Download as pptx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- PASIG F.O.I. ORDINANCE (Final & Approved Version)Document12 pagesPASIG F.O.I. ORDINANCE (Final & Approved Version)Vico Sotto75% (4)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Larisa Vetrova - How Lenin and Stalin Brainwashed Russians - Historical Facts and Propaganda PostersDocument102 pagesLarisa Vetrova - How Lenin and Stalin Brainwashed Russians - Historical Facts and Propaganda PostersRodrigo Cardoso UlguimNo ratings yet

- EquityDocument27 pagesEquitywan nur amira100% (1)

- FD Lecture XIII XIVDocument39 pagesFD Lecture XIII XIVVineet RanjanNo ratings yet

- Mechanics of Options MarketsDocument36 pagesMechanics of Options MarketsVineet RanjanNo ratings yet

- FD Lecture XVIIDocument38 pagesFD Lecture XVIIVineet RanjanNo ratings yet

- Validation of Basel II Models: Tomáš VáclavíkDocument16 pagesValidation of Basel II Models: Tomáš VáclavíkVineet RanjanNo ratings yet

- Strategic Outsourcing at Bharti Airtel Limited: Nikhil Pandey - 56 Rimjhim Kaul - 58 Ravi Bajaj - 59 Tanya Sharma - 62Document34 pagesStrategic Outsourcing at Bharti Airtel Limited: Nikhil Pandey - 56 Rimjhim Kaul - 58 Ravi Bajaj - 59 Tanya Sharma - 62Vineet RanjanNo ratings yet

- Power Finance Corporation Limited: Financing of Renewable Energy & Energy Efficiency ProjectsDocument39 pagesPower Finance Corporation Limited: Financing of Renewable Energy & Energy Efficiency ProjectsVineet RanjanNo ratings yet

- HMM Presentation 18febDocument42 pagesHMM Presentation 18febVineet RanjanNo ratings yet

- Ethics in Entertainment The Case of Reality TV Shows: Presented by Name - Anuj ROLL - 76Document9 pagesEthics in Entertainment The Case of Reality TV Shows: Presented by Name - Anuj ROLL - 76Vineet RanjanNo ratings yet

- 3 ReceivablesDocument13 pages3 Receivablesjoneth.duenasNo ratings yet

- Pratibha Patil Is India's First Woman PresidentDocument1 pagePratibha Patil Is India's First Woman Presidentdevesh pandeyNo ratings yet

- KWL ChartDocument4 pagesKWL ChartAMBROCIO JENALYN A.No ratings yet

- 1 Dunn. 2017. Whence The Lesbian in Queer Monumentality Intersections of Gender and Sexuality in Public MemoryDocument14 pages1 Dunn. 2017. Whence The Lesbian in Queer Monumentality Intersections of Gender and Sexuality in Public MemoryKetty UrrutiaNo ratings yet

- Republic Act 8551Document16 pagesRepublic Act 8551jerick gasconNo ratings yet

- APD Solutions and APD Solutions DeKalb LLC DocumentsDocument25 pagesAPD Solutions and APD Solutions DeKalb LLC DocumentsViola DavisNo ratings yet

- 5HR01 Assessment BriefDocument8 pages5HR01 Assessment BriefsirkelvinmuthomiNo ratings yet

- Sl. No. Name of The Works Approximate Value of Civil Engineering Construction Work EMD Amount PeriodDocument3 pagesSl. No. Name of The Works Approximate Value of Civil Engineering Construction Work EMD Amount PeriodAdNo ratings yet

- 14th Floor - FDGDFGDocument3 pages14th Floor - FDGDFGskyNo ratings yet

- Affidavit GhoshDocument10 pagesAffidavit GhoshNeeraj OjhaNo ratings yet

- Bail JudgementDocument5 pagesBail JudgementPrince hassan khanNo ratings yet

- Skeleton Memo ClaimantDocument2 pagesSkeleton Memo ClaimantAnay MehrotraNo ratings yet

- 02 Munawaroh 88-99 (Fiks)Document12 pages02 Munawaroh 88-99 (Fiks)8421yahhoNo ratings yet

- Principles of Mercantalism, How Did England Implement ThemDocument4 pagesPrinciples of Mercantalism, How Did England Implement ThemGunjan MadanNo ratings yet

- In The Supreme Court of IndiaDocument42 pagesIn The Supreme Court of IndiaDanish KhattarNo ratings yet

- Thermodynamics Basic (Edited)Document18 pagesThermodynamics Basic (Edited)ronnelNo ratings yet

- Chikki Tender Package 5Document46 pagesChikki Tender Package 5MallikarjunReddyObbineniNo ratings yet

- Memo PROJECT GLACE 2.0Document7 pagesMemo PROJECT GLACE 2.0marco medurandaNo ratings yet

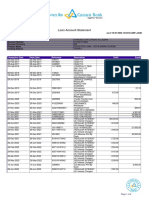

- Loan Account Statement: As of 10-07-2022 15:03:55 GMT +0530Document2 pagesLoan Account Statement: As of 10-07-2022 15:03:55 GMT +0530Sushmita kNo ratings yet

- Case Digests2 Labor LawDocument16 pagesCase Digests2 Labor LawKate Wynsleth Caser OrdinarioNo ratings yet

- Sixteenth All India Moot Court Competition, 2016: T. S. Venkateswara Iyer Memorial Ever Rolling TrophyDocument3 pagesSixteenth All India Moot Court Competition, 2016: T. S. Venkateswara Iyer Memorial Ever Rolling TrophyVicky Kumar100% (1)

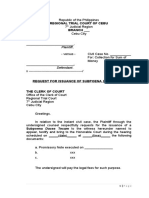

- Regional Trial Court of Cebu Branch - : PlaintiffDocument2 pagesRegional Trial Court of Cebu Branch - : PlaintiffNika RojasNo ratings yet

- Trans Defense A Ebook For The Defense of Transgender Men and Women - RemovedDocument112 pagesTrans Defense A Ebook For The Defense of Transgender Men and Women - RemovedMarie Landry's Spy ShopNo ratings yet

- PNP Counter AffidavitDocument3 pagesPNP Counter AffidavitARIESTEDES P. SINGAYANNo ratings yet

- Mock Exam 1 - MATHEMATICSDocument23 pagesMock Exam 1 - MATHEMATICSJohn Gamelle Jay CamposNo ratings yet

- Second Battle of TarainDocument3 pagesSecond Battle of TarainENGINEER SHAHID LODhiNo ratings yet

- Chapters 6-8 Animal FarmDocument6 pagesChapters 6-8 Animal FarmLuca XNo ratings yet