Download as ppt, pdf, or txt

You might also like

- Invoice (2) 2022Document1 pageInvoice (2) 2022Lavish SoodNo ratings yet

- Investment Decision IDocument28 pagesInvestment Decision Isiddhant hingoraniNo ratings yet

- Net Present Value and Other Investment RulesDocument34 pagesNet Present Value and Other Investment Ruleskristina niaNo ratings yet

- Net Present Value and Other Investment RulesDocument34 pagesNet Present Value and Other Investment RulesArviandi AntariksaNo ratings yet

- NPV Yang DiperkirakanDocument34 pagesNPV Yang Diperkirakanalda warsidaNo ratings yet

- Net Present Value and Other Investment Rules: Mcgraw-Hill/IrwinDocument34 pagesNet Present Value and Other Investment Rules: Mcgraw-Hill/IrwinQUYÊN PHAN ĐÌNH PHƯƠNGNo ratings yet

- Chap 005Document34 pagesChap 005NazifahNo ratings yet

- Chap5 ModifiedDocument42 pagesChap5 ModifiedRuba AwwadNo ratings yet

- Net Present Value and Other Investment Rules: Mcgraw-Hill/IrwinDocument32 pagesNet Present Value and Other Investment Rules: Mcgraw-Hill/IrwinASAD ULLAHNo ratings yet

- Chapter 5 and 6 (Cont) : Net Present Value and Other Investment RulesDocument34 pagesChapter 5 and 6 (Cont) : Net Present Value and Other Investment Rulesphuphong777No ratings yet

- Ch.06 - FIN 322Document37 pagesCh.06 - FIN 322Bouchraya MilitoNo ratings yet

- NPV, Internal Rate of Return (IRR), and The Profitability Index (PI)Document24 pagesNPV, Internal Rate of Return (IRR), and The Profitability Index (PI)Sumbul JavedNo ratings yet

- Capital Budgeting: Part I Investment CriteriaDocument49 pagesCapital Budgeting: Part I Investment Criteriarani namdevNo ratings yet

- Some Alternative Investment RulesDocument32 pagesSome Alternative Investment RulesI Gede Artha WijayaNo ratings yet

- Some Alternative Investment Rules: Corporate FinanceDocument27 pagesSome Alternative Investment Rules: Corporate FinanceNguyễn Thùy LinhNo ratings yet

- Chapter 11 Capital BudgetingDocument36 pagesChapter 11 Capital BudgetingPrachi PragyaNo ratings yet

- Capital Budgeting Decision Rules: What Real Investments Should Firms Make?Document29 pagesCapital Budgeting Decision Rules: What Real Investments Should Firms Make?Durre NayabNo ratings yet

- Rules NTDocument25 pagesRules NTDaisy FlowerNo ratings yet

- Cost of Capital and Capital Budgeting TechniquesDocument23 pagesCost of Capital and Capital Budgeting TechniquesUmay PelitNo ratings yet

- FINA2010 Financial Management: Lecture 5: Capital Budgeting IIDocument46 pagesFINA2010 Financial Management: Lecture 5: Capital Budgeting IIWai Lam HsuNo ratings yet

- Chapter 05 Net Present Value and Other Investment Rules PDFDocument35 pagesChapter 05 Net Present Value and Other Investment Rules PDFWan Maulana AkbarNo ratings yet

- Lecture 6 - IRR (N)Document24 pagesLecture 6 - IRR (N)Ky DulzNo ratings yet

- Comparison of AlternativesDocument80 pagesComparison of AlternativesHashim HussenNo ratings yet

- Pitt - Edu Schlinge Fall99 L7docDocument40 pagesPitt - Edu Schlinge Fall99 L7docCheryl GanitNo ratings yet

- CH 6Document32 pagesCH 6Zead MahmoodNo ratings yet

- The Basics of Capital Budgeting: Should We Build This Plant?Document70 pagesThe Basics of Capital Budgeting: Should We Build This Plant?Jithin NairNo ratings yet

- CB TechniquesDocument55 pagesCB TechniquesRahul MoreNo ratings yet

- FINA2010 Lecture 5 - TaggedDocument41 pagesFINA2010 Lecture 5 - TaggedchankikivnNo ratings yet

- CF MergedDocument249 pagesCF MergedDhruv PatelNo ratings yet

- NPV & Other Investment Rules - RossDocument30 pagesNPV & Other Investment Rules - RossPrometheus Smith100% (1)

- Chapter 8 Investment Decision Making RulesDocument10 pagesChapter 8 Investment Decision Making RulesMaya ShibuNo ratings yet

- NPV & Other Investment Rules: ACTSC 372: Corporate Finance Winter 2021 Pengyu WeiDocument26 pagesNPV & Other Investment Rules: ACTSC 372: Corporate Finance Winter 2021 Pengyu WeiClaire ZhangNo ratings yet

- Chap05 FMDocument42 pagesChap05 FMDil RRNo ratings yet

- 4th Lecture Cont. - Capital BudgetingDocument35 pages4th Lecture Cont. - Capital Budgetingabdel hameed ibrahimNo ratings yet

- Chapter 4 CLC PDFDocument36 pagesChapter 4 CLC PDFHương ChuNo ratings yet

- MS 602 - Lec - Capital BudgetingDocument52 pagesMS 602 - Lec - Capital BudgetingGEORGENo ratings yet

- Chap 007-Net Present Value and Other Investment RulesDocument37 pagesChap 007-Net Present Value and Other Investment Rulessarvenaz kamali matinNo ratings yet

- Ufanpv Irr1.2Document45 pagesUfanpv Irr1.2mayankNo ratings yet

- Investment Decision RulesDocument45 pagesInvestment Decision RulesLee ChiaNo ratings yet

- Capital BudgetingDocument32 pagesCapital BudgetingKonstantinos DelaportasNo ratings yet

- Net Present Value: Mod. 4.3 VCMDocument27 pagesNet Present Value: Mod. 4.3 VCMPrincesNo ratings yet

- Net Present Value and Other Investment CriteriaDocument32 pagesNet Present Value and Other Investment CriteriaKids SocietyNo ratings yet

- Capital BudgetingDocument12 pagesCapital Budgetingola nasserNo ratings yet

- 02 Lecture8 Organized OrganizedDocument12 pages02 Lecture8 Organized Organizednimona asantiNo ratings yet

- Net Present Value and Other Investment Rules: Mcgraw-Hill/IrwinDocument34 pagesNet Present Value and Other Investment Rules: Mcgraw-Hill/Irwingizex2013No ratings yet

- Investment DecDocument29 pagesInvestment DecSajal BasuNo ratings yet

- 3 Investment Appraisal Discounted Cash Flow TechniquesDocument38 pages3 Investment Appraisal Discounted Cash Flow TechniquesR SidharthNo ratings yet

- Internal Rate of ReturnDocument24 pagesInternal Rate of ReturnantonydonNo ratings yet

- Lecture 6 - IRR (N)Document24 pagesLecture 6 - IRR (N)Maricar Salvador PenaNo ratings yet

- Some Alternative Investment RulesDocument27 pagesSome Alternative Investment Ruleslinda zyongweNo ratings yet

- Net Present Value and Other Investment CriteriaDocument72 pagesNet Present Value and Other Investment CriteriaAbdullah MujahidNo ratings yet

- Capital BudgetingDocument20 pagesCapital BudgetingrishiomkumarNo ratings yet

- Capital Budgeting Decision Rules: What Real Investments Should Firms Make?Document31 pagesCapital Budgeting Decision Rules: What Real Investments Should Firms Make?mkkaran90No ratings yet

- Net Present Value: Session 4Document27 pagesNet Present Value: Session 4Chenchen HanNo ratings yet

- Capital Budget - Summary Notes and QuestionsDocument22 pagesCapital Budget - Summary Notes and QuestionsClaudine ReidNo ratings yet

- Capital Budgeting Week 14 Unit 14.4Document8 pagesCapital Budgeting Week 14 Unit 14.4Syed HammadNo ratings yet

- Managerial Finance Group 2C Online Wednesday Mid Term Ahmed Mohamed Mohamed Ibrahem ID: 20122069Document9 pagesManagerial Finance Group 2C Online Wednesday Mid Term Ahmed Mohamed Mohamed Ibrahem ID: 20122069Ahmed Mohamed AwadNo ratings yet

- Investment Criteria ExDocument14 pagesInvestment Criteria ExMon ThuNo ratings yet

- ARR, IRR and PIDocument8 pagesARR, IRR and PIAli HamzaNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Chapter 6Document32 pagesChapter 6SyedAunRazaRizviNo ratings yet

- Chapter 4Document40 pagesChapter 4SyedAunRazaRizviNo ratings yet

- Interest Rates and Bond ValuationDocument43 pagesInterest Rates and Bond ValuationSyedAunRazaRizviNo ratings yet

- Chapter 4Document40 pagesChapter 4SyedAunRazaRizviNo ratings yet

- 11 D Inventory Management Problems KEYDocument3 pages11 D Inventory Management Problems KEYCharisse BuquidNo ratings yet

- A. Retno Fuji OktavianiDocument15 pagesA. Retno Fuji OktavianiTira KiranaNo ratings yet

- Union of India Vs Solar PesticidesDocument6 pagesUnion of India Vs Solar PesticidesRanvidsNo ratings yet

- General Catalogue Makita 2023 2024Document200 pagesGeneral Catalogue Makita 2023 2024mudNo ratings yet

- A Comparison of Forecasting Methods For Hotel Revenue ManagementDocument15 pagesA Comparison of Forecasting Methods For Hotel Revenue ManagementNathaniel TanNo ratings yet

- Update Proforma Invoice YYH220927Document3 pagesUpdate Proforma Invoice YYH220927jesus RodriguezNo ratings yet

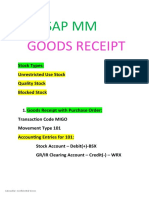

- Goods ReceiptDocument7 pagesGoods ReceiptghNo ratings yet

- Celpip Writing 8Document3 pagesCelpip Writing 8Learn TalkNo ratings yet

- Ashford MGT 330 Week 2 Assignment Starbucks StructureDocument2 pagesAshford MGT 330 Week 2 Assignment Starbucks StructureCharlotteNo ratings yet

- KAMANGA V HOLLARD INSURANCE BOTSWANA (PTY) LTD (2017) 1 BLR 359 (HC)Document5 pagesKAMANGA V HOLLARD INSURANCE BOTSWANA (PTY) LTD (2017) 1 BLR 359 (HC)Munyaradzi MusungoNo ratings yet

- 2390USD (EX-WORK) Includes: Optional Parts 120USD 10USD/PCS 10USD/PCS 15USD/PCSDocument6 pages2390USD (EX-WORK) Includes: Optional Parts 120USD 10USD/PCS 10USD/PCS 15USD/PCSMohamed IbrahemNo ratings yet

- Solved SSC CGL 2013 Tier 1 Paper With SolutionsDocument78 pagesSolved SSC CGL 2013 Tier 1 Paper With SolutionsNkavi SNo ratings yet

- Inner Circle Trader Ict Forex Ict NotesDocument110 pagesInner Circle Trader Ict Forex Ict NotesBurak AtlıNo ratings yet

- Country Dry SinkDocument4 pagesCountry Dry SinkjcpolicarpiNo ratings yet

- REBAR - BENDING - SCHEDULE - FORMAT - Yt - Google SheetsDocument2 pagesREBAR - BENDING - SCHEDULE - FORMAT - Yt - Google SheetsAZHA CLARICE VILLANUEVANo ratings yet

- Twitter & Agenda Setting - A Time Series Analysis of Public SalienceDocument1 pageTwitter & Agenda Setting - A Time Series Analysis of Public SalienceChrisJVargoNo ratings yet

- H04 System CablesDocument18 pagesH04 System CablesHoucinos TzNo ratings yet

- International Trade Literature ReviewDocument7 pagesInternational Trade Literature Reviewafdtalblw100% (1)

- Solutions For Non-Constant Growth Stock ValuationsDocument2 pagesSolutions For Non-Constant Growth Stock ValuationsNguyễn Bá Khánh TùngNo ratings yet

- HR Exam Question and Answer Paper For Competitive Exam - Exam ForumDocument5 pagesHR Exam Question and Answer Paper For Competitive Exam - Exam Forumdevarshi_shukla100% (2)

- Jabatan Bendahari: Tarikh Kredit Debit Keterangan Nombor Rujukan KampusDocument1 pageJabatan Bendahari: Tarikh Kredit Debit Keterangan Nombor Rujukan KampusArief HakimiNo ratings yet

- Chap 3 Resource Based View of FirmDocument34 pagesChap 3 Resource Based View of FirmAnshuNo ratings yet

- Tle 8 Periodical Test 2NDDocument3 pagesTle 8 Periodical Test 2NDLeymar MagudangNo ratings yet

- Monetary Policy and Its ComponentsDocument18 pagesMonetary Policy and Its Componentsrenisha gargNo ratings yet

- He Dressmaking Gr9 q1 Module-3Document16 pagesHe Dressmaking Gr9 q1 Module-3reymilyn zulueta100% (1)

- BY: Ynigesu Minchil Felekech Gizawu Selam Tesfaye Yohanis Petiros Ashenafi AshagrieDocument6 pagesBY: Ynigesu Minchil Felekech Gizawu Selam Tesfaye Yohanis Petiros Ashenafi AshagrieASHENAFI ASHAGRIENo ratings yet

- 2 Building Permit Front Back - DPWHDocument23 pages2 Building Permit Front Back - DPWHGretchen GuingabNo ratings yet

- Chapter 11 NISMDocument12 pagesChapter 11 NISMKiran VidhaniNo ratings yet

- Bank Reconciliation: Learning ObjectivesDocument15 pagesBank Reconciliation: Learning ObjectivesZunaeid Mahmud LamNo ratings yet