet

- Budgetary Control and Standard Costing2Document45 pagesBudgetary Control and Standard Costing2Pratyay DasNo ratings yet

- Budgetary Control and Standard Costing2Document45 pagesBudgetary Control and Standard Costing2Pratyay DasNo ratings yet

- Unit-5 - Budgets and Budgetory ControlDocument28 pagesUnit-5 - Budgets and Budgetory ControlCoimbatore foodieNo ratings yet

- Chap009 Profit PlanningDocument15 pagesChap009 Profit PlanningThida WinNo ratings yet

- Lo1 - MaDocument65 pagesLo1 - MaRawan ThiabNo ratings yet

- Budget by ArmaanDocument37 pagesBudget by Armaansyed bilalNo ratings yet

- Budgeting Budgetary ControlDocument10 pagesBudgeting Budgetary ControlPriya YûvãNo ratings yet

- 4 Budget and Budgetary Control SolutionsDocument74 pages4 Budget and Budgetary Control SolutionsRahul SinghNo ratings yet

- Strategy and The Master BudgetDocument6 pagesStrategy and The Master BudgetmadlangbayanryzNo ratings yet

- Managerial Accounting and Cost Concepts: Rights Reserved. Mcgraw-Hill/IrwinDocument67 pagesManagerial Accounting and Cost Concepts: Rights Reserved. Mcgraw-Hill/Irwinవెంకటరమణయ్య మాలెపాటిNo ratings yet

- Budgetary Control and Standard CostingDocument15 pagesBudgetary Control and Standard CostingPratyay DasNo ratings yet

- Budget ControlDocument33 pagesBudget Controladnan arshadNo ratings yet

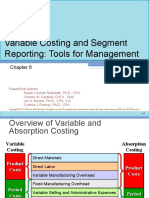

- Variable Costing and Segment Reporting: Tools For ManagementDocument20 pagesVariable Costing and Segment Reporting: Tools For ManagementFarhan RabbehNo ratings yet

- SPPTChap 010Document19 pagesSPPTChap 010Farhan RabbehNo ratings yet

- Standard Costs and VariancesDocument19 pagesStandard Costs and VariancesFarhan RabbehNo ratings yet

- Managerial Accounting and Cost ConceptsDocument19 pagesManagerial Accounting and Cost ConceptsFarhan RabbehNo ratings yet

- Flexible Budgets and Performance AnalysisDocument22 pagesFlexible Budgets and Performance AnalysisFarhan RabbehNo ratings yet

- Assignment On NegotiationDocument4 pagesAssignment On NegotiationFarhan RabbehNo ratings yet

- MSDS 731Document7 pagesMSDS 731GautamNo ratings yet

- Const. ContractsDocument9 pagesConst. ContractsKenneth Bryan Tegerero TegioNo ratings yet

- Blank Noise Ass TemplateDocument16 pagesBlank Noise Ass TemplateDucVikingNo ratings yet

- Fluid Machines Lecture Notes CH-4-Centrifugal CompressorDocument21 pagesFluid Machines Lecture Notes CH-4-Centrifugal CompressorBINNo ratings yet

- Tony Robbins NotesDocument3 pagesTony Robbins Notesrationalgaze0% (2)

- Chapter 1 Editors Introductory ChapterDocument13 pagesChapter 1 Editors Introductory Chapterroxebag437No ratings yet

- Musculoskeletal QuestionsDocument4 pagesMusculoskeletal QuestionsJen Del Mundo100% (1)

- SAmple Format (Police Report)Document3 pagesSAmple Format (Police Report)Johnpatrick DejesusNo ratings yet

- Unit 4Document8 pagesUnit 4lolybarreiroNo ratings yet

- Day 4 - Technocracy vs. Communism - Socialism, FascismDocument6 pagesDay 4 - Technocracy vs. Communism - Socialism, FascismocigranNo ratings yet

- WP 1997 - 16 Catherine Marquette-07112007 - 1Document19 pagesWP 1997 - 16 Catherine Marquette-07112007 - 1k1l2d3No ratings yet

- Marylou Curran Resume 4Document2 pagesMarylou Curran Resume 4Brandy SniderNo ratings yet

- Austin - A Plea For ExcusesDocument31 pagesAustin - A Plea For ExcusesexactedNo ratings yet

- Wipro Integrated Annual Report 2020 21Document386 pagesWipro Integrated Annual Report 2020 21Rithesh KNo ratings yet

- The 7 Habits of HIGHLY Effective PeopleDocument12 pagesThe 7 Habits of HIGHLY Effective PeopleWahid T. YahyahNo ratings yet

- Joseph Straus - A Principle of Voice Leading in The Music of StravinskyDocument20 pagesJoseph Straus - A Principle of Voice Leading in The Music of StravinskyIliya GramatikoffNo ratings yet

- Rundown Acara WorkshopDocument6 pagesRundown Acara WorkshopAnnas Nuraini br gintingNo ratings yet

- Brushless DC Motors - Part I: Construction and Operating PrinciplesDocument14 pagesBrushless DC Motors - Part I: Construction and Operating PrinciplesHung Nguyen HuyNo ratings yet

- How To Write An EssayDocument4 pagesHow To Write An EssayShah BaibrassNo ratings yet

- AWHERO - Military Applications Brochure - Gen2020Document4 pagesAWHERO - Military Applications Brochure - Gen2020زين الدين مروانيNo ratings yet

- Low Sperm Count and Its Homeopathic Cure - DR Bashir Mahmud ElliasDocument9 pagesLow Sperm Count and Its Homeopathic Cure - DR Bashir Mahmud ElliasBashir Mahmud ElliasNo ratings yet

- Upload 9Document3 pagesUpload 9Meghna CmNo ratings yet

- First Class Dhanbad 2012Document4 pagesFirst Class Dhanbad 2012ihateu1No ratings yet

- Intermediate Accounting I Inventories 2 PDFDocument2 pagesIntermediate Accounting I Inventories 2 PDFJoovs JoovhoNo ratings yet

- Statistics DLL - W3Document11 pagesStatistics DLL - W3Jovito EspantoNo ratings yet

- (M2) REVIEW - Coursebook Guidance For Module Two V1aDocument13 pages(M2) REVIEW - Coursebook Guidance For Module Two V1ahariNo ratings yet

- Faculty Collaborative Research: Pokhara University Research Center (PURC) Dhungepatan, Pokhara Lekhnath, KaskiDocument8 pagesFaculty Collaborative Research: Pokhara University Research Center (PURC) Dhungepatan, Pokhara Lekhnath, KaskiAnandNo ratings yet

- Thesis in Teaching English As Foreign LanguageDocument8 pagesThesis in Teaching English As Foreign Languagereneedelgadoalbuquerque100% (2)