Download as ppt, pdf, or txt

You might also like

- Topic 5 Stamp DutyDocument38 pagesTopic 5 Stamp DutySITI HAMIZAH HAMZAHNo ratings yet

- Topic 5 Stamp DutyDocument38 pagesTopic 5 Stamp Duty2022478048No ratings yet

- Stamp Duty: Advanced Malaysian Taxation - Chapter 53 CKF Stamp Act 1949Document43 pagesStamp Duty: Advanced Malaysian Taxation - Chapter 53 CKF Stamp Act 1949aishahNo ratings yet

- C2 Stamp DutyDocument11 pagesC2 Stamp DutyporzvtzoNo ratings yet

- Amendments For NOV 21: Amendment in 1 Min Series Available On InstagramDocument32 pagesAmendments For NOV 21: Amendment in 1 Min Series Available On InstagramAakriti SinghalNo ratings yet

- Abft1024 L14 - LtyDocument3 pagesAbft1024 L14 - Ltylfc778No ratings yet

- Catan Selina Mari Unit 2 Intacc3 099Document12 pagesCatan Selina Mari Unit 2 Intacc3 099Elc Elc ElcNo ratings yet

- Tax-Remedies (Govt-Remedies-Highlights)Document38 pagesTax-Remedies (Govt-Remedies-Highlights)Yves Nicollete LabadanNo ratings yet

- 5rd Sessiom - Audit of LeaseDocument20 pages5rd Sessiom - Audit of LeaseRUFFA SANCHEZNo ratings yet

- Leases Part 1 Accounting by LesseesDocument18 pagesLeases Part 1 Accounting by Lesseesnathaliefayeb.tajaNo ratings yet

- RPGT A Comprehensive Guide To Real Property Gains Tax in MalaysiaDocument9 pagesRPGT A Comprehensive Guide To Real Property Gains Tax in Malaysiahekate.yantraNo ratings yet

- GST Amdts Part 2Document5 pagesGST Amdts Part 2amankhurana0910No ratings yet

- 16 Republic Vs GMCC United Development CorpDocument2 pages16 Republic Vs GMCC United Development CorpIsh100% (1)

- GRN As: Te ND CR NoDocument2 pagesGRN As: Te ND CR NoEldhoThomasNo ratings yet

- F2 Fin Acc IAS 37 Conor FoleyDocument9 pagesF2 Fin Acc IAS 37 Conor FoleyLove alexchelle ducutNo ratings yet

- ACCT203 LeaseDocument4 pagesACCT203 LeaseSweet Emme100% (1)

- Paper 19 Dec2023 Syllabus2022Document40 pagesPaper 19 Dec2023 Syllabus2022Abhijith ViratNo ratings yet

- Time of Supply of ServicesDocument10 pagesTime of Supply of ServicesShiwang AgrawalNo ratings yet

- 5rd Sessiom - Audit of LeaseDocument21 pages5rd Sessiom - Audit of LeaseRyan Victor Morales100% (1)

- PSAK 71 Instrumen Keuangan 23052021Document102 pagesPSAK 71 Instrumen Keuangan 23052021Marcellindo Brilliant100% (1)

- Tax Planning & Compliance - nd-2021 - Suggested - AnswersDocument10 pagesTax Planning & Compliance - nd-2021 - Suggested - AnswersMohammad Rakibul IslamNo ratings yet

- CA-Intermediate - Income Tax Amendments For May 2024 AttemptDocument17 pagesCA-Intermediate - Income Tax Amendments For May 2024 Attemptwaqtkeebaatein12No ratings yet

- RPT - CollectionDocument3 pagesRPT - CollectionKezNo ratings yet

- TXHKG 2022 Dec ADocument8 pagesTXHKG 2022 Dec AmyheartfallsinnewyorkNo ratings yet

- Finance Act (NO.2) 2009: Prepared byDocument46 pagesFinance Act (NO.2) 2009: Prepared bymehul rakholiyaNo ratings yet

- Tax Ranjan SirDocument111 pagesTax Ranjan SirMd. Anowar MorshedNo ratings yet

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismjaipalmeNo ratings yet

- GST Amendments For CA Inter Nov 2023 by CA Sanchit GroverDocument27 pagesGST Amendments For CA Inter Nov 2023 by CA Sanchit GroverjoyboyishehereNo ratings yet

- Concept of SupplyDocument4 pagesConcept of SupplySamartha UmbareNo ratings yet

- BIR Ruling No. 634-19Document5 pagesBIR Ruling No. 634-19SGNo ratings yet

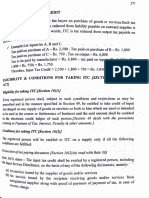

- Itc Eligibility and Conditions + Duration For PaymentDocument5 pagesItc Eligibility and Conditions + Duration For PaymentGOKUL BNo ratings yet

- Types of AssessmentDocument9 pagesTypes of AssessmentRasel AshrafulNo ratings yet

- Roll No. R129216092 SAP ID 500055666: Open Book - Through Blackboard Learning Management SystemDocument6 pagesRoll No. R129216092 SAP ID 500055666: Open Book - Through Blackboard Learning Management SystemSONAL AGARWALNo ratings yet

- Recovery of Tax: (Goods and Services Tax)Document3 pagesRecovery of Tax: (Goods and Services Tax)11priyagargNo ratings yet

- Answers To Taxation Tutorial Questions 02Document3 pagesAnswers To Taxation Tutorial Questions 02habolcorporateNo ratings yet

- Qrmp-Scheme NovDocument2 pagesQrmp-Scheme NovVishwanath HollaNo ratings yet

- Recovery of Tax: (Goods and Services Tax)Document3 pagesRecovery of Tax: (Goods and Services Tax)sridharanNo ratings yet

- Cgtmse - 17 01 2023-41-50Document10 pagesCgtmse - 17 01 2023-41-50kamaiiiNo ratings yet

- PDF Chapter 9 Audit of Liabilities Roque CompressDocument77 pagesPDF Chapter 9 Audit of Liabilities Roque CompressLovely Dela Cruz GanoanNo ratings yet

- Day 6 & 7Document23 pagesDay 6 & 7PrasanthNo ratings yet

- Contract of Service - Construction of Hoist Foundation For M3 (Reviewed)Document12 pagesContract of Service - Construction of Hoist Foundation For M3 (Reviewed)Albert Conrad II LopezNo ratings yet

- GR No. 161397Document7 pagesGR No. 161397woahae13No ratings yet

- ITC Reversal - 180 DaysDocument2 pagesITC Reversal - 180 DaysVijayNo ratings yet

- Interest On SecuritiesDocument25 pagesInterest On SecuritieskhNo ratings yet

- Amortisation of Telecom Licence Fees (SecDocument6 pagesAmortisation of Telecom Licence Fees (SecDipti SahuNo ratings yet

- Final New Indirect Tax Laws Test 3 Detailed May Solution 1617180255Document17 pagesFinal New Indirect Tax Laws Test 3 Detailed May Solution 1617180255CAtestseriesNo ratings yet

- Century Bankers Insurance Corp. vs. LagmanDocument3 pagesCentury Bankers Insurance Corp. vs. LagmanMay Lann LamisNo ratings yet

- Asset For A Period of Time in Exchange For Consideration (IFRS #16)Document6 pagesAsset For A Period of Time in Exchange For Consideration (IFRS #16)Its meh SushiNo ratings yet

- Documentary Stamp Tax (DST) : Don't Watch The Clock. Do What It Does: Keep GoingDocument6 pagesDocumentary Stamp Tax (DST) : Don't Watch The Clock. Do What It Does: Keep GoingRubierosseNo ratings yet

- Merits of GST:: Compensation To Loss Making States For Five Years: It Has Been Proposed That TheDocument10 pagesMerits of GST:: Compensation To Loss Making States For Five Years: It Has Been Proposed That TheJyoti SinghNo ratings yet

- RMC 58-2008 PDFDocument3 pagesRMC 58-2008 PDFChristineNo ratings yet

- LEASESDocument5 pagesLEASESHappy MagdangalNo ratings yet

- TD Water tENDERDocument179 pagesTD Water tENDERSwapnil UpareNo ratings yet

- Tax Remedies of The Taxpayer PDFDocument4 pagesTax Remedies of The Taxpayer PDFJester LimNo ratings yet

- Adobe Scan Feb 21, 2024Document3 pagesAdobe Scan Feb 21, 2024Nidhi LanjewarNo ratings yet

- 21 Allied Banking Corp. v. Quezon City20180322-1159-1qhqio3Document4 pages21 Allied Banking Corp. v. Quezon City20180322-1159-1qhqio3Sheena MarieNo ratings yet

- Philippine Banking Vs CIRDocument7 pagesPhilippine Banking Vs CIRKenmar NoganNo ratings yet

- Tax RemediesDocument12 pagesTax RemediesMei Leen DanielesNo ratings yet

- Prakalathan, A008Document5 pagesPrakalathan, A008Vinayak PuriNo ratings yet

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Comparative Statement - Ingot (Ie07 Grade) - For CST CustomersDocument4 pagesComparative Statement - Ingot (Ie07 Grade) - For CST CustomersSanjayNo ratings yet

- Tachyon Communications PVT LTDDocument1 pageTachyon Communications PVT LTD5647-sumit-11e UpadhyayNo ratings yet

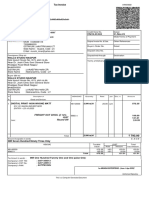

- Invoice: Bernie Allen LTDDocument20 pagesInvoice: Bernie Allen LTDTheMissTehNo ratings yet

- Guoiailon: Hino MetroDocument1 pageGuoiailon: Hino MetrojmNo ratings yet

- Flipkart Labels 09 Mar 2024 03 25Document8 pagesFlipkart Labels 09 Mar 2024 03 25ratiexpressNo ratings yet

- Aman Angel (Indore) GST-46Document1 pageAman Angel (Indore) GST-46Prince KhuranaNo ratings yet

- InvoiceDocument1 pageInvoiceBrian Michel RomanNo ratings yet

- CN 282Document1 pageCN 282f4m0uqb2riNo ratings yet

- Bardwan Hotel BillDocument1 pageBardwan Hotel Billsounak kumarNo ratings yet

- Received With Thanks ' 7,890.00 Through Payment Gateway Over The Internet FromDocument1 pageReceived With Thanks ' 7,890.00 Through Payment Gateway Over The Internet FromPrince DhakaNo ratings yet

- Unit 04 Input Tax CreditDocument20 pagesUnit 04 Input Tax CreditSathya saiNo ratings yet

- Public Finance GSTDocument10 pagesPublic Finance GSTMamta KasodariyaNo ratings yet

- Tax InvoiceDocument1 pageTax InvoiceVitrrag ShahNo ratings yet

- Amazon July Seller InvoiceDocument4 pagesAmazon July Seller InvoiceShoyab ZeonNo ratings yet

- Debit Note PDFDocument3 pagesDebit Note PDFMani ShuklaNo ratings yet

- E-Way Bill 02.07.2021Document1 pageE-Way Bill 02.07.2021sathish pullela8No ratings yet

- Invoice HRPL 139Document1 pageInvoice HRPL 139Sunil PatelNo ratings yet

- cp21 Vat Registration CertificateDocument3 pagescp21 Vat Registration Certificatevtmnewsltd100% (1)

- Cma Final GST Handwritten Notes - 1608648948Document2 pagesCma Final GST Handwritten Notes - 1608648948Padmini SatapathyNo ratings yet

- Quotation For Yogesh SirDocument1 pageQuotation For Yogesh SirSuthar Madan BheraramNo ratings yet

- Sapna Infoway PVT LTD No: 24,2nd Cross, Gandhinagar Bangalore - 560009. PH: 080-4011 4411 GST No: 29AAHCS5435R1ZH InvoiceDocument1 pageSapna Infoway PVT LTD No: 24,2nd Cross, Gandhinagar Bangalore - 560009. PH: 080-4011 4411 GST No: 29AAHCS5435R1ZH InvoiceVijayNo ratings yet

- Flipkart izTDLqDhhUGmP4d9CTVuPGDocument79 pagesFlipkart izTDLqDhhUGmP4d9CTVuPGAI TOOLS FOR BUSINESSNo ratings yet

- Statement 42866198Document1 pageStatement 42866198stkurniasarispd91No ratings yet

- Https Provedaindia - Com Tmpsalesprint - Aspx Id 59382Document1 pageHttps Provedaindia - Com Tmpsalesprint - Aspx Id 59382basudevNo ratings yet

- GRTDefaultDoc 94 QTY BARNALADocument3 pagesGRTDefaultDoc 94 QTY BARNALAWifi Internet Cafe & Multi ServicesNo ratings yet

- AnnapurnaDocument2 pagesAnnapurnaredfashionhubNo ratings yet

- Journal Entry GSTDocument8 pagesJournal Entry GSTSimardeep SalujaNo ratings yet

- MQP Ans 01Document9 pagesMQP Ans 01divyakini12No ratings yet

- Pajak Pertambahan Nilai Terhadap Penyerahan Kendaraan Bermotor Bekas Secara Eceran: Siapa Yang Paling Diunntungkan?Document7 pagesPajak Pertambahan Nilai Terhadap Penyerahan Kendaraan Bermotor Bekas Secara Eceran: Siapa Yang Paling Diunntungkan?PUTRI DIAH ANGGRAININo ratings yet

- Invoice - MR Animesh Aggarwal - 28 Jan 23 - Ded-GoiDocument1 pageInvoice - MR Animesh Aggarwal - 28 Jan 23 - Ded-GoiJatin SalujaNo ratings yet