Presentation - Capital Flows and Capital Account Liberalisation in The Post-Financial-Crisis Era Challenges Opportunities and Policy Responses

Presentation - Capital Flows and Capital Account Liberalisation in The Post-Financial-Crisis Era Challenges Opportunities and Policy Responses

You might also like

- First American Bank Case SolutionDocument13 pagesFirst American Bank Case Solutionharleeniitr80% (5)

- Year 5 RE Summer One - Sikhism What Is The Best Way For A Sikh To Show Commitment To God.199911722Document1 pageYear 5 RE Summer One - Sikhism What Is The Best Way For A Sikh To Show Commitment To God.199911722OnyxSungaNo ratings yet

- What Is The Meaning of The Term Reinsurance?Document3 pagesWhat Is The Meaning of The Term Reinsurance?Shipra Singh0% (1)

- Etihad Bank - Global IMCDocument22 pagesEtihad Bank - Global IMCChristine AghabiNo ratings yet

- Ag EconomicsDocument102 pagesAg EconomicsWaren Lloren100% (1)

- An Overview of The Indian Financial System in The Post-1950 PeriodDocument25 pagesAn Overview of The Indian Financial System in The Post-1950 PeriodPalNo ratings yet

- 1.1 Core Economic Indicators: Indicators FY 02 FY 03 FY 04 FY 05 FY 06Document4 pages1.1 Core Economic Indicators: Indicators FY 02 FY 03 FY 04 FY 05 FY 06Abu AlkhtatNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Eight Months Data of 2022.23Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Eight Months Data of 2022.23acharya.arpan08No ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Five Months Data of 2021.22Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Five Months Data of 2021.22Mohan PudasainiNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Two Months Data of 2021.22 2Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Two Months Data of 2021.22 2shyam karkiNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Three Months Data of 2021.22 2Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Three Months Data of 2021.22 2Chetan PokharelNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On One Month Data of 2023.24 1Document85 pagesCurrent Macroeconomic and Financial Situation Tables Based On One Month Data of 2023.24 1shyam karkiNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Six Months Data of 2021.22Document85 pagesCurrent Macroeconomic and Financial Situation Tables Based On Six Months Data of 2021.22Sashank GaudelNo ratings yet

- Equities Update: MorningDocument2 pagesEquities Update: MorningsfarithaNo ratings yet

- How Does Exchange Rate Regime Affects Inflation Evidence (Autosaved)Document17 pagesHow Does Exchange Rate Regime Affects Inflation Evidence (Autosaved)foday joofNo ratings yet

- Securities and Exchange Board of IndiaDocument10 pagesSecurities and Exchange Board of IndiaRaman RanaNo ratings yet

- Current Macroeconomic Situation Tables Based On Six Months Data of 2080.81 1Document85 pagesCurrent Macroeconomic Situation Tables Based On Six Months Data of 2080.81 1gharmabasNo ratings yet

- Selected Topic: The Role of Financial Derivatives in Emerging MarketsDocument18 pagesSelected Topic: The Role of Financial Derivatives in Emerging MarketsAna RomeroNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Seven Months Data of 2022.23 3Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Seven Months Data of 2022.23 3shyam karkiNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Six Months Data of 2022.23 1Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Six Months Data of 2022.23 1shyam karkiNo ratings yet

- Malaysia Equity: 2011 OutlookDocument36 pagesMalaysia Equity: 2011 OutlookRidhwan KhabirNo ratings yet

- Pertemuan Pertama:: Aspek Keuangan GlobalDocument52 pagesPertemuan Pertama:: Aspek Keuangan GlobalMazmur Binsar Hamonangan DamanikNo ratings yet

- ABM Weekly Techno-Derivatives Snapshot 13 July 2020Document35 pagesABM Weekly Techno-Derivatives Snapshot 13 July 2020Mukesh GuptaNo ratings yet

- Statistical TablesDocument108 pagesStatistical TablesAakriti AdhikariNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Eight Months Data 2020.21 1Document83 pagesCurrent Macroeconomic and Financial Situation Tables Based On Eight Months Data 2020.21 1Kiran RaiNo ratings yet

- Week 12-Turkish Economy in Brief-1Document44 pagesWeek 12-Turkish Economy in Brief-1kvothee100No ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Eleven Months Data of 2022.23 4Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Eleven Months Data of 2022.23 4shyam karkiNo ratings yet

- Economic Growth, Inflation, and Monetary Policy in Pakistan: Preliminary Empirical EstimatesDocument14 pagesEconomic Growth, Inflation, and Monetary Policy in Pakistan: Preliminary Empirical Estimateskoolzain5759No ratings yet

- Macroeconomics, Agriculture, and Food Security PDFDocument644 pagesMacroeconomics, Agriculture, and Food Security PDFHemu BhardwajNo ratings yet

- Econometric Determinants of Liquidity of The Bond MarketDocument24 pagesEconometric Determinants of Liquidity of The Bond MarketBasmaNo ratings yet

- How The Global Financial Crisis Has Affected The Small States of Seychelles & MauritiusDocument32 pagesHow The Global Financial Crisis Has Affected The Small States of Seychelles & MauritiusRajiv BissoonNo ratings yet

- Current Macroeconomic and Financial SItuation. Tables Based On Annual Data of 2019.20. 1Document89 pagesCurrent Macroeconomic and Financial SItuation. Tables Based On Annual Data of 2019.20. 1hello worldNo ratings yet

- Mozal Finance EXCEL Group 15dec2013Document15 pagesMozal Finance EXCEL Group 15dec2013Abhijit TailangNo ratings yet

- AR2010 2011englishDocument87 pagesAR2010 2011englishshovon mukitNo ratings yet

- ch06Document8 pagesch06nepalman2023No ratings yet

- Vietnam Economy and Stock Market: 2021 Mid-Year Outlook: Post-Pandemic Investment StrategyDocument58 pagesVietnam Economy and Stock Market: 2021 Mid-Year Outlook: Post-Pandemic Investment StrategyDinh Minh TriNo ratings yet

- Grammer 2Document10 pagesGrammer 2rishabhmehta2008No ratings yet

- Kenanga Today-200730 (Kenanga)Document6 pagesKenanga Today-200730 (Kenanga)Jo AnneNo ratings yet

- International Capital: A Threat To Human Dignity and Life On Planet EarthDocument10 pagesInternational Capital: A Threat To Human Dignity and Life On Planet EarthWaritsa YolandaNo ratings yet

- 2021-07-07-Mirae Asset Securiti-2021 MID-YEAR OUTLOOK POST-PANDEMIC INVESTMENT STRATEGY-92953422Document58 pages2021-07-07-Mirae Asset Securiti-2021 MID-YEAR OUTLOOK POST-PANDEMIC INVESTMENT STRATEGY-92953422Tung NgoNo ratings yet

- Most Market Outlook Most Market Outlook Most Market Outlook: Morning UpdateDocument7 pagesMost Market Outlook Most Market Outlook Most Market Outlook: Morning Updatevikalp123123No ratings yet

- Lecture Notes: FDI DeterminantsDocument30 pagesLecture Notes: FDI DeterminantsAmritangshu BanerjeeNo ratings yet

- Insights EdelMFDocument81 pagesInsights EdelMFSindhuja AvinashNo ratings yet

- Introduction: India's Economy After Liberalization: January 2012Document47 pagesIntroduction: India's Economy After Liberalization: January 2012Prakhar GuptaNo ratings yet

- Current Macroeconomic and Financial Situation. Tables. Based On Annual Data of 2022.23 2Document94 pagesCurrent Macroeconomic and Financial Situation. Tables. Based On Annual Data of 2022.23 2shyam karkiNo ratings yet

- Morning Report EquityDocument4 pagesMorning Report EquitySathyamNo ratings yet

- A Lecture On Securities Market: Presented byDocument52 pagesA Lecture On Securities Market: Presented byrobinkapoor100% (3)

- R qt0609f PDFDocument14 pagesR qt0609f PDFjohnNo ratings yet

- Statistical Bulletin October 2020Document31 pagesStatistical Bulletin October 2020Fuaad DodooNo ratings yet

- BNY Mellon Asian Equity Fund: As at 31 December 2010Document4 pagesBNY Mellon Asian Equity Fund: As at 31 December 2010Javier Muñoz AbelláNo ratings yet

- India Review 2Document5 pagesIndia Review 2Neoraiders RockNo ratings yet

- Sharekhan's Top Equity Fund Picks: September 14, 2010Document4 pagesSharekhan's Top Equity Fund Picks: September 14, 2010dinesh216No ratings yet

- 2021 Sep Strategy ENDocument58 pages2021 Sep Strategy ENDinh Minh TriNo ratings yet

- Indian Mutual Fund IndustryDocument25 pagesIndian Mutual Fund Industryravijha_1984No ratings yet

- International Fin MGT: A Brief IntroductionDocument98 pagesInternational Fin MGT: A Brief Introductionanji 123No ratings yet

- PPFCF PPFAS Monthly Portfolio Report Sept 30 2021Document15 pagesPPFCF PPFAS Monthly Portfolio Report Sept 30 2021KumaraswamyNo ratings yet

- NSE India - Nov22 - EUDocument9 pagesNSE India - Nov22 - EUpremalgandhi10No ratings yet

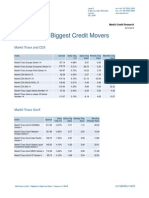

- Markit News: Biggest Credit Movers: Markit Itraxx and CDXDocument5 pagesMarkit News: Biggest Credit Movers: Markit Itraxx and CDXAndrea MacettiNo ratings yet

- Annual Data of 2020.21 5Document97 pagesAnnual Data of 2020.21 5Aakriti AdhikariNo ratings yet

- 09 Feb Eurekahedge ReportDocument24 pages09 Feb Eurekahedge ReportWeixiang YanNo ratings yet

- LN 11Document63 pagesLN 11VinitaNo ratings yet

- 2024 4q Presentation enDocument30 pages2024 4q Presentation ensurishreya15No ratings yet

- Equities Update: MorningDocument2 pagesEquities Update: MorningsfarithaNo ratings yet

- Indian EconomyDocument44 pagesIndian Economykapil godaraNo ratings yet

- Optimum Currency Areas: A Monetary Union for Southern AfricaFrom EverandOptimum Currency Areas: A Monetary Union for Southern AfricaNo ratings yet

- Typology and Benchmark of Tools For Assessing The Mobile Networks Qos and QoeDocument57 pagesTypology and Benchmark of Tools For Assessing The Mobile Networks Qos and QoeOnyxSungaNo ratings yet

- UCSP Political ScienceDocument42 pagesUCSP Political ScienceOnyxSungaNo ratings yet

- Catastrophe Readiness and Response - Session 11-Emergent OrganizationsDocument40 pagesCatastrophe Readiness and Response - Session 11-Emergent OrganizationsOnyxSungaNo ratings yet

- You Had Me at Zombie: Career Planning in The Walking Dead EraDocument35 pagesYou Had Me at Zombie: Career Planning in The Walking Dead EraOnyxSungaNo ratings yet

- Welcome!: School Culture and Transformational ChangeDocument25 pagesWelcome!: School Culture and Transformational ChangeOnyxSungaNo ratings yet

- L E D P: The Local Economic Development ProgrammeDocument59 pagesL E D P: The Local Economic Development ProgrammeOnyxSungaNo ratings yet

- Tourism Information Technology: 3 EditionDocument23 pagesTourism Information Technology: 3 EditionOnyxSungaNo ratings yet

- Sikhism: The Life of Guru Nanak (The Founder of Sikhism)Document2 pagesSikhism: The Life of Guru Nanak (The Founder of Sikhism)OnyxSungaNo ratings yet

- SikhismDocument19 pagesSikhismOnyxSungaNo ratings yet

- Education Phase 3 Religion and Food ChoiceDocument18 pagesEducation Phase 3 Religion and Food ChoiceOnyxSungaNo ratings yet

- London Diocesan Board For Schools Syllabus For Religious EducationDocument1 pageLondon Diocesan Board For Schools Syllabus For Religious EducationOnyxSungaNo ratings yet

- Hinduism BuddhismDocument23 pagesHinduism BuddhismOnyxSungaNo ratings yet

- You Need To Know 3. Key WordsDocument1 pageYou Need To Know 3. Key WordsOnyxSungaNo ratings yet

- Sikhism in KS2 PowerpointDocument61 pagesSikhism in KS2 PowerpointOnyxSungaNo ratings yet

- Sikhism Pilgrimage Spot in IndiaDocument9 pagesSikhism Pilgrimage Spot in IndiaOnyxSungaNo ratings yet

- Sikh Dharam: Key Question 1Document27 pagesSikh Dharam: Key Question 1OnyxSungaNo ratings yet

- Sikhism and The Five K'S: Guru Gobind SinghDocument9 pagesSikhism and The Five K'S: Guru Gobind SinghOnyxSungaNo ratings yet

- Hs-Adult PP PresentationDocument43 pagesHs-Adult PP PresentationOnyxSungaNo ratings yet

- Sikhism: An Introduction: Sikh Society in NetherlandsDocument18 pagesSikhism: An Introduction: Sikh Society in NetherlandsOnyxSungaNo ratings yet

- Intro To SikhismDocument28 pagesIntro To SikhismOnyxSungaNo ratings yet

- Buisness StrategyDocument3 pagesBuisness Strategyrajaroma45No ratings yet

- Introduction To Corporate Finance, Megginson, Smart and LuceyDocument6 pagesIntroduction To Corporate Finance, Megginson, Smart and LuceyGvz HndraNo ratings yet

- Methods/Approaches To ValuationDocument3 pagesMethods/Approaches To ValuationPankaj2cNo ratings yet

- Consumers Equlibrium With IC AnalysisDocument3 pagesConsumers Equlibrium With IC AnalysisAKASH KULSHRESTHANo ratings yet

- The Core Function of The Marketing Department Is To Understand and Satisfy Consumer NeedDocument5 pagesThe Core Function of The Marketing Department Is To Understand and Satisfy Consumer NeedniceprachiNo ratings yet

- Product PlanningDocument2 pagesProduct PlanningryanNo ratings yet

- Competencies and CapabilitiesDocument10 pagesCompetencies and CapabilitiesMarwan BecharaNo ratings yet

- International Working Capital ManagementDocument28 pagesInternational Working Capital ManagementAvayant Kumar Singh100% (2)

- Analysis A-REITs and NZ-REITsDocument43 pagesAnalysis A-REITs and NZ-REITsRandolph KirkNo ratings yet

- Unit1 International MarketingDocument15 pagesUnit1 International MarketingSoukaina NacirNo ratings yet

- The Limits of DemocracyDocument34 pagesThe Limits of DemocracyNataliiaRojazNo ratings yet

- Hair Color Consumer BehaviourDocument28 pagesHair Color Consumer Behaviourhitesh100% (2)

- SOC Indus Multiplier MaxDocument4 pagesSOC Indus Multiplier Maxmanoj baroka0% (1)

- Mock Test 3 - Recent Questions With Answers! - Dec 2010Document8 pagesMock Test 3 - Recent Questions With Answers! - Dec 2010huntenz100% (1)

- Unec 1642279326Document19 pagesUnec 1642279326Qelender MustafayevNo ratings yet

- Assessment Task 3 - BSBMKG502 (Final)Document17 pagesAssessment Task 3 - BSBMKG502 (Final)sarinna LeeNo ratings yet

- Barilla Spa Bullwhip EffectDocument9 pagesBarilla Spa Bullwhip EffectAlee Di VaioNo ratings yet

- Learning Arc - Independent Learning Resource Y12 Micro EconomicsDocument8 pagesLearning Arc - Independent Learning Resource Y12 Micro EconomicsshutupfagNo ratings yet

- mm2 Coffee CaseDocument11 pagesmm2 Coffee CaseShubham ThakurNo ratings yet

- Chapter 7 - Portfolio Theory and The Capital Asset Model Pricing (Compatibility Mode)Document21 pagesChapter 7 - Portfolio Theory and The Capital Asset Model Pricing (Compatibility Mode)Hanh TranNo ratings yet

- What Is The Difference Between P & L Ac and Income & Expenditure Statement?Document22 pagesWhat Is The Difference Between P & L Ac and Income & Expenditure Statement?pranjali shindeNo ratings yet

- Pemaxx Zoom ClassDocument20 pagesPemaxx Zoom ClassgqdevotiongroupNo ratings yet

- Markowitz Portfolio ModelDocument9 pagesMarkowitz Portfolio ModelSamia Islam BushraNo ratings yet

- Games Workshop 2013 Retailer PolicyDocument8 pagesGames Workshop 2013 Retailer PolicyJimmy WungNo ratings yet

- LDM - Case Schedule and Questions - 2019Document3 pagesLDM - Case Schedule and Questions - 2019Krnav MehtaNo ratings yet

- Inventory Management Bhel BhaavisgDocument7 pagesInventory Management Bhel BhaavisgkharemixNo ratings yet

Download as ppt, pdf, or txt

You might also like

- First American Bank Case SolutionDocument13 pagesFirst American Bank Case Solutionharleeniitr80% (5)

- Year 5 RE Summer One - Sikhism What Is The Best Way For A Sikh To Show Commitment To God.199911722Document1 pageYear 5 RE Summer One - Sikhism What Is The Best Way For A Sikh To Show Commitment To God.199911722OnyxSungaNo ratings yet

- What Is The Meaning of The Term Reinsurance?Document3 pagesWhat Is The Meaning of The Term Reinsurance?Shipra Singh0% (1)

- Etihad Bank - Global IMCDocument22 pagesEtihad Bank - Global IMCChristine AghabiNo ratings yet

- Ag EconomicsDocument102 pagesAg EconomicsWaren Lloren100% (1)

- An Overview of The Indian Financial System in The Post-1950 PeriodDocument25 pagesAn Overview of The Indian Financial System in The Post-1950 PeriodPalNo ratings yet

- 1.1 Core Economic Indicators: Indicators FY 02 FY 03 FY 04 FY 05 FY 06Document4 pages1.1 Core Economic Indicators: Indicators FY 02 FY 03 FY 04 FY 05 FY 06Abu AlkhtatNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Eight Months Data of 2022.23Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Eight Months Data of 2022.23acharya.arpan08No ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Five Months Data of 2021.22Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Five Months Data of 2021.22Mohan PudasainiNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Two Months Data of 2021.22 2Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Two Months Data of 2021.22 2shyam karkiNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Three Months Data of 2021.22 2Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Three Months Data of 2021.22 2Chetan PokharelNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On One Month Data of 2023.24 1Document85 pagesCurrent Macroeconomic and Financial Situation Tables Based On One Month Data of 2023.24 1shyam karkiNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Six Months Data of 2021.22Document85 pagesCurrent Macroeconomic and Financial Situation Tables Based On Six Months Data of 2021.22Sashank GaudelNo ratings yet

- Equities Update: MorningDocument2 pagesEquities Update: MorningsfarithaNo ratings yet

- How Does Exchange Rate Regime Affects Inflation Evidence (Autosaved)Document17 pagesHow Does Exchange Rate Regime Affects Inflation Evidence (Autosaved)foday joofNo ratings yet

- Securities and Exchange Board of IndiaDocument10 pagesSecurities and Exchange Board of IndiaRaman RanaNo ratings yet

- Current Macroeconomic Situation Tables Based On Six Months Data of 2080.81 1Document85 pagesCurrent Macroeconomic Situation Tables Based On Six Months Data of 2080.81 1gharmabasNo ratings yet

- Selected Topic: The Role of Financial Derivatives in Emerging MarketsDocument18 pagesSelected Topic: The Role of Financial Derivatives in Emerging MarketsAna RomeroNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Seven Months Data of 2022.23 3Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Seven Months Data of 2022.23 3shyam karkiNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Six Months Data of 2022.23 1Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Six Months Data of 2022.23 1shyam karkiNo ratings yet

- Malaysia Equity: 2011 OutlookDocument36 pagesMalaysia Equity: 2011 OutlookRidhwan KhabirNo ratings yet

- Pertemuan Pertama:: Aspek Keuangan GlobalDocument52 pagesPertemuan Pertama:: Aspek Keuangan GlobalMazmur Binsar Hamonangan DamanikNo ratings yet

- ABM Weekly Techno-Derivatives Snapshot 13 July 2020Document35 pagesABM Weekly Techno-Derivatives Snapshot 13 July 2020Mukesh GuptaNo ratings yet

- Statistical TablesDocument108 pagesStatistical TablesAakriti AdhikariNo ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Eight Months Data 2020.21 1Document83 pagesCurrent Macroeconomic and Financial Situation Tables Based On Eight Months Data 2020.21 1Kiran RaiNo ratings yet

- Week 12-Turkish Economy in Brief-1Document44 pagesWeek 12-Turkish Economy in Brief-1kvothee100No ratings yet

- Current Macroeconomic and Financial Situation Tables Based On Eleven Months Data of 2022.23 4Document84 pagesCurrent Macroeconomic and Financial Situation Tables Based On Eleven Months Data of 2022.23 4shyam karkiNo ratings yet

- Economic Growth, Inflation, and Monetary Policy in Pakistan: Preliminary Empirical EstimatesDocument14 pagesEconomic Growth, Inflation, and Monetary Policy in Pakistan: Preliminary Empirical Estimateskoolzain5759No ratings yet

- Macroeconomics, Agriculture, and Food Security PDFDocument644 pagesMacroeconomics, Agriculture, and Food Security PDFHemu BhardwajNo ratings yet

- Econometric Determinants of Liquidity of The Bond MarketDocument24 pagesEconometric Determinants of Liquidity of The Bond MarketBasmaNo ratings yet

- How The Global Financial Crisis Has Affected The Small States of Seychelles & MauritiusDocument32 pagesHow The Global Financial Crisis Has Affected The Small States of Seychelles & MauritiusRajiv BissoonNo ratings yet

- Current Macroeconomic and Financial SItuation. Tables Based On Annual Data of 2019.20. 1Document89 pagesCurrent Macroeconomic and Financial SItuation. Tables Based On Annual Data of 2019.20. 1hello worldNo ratings yet

- Mozal Finance EXCEL Group 15dec2013Document15 pagesMozal Finance EXCEL Group 15dec2013Abhijit TailangNo ratings yet

- AR2010 2011englishDocument87 pagesAR2010 2011englishshovon mukitNo ratings yet

- ch06Document8 pagesch06nepalman2023No ratings yet

- Vietnam Economy and Stock Market: 2021 Mid-Year Outlook: Post-Pandemic Investment StrategyDocument58 pagesVietnam Economy and Stock Market: 2021 Mid-Year Outlook: Post-Pandemic Investment StrategyDinh Minh TriNo ratings yet

- Grammer 2Document10 pagesGrammer 2rishabhmehta2008No ratings yet

- Kenanga Today-200730 (Kenanga)Document6 pagesKenanga Today-200730 (Kenanga)Jo AnneNo ratings yet

- International Capital: A Threat To Human Dignity and Life On Planet EarthDocument10 pagesInternational Capital: A Threat To Human Dignity and Life On Planet EarthWaritsa YolandaNo ratings yet

- 2021-07-07-Mirae Asset Securiti-2021 MID-YEAR OUTLOOK POST-PANDEMIC INVESTMENT STRATEGY-92953422Document58 pages2021-07-07-Mirae Asset Securiti-2021 MID-YEAR OUTLOOK POST-PANDEMIC INVESTMENT STRATEGY-92953422Tung NgoNo ratings yet

- Most Market Outlook Most Market Outlook Most Market Outlook: Morning UpdateDocument7 pagesMost Market Outlook Most Market Outlook Most Market Outlook: Morning Updatevikalp123123No ratings yet

- Lecture Notes: FDI DeterminantsDocument30 pagesLecture Notes: FDI DeterminantsAmritangshu BanerjeeNo ratings yet

- Insights EdelMFDocument81 pagesInsights EdelMFSindhuja AvinashNo ratings yet

- Introduction: India's Economy After Liberalization: January 2012Document47 pagesIntroduction: India's Economy After Liberalization: January 2012Prakhar GuptaNo ratings yet

- Current Macroeconomic and Financial Situation. Tables. Based On Annual Data of 2022.23 2Document94 pagesCurrent Macroeconomic and Financial Situation. Tables. Based On Annual Data of 2022.23 2shyam karkiNo ratings yet

- Morning Report EquityDocument4 pagesMorning Report EquitySathyamNo ratings yet

- A Lecture On Securities Market: Presented byDocument52 pagesA Lecture On Securities Market: Presented byrobinkapoor100% (3)

- R qt0609f PDFDocument14 pagesR qt0609f PDFjohnNo ratings yet

- Statistical Bulletin October 2020Document31 pagesStatistical Bulletin October 2020Fuaad DodooNo ratings yet

- BNY Mellon Asian Equity Fund: As at 31 December 2010Document4 pagesBNY Mellon Asian Equity Fund: As at 31 December 2010Javier Muñoz AbelláNo ratings yet

- India Review 2Document5 pagesIndia Review 2Neoraiders RockNo ratings yet

- Sharekhan's Top Equity Fund Picks: September 14, 2010Document4 pagesSharekhan's Top Equity Fund Picks: September 14, 2010dinesh216No ratings yet

- 2021 Sep Strategy ENDocument58 pages2021 Sep Strategy ENDinh Minh TriNo ratings yet

- Indian Mutual Fund IndustryDocument25 pagesIndian Mutual Fund Industryravijha_1984No ratings yet

- International Fin MGT: A Brief IntroductionDocument98 pagesInternational Fin MGT: A Brief Introductionanji 123No ratings yet

- PPFCF PPFAS Monthly Portfolio Report Sept 30 2021Document15 pagesPPFCF PPFAS Monthly Portfolio Report Sept 30 2021KumaraswamyNo ratings yet

- NSE India - Nov22 - EUDocument9 pagesNSE India - Nov22 - EUpremalgandhi10No ratings yet

- Markit News: Biggest Credit Movers: Markit Itraxx and CDXDocument5 pagesMarkit News: Biggest Credit Movers: Markit Itraxx and CDXAndrea MacettiNo ratings yet

- Annual Data of 2020.21 5Document97 pagesAnnual Data of 2020.21 5Aakriti AdhikariNo ratings yet

- 09 Feb Eurekahedge ReportDocument24 pages09 Feb Eurekahedge ReportWeixiang YanNo ratings yet

- LN 11Document63 pagesLN 11VinitaNo ratings yet

- 2024 4q Presentation enDocument30 pages2024 4q Presentation ensurishreya15No ratings yet

- Equities Update: MorningDocument2 pagesEquities Update: MorningsfarithaNo ratings yet

- Indian EconomyDocument44 pagesIndian Economykapil godaraNo ratings yet

- Optimum Currency Areas: A Monetary Union for Southern AfricaFrom EverandOptimum Currency Areas: A Monetary Union for Southern AfricaNo ratings yet

- Typology and Benchmark of Tools For Assessing The Mobile Networks Qos and QoeDocument57 pagesTypology and Benchmark of Tools For Assessing The Mobile Networks Qos and QoeOnyxSungaNo ratings yet

- UCSP Political ScienceDocument42 pagesUCSP Political ScienceOnyxSungaNo ratings yet

- Catastrophe Readiness and Response - Session 11-Emergent OrganizationsDocument40 pagesCatastrophe Readiness and Response - Session 11-Emergent OrganizationsOnyxSungaNo ratings yet

- You Had Me at Zombie: Career Planning in The Walking Dead EraDocument35 pagesYou Had Me at Zombie: Career Planning in The Walking Dead EraOnyxSungaNo ratings yet

- Welcome!: School Culture and Transformational ChangeDocument25 pagesWelcome!: School Culture and Transformational ChangeOnyxSungaNo ratings yet

- L E D P: The Local Economic Development ProgrammeDocument59 pagesL E D P: The Local Economic Development ProgrammeOnyxSungaNo ratings yet

- Tourism Information Technology: 3 EditionDocument23 pagesTourism Information Technology: 3 EditionOnyxSungaNo ratings yet

- Sikhism: The Life of Guru Nanak (The Founder of Sikhism)Document2 pagesSikhism: The Life of Guru Nanak (The Founder of Sikhism)OnyxSungaNo ratings yet

- SikhismDocument19 pagesSikhismOnyxSungaNo ratings yet

- Education Phase 3 Religion and Food ChoiceDocument18 pagesEducation Phase 3 Religion and Food ChoiceOnyxSungaNo ratings yet

- London Diocesan Board For Schools Syllabus For Religious EducationDocument1 pageLondon Diocesan Board For Schools Syllabus For Religious EducationOnyxSungaNo ratings yet

- Hinduism BuddhismDocument23 pagesHinduism BuddhismOnyxSungaNo ratings yet

- You Need To Know 3. Key WordsDocument1 pageYou Need To Know 3. Key WordsOnyxSungaNo ratings yet

- Sikhism in KS2 PowerpointDocument61 pagesSikhism in KS2 PowerpointOnyxSungaNo ratings yet

- Sikhism Pilgrimage Spot in IndiaDocument9 pagesSikhism Pilgrimage Spot in IndiaOnyxSungaNo ratings yet

- Sikh Dharam: Key Question 1Document27 pagesSikh Dharam: Key Question 1OnyxSungaNo ratings yet

- Sikhism and The Five K'S: Guru Gobind SinghDocument9 pagesSikhism and The Five K'S: Guru Gobind SinghOnyxSungaNo ratings yet

- Hs-Adult PP PresentationDocument43 pagesHs-Adult PP PresentationOnyxSungaNo ratings yet

- Sikhism: An Introduction: Sikh Society in NetherlandsDocument18 pagesSikhism: An Introduction: Sikh Society in NetherlandsOnyxSungaNo ratings yet

- Intro To SikhismDocument28 pagesIntro To SikhismOnyxSungaNo ratings yet

- Buisness StrategyDocument3 pagesBuisness Strategyrajaroma45No ratings yet

- Introduction To Corporate Finance, Megginson, Smart and LuceyDocument6 pagesIntroduction To Corporate Finance, Megginson, Smart and LuceyGvz HndraNo ratings yet

- Methods/Approaches To ValuationDocument3 pagesMethods/Approaches To ValuationPankaj2cNo ratings yet

- Consumers Equlibrium With IC AnalysisDocument3 pagesConsumers Equlibrium With IC AnalysisAKASH KULSHRESTHANo ratings yet

- The Core Function of The Marketing Department Is To Understand and Satisfy Consumer NeedDocument5 pagesThe Core Function of The Marketing Department Is To Understand and Satisfy Consumer NeedniceprachiNo ratings yet

- Product PlanningDocument2 pagesProduct PlanningryanNo ratings yet

- Competencies and CapabilitiesDocument10 pagesCompetencies and CapabilitiesMarwan BecharaNo ratings yet

- International Working Capital ManagementDocument28 pagesInternational Working Capital ManagementAvayant Kumar Singh100% (2)

- Analysis A-REITs and NZ-REITsDocument43 pagesAnalysis A-REITs and NZ-REITsRandolph KirkNo ratings yet

- Unit1 International MarketingDocument15 pagesUnit1 International MarketingSoukaina NacirNo ratings yet

- The Limits of DemocracyDocument34 pagesThe Limits of DemocracyNataliiaRojazNo ratings yet

- Hair Color Consumer BehaviourDocument28 pagesHair Color Consumer Behaviourhitesh100% (2)

- SOC Indus Multiplier MaxDocument4 pagesSOC Indus Multiplier Maxmanoj baroka0% (1)

- Mock Test 3 - Recent Questions With Answers! - Dec 2010Document8 pagesMock Test 3 - Recent Questions With Answers! - Dec 2010huntenz100% (1)

- Unec 1642279326Document19 pagesUnec 1642279326Qelender MustafayevNo ratings yet

- Assessment Task 3 - BSBMKG502 (Final)Document17 pagesAssessment Task 3 - BSBMKG502 (Final)sarinna LeeNo ratings yet

- Barilla Spa Bullwhip EffectDocument9 pagesBarilla Spa Bullwhip EffectAlee Di VaioNo ratings yet

- Learning Arc - Independent Learning Resource Y12 Micro EconomicsDocument8 pagesLearning Arc - Independent Learning Resource Y12 Micro EconomicsshutupfagNo ratings yet

- mm2 Coffee CaseDocument11 pagesmm2 Coffee CaseShubham ThakurNo ratings yet

- Chapter 7 - Portfolio Theory and The Capital Asset Model Pricing (Compatibility Mode)Document21 pagesChapter 7 - Portfolio Theory and The Capital Asset Model Pricing (Compatibility Mode)Hanh TranNo ratings yet

- What Is The Difference Between P & L Ac and Income & Expenditure Statement?Document22 pagesWhat Is The Difference Between P & L Ac and Income & Expenditure Statement?pranjali shindeNo ratings yet

- Pemaxx Zoom ClassDocument20 pagesPemaxx Zoom ClassgqdevotiongroupNo ratings yet

- Markowitz Portfolio ModelDocument9 pagesMarkowitz Portfolio ModelSamia Islam BushraNo ratings yet

- Games Workshop 2013 Retailer PolicyDocument8 pagesGames Workshop 2013 Retailer PolicyJimmy WungNo ratings yet

- LDM - Case Schedule and Questions - 2019Document3 pagesLDM - Case Schedule and Questions - 2019Krnav MehtaNo ratings yet

- Inventory Management Bhel BhaavisgDocument7 pagesInventory Management Bhel BhaavisgkharemixNo ratings yet