Download as ppt, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5835)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Psychology 5th Edition Ciccarelli Solutions ManualDocument66 pagesPsychology 5th Edition Ciccarelli Solutions ManualMichaelMurrayybdix100% (20)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Intersubjectivity in Primary and Secondary Education A Review StudyDocument23 pagesIntersubjectivity in Primary and Secondary Education A Review StudyEDDY ALEXANDER VILLADA MARQUEZNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Seismic Earth Pressures On Cantilever Retaining Structures 2010Document10 pagesSeismic Earth Pressures On Cantilever Retaining Structures 2010myplaxisNo ratings yet

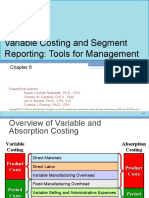

- Variable Costing and Segment Reporting: Tools For ManagementDocument20 pagesVariable Costing and Segment Reporting: Tools For ManagementFarhan RabbehNo ratings yet

- SPPTChap 010Document19 pagesSPPTChap 010Farhan RabbehNo ratings yet

- Standard Costs and VariancesDocument19 pagesStandard Costs and VariancesFarhan RabbehNo ratings yet

- Managerial Accounting and Cost ConceptsDocument19 pagesManagerial Accounting and Cost ConceptsFarhan RabbehNo ratings yet

- Flexible Budgets and Performance AnalysisDocument22 pagesFlexible Budgets and Performance AnalysisFarhan RabbehNo ratings yet

- SPPTChap 008Document17 pagesSPPTChap 008Farhan RabbehNo ratings yet

- Assignment On NegotiationDocument4 pagesAssignment On NegotiationFarhan RabbehNo ratings yet

- Rashtrasant Tukadoji Maharaj Nagpur UniversityDocument1 pageRashtrasant Tukadoji Maharaj Nagpur UniversityAkash RautNo ratings yet

- Destiny and DevilDocument177 pagesDestiny and DevilSrinivasan NarasimhanNo ratings yet

- TECHNICAL CATALOGUE - VSF - IEC - ATEX - EN - Rev1 - 2017 PDFDocument172 pagesTECHNICAL CATALOGUE - VSF - IEC - ATEX - EN - Rev1 - 2017 PDFLASCARZAMFIRESCUNo ratings yet

- Holochwost, S. J., Propper, C. B., Wolf, D. P., Willoughby, M. T., Fisher, K. R., Kolacz, J., Volpe, V. V., & Jaffee, S. R.Document21 pagesHolochwost, S. J., Propper, C. B., Wolf, D. P., Willoughby, M. T., Fisher, K. R., Kolacz, J., Volpe, V. V., & Jaffee, S. R.paulinhosvieiraNo ratings yet

- Diversity and Taxonomy of Wood Rotting Fungi From Dharashiv (Osmanabad) District (M.S.) IndiaDocument8 pagesDiversity and Taxonomy of Wood Rotting Fungi From Dharashiv (Osmanabad) District (M.S.) IndiaIJAR JOURNALNo ratings yet

- Environmental Science - Pollutants and Water PollutionDocument9 pagesEnvironmental Science - Pollutants and Water Pollutionaazadi47.mbp50No ratings yet

- Holt California Algebra 1 Homework and Practice Workbook AnswersDocument5 pagesHolt California Algebra 1 Homework and Practice Workbook Answersafmtcbjca100% (1)

- Cegesoft Peel (OPP)Document1 pageCegesoft Peel (OPP)paromanikNo ratings yet

- I'm Learning About Numbers WorksheetsDocument22 pagesI'm Learning About Numbers WorksheetsJozel M. ManuelNo ratings yet

- Five-Phase Induction Motor Drive-A Comprehensive RDocument17 pagesFive-Phase Induction Motor Drive-A Comprehensive RAnshuman MohantyNo ratings yet

- TP - PPST 2023Document4 pagesTP - PPST 2023NI KoLsNo ratings yet

- English Quarter 3Document7 pagesEnglish Quarter 3gailNo ratings yet

- What Is The Format of A Memo?Document3 pagesWhat Is The Format of A Memo?Syeda Ghazia BatoolNo ratings yet

- 11aug2023131058 Esiareport VDP, Thy, Mt&Pzugss1108Document275 pages11aug2023131058 Esiareport VDP, Thy, Mt&Pzugss1108akhilaggarwalNo ratings yet

- Full Chapter The Zoo and Screen Media Images of Exhibition and Encounter 1St Edition Michael Lawrence PDFDocument53 pagesFull Chapter The Zoo and Screen Media Images of Exhibition and Encounter 1St Edition Michael Lawrence PDFpamela.thomas142100% (6)

- Raincut Erosion Control of Topsoil With Geojute and Vegetation in BangladeshDocument37 pagesRaincut Erosion Control of Topsoil With Geojute and Vegetation in BangladeshMana IchsanNo ratings yet

- Science 5-Q3-SLM2Document13 pagesScience 5-Q3-SLM2Gradefive MolaveNo ratings yet

- Gülyüz Et Al. Multiphase Deformation, Fluid Flow and Mineralization in Epithermal Systems Inferences From Structures, Vein Textures and Breccias of The Kestanelik Epithermal Au-ADocument22 pagesGülyüz Et Al. Multiphase Deformation, Fluid Flow and Mineralization in Epithermal Systems Inferences From Structures, Vein Textures and Breccias of The Kestanelik Epithermal Au-Ahüseyin burak göktaşNo ratings yet

- Freud in The PampasDocument328 pagesFreud in The Pampasparadoxe89No ratings yet

- UntitledDocument29 pagesUntitledJimmy A GenonNo ratings yet

- Zero Energy BuildingDocument7 pagesZero Energy BuildingIJRASETPublicationsNo ratings yet

- Behavior TrackerDocument2 pagesBehavior Trackerapi-258960155No ratings yet

- National Merit Mopup Government Sponsorship Admission List 2020-2021Document4 pagesNational Merit Mopup Government Sponsorship Admission List 2020-2021The Campus Times100% (1)

- A Review of Mixed Methods, Pragmatism and Abduction TechniquesDocument14 pagesA Review of Mixed Methods, Pragmatism and Abduction TechniquesDeep ShiNo ratings yet

- WLP Q1 - W4 Oct. 26 30Document17 pagesWLP Q1 - W4 Oct. 26 30Jessibel AlejandroNo ratings yet

- Non-Verbal Communication in SpainDocument20 pagesNon-Verbal Communication in SpainDarina PiskunovaNo ratings yet

- Chapter ReviewsDocument16 pagesChapter ReviewsLélio CaiadoNo ratings yet