Download as pptx, pdf, or txt

You might also like

- Protein and Nutrition in Critically Ill PatientDocument43 pagesProtein and Nutrition in Critically Ill PatientTom KristiantoNo ratings yet

- Mba-Marketing Principles Case Analysis-Wong LohDocument3 pagesMba-Marketing Principles Case Analysis-Wong LohMhild Gandawali100% (2)

- Acute Hemodialysis PrescriptionDocument13 pagesAcute Hemodialysis PrescriptionR DNo ratings yet

- Assessing AbdomenDocument115 pagesAssessing AbdomenKris TinaNo ratings yet

- 4 Headache PDFDocument39 pages4 Headache PDFJohn Ryan ParisNo ratings yet

- Hypertension: Short Term RegulationDocument6 pagesHypertension: Short Term RegulationAbdallah Essam Al-ZireeniNo ratings yet

- Renal EmergenciesDocument17 pagesRenal EmergenciesPrasad MgNo ratings yet

- Liver Cirrhosis PowerPointDocument12 pagesLiver Cirrhosis PowerPointFrancis Adrian100% (2)

- Principles of Nephrology NursingDocument11 pagesPrinciples of Nephrology NursingDhanya RaghuNo ratings yet

- Traditional Systems of Medicines. F19 FinaldocxDocument8 pagesTraditional Systems of Medicines. F19 FinaldocxAroob FaisalNo ratings yet

- Fulminant Hepatic FailureDocument12 pagesFulminant Hepatic Failureafghansyah arfiantoNo ratings yet

- Needle Cricothyroidotomy 2 - Hatem AlsrourDocument32 pagesNeedle Cricothyroidotomy 2 - Hatem Alsrourhatem alsrour100% (2)

- Kidney TransplantDocument11 pagesKidney TransplantPrincess Xzmae RamirezNo ratings yet

- Pancreatitis: Def Pancreatitis (Inflammation of The Pancreas) Is A Serious Disorder. The Most Basic Classification SystemDocument5 pagesPancreatitis: Def Pancreatitis (Inflammation of The Pancreas) Is A Serious Disorder. The Most Basic Classification SystemSanthu Su100% (2)

- Module 1 To 4Document208 pagesModule 1 To 4smbawasainiNo ratings yet

- Hypertension: Mayur BV BPH 3 Semester PSPHDocument29 pagesHypertension: Mayur BV BPH 3 Semester PSPHBijay Kumar MahatoNo ratings yet

- Healthcare EnvironmentDocument24 pagesHealthcare EnvironmentJOHN VINCENT BJORN GRAGEDA100% (1)

- Vijaya College of Nursing: Course Subject Unit Bio-Psycho Social PathophysiologyDocument3 pagesVijaya College of Nursing: Course Subject Unit Bio-Psycho Social PathophysiologyReshma Rinu50% (2)

- Appendectomy: Colegio de San Juan de Letran - CalambaDocument14 pagesAppendectomy: Colegio de San Juan de Letran - CalambaJiedNo ratings yet

- Acute Pancreatitis NOTESDocument17 pagesAcute Pancreatitis NOTESsameeha semiNo ratings yet

- Hemodiafiltration Kuhlmann PDFDocument31 pagesHemodiafiltration Kuhlmann PDFDavid SantosoNo ratings yet

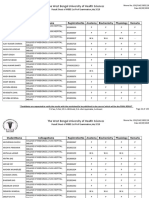

- The West Bengal University of Health SciencesDocument9 pagesThe West Bengal University of Health Sciencesbhaskar rayNo ratings yet

- Clinico Social CaseDocument6 pagesClinico Social CaseNakshatra ReddyNo ratings yet

- Biochemistry of Jaundice 03Document52 pagesBiochemistry of Jaundice 03Cathleen May Dela Cruz50% (2)

- Acute Intestinal Obstruction...Document42 pagesAcute Intestinal Obstruction...Ali100% (2)

- Antituberculous Therapy in Special SituationsDocument8 pagesAntituberculous Therapy in Special SituationsMobeen Raza100% (1)

- Trends & Issues in MSN NursingDocument41 pagesTrends & Issues in MSN NursingRajesh Sharma100% (3)

- Introduction To NutritionDocument19 pagesIntroduction To Nutritionseanne kskwkwkaNo ratings yet

- Therapeutic Positioning and Back MassageDocument7 pagesTherapeutic Positioning and Back MassageJavieNo ratings yet

- Zollinger Ellis Wps OfficeDocument15 pagesZollinger Ellis Wps OfficeAbhash MishraNo ratings yet

- Prepared by Inzar Yasin Ammar LabibDocument47 pagesPrepared by Inzar Yasin Ammar LabibdiaNo ratings yet

- 3136 - OA - Motivation Among Nurses PDFDocument6 pages3136 - OA - Motivation Among Nurses PDFShahnaz DarNo ratings yet

- Adult Health Nursing II Practicum Course Syllabus 2020-2021Document117 pagesAdult Health Nursing II Practicum Course Syllabus 2020-2021Hajer AlowaisiNo ratings yet

- Hemodynamic MonitoringDocument4 pagesHemodynamic Monitoringgurneet kourNo ratings yet

- Cardiac PPT SeminarDocument129 pagesCardiac PPT SeminarjoashannNo ratings yet

- Liver Function Test FinalDocument98 pagesLiver Function Test FinalHussain AzharNo ratings yet

- Lung Cancer (Bronchogenic Carcinoma)Document45 pagesLung Cancer (Bronchogenic Carcinoma)Howell Thomas Montilla AlamoNo ratings yet

- Health Economics - Lecture Ch13Document39 pagesHealth Economics - Lecture Ch13Katherine SauerNo ratings yet

- Diabetes Case StudiesDocument20 pagesDiabetes Case StudiesManish KanojiyaNo ratings yet

- Nursing Management of Pediatric EmergenciesDocument24 pagesNursing Management of Pediatric EmergenciesJesena SalveNo ratings yet

- Surgical Management of ObesityDocument13 pagesSurgical Management of Obesityمحمد حميدانNo ratings yet

- Fiscal PlanningDocument22 pagesFiscal PlanningRadha Sri100% (2)

- HD Priming Checklist 2022Document2 pagesHD Priming Checklist 2022Zyra DIOKNO50% (2)

- 5 FMCH Research BiasDocument3 pages5 FMCH Research BiasMia CadizNo ratings yet

- Macro and Micro MineralsDocument54 pagesMacro and Micro MineralsTrish LeonardoNo ratings yet

- Common Drugs Use in OphthalmologyDocument40 pagesCommon Drugs Use in Ophthalmologyณัช เกษมNo ratings yet

- Post Operative HemorrhageDocument16 pagesPost Operative Hemorrhagenishimura89No ratings yet

- Disorders of The BloodDocument35 pagesDisorders of The BloodNoor IbrahimNo ratings yet

- History of Old ClientDocument33 pagesHistory of Old ClientMuhammad Aamir100% (1)

- Ugib &lgibDocument41 pagesUgib &lgibDawex IsraelNo ratings yet

- PneumothoraxDocument2 pagesPneumothoraxAfif MansorNo ratings yet

- Renal CancerDocument34 pagesRenal CancerArya100% (1)

- Nursing Lecture NotesDocument11 pagesNursing Lecture NotesKwabena AmankwaNo ratings yet

- Manual Blood Pressure Competency ChecklistDocument1 pageManual Blood Pressure Competency Checklistshubham verma100% (1)

- Dr. Sunatrio - Management Hypovolemic ShockDocument59 pagesDr. Sunatrio - Management Hypovolemic ShockArga Putra SaboeNo ratings yet

- Drug Indication Action Side Effects and Adverse Reaction Nursing ConsiderationDocument8 pagesDrug Indication Action Side Effects and Adverse Reaction Nursing Considerationkier khierNo ratings yet

- Hypertension SPMDocument25 pagesHypertension SPMSai tejendraNo ratings yet

- Link ClickDocument4 pagesLink ClickMitch MontielNo ratings yet

- Effectiveness of Structured Teaching Programme On Knowledge Regarding Acid Peptic Disease and Its Prevention Among The Industrial WorkersDocument6 pagesEffectiveness of Structured Teaching Programme On Knowledge Regarding Acid Peptic Disease and Its Prevention Among The Industrial WorkersIJAR JOURNALNo ratings yet

- Management of Tuberculosis: A guide for clinicians (eBook edition)From EverandManagement of Tuberculosis: A guide for clinicians (eBook edition)No ratings yet

- Role of Dietary Fibers and Nutraceuticals in Preventing DiseasesFrom EverandRole of Dietary Fibers and Nutraceuticals in Preventing DiseasesRating: 5 out of 5 stars5/5 (1)

- General ElectricDocument4 pagesGeneral ElectricMJ Villamor Aquillo100% (1)

- IllustrationDocument3 pagesIllustrationVamsi Krishna BNo ratings yet

- Product Disclosure SheetDocument9 pagesProduct Disclosure SheetNurulhikmah RoslanNo ratings yet

- CHAPTER II Review of Related LiteratureDocument8 pagesCHAPTER II Review of Related LiteratureRonald AbletesNo ratings yet

- Macroeconomics Canadian 7th Edition Abel Solutions ManualDocument36 pagesMacroeconomics Canadian 7th Edition Abel Solutions Manualsinapateprear4k100% (27)

- Market Awareness of Brand Aditya Birla Money LTD'Document61 pagesMarket Awareness of Brand Aditya Birla Money LTD'ALI0911No ratings yet

- Name: Schedule: Course, Year, & Section: Faculty:: Week 3Document5 pagesName: Schedule: Course, Year, & Section: Faculty:: Week 3Ramil VillacarlosNo ratings yet

- Laws, Ethics, and Social Responsibility in Pricing: College of Management and Business TechnologyDocument21 pagesLaws, Ethics, and Social Responsibility in Pricing: College of Management and Business TechnologyFergus ParungaoNo ratings yet

- Honda MarketingDocument22 pagesHonda MarketingJAY BHAMRE100% (1)

- MccainDocument5 pagesMccainknnaikNo ratings yet

- PART I Philippine MoneyDocument119 pagesPART I Philippine MoneyPinky Longalong100% (1)

- NDPL Case StudyDocument10 pagesNDPL Case StudyPrateek BhargavaNo ratings yet

- PM Assignment 2 Bharti Walmart 31 39Document16 pagesPM Assignment 2 Bharti Walmart 31 39Ranjan MondalNo ratings yet

- Conceptual Framework Elements of Financial StatementsDocument18 pagesConceptual Framework Elements of Financial StatementsmaricrisNo ratings yet

- Pay and Benefits in The Public Sector: Martin Rama Development Research GroupDocument21 pagesPay and Benefits in The Public Sector: Martin Rama Development Research GroupShashank RaiNo ratings yet

- Women in AgricultureDocument3 pagesWomen in AgricultureRajul C DasNo ratings yet

- A Study On Loans and Advances by Rohit RDocument91 pagesA Study On Loans and Advances by Rohit RChandrashekhar GurnuleNo ratings yet

- Purchasing Power ParityDocument5 pagesPurchasing Power ParityRahul Kumar AwadeNo ratings yet

- Chapter 4Document20 pagesChapter 4Avezia Gabby Ariane LaupaNo ratings yet

- Importance of Work Study Method For Garments Productivity Expansion.Document63 pagesImportance of Work Study Method For Garments Productivity Expansion.Rayhan kabirNo ratings yet

- Contract of Work in The Construction and Painting of Table For E-ClassroomDocument1 pageContract of Work in The Construction and Painting of Table For E-ClassroomAileen Rizaldo MejiaNo ratings yet

- Annual Report: GSP Finance Company (Bangladesh) LimitedDocument101 pagesAnnual Report: GSP Finance Company (Bangladesh) LimitedSakib AhmedNo ratings yet

- Go Negosyo ActDocument26 pagesGo Negosyo ActEngiemar Barbasa TupasNo ratings yet

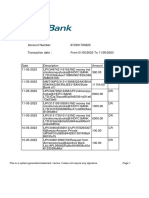

- Statement 1683800003450Document5 pagesStatement 1683800003450Rajeev BangaNo ratings yet

- 4 Types of Capacity StrategyDocument7 pages4 Types of Capacity StrategySaga HayyuNo ratings yet

- Moulaert 2007Document15 pagesMoulaert 2007Raquel FranciscoNo ratings yet

- Reaction PaperDocument2 pagesReaction PaperJoice RuzolNo ratings yet

- SHAREHOLDERS PARTICIPATE IN THE MANAGEMENT OF THE COMPANY PRINCIPLES AND BEYOND-SynopsisDocument4 pagesSHAREHOLDERS PARTICIPATE IN THE MANAGEMENT OF THE COMPANY PRINCIPLES AND BEYOND-SynopsisdheerajNo ratings yet