Download as pptx, pdf, or txt

You might also like

- Mastering Fundamental AnalysisDocument242 pagesMastering Fundamental Analysissairanga1997% (31)

- Mergers and Acquisitions ModuleDocument116 pagesMergers and Acquisitions Modulegs_waiting_4_u80% (10)

- Pas 1 - Presentation of Financial StatementsDocument30 pagesPas 1 - Presentation of Financial StatementsLee Anne Gallema Camarao100% (3)

- FABM 2 Statement of Financial PositionDocument20 pagesFABM 2 Statement of Financial PositionVictoria Manalaysay100% (1)

- PAS 10 Events After The Reporting PeriodDocument2 pagesPAS 10 Events After The Reporting PeriodJennicaBailonNo ratings yet

- Iron Condor Trade Setup TipsDocument6 pagesIron Condor Trade Setup Tipsjamisonsobral8302No ratings yet

- Pas 10 - Events After The Reporting PeriodDocument11 pagesPas 10 - Events After The Reporting PeriodBritnys Nim100% (1)

- Pas 10 - Events After The Reporting PeriodDocument10 pagesPas 10 - Events After The Reporting PeriodRuth Concepcion Fortu Crisanto-Batitis100% (2)

- Pas 10 Events After The Reporting PeriodDocument8 pagesPas 10 Events After The Reporting PeriodblesieqNo ratings yet

- Pas 10Document8 pagesPas 10Reen DomingoNo ratings yet

- Pas 10 - Events After The Reporting PeriodDocument8 pagesPas 10 - Events After The Reporting PeriodAnneNo ratings yet

- Pas 10 Events After The Reporting PeriodDocument11 pagesPas 10 Events After The Reporting PeriodReymond CadiligNo ratings yet

- Week 3 PAS 10Document11 pagesWeek 3 PAS 10abeladelmundosuarezNo ratings yet

- CFAS - Lec. 5 PAS 7, PAS8, PAS10Document28 pagesCFAS - Lec. 5 PAS 7, PAS8, PAS10latte aeriNo ratings yet

- Notes To FS - Part 1Document24 pagesNotes To FS - Part 1Precious Jireh100% (1)

- Chapte 4Document10 pagesChapte 4Mary Ann Alegria MorenoNo ratings yet

- Chapter 7 Notes Part 1Document24 pagesChapter 7 Notes Part 1AndreaaAAaa TagleNo ratings yet

- 2 Conceptual Framework For Financial ReportingDocument15 pages2 Conceptual Framework For Financial ReportingJohn Rey MorenoNo ratings yet

- (Intermediate Accounting 3) : Lecture AidDocument24 pages(Intermediate Accounting 3) : Lecture AidJackyline Magsino100% (2)

- PAS 34 - INTERIM FINANCIAL REPTG LectureDocument17 pagesPAS 34 - INTERIM FINANCIAL REPTG LectureMon RamNo ratings yet

- Events After The Reporting Period: Adjusting Events Non-Adjusting EventsDocument1 pageEvents After The Reporting Period: Adjusting Events Non-Adjusting EventsDora the ExplorerNo ratings yet

- Conceptual Framework: & Accounting StandardsDocument17 pagesConceptual Framework: & Accounting StandardsMichael Jack SalvadorNo ratings yet

- 2 - Conceptual Framework For Financial ReportingDocument13 pages2 - Conceptual Framework For Financial ReportingAresta, Novie MaeNo ratings yet

- Pas 29Document6 pagesPas 29AnneNo ratings yet

- Philippine Accounting Standards 10Document1 pagePhilippine Accounting Standards 10Catherine AguilarNo ratings yet

- Chapter 4 Events After Reporting PeriodDocument2 pagesChapter 4 Events After Reporting Periodsonchaenyoung2No ratings yet

- Pas 10Document1 pagePas 10Sacedon, Trishia Mae C.No ratings yet

- Pas 10 Events After The Reporting PeriodDocument1 pagePas 10 Events After The Reporting PeriodAcissej100% (1)

- Pas 7 - Statement of Cash Flows - W RecordingDocument14 pagesPas 7 - Statement of Cash Flows - W Recordingwendy alcoseba100% (1)

- E Ias 10Document15 pagesE Ias 10Daniel MNo ratings yet

- Pfrs 5 - Nca Held For Sale & Discontinued OpnsDocument23 pagesPfrs 5 - Nca Held For Sale & Discontinued OpnsAdrianIlagan100% (1)

- ACCA - F3 Chapter-19-1Document10 pagesACCA - F3 Chapter-19-1Nile NguyenNo ratings yet

- At.3217 - Completing The Audit and Post-Audit ResponsibilitiesDocument7 pagesAt.3217 - Completing The Audit and Post-Audit ResponsibilitiesDenny June CraususNo ratings yet

- Events After The Reporting PeriodDocument4 pagesEvents After The Reporting PeriodGlen JavellanaNo ratings yet

- CFAS - Lec. 9 PAS 21 and 23Document22 pagesCFAS - Lec. 9 PAS 21 and 23latte aeriNo ratings yet

- Topic 6 - Part 2 Event After Reporting Period - A232Document14 pagesTopic 6 - Part 2 Event After Reporting Period - A232balqisNo ratings yet

- Pas 7 - Statement of Cash FlowsDocument14 pagesPas 7 - Statement of Cash FlowsBritnys NimNo ratings yet

- Conceptual FrameworkDocument15 pagesConceptual FrameworkAnneNo ratings yet

- Ias 10 Events After The Reporting Period: Fact SheetDocument8 pagesIas 10 Events After The Reporting Period: Fact SheetRJNo ratings yet

- Module 017 Week006-Finacct3 Notes To The Financial StatementsDocument5 pagesModule 017 Week006-Finacct3 Notes To The Financial Statementsman ibeNo ratings yet

- Ifrs at A Glance: IAS 10 Events After The ReportingDocument4 pagesIfrs at A Glance: IAS 10 Events After The ReportingJozelle Grace PadelNo ratings yet

- Pas 21Document4 pagesPas 21AnneNo ratings yet

- Week 10 CfasDocument88 pagesWeek 10 Cfas2023303601No ratings yet

- Review of The Event After The Reporting PeriodDocument1 pageReview of The Event After The Reporting PeriodLu LacNo ratings yet

- IND AS On Fixed AssetsDocument1 pageIND AS On Fixed Assetschandrakumar k pNo ratings yet

- Pas 1 - Presentation of Financial Statements - RecordingDocument41 pagesPas 1 - Presentation of Financial Statements - Recordingwendy alcosebaNo ratings yet

- Week 10 CfasDocument121 pagesWeek 10 CfasblesieqNo ratings yet

- Pas 1 - Presentation of Financial StatementsDocument30 pagesPas 1 - Presentation of Financial StatementsClint Baring Arranchado100% (1)

- 2 Conceptual Framework For Financial Reporting 1Document46 pages2 Conceptual Framework For Financial Reporting 1Britnys Nim67% (3)

- CFAS - Lec. 2Document44 pagesCFAS - Lec. 2latte aeriNo ratings yet

- PAS 10 UpdatedDocument16 pagesPAS 10 Updatedadulusman501No ratings yet

- Summary Ias 10 EarpDocument3 pagesSummary Ias 10 EarpMuhammad Tufail DogarNo ratings yet

- Pas 8 - Acctg Policies, Changes in Acctg Estimates & ErrorsDocument14 pagesPas 8 - Acctg Policies, Changes in Acctg Estimates & ErrorsBritnys Nim100% (1)

- Nas 10Document11 pagesNas 10anujnepal9595No ratings yet

- Pas 8Document12 pagesPas 8carranchonickajoyNo ratings yet

- Subsequent Events PDFDocument1 pageSubsequent Events PDFMjhayeNo ratings yet

- Pas 8 - Acctg Policies, Changes in Acctg Estimates & ErrorsDocument14 pagesPas 8 - Acctg Policies, Changes in Acctg Estimates & ErrorsStephane Kate CaracaNo ratings yet

- CFAS - Lec. 12 PAS 29, 32Document31 pagesCFAS - Lec. 12 PAS 29, 32latte aeriNo ratings yet

- Final Exam ReviewDocument5 pagesFinal Exam ReviewBlake CrusiusNo ratings yet

- Events After The Reporting PeriodDocument1 pageEvents After The Reporting PeriodFaye RagosNo ratings yet

- IAS 10 - Events After Reporting DateDocument8 pagesIAS 10 - Events After Reporting DateKhuraim Abu BakrNo ratings yet

- Pas 10Document11 pagesPas 10Princess Jullyn ClaudioNo ratings yet

- Chapter 2 Completing The Audit Process Isa 560Document52 pagesChapter 2 Completing The Audit Process Isa 560黄勇添No ratings yet

- Operations Management - Lesson 3Document13 pagesOperations Management - Lesson 3Victoria ManalaysayNo ratings yet

- Understanding Quality: Operations ManagementDocument10 pagesUnderstanding Quality: Operations ManagementVictoria ManalaysayNo ratings yet

- Lesson 1: Orientation of The CourseDocument28 pagesLesson 1: Orientation of The CourseVictoria Manalaysay0% (1)

- Operation Management Lesson 1 ReviewerDocument3 pagesOperation Management Lesson 1 ReviewerVictoria ManalaysayNo ratings yet

- Operation Management Handout 1Document2 pagesOperation Management Handout 1Victoria ManalaysayNo ratings yet

- Problems in ProportionsDocument9 pagesProblems in ProportionsVictoria ManalaysayNo ratings yet

- Financial Sector Reforms - Meaning and ObjectivesDocument9 pagesFinancial Sector Reforms - Meaning and ObjectivesAmrit Kaur100% (1)

- FINS2624 Final Exam 2010 Semester 2Document22 pagesFINS2624 Final Exam 2010 Semester 2AnnabelleNo ratings yet

- Options PDFDocument8 pagesOptions PDFSAMRAT PAULNo ratings yet

- CMPC 311 Midterm ExaminationDocument13 pagesCMPC 311 Midterm ExaminationDjunah ArellanoNo ratings yet

- A3 - Venture Capital Readiness ChecklistDocument1 pageA3 - Venture Capital Readiness ChecklistPedro DuarteNo ratings yet

- Report On Working Capital ManagementDocument33 pagesReport On Working Capital ManagementSazib SarkarNo ratings yet

- Graham FormulasDocument2 pagesGraham FormulasKarri Krishna RaoNo ratings yet

- Lec01 SwayamDocument14 pagesLec01 Swayamkushal srivastavaNo ratings yet

- Acc406 - Aug 2021 - QDocument12 pagesAcc406 - Aug 2021 - Qtengku rilNo ratings yet

- RMD Unit VDocument11 pagesRMD Unit Vjagan rathodNo ratings yet

- Essentials of Corporate Finance Ross 8th Edition Solutions ManualDocument9 pagesEssentials of Corporate Finance Ross 8th Edition Solutions ManualJeffBrandtboqdx100% (44)

- Asian SessionDocument7 pagesAsian SessionKamil100% (1)

- Essentials of Corporate Finance 9Th Edition Ross Solutions Manual Full Chapter PDFDocument36 pagesEssentials of Corporate Finance 9Th Edition Ross Solutions Manual Full Chapter PDFroberto.mcdaniel967100% (10)

- 21 Useful Ways To Improve Your Trading System PDFDocument6 pages21 Useful Ways To Improve Your Trading System PDFJoe DNo ratings yet

- Revenue: Godfrey Hodgson Holmes TarcaDocument24 pagesRevenue: Godfrey Hodgson Holmes Tarcamichele hazelNo ratings yet

- GPS vs. TJX Financial AnalysisDocument12 pagesGPS vs. TJX Financial AnalysisBen Van NesteNo ratings yet

- Seeking AlphaDocument3 pagesSeeking AlphaboletodonNo ratings yet

- Provide An Investment Recommendation: Email To ManagementDocument1 pageProvide An Investment Recommendation: Email To Managementdavin nathanNo ratings yet

- Sbi Mutual Fund: SBI Magnum Children's Benefit Fund - Savings PlanDocument9 pagesSbi Mutual Fund: SBI Magnum Children's Benefit Fund - Savings PlanvvpvarunNo ratings yet

- Chap 4 BMADocument38 pagesChap 4 BMAGaurav SainiNo ratings yet

- Strategic Finance ManagementDocument8 pagesStrategic Finance ManagementShiv KothariNo ratings yet

- Componentization and Cost SegregationDocument1 pageComponentization and Cost SegregationRamanujam RaghavanNo ratings yet

- CA Final SFM Past Papers Theory !!!Document65 pagesCA Final SFM Past Papers Theory !!!sankalpyovaity999No ratings yet

- Tugas Pertemuan 4 - Alya Sufi Ikrima - 041911333248Document5 pagesTugas Pertemuan 4 - Alya Sufi Ikrima - 041911333248Alya Sufi Ikrima100% (1)

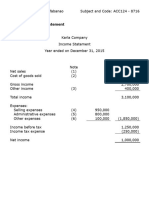

- ACC124 - Assignment On Income StatementDocument6 pagesACC124 - Assignment On Income StatementRuzuiNo ratings yet

- Chapter 3 Market EfficiencyDocument14 pagesChapter 3 Market EfficiencyMarian Mariez PacioNo ratings yet

- Marketing Analytics Antim PraharDocument12 pagesMarketing Analytics Antim Praharsakashsharma2799No ratings yet