Download as pptx, pdf, or txt

You might also like

- VZ - Verizon Communications IncDocument10 pagesVZ - Verizon Communications Incdantulo1234No ratings yet

- Pettet, Lowry & Reisberg's Company Law '12Document657 pagesPettet, Lowry & Reisberg's Company Law '12mamahannatuadamu100% (1)

- Financial Management 16th Edition Chapter 7Document32 pagesFinancial Management 16th Edition Chapter 7drcoolzNo ratings yet

- Analysis of Demat Account and Online TradingDocument70 pagesAnalysis of Demat Account and Online Tradingpraveen18866882% (11)

- Small & Payment Banks PPT FinalDocument12 pagesSmall & Payment Banks PPT FinalAakash JainNo ratings yet

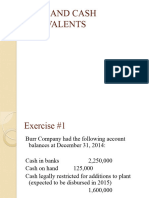

- Cash and Cash EquivalentDocument11 pagesCash and Cash EquivalentWilsonNo ratings yet

- L10FWF-PPIO& Redemptions-26April2014-1Document9 pagesL10FWF-PPIO& Redemptions-26April2014-1Garbo BentleyNo ratings yet

- Ausom - Spring 2021 Bsaf 5 - Commercial Banking and Lending Main PurposeDocument14 pagesAusom - Spring 2021 Bsaf 5 - Commercial Banking and Lending Main PurposeAlina ZubairNo ratings yet

- Ausom - Spring 2021 Bsaf 5 - Commercial Banking and Lending Main PurposeDocument16 pagesAusom - Spring 2021 Bsaf 5 - Commercial Banking and Lending Main PurposeAlina ZubairNo ratings yet

- Tutorial 8 QuestionsDocument6 pagesTutorial 8 QuestionsĐỗ Minh HuyềnNo ratings yet

- LiquidityDocument26 pagesLiquidityPallavi RanjanNo ratings yet

- Monetary Board: Activity 1Document6 pagesMonetary Board: Activity 1Ericka DeguzmanNo ratings yet

- FIN301 - Money, Banking & Interest RateDocument43 pagesFIN301 - Money, Banking & Interest RateCatherine Amor MontillaNo ratings yet

- Bsaf 5B CBL 7-12-20Document39 pagesBsaf 5B CBL 7-12-20Ahmed NiazNo ratings yet

- Types of Accounts, Bank Guarantee, LC, Line of CreditDocument44 pagesTypes of Accounts, Bank Guarantee, LC, Line of Creditkaren sunilNo ratings yet

- Lesson 1 AP: Minimum Composition of The SFP and Some Audit NotesDocument14 pagesLesson 1 AP: Minimum Composition of The SFP and Some Audit NotesDebs FanogaNo ratings yet

- Banking and LendingDocument38 pagesBanking and Lendingtech& GamingNo ratings yet

- Risk Management in Financial InstitutionDocument33 pagesRisk Management in Financial InstitutionIrish IceNo ratings yet

- Basel - Foreing Exchange-2022Document32 pagesBasel - Foreing Exchange-2022Salman AhmedNo ratings yet

- FSS Unit Iii 20 .3.14Document90 pagesFSS Unit Iii 20 .3.14GEETA72No ratings yet

- What Is Relationship Banking?Document36 pagesWhat Is Relationship Banking?llllkkkkNo ratings yet

- AFB Short NotesDocument5 pagesAFB Short Notesstudy studyNo ratings yet

- Cash and Cash Equivalents Problems For DiscussionDocument5 pagesCash and Cash Equivalents Problems For DiscussionchristineNo ratings yet

- Chapter 1 Cash and Cash EquivalentsDocument23 pagesChapter 1 Cash and Cash EquivalentsZeo AlcantaraNo ratings yet

- BDL Compared To FDL and EcbDocument60 pagesBDL Compared To FDL and EcbmaddikNo ratings yet

- NotesDocument30 pagesNotesMelinda LeeNo ratings yet

- Working Capital Finance Trade Credit, Bank Finance and Commercial PaperDocument105 pagesWorking Capital Finance Trade Credit, Bank Finance and Commercial PaperNishkushNo ratings yet

- Commercial BanksDocument7 pagesCommercial BanksMahealaniPerezNo ratings yet

- Liquidity ManagmentDocument37 pagesLiquidity ManagmentjahanNo ratings yet

- Banking Laws IIDocument34 pagesBanking Laws IIAmi UzukiNo ratings yet

- CBL Bsaf-5 7-7-20 S20Document45 pagesCBL Bsaf-5 7-7-20 S20HamzaNo ratings yet

- Chapter 1 Cash and Cash Equivalents Students Copy 2Document23 pagesChapter 1 Cash and Cash Equivalents Students Copy 2Shyra RiveraNo ratings yet

- File 1641790871 0004738 BLPDocument118 pagesFile 1641790871 0004738 BLPwww.ishusingh4420No ratings yet

- Fundmanagement 150509075339 Lva1 App6892Document21 pagesFundmanagement 150509075339 Lva1 App6892NILA CAYA TRINIDADNo ratings yet

- Bank Accounts and Credit SecuritiesDocument13 pagesBank Accounts and Credit SecuritiesJay Alcain OrpianoNo ratings yet

- Money and Banking (Econ 121) Problem Set 3 Answer Key Instructor: Chao WeiDocument3 pagesMoney and Banking (Econ 121) Problem Set 3 Answer Key Instructor: Chao WeiGgggggggNo ratings yet

- Modern Banking AnswersDocument10 pagesModern Banking AnswersAndalNo ratings yet

- Lesson 4Document60 pagesLesson 4ArthurNo ratings yet

- Chapter 3 Part 1Document6 pagesChapter 3 Part 1AliansNo ratings yet

- Ch8 MyLabDocument6 pagesCh8 MyLabJosue VitaleNo ratings yet

- Facets of Cash ManagementDocument6 pagesFacets of Cash Managementjustin lytanNo ratings yet

- 02 Financial MarketDocument86 pages02 Financial MarketAnuska JayswalNo ratings yet

- Cash and Cash EquivalentDocument5 pagesCash and Cash EquivalentMASIGLAT, CRIZEL JOY, Y.No ratings yet

- The Banking Firm and The Management of Financial Institutions The Bank Balance SheetDocument5 pagesThe Banking Firm and The Management of Financial Institutions The Bank Balance SheetChaituNo ratings yet

- NHTM2 CK DecuongDocument22 pagesNHTM2 CK DecuongGia BửuNo ratings yet

- Module 2Document57 pagesModule 2Tejaswini TejuNo ratings yet

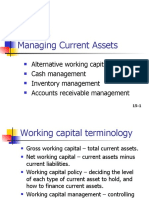

- FINBUSI Managing Current AssetsDocument52 pagesFINBUSI Managing Current AssetsRinna Lynn FraniNo ratings yet

- Cash ManagementDocument60 pagesCash ManagementAlif Khan100% (1)

- Cash and Cash EquivalentsDocument38 pagesCash and Cash EquivalentschristianallenmlagosNo ratings yet

- Chapter 2 Cash and Cash Equivalents PDFDocument21 pagesChapter 2 Cash and Cash Equivalents PDFVan TisbeNo ratings yet

- 5 - Topic5Managing - Current - Assets-EditedDocument47 pages5 - Topic5Managing - Current - Assets-EditedCOCONUTNo ratings yet

- Basic Banking: January 19, 2010Document39 pagesBasic Banking: January 19, 2010rushi_raut123182No ratings yet

- Pdic LawDocument27 pagesPdic LawEugene Carlo OntolanNo ratings yet

- Introduction To Banking SystemsDocument16 pagesIntroduction To Banking SystemsSagar AnsaryNo ratings yet

- Topic 2 Depository in SDocument5 pagesTopic 2 Depository in SNayr RomzNo ratings yet

- Analysis of Financial StatementsDocument17 pagesAnalysis of Financial StatementsRajesh PatilNo ratings yet

- Yawa PerdDocument8 pagesYawa Perdyawi diskatersNo ratings yet

- Private Placement Programs.2020 (1) - 1Document5 pagesPrivate Placement Programs.2020 (1) - 1azay100% (1)

- T10 Managing Finance Notes by SeahDocument43 pagesT10 Managing Finance Notes by SeahSeah Chooi KhengNo ratings yet

- Chap 012 BBDocument8 pagesChap 012 BBMyaNo ratings yet

- Commercial Banking Lending Policies of Banks and FisDocument47 pagesCommercial Banking Lending Policies of Banks and Fisrahul8909No ratings yet

- Commercial BankingDocument35 pagesCommercial BankingAJ SAN JUANNo ratings yet

- Agent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaFrom EverandAgent Banking Uganda Handbook: A simple guide to starting and running a profitable agent banking business in UgandaNo ratings yet

- The Global Liquidity Tracker - 17 Jun 22Document9 pagesThe Global Liquidity Tracker - 17 Jun 22Apurva ShethNo ratings yet

- She Accounting (Uploaded)Document2 pagesShe Accounting (Uploaded)Kim HoranNo ratings yet

- Terms and Conditions EToroDocument35 pagesTerms and Conditions ETorokillaruna04No ratings yet

- Consumer Credit February 14, 2011Document23 pagesConsumer Credit February 14, 2011arithzNo ratings yet

- Mco 04 em PDFDocument8 pagesMco 04 em PDFFirdosh Khan67% (3)

- Global Public MA Guide PDFDocument741 pagesGlobal Public MA Guide PDFRafael Ernesto Ponce PérezNo ratings yet

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToMurthy KarumuriNo ratings yet

- Final Project Report On Study Of: "Techniques Used For Credit Assessment"Document68 pagesFinal Project Report On Study Of: "Techniques Used For Credit Assessment"nishant oraonNo ratings yet

- Handbook of Income Tax (HIT) by Farid Mohmmad NasirDocument43 pagesHandbook of Income Tax (HIT) by Farid Mohmmad NasirPiyal HossainNo ratings yet

- A Study On Working Capital Mang On Maruti SuzukiDocument40 pagesA Study On Working Capital Mang On Maruti SuzukiDanika RajeshwariNo ratings yet

- Vikas Maheshwari 05106Document92 pagesVikas Maheshwari 05106Raju Cool100% (1)

- Product Booklet English VersionDocument88 pagesProduct Booklet English VersionUday Gopal100% (2)

- NYS V Trump Exhibit July 30, 2012 Letter From Deutsche Bank To CushmanDocument4 pagesNYS V Trump Exhibit July 30, 2012 Letter From Deutsche Bank To CushmanFile 411No ratings yet

- Capital Markets Fundamentals - Ethiopian ContextDocument50 pagesCapital Markets Fundamentals - Ethiopian ContextHub TechnologyNo ratings yet

- Stock Market: An Index of Economic GrowthDocument51 pagesStock Market: An Index of Economic GrowthishanjandNo ratings yet

- Non-Banking Financial CompanyDocument36 pagesNon-Banking Financial CompanyDipak MahalikNo ratings yet

- Law - Insider - As Indenture Trustee Exchange Administrator and - Filed - 05 05 2020 - Contract PDFDocument96 pagesLaw - Insider - As Indenture Trustee Exchange Administrator and - Filed - 05 05 2020 - Contract PDFBunny Fontaine100% (2)

- SEC Opinion 10-34Document2 pagesSEC Opinion 10-34Tina Reyes-BattadNo ratings yet

- Project On NJ India Invest PVT LTDDocument77 pagesProject On NJ India Invest PVT LTDHatim Ali100% (1)

- Mc0 Initial Public OfferingsDocument558 pagesMc0 Initial Public Offeringspetertang2003No ratings yet

- Project Work: Indian Financial System (Ifs)Document20 pagesProject Work: Indian Financial System (Ifs)Vijetha MadhavarapuNo ratings yet

- 1) SEBI Issue of Capital and Disclosure Requirements (ICDR) Regulations 2009Document12 pages1) SEBI Issue of Capital and Disclosure Requirements (ICDR) Regulations 2009Shasha GuptaNo ratings yet

- Motial Oswal India Excellence (Mid To Mega)Document29 pagesMotial Oswal India Excellence (Mid To Mega)SandyNo ratings yet

- 1.1 Introduction To The Stock MarketDocument4 pages1.1 Introduction To The Stock MarketYesaswiniNo ratings yet

- Graham High Yield and Safe Investments 1918Document5 pagesGraham High Yield and Safe Investments 1918Francisco MaassNo ratings yet

- EPD - Schwab PDFDocument16 pagesEPD - Schwab PDFJeff SturgeonNo ratings yet