Download as pptx, pdf, or txt

You might also like

- Savoury Snacks in Vietnam AnalysisDocument3 pagesSavoury Snacks in Vietnam AnalysisVõ Nguyễn Thu UyênNo ratings yet

- Working Capital Cocacola TOTAL PROJECT (1) - 1Document84 pagesWorking Capital Cocacola TOTAL PROJECT (1) - 1Gopi Nath75% (4)

- Pillsbury Cookie Case StudyDocument12 pagesPillsbury Cookie Case Studyvaibhav67% (6)

- Cadbury Dairy Milk - Marketing AssignmentDocument19 pagesCadbury Dairy Milk - Marketing AssignmentZoeb Eisa100% (2)

- Implementation of Management Information System in Kentucky Fried Chicken (KFC)Document18 pagesImplementation of Management Information System in Kentucky Fried Chicken (KFC)Satyabrata Sahu89% (37)

- Grocery Store Math WorksheetDocument3 pagesGrocery Store Math Worksheetkara laneNo ratings yet

- Typical Properties of Britesorb® L10Document1 pageTypical Properties of Britesorb® L10DhilNo ratings yet

- Final Project ReportDocument21 pagesFinal Project ReportSRIRAMA CHANDRANo ratings yet

- Pillsbury Case AnalysisDocument7 pagesPillsbury Case AnalysisKanishk GuptaNo ratings yet

- Marketing Plan: Pillsbury Cookie ChallengeDocument16 pagesMarketing Plan: Pillsbury Cookie ChallengeYash MittalNo ratings yet

- Executive Summary:: Advanced & Applied Business Research Pillsbury Cookie Challenge Due Date: 4 March 2013Document6 pagesExecutive Summary:: Advanced & Applied Business Research Pillsbury Cookie Challenge Due Date: 4 March 2013chacha_420100% (1)

- Pillsbury Cookie Challenge: By: Group-17P087-Keshav Gupta 17064-Aditya ChandarayanDocument6 pagesPillsbury Cookie Challenge: By: Group-17P087-Keshav Gupta 17064-Aditya ChandarayanKeshav GuptaNo ratings yet

- Pillsbury Cookie Challenge: by Group 9Document7 pagesPillsbury Cookie Challenge: by Group 9Aman UpadhyayNo ratings yet

- Marketing Management: Case: Cadbury BytesDocument5 pagesMarketing Management: Case: Cadbury BytesArnab RayNo ratings yet

- GhandourDocument22 pagesGhandourTarek Tomeh0% (3)

- How Consumers Are Faring Mid 2022Document5 pagesHow Consumers Are Faring Mid 2022Debmalya JanaNo ratings yet

- Section A - Group 7 - PillsburyDocument12 pagesSection A - Group 7 - PillsburyRahul DwivediNo ratings yet

- Coffee in The Philippines AnalysisDocument3 pagesCoffee in The Philippines AnalysisMyra Joanna ArceNo ratings yet

- Pillsbury Cookie ChallengeDocument5 pagesPillsbury Cookie ChallengeAkshay BrockNo ratings yet

- Cadbury Dairy MilkDocument20 pagesCadbury Dairy MilkSRIRAMA CHANDRANo ratings yet

- Case Study #2Document7 pagesCase Study #2alexandro.tovar10No ratings yet

- Term Paper PPT PlaceDocument37 pagesTerm Paper PPT PlaceNirmal ThapaNo ratings yet

- HMK CaseDocument15 pagesHMK CaseLinh Le Nguyen HongNo ratings yet

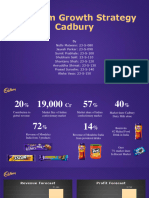

- Quantum Growth Strategy - CadburyDocument40 pagesQuantum Growth Strategy - CadburyPrasad SurosheNo ratings yet

- Pillsbury Challenge Case Paper PDFDocument14 pagesPillsbury Challenge Case Paper PDFRoman DiPasqualeNo ratings yet

- Project On Cadburychocolates: Made By:-GAURAV BULANI (10074) NIDHI SINGH (10118) ABHAY SINGH (10061)Document31 pagesProject On Cadburychocolates: Made By:-GAURAV BULANI (10074) NIDHI SINGH (10118) ABHAY SINGH (10061)abhaysingh7891100% (1)

- Assignment - (6A) Pilsbury Cookies SegmentDocument2 pagesAssignment - (6A) Pilsbury Cookies SegmentrizqighaniNo ratings yet

- Cad BuryDocument15 pagesCad Buryyash20987No ratings yet

- 9 Actionable Insights To Stay RelevantDocument25 pages9 Actionable Insights To Stay RelevantManish PatelNo ratings yet

- Final PPT CadburyDocument38 pagesFinal PPT CadburyChintan JainNo ratings yet

- Pillsbury WACDocument15 pagesPillsbury WACShahid Iqbal0% (1)

- YNCG Case Comp Group 2Document29 pagesYNCG Case Comp Group 2mintdang2020No ratings yet

- Cudbury IndiaDocument34 pagesCudbury IndiaritikNo ratings yet

- Parle G Presentation (Autosaved)Document13 pagesParle G Presentation (Autosaved)Priya JoshiNo ratings yet

- Marketing Presentation - Group 8Document16 pagesMarketing Presentation - Group 8VamsiKrishnaKondapuramNo ratings yet

- Grab SG Food and Grocery Trends 2022 RecapDocument45 pagesGrab SG Food and Grocery Trends 2022 RecapmischabartonNo ratings yet

- Case Study - Cadbury World: Submitted By: BSMA 1102 Group 9Document14 pagesCase Study - Cadbury World: Submitted By: BSMA 1102 Group 9Marie Remelyn AalaNo ratings yet

- Situation Analysis: Institute of Rural Management Anand PGDRM-42 Term II MMTDocument2 pagesSituation Analysis: Institute of Rural Management Anand PGDRM-42 Term II MMTanup kumarNo ratings yet

- Sunum BahcesehirUni Ocak2023Document23 pagesSunum BahcesehirUni Ocak2023selendenizeviNo ratings yet

- The Ice CreamDocument29 pagesThe Ice Creamassia.d.dimitrovaNo ratings yet

- 4 MR CasesDocument29 pages4 MR CasesAbdullahNo ratings yet

- Research Papers On Cadbury Dairy MilkDocument6 pagesResearch Papers On Cadbury Dairy Milkafnknlsjcpanrs100% (1)

- Cadbury Project ReportDocument26 pagesCadbury Project ReportMahendra PatadiaNo ratings yet

- Pillsbury Cookie ChallengeDocument7 pagesPillsbury Cookie ChallengeDeepta Guha100% (1)

- Fundamental of Marketing MKT410: U T M SDocument22 pagesFundamental of Marketing MKT410: U T M SRap DutaNo ratings yet

- Case Study 2 - Pillburys Cookie ChallengeDocument16 pagesCase Study 2 - Pillburys Cookie Challengesharmila0% (1)

- Cadbury India: Analysis of The Marketing StrategiesDocument15 pagesCadbury India: Analysis of The Marketing StrategiesRashi JainNo ratings yet

- Mccormick Case CompetitionDocument14 pagesMccormick Case Competitionapi-663792863No ratings yet

- St. Paul University Quezon CityDocument19 pagesSt. Paul University Quezon CityMarieLa OwanNo ratings yet

- 13 - Findings and Suggestions and ConclusionsDocument10 pages13 - Findings and Suggestions and ConclusionsAnimesh TiwariNo ratings yet

- Kazi Farm Kitchen in The Bakery IndustryDocument20 pagesKazi Farm Kitchen in The Bakery Industryshariar MasudNo ratings yet

- Relaunch Strategy of Cadbury's PicnicDocument67 pagesRelaunch Strategy of Cadbury's PicnicHeemanish MiddeNo ratings yet

- FINALDocument40 pagesFINALNayanshree JainNo ratings yet

- Cadbury Dairy Milk PresentationDocument18 pagesCadbury Dairy Milk PresentationAdil ArshadNo ratings yet

- Public Policy Club: India & Geo-Political Relationships Group 14Document9 pagesPublic Policy Club: India & Geo-Political Relationships Group 14chetan singhNo ratings yet

- Britannia ProjectDocument29 pagesBritannia Projectapi-379642975% (8)

- Cadbury ArticleDocument30 pagesCadbury ArticleBoaz EapenNo ratings yet

- Ict Jan-Feb 2022 (6) - 1-36Document3 pagesIct Jan-Feb 2022 (6) - 1-36Zaheer AbbasNo ratings yet

- The Amazon Roadmap: How Innovative Brands Are Reinventing The Path To MarketFrom EverandThe Amazon Roadmap: How Innovative Brands Are Reinventing The Path To MarketNo ratings yet

- The Smart Canadian's Guide to Saving Money: Pat Foran is On Your Side, Helping You to Stop Wasting Money, Start Saving It, and Build Your WealthFrom EverandThe Smart Canadian's Guide to Saving Money: Pat Foran is On Your Side, Helping You to Stop Wasting Money, Start Saving It, and Build Your WealthNo ratings yet

- Take The Robot Out of The Human: The 5 Essentials to Thrive in a New Digital WorldFrom EverandTake The Robot Out of The Human: The 5 Essentials to Thrive in a New Digital WorldNo ratings yet

- The Frugal Fabriholic: Your 12-Step Plan for Saving More Cash for Your Quilting StashFrom EverandThe Frugal Fabriholic: Your 12-Step Plan for Saving More Cash for Your Quilting StashNo ratings yet

- Family Inc.: Using Business Principles to Maximize Your Family's WealthFrom EverandFamily Inc.: Using Business Principles to Maximize Your Family's WealthRating: 5 out of 5 stars5/5 (1)

- PBL Bio Form4 Sem1 2023 .Document10 pagesPBL Bio Form4 Sem1 2023 .Never Gonna Give You UpNo ratings yet

- Cool Vietnam. Mid-2017 PDFDocument125 pagesCool Vietnam. Mid-2017 PDFDuc Pham Viet100% (1)

- How To Make Instant Noodle: Text 1Document3 pagesHow To Make Instant Noodle: Text 1Ferdian HardianataNo ratings yet

- Cac41 03eDocument2 pagesCac41 03eΕλενη ΚαρακωνσταντίνουNo ratings yet

- Jss1 Third Term English Lesson NoteDocument11 pagesJss1 Third Term English Lesson NoteSamuel Tobi David100% (4)

- E T.L.E 104 BTVTED: 2E-1 Home Economic Literacy My Porfolio: Submitted To Submitted byDocument22 pagesE T.L.E 104 BTVTED: 2E-1 Home Economic Literacy My Porfolio: Submitted To Submitted byTyronne FelicitasNo ratings yet

- SHARP CatalogueDocument20 pagesSHARP CataloguebaluNo ratings yet

- Editor: Lalsangliana Jt. Ed.: H.Document4 pagesEditor: Lalsangliana Jt. Ed.: H.bawihpuiapaNo ratings yet

- Abhi Al Ghani - Fase 3Document12 pagesAbhi Al Ghani - Fase 3Abhi Al GhaniNo ratings yet

- TLE Bread PastryProduction7 8 Week4Document4 pagesTLE Bread PastryProduction7 8 Week4Karen Joy Bobos CalNo ratings yet

- Unit 03Document11 pagesUnit 03QuanNo ratings yet

- Objective: Martin L. GriffinDocument4 pagesObjective: Martin L. GriffinMartin GriffinNo ratings yet

- Business Plan: Entrepreneurship ProjectDocument29 pagesBusiness Plan: Entrepreneurship ProjectÃpõõrv ShãrmãNo ratings yet

- Koica-Knu Master's Degree Program in Agricultural EngineeringDocument29 pagesKoica-Knu Master's Degree Program in Agricultural EngineeringFoudeNo ratings yet

- REAL Chart of AccountsDocument4 pagesREAL Chart of Accountsllerry racuya100% (1)

- Masha Sardari Nutrition ResumeDocument2 pagesMasha Sardari Nutrition Resumeapi-428097674No ratings yet

- Semi-Detailed Lesson PlanDocument2 pagesSemi-Detailed Lesson PlanitsmeJelly RoseNo ratings yet

- The Pittston Dispatch 12-30-2012Document76 pagesThe Pittston Dispatch 12-30-2012The Times LeaderNo ratings yet

- Risks and Benefits of Food Additives: Susan S. SumnerDocument16 pagesRisks and Benefits of Food Additives: Susan S. SumnertintfenNo ratings yet

- Naskah PublikasiDocument10 pagesNaskah PublikasiAna TasyaNo ratings yet

- Organizational Structure in A HotelDocument57 pagesOrganizational Structure in A HotelHope OLPINDANo ratings yet

- SOAP NoteDocument8 pagesSOAP NoteAnonymous p0y5mmLQNo ratings yet

- Tita Ma. Module 7Document18 pagesTita Ma. Module 7Vangeline UllaNo ratings yet

- 2015 Ndea CommitteeDocument5 pages2015 Ndea CommitteeMerben AlmioNo ratings yet

- The Rice Myth (Bohol Version)Document1 pageThe Rice Myth (Bohol Version)Shie La Santillan MedezNo ratings yet

- IELTS Listening Actual Tests and Answers 2021Document167 pagesIELTS Listening Actual Tests and Answers 2021Nguyễn Thảo PhươngNo ratings yet