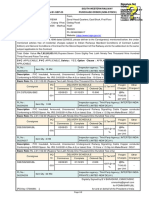

GST at A Glance

GST at A Glance

You might also like

- PW37196 34541005Document2 pagesPW37196 34541005rajan singhNo ratings yet

- Salary Sheet (Jestha) - Amar ThakurDocument1 pageSalary Sheet (Jestha) - Amar ThakurAmar ThakurNo ratings yet

- GST Law in Brief and Chart 2021Document18 pagesGST Law in Brief and Chart 2021sukumar basuNo ratings yet

- GST PPT Intro (1) - MergedDocument47 pagesGST PPT Intro (1) - MergedRahulNo ratings yet

- Overview of GSTDocument25 pagesOverview of GSTjugr57No ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- Cross Border B2C (Business To Consumer) Services Provided in Taxable Territory Cross Border B2B (Business To Business) Services OidarDocument16 pagesCross Border B2C (Business To Consumer) Services Provided in Taxable Territory Cross Border B2B (Business To Business) Services OidarSushant SaxenaNo ratings yet

- Chapter 1-6Document16 pagesChapter 1-6adityanagar3333No ratings yet

- GST Oct 17Document23 pagesGST Oct 17himanNo ratings yet

- SyllabusDocument17 pagesSyllabusHarsh ShahNo ratings yet

- Goods and Service TaxDocument30 pagesGoods and Service TaxR.SUDHIR RameshNo ratings yet

- Ca Inter GST Module 1Document46 pagesCa Inter GST Module 1sukritisuman2No ratings yet

- GST NotesDocument156 pagesGST NotesNishthaNo ratings yet

- GST ExplainedDocument8 pagesGST Explainedvikashchoudhary22082002No ratings yet

- What Is GST?: Goods and Service TaxDocument11 pagesWhat Is GST?: Goods and Service TaxAditya ChitaliyaNo ratings yet

- Budget Proposal - 2O24Document12 pagesBudget Proposal - 2O24tkgeneral12No ratings yet

- Presentation ON: Goods and Service Tax: Applicability, Itc and ReturnsDocument31 pagesPresentation ON: Goods and Service Tax: Applicability, Itc and ReturnsSonal AggarwalNo ratings yet

- Overview GSTDocument56 pagesOverview GSTrahulNo ratings yet

- RegistrationDocument2 pagesRegistrationSandana PrajapatiNo ratings yet

- GST BasicsDocument56 pagesGST BasicsrahulNo ratings yet

- GST and Salary NotesDocument99 pagesGST and Salary NotesIsha ParwaniNo ratings yet

- LAW Related-GST PresentationDocument137 pagesLAW Related-GST PresentationshreyasNo ratings yet

- Goods and Services Tax - 2021Document43 pagesGoods and Services Tax - 2021gsvighneshnairNo ratings yet

- Valuable Consideration: Made SupplyDocument22 pagesValuable Consideration: Made SupplyJaihindNo ratings yet

- By Damodar Agrawal & Associates: Damodar06@yahoo - Co.inDocument374 pagesBy Damodar Agrawal & Associates: Damodar06@yahoo - Co.inNiteshNo ratings yet

- Unit4. Taxation System in IndiaDocument35 pagesUnit4. Taxation System in IndiaAakankshaNo ratings yet

- GST Unit 1Document52 pagesGST Unit 1SANSKRITI YADAV 22DM236No ratings yet

- GST Note - V2Document8 pagesGST Note - V2Pratik GosaviNo ratings yet

- Goods & Service TaxDocument13 pagesGoods & Service TaxRajeev RanjanNo ratings yet

- Basics of GSTDocument40 pagesBasics of GSTsportnik.in100% (1)

- Book 2Document34 pagesBook 2Kritika JainNo ratings yet

- Chapter 9 - RegistrationDocument20 pagesChapter 9 - Registrationcloudhunter910No ratings yet

- Overview of GST - PPT For GACDocument57 pagesOverview of GST - PPT For GACRonak DesaiNo ratings yet

- TDS Rates 2022-2023Document3 pagesTDS Rates 2022-2023George K SonyNo ratings yet

- GST Implication 17Document14 pagesGST Implication 17Priyadarshan KrishnaNo ratings yet

- Basic Hints For GSTDocument42 pagesBasic Hints For GSTReeni SamuelNo ratings yet

- GST FrameworkDocument21 pagesGST FrameworkExecutive EngineerNo ratings yet

- Goods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLADocument30 pagesGoods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLAKrishna ShuklaNo ratings yet

- Goods and Services Tax (GST) in IndiaDocument30 pagesGoods and Services Tax (GST) in IndiarupalNo ratings yet

- Goods and Services Tax (GST) Presentation To The Members of GJEPCDocument53 pagesGoods and Services Tax (GST) Presentation To The Members of GJEPCAnkita TomarNo ratings yet

- GST OverviewDocument18 pagesGST Overviewrathoursoumya1305No ratings yet

- Composition SchemeDocument2 pagesComposition SchemeMadhur MadnaniNo ratings yet

- TYBAF 157 ReddhiVaru SemV IndirectTaxesDocument6 pagesTYBAF 157 ReddhiVaru SemV IndirectTaxesjaimin vasaniNo ratings yet

- Topic 9 - Registration Under GSTDocument4 pagesTopic 9 - Registration Under GSTMehul GuptaNo ratings yet

- GSTDocument42 pagesGSTSwarga Santosh Mohanty100% (1)

- Composition SchemeDocument2 pagesComposition SchemeMadhur MadnaniNo ratings yet

- Presentation On GSTDocument24 pagesPresentation On GSTsajidneki365No ratings yet

- Chp 7 - Composition scheme final (1)Document7 pagesChp 7 - Composition scheme final (1)sunraypower2010No ratings yet

- GST RegistrationDocument4 pagesGST RegistrationJCGCFGCGNo ratings yet

- Overview of GST Model GST Law Meaning Scope of SupplyDocument47 pagesOverview of GST Model GST Law Meaning Scope of SupplyShubham More CenationNo ratings yet

- GST BasicDocument47 pagesGST BasicRachna khuranaNo ratings yet

- AMFI GST FAQsDocument12 pagesAMFI GST FAQsMargi PatelNo ratings yet

- Registration: GlimpsesDocument12 pagesRegistration: GlimpsesAdventure TimeNo ratings yet

- Chapter I: Implementation of GSTDocument23 pagesChapter I: Implementation of GSTTax NatureNo ratings yet

- Impacts of GST On Indian EconomyDocument14 pagesImpacts of GST On Indian EconomyR.Deepak KannaNo ratings yet

- GST SupplyDocument15 pagesGST SupplySaloni KejdiwalNo ratings yet

- Goods and Service Tax (GST)Document17 pagesGoods and Service Tax (GST)Manav SethiNo ratings yet

- CA INTER IDT-GSTBOOK PNNDocument8 pagesCA INTER IDT-GSTBOOK PNNshivam kharivale 55No ratings yet

- Goods and Services Tax (GST) in India: CA. Preeti GoyalDocument30 pagesGoods and Services Tax (GST) in India: CA. Preeti GoyalArvind PalNo ratings yet

- Provisions of GST Effective From 1St April 2019Document3 pagesProvisions of GST Effective From 1St April 2019Giri SukumarNo ratings yet

- Finance Act Tax Handbook 2023Document33 pagesFinance Act Tax Handbook 2023TANVEER HUSSAINNo ratings yet

- Revenue Memorandum Circular 36-2021 v2Document32 pagesRevenue Memorandum Circular 36-2021 v2lizzyNo ratings yet

- 2018 Income Tax QDocument4 pages2018 Income Tax QlightNo ratings yet

- Final On Passive Income Grcbarbin2Document6 pagesFinal On Passive Income Grcbarbin2Joneric RamosNo ratings yet

- Vat Part IDocument37 pagesVat Part IXhin CagatinNo ratings yet

- Rewarded: 2010 Employee Stock Purchase Plan (ESPP) GuideDocument16 pagesRewarded: 2010 Employee Stock Purchase Plan (ESPP) GuidedeederushaNo ratings yet

- Cross RatesDocument1 pageCross RatesTiso Blackstar GroupNo ratings yet

- Notice: Accessing Student Financing ServicesDocument1 pageNotice: Accessing Student Financing ServicesLamar TaylorNo ratings yet

- English PB 23Document2 pagesEnglish PB 23bilal mustafa100% (1)

- IRS Publication Form 8867Document4 pagesIRS Publication Form 8867Francis Wolfgang UrbanNo ratings yet

- CIR Vs Pineda DigestDocument1 pageCIR Vs Pineda DigestRoz Lourdiz CamachoNo ratings yet

- Itr 1 FormatDocument3 pagesItr 1 FormatPawanNo ratings yet

- Irs Form 1099 Misc PDFDocument8 pagesIrs Form 1099 Misc PDFMikhael Yah-Shah Dean: VeilourNo ratings yet

- Computaion Pre FinalDocument4 pagesComputaion Pre FinalPaupauNo ratings yet

- Digital Order SummaryDocument2 pagesDigital Order SummaryDiego Alonso Herrera HernándezNo ratings yet

- E-Auctions - MSTC Limited-BelghoriaDocument8 pagesE-Auctions - MSTC Limited-BelghoriamannakauNo ratings yet

- Accounting For Income TaxDocument4 pagesAccounting For Income TaxMjhayeNo ratings yet

- Local Business Tax (Notes)Document8 pagesLocal Business Tax (Notes)Y P Dela PeñaNo ratings yet

- PayslipDocument2 pagesPayslipbrij18No ratings yet

- Transfer PricingDocument6 pagesTransfer Pricingrpulgam09No ratings yet

- Vit Men'S Hostel: CircularDocument6 pagesVit Men'S Hostel: CircularSoumyajyoti MukherjeeNo ratings yet

- MM - Brazil - Fiscal - Book - Mastersaf 2 1Document30 pagesMM - Brazil - Fiscal - Book - Mastersaf 2 1guroyalNo ratings yet

- CAT Rules Against Grossing Up Method On PAYE - 3Document3 pagesCAT Rules Against Grossing Up Method On PAYE - 3vicenza-marie FukoNo ratings yet

- Boat Headphone InvoiceDocument1 pageBoat Headphone InvoiceShashank Tripathi100% (1)

- 19 C New PO 56235256201449 DT 01-SEP-23 On VINDHYA TELELINKS LIMITED-REWADocument8 pages19 C New PO 56235256201449 DT 01-SEP-23 On VINDHYA TELELINKS LIMITED-REWAManojNo ratings yet

- Samara University College of Business and Economics Department of Accounting and FinanceDocument51 pagesSamara University College of Business and Economics Department of Accounting and FinanceAllis WellNo ratings yet

- Account Statement 22 Aug 2023-22 Aug 2023Document2 pagesAccount Statement 22 Aug 2023-22 Aug 2023PRONAB MAJHINo ratings yet

- Invoice Shalter BatugadeDocument8 pagesInvoice Shalter BatugadeFuri HZNo ratings yet

Download as pptx, pdf, or txt

You might also like

- PW37196 34541005Document2 pagesPW37196 34541005rajan singhNo ratings yet

- Salary Sheet (Jestha) - Amar ThakurDocument1 pageSalary Sheet (Jestha) - Amar ThakurAmar ThakurNo ratings yet

- GST Law in Brief and Chart 2021Document18 pagesGST Law in Brief and Chart 2021sukumar basuNo ratings yet

- GST PPT Intro (1) - MergedDocument47 pagesGST PPT Intro (1) - MergedRahulNo ratings yet

- Overview of GSTDocument25 pagesOverview of GSTjugr57No ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- Presentation On : Kiet Group of InstitutionsDocument27 pagesPresentation On : Kiet Group of InstitutionsVaishali SharmaNo ratings yet

- Cross Border B2C (Business To Consumer) Services Provided in Taxable Territory Cross Border B2B (Business To Business) Services OidarDocument16 pagesCross Border B2C (Business To Consumer) Services Provided in Taxable Territory Cross Border B2B (Business To Business) Services OidarSushant SaxenaNo ratings yet

- Chapter 1-6Document16 pagesChapter 1-6adityanagar3333No ratings yet

- GST Oct 17Document23 pagesGST Oct 17himanNo ratings yet

- SyllabusDocument17 pagesSyllabusHarsh ShahNo ratings yet

- Goods and Service TaxDocument30 pagesGoods and Service TaxR.SUDHIR RameshNo ratings yet

- Ca Inter GST Module 1Document46 pagesCa Inter GST Module 1sukritisuman2No ratings yet

- GST NotesDocument156 pagesGST NotesNishthaNo ratings yet

- GST ExplainedDocument8 pagesGST Explainedvikashchoudhary22082002No ratings yet

- What Is GST?: Goods and Service TaxDocument11 pagesWhat Is GST?: Goods and Service TaxAditya ChitaliyaNo ratings yet

- Budget Proposal - 2O24Document12 pagesBudget Proposal - 2O24tkgeneral12No ratings yet

- Presentation ON: Goods and Service Tax: Applicability, Itc and ReturnsDocument31 pagesPresentation ON: Goods and Service Tax: Applicability, Itc and ReturnsSonal AggarwalNo ratings yet

- Overview GSTDocument56 pagesOverview GSTrahulNo ratings yet

- RegistrationDocument2 pagesRegistrationSandana PrajapatiNo ratings yet

- GST BasicsDocument56 pagesGST BasicsrahulNo ratings yet

- GST and Salary NotesDocument99 pagesGST and Salary NotesIsha ParwaniNo ratings yet

- LAW Related-GST PresentationDocument137 pagesLAW Related-GST PresentationshreyasNo ratings yet

- Goods and Services Tax - 2021Document43 pagesGoods and Services Tax - 2021gsvighneshnairNo ratings yet

- Valuable Consideration: Made SupplyDocument22 pagesValuable Consideration: Made SupplyJaihindNo ratings yet

- By Damodar Agrawal & Associates: Damodar06@yahoo - Co.inDocument374 pagesBy Damodar Agrawal & Associates: Damodar06@yahoo - Co.inNiteshNo ratings yet

- Unit4. Taxation System in IndiaDocument35 pagesUnit4. Taxation System in IndiaAakankshaNo ratings yet

- GST Unit 1Document52 pagesGST Unit 1SANSKRITI YADAV 22DM236No ratings yet

- GST Note - V2Document8 pagesGST Note - V2Pratik GosaviNo ratings yet

- Goods & Service TaxDocument13 pagesGoods & Service TaxRajeev RanjanNo ratings yet

- Basics of GSTDocument40 pagesBasics of GSTsportnik.in100% (1)

- Book 2Document34 pagesBook 2Kritika JainNo ratings yet

- Chapter 9 - RegistrationDocument20 pagesChapter 9 - Registrationcloudhunter910No ratings yet

- Overview of GST - PPT For GACDocument57 pagesOverview of GST - PPT For GACRonak DesaiNo ratings yet

- TDS Rates 2022-2023Document3 pagesTDS Rates 2022-2023George K SonyNo ratings yet

- GST Implication 17Document14 pagesGST Implication 17Priyadarshan KrishnaNo ratings yet

- Basic Hints For GSTDocument42 pagesBasic Hints For GSTReeni SamuelNo ratings yet

- GST FrameworkDocument21 pagesGST FrameworkExecutive EngineerNo ratings yet

- Goods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLADocument30 pagesGoods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLAKrishna ShuklaNo ratings yet

- Goods and Services Tax (GST) in IndiaDocument30 pagesGoods and Services Tax (GST) in IndiarupalNo ratings yet

- Goods and Services Tax (GST) Presentation To The Members of GJEPCDocument53 pagesGoods and Services Tax (GST) Presentation To The Members of GJEPCAnkita TomarNo ratings yet

- GST OverviewDocument18 pagesGST Overviewrathoursoumya1305No ratings yet

- Composition SchemeDocument2 pagesComposition SchemeMadhur MadnaniNo ratings yet

- TYBAF 157 ReddhiVaru SemV IndirectTaxesDocument6 pagesTYBAF 157 ReddhiVaru SemV IndirectTaxesjaimin vasaniNo ratings yet

- Topic 9 - Registration Under GSTDocument4 pagesTopic 9 - Registration Under GSTMehul GuptaNo ratings yet

- GSTDocument42 pagesGSTSwarga Santosh Mohanty100% (1)

- Composition SchemeDocument2 pagesComposition SchemeMadhur MadnaniNo ratings yet

- Presentation On GSTDocument24 pagesPresentation On GSTsajidneki365No ratings yet

- Chp 7 - Composition scheme final (1)Document7 pagesChp 7 - Composition scheme final (1)sunraypower2010No ratings yet

- GST RegistrationDocument4 pagesGST RegistrationJCGCFGCGNo ratings yet

- Overview of GST Model GST Law Meaning Scope of SupplyDocument47 pagesOverview of GST Model GST Law Meaning Scope of SupplyShubham More CenationNo ratings yet

- GST BasicDocument47 pagesGST BasicRachna khuranaNo ratings yet

- AMFI GST FAQsDocument12 pagesAMFI GST FAQsMargi PatelNo ratings yet

- Registration: GlimpsesDocument12 pagesRegistration: GlimpsesAdventure TimeNo ratings yet

- Chapter I: Implementation of GSTDocument23 pagesChapter I: Implementation of GSTTax NatureNo ratings yet

- Impacts of GST On Indian EconomyDocument14 pagesImpacts of GST On Indian EconomyR.Deepak KannaNo ratings yet

- GST SupplyDocument15 pagesGST SupplySaloni KejdiwalNo ratings yet

- Goods and Service Tax (GST)Document17 pagesGoods and Service Tax (GST)Manav SethiNo ratings yet

- CA INTER IDT-GSTBOOK PNNDocument8 pagesCA INTER IDT-GSTBOOK PNNshivam kharivale 55No ratings yet

- Goods and Services Tax (GST) in India: CA. Preeti GoyalDocument30 pagesGoods and Services Tax (GST) in India: CA. Preeti GoyalArvind PalNo ratings yet

- Provisions of GST Effective From 1St April 2019Document3 pagesProvisions of GST Effective From 1St April 2019Giri SukumarNo ratings yet

- Finance Act Tax Handbook 2023Document33 pagesFinance Act Tax Handbook 2023TANVEER HUSSAINNo ratings yet

- Revenue Memorandum Circular 36-2021 v2Document32 pagesRevenue Memorandum Circular 36-2021 v2lizzyNo ratings yet

- 2018 Income Tax QDocument4 pages2018 Income Tax QlightNo ratings yet

- Final On Passive Income Grcbarbin2Document6 pagesFinal On Passive Income Grcbarbin2Joneric RamosNo ratings yet

- Vat Part IDocument37 pagesVat Part IXhin CagatinNo ratings yet

- Rewarded: 2010 Employee Stock Purchase Plan (ESPP) GuideDocument16 pagesRewarded: 2010 Employee Stock Purchase Plan (ESPP) GuidedeederushaNo ratings yet

- Cross RatesDocument1 pageCross RatesTiso Blackstar GroupNo ratings yet

- Notice: Accessing Student Financing ServicesDocument1 pageNotice: Accessing Student Financing ServicesLamar TaylorNo ratings yet

- English PB 23Document2 pagesEnglish PB 23bilal mustafa100% (1)

- IRS Publication Form 8867Document4 pagesIRS Publication Form 8867Francis Wolfgang UrbanNo ratings yet

- CIR Vs Pineda DigestDocument1 pageCIR Vs Pineda DigestRoz Lourdiz CamachoNo ratings yet

- Itr 1 FormatDocument3 pagesItr 1 FormatPawanNo ratings yet

- Irs Form 1099 Misc PDFDocument8 pagesIrs Form 1099 Misc PDFMikhael Yah-Shah Dean: VeilourNo ratings yet

- Computaion Pre FinalDocument4 pagesComputaion Pre FinalPaupauNo ratings yet

- Digital Order SummaryDocument2 pagesDigital Order SummaryDiego Alonso Herrera HernándezNo ratings yet

- E-Auctions - MSTC Limited-BelghoriaDocument8 pagesE-Auctions - MSTC Limited-BelghoriamannakauNo ratings yet

- Accounting For Income TaxDocument4 pagesAccounting For Income TaxMjhayeNo ratings yet

- Local Business Tax (Notes)Document8 pagesLocal Business Tax (Notes)Y P Dela PeñaNo ratings yet

- PayslipDocument2 pagesPayslipbrij18No ratings yet

- Transfer PricingDocument6 pagesTransfer Pricingrpulgam09No ratings yet

- Vit Men'S Hostel: CircularDocument6 pagesVit Men'S Hostel: CircularSoumyajyoti MukherjeeNo ratings yet

- MM - Brazil - Fiscal - Book - Mastersaf 2 1Document30 pagesMM - Brazil - Fiscal - Book - Mastersaf 2 1guroyalNo ratings yet

- CAT Rules Against Grossing Up Method On PAYE - 3Document3 pagesCAT Rules Against Grossing Up Method On PAYE - 3vicenza-marie FukoNo ratings yet

- Boat Headphone InvoiceDocument1 pageBoat Headphone InvoiceShashank Tripathi100% (1)

- 19 C New PO 56235256201449 DT 01-SEP-23 On VINDHYA TELELINKS LIMITED-REWADocument8 pages19 C New PO 56235256201449 DT 01-SEP-23 On VINDHYA TELELINKS LIMITED-REWAManojNo ratings yet

- Samara University College of Business and Economics Department of Accounting and FinanceDocument51 pagesSamara University College of Business and Economics Department of Accounting and FinanceAllis WellNo ratings yet

- Account Statement 22 Aug 2023-22 Aug 2023Document2 pagesAccount Statement 22 Aug 2023-22 Aug 2023PRONAB MAJHINo ratings yet

- Invoice Shalter BatugadeDocument8 pagesInvoice Shalter BatugadeFuri HZNo ratings yet