Download as pptx, pdf, or txt

You might also like

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- Boardwork Problem SolvingDocument6 pagesBoardwork Problem SolvingNorlijun V. HilutinNo ratings yet

- Rural Banking and Agricultural FinancingDocument17 pagesRural Banking and Agricultural FinancingNilanshi MukherjeeNo ratings yet

- This Paper Entitled 'RURAL FINANCING' Throws Light On The Following AspectsDocument6 pagesThis Paper Entitled 'RURAL FINANCING' Throws Light On The Following AspectshazursaranNo ratings yet

- Ms. E. Jeevitha: Rural BankingDocument16 pagesMs. E. Jeevitha: Rural Bankingpravin_kotecha7383100% (1)

- Nabard InterviewDocument7 pagesNabard InterviewAmit GodaraNo ratings yet

- Report 2Document31 pagesReport 2AravindNo ratings yet

- Proect Rural Banking in IndiaDocument108 pagesProect Rural Banking in IndiaRohitRana100% (5)

- Banking StructureDocument16 pagesBanking StructuresikandarNo ratings yet

- Finincial Analysis of Tumkur Grain Merchants Co-Operative BankDocument110 pagesFinincial Analysis of Tumkur Grain Merchants Co-Operative BankPrashanth PB50% (2)

- Analyzing Deposits and Loans 7 (AutoRecovered)Document18 pagesAnalyzing Deposits and Loans 7 (AutoRecovered)samritisaini1No ratings yet

- Rural Finance Study - Finance Presence in Rural India by RC&M IndiaDocument54 pagesRural Finance Study - Finance Presence in Rural India by RC&M Indiarcmindia_videoNo ratings yet

- Cooperative Banks: School of Law, Narsee Monjee Institute of Management Studies, BangaloreDocument13 pagesCooperative Banks: School of Law, Narsee Monjee Institute of Management Studies, BangaloreHIMANSHU GOYALNo ratings yet

- 09 Chapter 3Document40 pages09 Chapter 3kaviyaNo ratings yet

- Banking Law NotesDocument17 pagesBanking Law NotesgoluNo ratings yet

- Rural BankingDocument22 pagesRural BankingGungun KumariNo ratings yet

- 09 - Chapter 3 PDFDocument31 pages09 - Chapter 3 PDFPRASHANTAKUMARNo ratings yet

- Fin CA2Document9 pagesFin CA2Fizan NaikNo ratings yet

- Synopsis (Vikas)Document20 pagesSynopsis (Vikas)vikasbhardwaj18.v43No ratings yet

- Role of Cooperative Bank in AgriculturalDocument65 pagesRole of Cooperative Bank in Agriculturalkaushal244280% (5)

- What Is Co-OperationDocument15 pagesWhat Is Co-OperationManaswi Vidyadhar ShetyeNo ratings yet

- Insurance & Banking ProjectDocument15 pagesInsurance & Banking Projectfundoo16No ratings yet

- MathDocument9 pagesMathADITYA DESHMUKHNo ratings yet

- Vsit Rohit ProjectDocument10 pagesVsit Rohit ProjectNaresh KhutikarNo ratings yet

- National Bank For Agriculture and Rural DevelopmentDocument28 pagesNational Bank For Agriculture and Rural DevelopmentgeetaNo ratings yet

- Appl Ioed Eco8267827989Document6 pagesAppl Ioed Eco8267827989Meghna TripathiNo ratings yet

- Rural Banking & MicrofinanceDocument31 pagesRural Banking & MicrofinanceAshish AggarwalNo ratings yet

- Rural Banking - SCRIPTDocument16 pagesRural Banking - SCRIPTArchisha GargNo ratings yet

- National Bank For Agriculture and Rural Development (NABARD)Document2 pagesNational Bank For Agriculture and Rural Development (NABARD)122087041 YOGESHWAR DNo ratings yet

- History: India Mumbai Maharashtra AgricultureDocument5 pagesHistory: India Mumbai Maharashtra Agriculturesonål_gupta_26No ratings yet

- Nabard BankDocument60 pagesNabard Bankjaiswalpradeep507100% (3)

- Rural Banking and Financial Institions in INDIA PDFDocument20 pagesRural Banking and Financial Institions in INDIA PDFgowtham reddyNo ratings yet

- Agrifinance Assignment - TMPDocument14 pagesAgrifinance Assignment - TMPMANSHI RAINo ratings yet

- Euro CrisesDocument45 pagesEuro CrisesSupriya PatekarNo ratings yet

- Economics SEM 2 RPDocument13 pagesEconomics SEM 2 RPVansh Batch 2026No ratings yet

- Lead Bank SchemeDocument5 pagesLead Bank SchemeGopi ShankarNo ratings yet

- Co Operative BankDocument19 pagesCo Operative BankritzchavanNo ratings yet

- Co Operative BanksDocument4 pagesCo Operative BanksstarkishNo ratings yet

- Nabard Working CapitalDocument12 pagesNabard Working CapitalJaspreet SinghNo ratings yet

- Dr. Swapan Kumar Roy, Rural Development in India: What Roles Do Nabard & Rrbs Play?Document19 pagesDr. Swapan Kumar Roy, Rural Development in India: What Roles Do Nabard & Rrbs Play?ABHIJEETNo ratings yet

- Higher Financing InstitutionsDocument10 pagesHigher Financing InstitutionsApeksha GuruwadeyarNo ratings yet

- Sources of Agriculture FinanceDocument4 pagesSources of Agriculture Financeanjaligupta23102003No ratings yet

- Regional Rural BanksDocument4 pagesRegional Rural BanksSiddhartha BindalNo ratings yet

- "National Bank For Agriculture and Rural Development & Gujarat Agro Industries Corporation " Submitted ToDocument18 pages"National Bank For Agriculture and Rural Development & Gujarat Agro Industries Corporation " Submitted ToParthMairNo ratings yet

- Co-Operative Banks in IndiaDocument9 pagesCo-Operative Banks in Indiachaitali jadhavNo ratings yet

- Banking LAWDocument20 pagesBanking LAWRohit DangiNo ratings yet

- MBA Training ReportDocument69 pagesMBA Training ReportDeepak Thakur79% (14)

- Santhosh ProjectDocument60 pagesSanthosh Project2562923100% (1)

- NABARDDocument25 pagesNABARDAmit KumarNo ratings yet

- NABARDDocument5 pagesNABARDFlavia NunesNo ratings yet

- The Role of Nabard in Agriculture and Rural Development: An Parvesh Kumar GoyalDocument6 pagesThe Role of Nabard in Agriculture and Rural Development: An Parvesh Kumar GoyalRATHLOGICNo ratings yet

- Capital BudgetingDocument41 pagesCapital BudgetingLeela KrishnaNo ratings yet

- Chapter 1: IntroductionDocument22 pagesChapter 1: IntroductionVishakha RathodNo ratings yet

- Hiral Eco AssignmentDocument9 pagesHiral Eco Assignmentpradeep jadavNo ratings yet

- NABARD Organisational Set Up and Functions 556Document7 pagesNABARD Organisational Set Up and Functions 556sauravNo ratings yet

- National Bank For Agriculture and Rural Development (Nabard)Document7 pagesNational Bank For Agriculture and Rural Development (Nabard)LamheNo ratings yet

- National Bank For Agriculture and Rural Development - WikipediaDocument27 pagesNational Bank For Agriculture and Rural Development - Wikipediaryancar6100No ratings yet

- Agriculture FinanceDocument8 pagesAgriculture Financeramanpreet kaurNo ratings yet

- BankingDocument37 pagesBankingTanya GoelNo ratings yet

- PREET 2nd Project FinalDocument73 pagesPREET 2nd Project Final308 Kiranjeet KaurNo ratings yet

- Access to Finance: Microfinance Innovations in the People's Republic of ChinaFrom EverandAccess to Finance: Microfinance Innovations in the People's Republic of ChinaNo ratings yet

- NeoLiberalism and The Counter-EnlightenmentDocument26 pagesNeoLiberalism and The Counter-EnlightenmentvanathelNo ratings yet

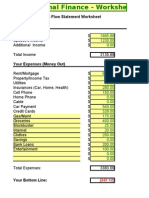

- Your Personal Cash Flow Statement Worksheet Income (Money In)Document4 pagesYour Personal Cash Flow Statement Worksheet Income (Money In)api-3831249No ratings yet

- Fab Plans CatDocument18 pagesFab Plans CatawatereautoservicesNo ratings yet

- Forms For Principal Borrower BDO LoanDocument8 pagesForms For Principal Borrower BDO LoanCha JavierNo ratings yet

- Presentation Report On Loans and AdvancesDocument20 pagesPresentation Report On Loans and AdvancesHawk AujlaNo ratings yet

- RA 9243 - Rationalizing The Provision of Documentary Stamp TaxDocument5 pagesRA 9243 - Rationalizing The Provision of Documentary Stamp TaxCrislene CruzNo ratings yet

- Ursa Minor-Course CurriculumDocument14 pagesUrsa Minor-Course CurriculumArvi SunNo ratings yet

- Kinds of MoneyDocument24 pagesKinds of MoneyIntet Nuestro100% (1)

- Impacting Digital Payments in India KPMG ReportDocument32 pagesImpacting Digital Payments in India KPMG Reportsaty16No ratings yet

- Establishment, Composition and Functions and Powers of NRBDocument15 pagesEstablishment, Composition and Functions and Powers of NRBMadan Shrestha100% (1)

- Credit CardDocument6 pagesCredit Cardredwanur_rahman2002No ratings yet

- ASEBA - Mtoken - GladstoneDocument2 pagesASEBA - Mtoken - GladstonesantiagomatamorosNo ratings yet

- FEE SCHEDULE 2017/2018: Cambridge IGCSE Curriculum Academic Year: August 2017 To July 2018Document1 pageFEE SCHEDULE 2017/2018: Cambridge IGCSE Curriculum Academic Year: August 2017 To July 2018anjanamenonNo ratings yet

- AtmDocument1 pageAtmmaheshNo ratings yet

- E-Mail - Bo3900@pnb - Co.in: Punjab National Bank International Banking Division Head Office:New Delhi Page 1 of 12Document12 pagesE-Mail - Bo3900@pnb - Co.in: Punjab National Bank International Banking Division Head Office:New Delhi Page 1 of 12kirpaldoadNo ratings yet

- Morocco: Financial System Stability Assessment-Update: International Monetary Fund Washington, D.CDocument41 pagesMorocco: Financial System Stability Assessment-Update: International Monetary Fund Washington, D.CPatsy CarterNo ratings yet

- Financial Market PDFDocument64 pagesFinancial Market PDFsnehachandan91No ratings yet

- Kivonat 20221130 049Document6 pagesKivonat 20221130 049didy dodoNo ratings yet

- On Environmental Factors Responsible For Idbi's PerformanceDocument53 pagesOn Environmental Factors Responsible For Idbi's PerformanceRushabh VoraNo ratings yet

- INV5606545Document11 pagesINV5606545mrgrayinthedarkNo ratings yet

- Guide For Contribution Payment Via Jompay: 3 Simple Steps On How To Use Jompay From Internet or Mobile BankingDocument8 pagesGuide For Contribution Payment Via Jompay: 3 Simple Steps On How To Use Jompay From Internet or Mobile BankingMohd AimanNo ratings yet

- Credit Manual: United Bank LimitedDocument120 pagesCredit Manual: United Bank LimitedAsif RafiNo ratings yet

- Test PDFDocument3 pagesTest PDFkazim4ualiNo ratings yet

- Contribution of Insurance Sector in Nepalese EconomyDocument10 pagesContribution of Insurance Sector in Nepalese EconomySharad Pyakurel100% (1)

- 19cse214: Theory of Computation: Case Study ReportDocument5 pages19cse214: Theory of Computation: Case Study ReportHarish RNo ratings yet

- MAGNO vs. CADocument2 pagesMAGNO vs. CAavocado booksNo ratings yet

- Case On Foreign Currency Deposit SecrecyDocument1 pageCase On Foreign Currency Deposit SecrecyJu BalajadiaNo ratings yet

- Assignment 1 Business & FinanceDocument4 pagesAssignment 1 Business & FinanceSan Lizas AirenNo ratings yet

- Request For Proposal To Do The Enrollment For Phase 2 All Over IndiaDocument118 pagesRequest For Proposal To Do The Enrollment For Phase 2 All Over Indiaarun_shakar511No ratings yet