Download as pptx, pdf, or txt

You might also like

- AssignmentDocument24 pagesAssignmentKwame Tetteh Jnr60% (5)

- Fin242 - Financial Analysis (Group Assignment)Document15 pagesFin242 - Financial Analysis (Group Assignment)Fariq Aizan100% (6)

- Revised Edition Entrepreneurship A Level Revision NotesDocument128 pagesRevised Edition Entrepreneurship A Level Revision NotesDuete Emma85% (48)

- Pallavi Textiles Limited: Presentation by Group 5Document11 pagesPallavi Textiles Limited: Presentation by Group 5Raeesa IssaniNo ratings yet

- Financial Management: ABV-Indian Institute of Information Technology and Management Gwalior (IIITM), GwaliorDocument8 pagesFinancial Management: ABV-Indian Institute of Information Technology and Management Gwalior (IIITM), GwaliorAbhishek ChaurasiaNo ratings yet

- Ramco WordDocument8 pagesRamco WordSomil GuptaNo ratings yet

- Fly Ash Brick Project: Feasibility Study Using CVP AnalysisDocument20 pagesFly Ash Brick Project: Feasibility Study Using CVP Analysissantiago gonzalez0% (1)

- Ross Fundamentals of Corporate Finance 13e CH14Document42 pagesRoss Fundamentals of Corporate Finance 13e CH14aamnaNo ratings yet

- FinalDocument26 pagesFinalHarshit MehtaNo ratings yet

- Chapter-4: AnalysisDocument9 pagesChapter-4: AnalysisBusra HaqueNo ratings yet

- Ratio AnalysisDocument13 pagesRatio AnalysisBharatsinh SarvaiyaNo ratings yet

- CF K C ChandanDocument10 pagesCF K C ChandanChandan K CNo ratings yet

- Assignment ON Corporate Finance (4529202) "Jindal Steel Company" - : Submitted ByDocument13 pagesAssignment ON Corporate Finance (4529202) "Jindal Steel Company" - : Submitted ByhunnyNo ratings yet

- Lecture 3.3Document28 pagesLecture 3.3Classinfo CuNo ratings yet

- Industry-Plastic Pipes Return On Capital Employed 29.15%: PRICE - INR 172.20 NSC - PPL Sector - Plastic ProductsDocument8 pagesIndustry-Plastic Pipes Return On Capital Employed 29.15%: PRICE - INR 172.20 NSC - PPL Sector - Plastic Productssaumya singhNo ratings yet

- FS-AnalysisforDMCI Holdings Inc-ALAWANDocument12 pagesFS-AnalysisforDMCI Holdings Inc-ALAWANNathalia AlawanNo ratings yet

- Analysis and InterpretationDocument5 pagesAnalysis and InterpretationAakankshaNo ratings yet

- FM Cia 3 FinalDocument33 pagesFM Cia 3 FinalRohit GoyalNo ratings yet

- From Cost of Equity To Cost of CapitalDocument21 pagesFrom Cost of Equity To Cost of Capitalsujata dawadiNo ratings yet

- Far 340: Financial Analysis Statement Petronas Gas BerhadDocument26 pagesFar 340: Financial Analysis Statement Petronas Gas BerhadaishahNo ratings yet

- RA Case Study Mock 1Document7 pagesRA Case Study Mock 1dbbNo ratings yet

- 004 - Financial Ratios Part 1 (Lecture)Document32 pages004 - Financial Ratios Part 1 (Lecture)Felix 21No ratings yet

- Great Eastern Shipping Company Limited (Case Study) : Submitted To:-Submitted ByDocument6 pagesGreat Eastern Shipping Company Limited (Case Study) : Submitted To:-Submitted ByAbhishek ChaurasiaNo ratings yet

- Computer Age Management Services LTD (CAMS) : Mittal School of BusinessDocument25 pagesComputer Age Management Services LTD (CAMS) : Mittal School of BusinessVaishnavi KandukuriNo ratings yet

- Submitted To Khuram ShaffiDocument12 pagesSubmitted To Khuram Shaffiharis meerNo ratings yet

- Financial Analysis presentaTIONDocument18 pagesFinancial Analysis presentaTIONRaj MishraNo ratings yet

- Financial Analysis TATA STEElDocument18 pagesFinancial Analysis TATA STEElneha mundraNo ratings yet

- Prestige Institute of Management and ResearchDocument11 pagesPrestige Institute of Management and ResearchVijay SinghNo ratings yet

- Corporate Finance: DLF LTDDocument7 pagesCorporate Finance: DLF LTDvipul tutejaNo ratings yet

- Capital Structure and Firm ValueDocument38 pagesCapital Structure and Firm Valuerkarora1209No ratings yet

- Final Fadm Presentation2Document58 pagesFinal Fadm Presentation2shubbhi27No ratings yet

- DANDOT Annual Report 2022.CdrDocument12 pagesDANDOT Annual Report 2022.CdrayeshamohsinlaptopNo ratings yet

- The Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Document41 pagesThe Basics of Capital Budgeting: Evaluating Cash Flows: Should We Build This Plant?Vaishali GuptaNo ratings yet

- IFE and Financial Ratios Lucky CementDocument19 pagesIFE and Financial Ratios Lucky CementUsman FarooqNo ratings yet

- Fin 302 ReportDocument60 pagesFin 302 ReportMd. Iftekhar RahmanNo ratings yet

- Capital Structure Analysis of Hero Honda, For The Year 2005 To 2010Document8 pagesCapital Structure Analysis of Hero Honda, For The Year 2005 To 2010shrutiNo ratings yet

- An Appraisal of Dividend Policy of Meghna Cement Mills LimitedDocument21 pagesAn Appraisal of Dividend Policy of Meghna Cement Mills LimitedMd. Mesbah Uddin100% (6)

- Financial ManagementDocument3 pagesFinancial Managementhyp siinNo ratings yet

- Chapter 13: Risk, Cost of Capital, and Capital BudgetingDocument35 pagesChapter 13: Risk, Cost of Capital, and Capital BudgetingKoey TseNo ratings yet

- Breadtalk PPT (Chee Jia Lih)Document5 pagesBreadtalk PPT (Chee Jia Lih)Jia LihNo ratings yet

- Debt Management RatiosDocument3 pagesDebt Management RatioslibnganNo ratings yet

- 6611 - Grp6 - Module 2Document25 pages6611 - Grp6 - Module 2Palize QaziNo ratings yet

- Hospital Corporation of AmericaDocument16 pagesHospital Corporation of AmericaDhruv Kalia50% (2)

- Capital Structure Analysis of Hero Honda, For The Year 2005 To 2010Document7 pagesCapital Structure Analysis of Hero Honda, For The Year 2005 To 2010pushpraj rastogiNo ratings yet

- Capital Structure Analysis of Hero HondaDocument7 pagesCapital Structure Analysis of Hero HondaNiklesh ChandakNo ratings yet

- 5 - Cost of Cap UploadDocument4 pages5 - Cost of Cap UploadMayank RanjanNo ratings yet

- Term Paper Assignment PPT FinalDocument26 pagesTerm Paper Assignment PPT FinalUday tejaNo ratings yet

- Value DriversDocument28 pagesValue DriversAbhishek SachdevaNo ratings yet

- Thal LTDDocument8 pagesThal LTDZameer AbbasiNo ratings yet

- Princ 254Document9 pagesPrinc 254RaktimNo ratings yet

- SONA BLW Precision Forgings Ltd. (Sona Comstar) : Q1 FY22 Earnings Conference Call TranscriptDocument24 pagesSONA BLW Precision Forgings Ltd. (Sona Comstar) : Q1 FY22 Earnings Conference Call TranscriptVishal PrasadNo ratings yet

- Previous Business LessonDocument49 pagesPrevious Business LessonsumuzmNo ratings yet

- Cost of Capital and Investment CriteriaDocument9 pagesCost of Capital and Investment Criteriamuhyideen6abdulganiyNo ratings yet

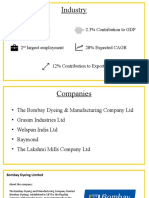

- Industry: Textile Industry 2.3% Contribution To GDPDocument16 pagesIndustry: Textile Industry 2.3% Contribution To GDPNishita VoraNo ratings yet

- FM ReportDocument6 pagesFM ReportKAIF KHANNo ratings yet

- Finance Ratios of ToyotaDocument4 pagesFinance Ratios of ToyotaMaryam KhalidNo ratings yet

- Financial Management Cia3Document9 pagesFinancial Management Cia3Prince ChaudharyNo ratings yet

- Capital Structure Analysis of Hero HondaDocument8 pagesCapital Structure Analysis of Hero HondaHari ShankarNo ratings yet

- Current Ratio: Gloss Paints LTDDocument9 pagesCurrent Ratio: Gloss Paints LTDAmit SharmaNo ratings yet

- Curing Corporate Short-Termism: Future Growth vs. Current EarningsFrom EverandCuring Corporate Short-Termism: Future Growth vs. Current EarningsNo ratings yet

- SSC CGL 2019 Exam Paper - GSDocument126 pagesSSC CGL 2019 Exam Paper - GSRavindra Pratap Singh KalhanshNo ratings yet

- Primitive Accounting Middle Ages Industrial Revolution & Corporate Organization Information AgeDocument28 pagesPrimitive Accounting Middle Ages Industrial Revolution & Corporate Organization Information AgePhil Cahilig-GariginovichNo ratings yet

- OU UG Annual March April 2015 ResultsDocument124 pagesOU UG Annual March April 2015 ResultsMruthyunjayNo ratings yet

- Sonal Project (Transfer of Property Act)Document15 pagesSonal Project (Transfer of Property Act)Handcrafting BeautiesNo ratings yet

- Bir - Train - It & WT - 20180418Document87 pagesBir - Train - It & WT - 20180418Corrine AbucejoNo ratings yet

- Specialized BanksDocument14 pagesSpecialized BankspaescorpisoNo ratings yet

- The Internal Environment SWOT AnalysisDocument3 pagesThe Internal Environment SWOT AnalysisMirta SaparinNo ratings yet

- Development of Agricultural Cooperatives in The Eu - 2014 PDFDocument386 pagesDevelopment of Agricultural Cooperatives in The Eu - 2014 PDFGabriell HaziNo ratings yet

- The Bajaj Group Is Amongst The Top 10 Business Houses in IndiaDocument88 pagesThe Bajaj Group Is Amongst The Top 10 Business Houses in IndiaHardik PurohitNo ratings yet

- Latihan Soal Rekonsiliasi BankDocument1 pageLatihan Soal Rekonsiliasi BankIchsan WibowoNo ratings yet

- Negotiable Instrument CasesDocument12 pagesNegotiable Instrument CasesAyban NabatarNo ratings yet

- Strategic Mamangement Project On Haleeb FoodsDocument83 pagesStrategic Mamangement Project On Haleeb Foodsmuhammad irfan73% (11)

- ECON 105 Syllabus Fall 2011 SyllabusDocument3 pagesECON 105 Syllabus Fall 2011 Syllabusbsaleh8138No ratings yet

- Annual Report 09 10 PDFDocument108 pagesAnnual Report 09 10 PDFSiva KumarNo ratings yet

- Dividend Policy & Capital Structure of Two ConpaniesDocument19 pagesDividend Policy & Capital Structure of Two ConpaniesUtpal Ghosh100% (1)

- Amtrak Case Study Executive SummaryDocument1 pageAmtrak Case Study Executive SummaryNatasha Suddhi0% (2)

- Portfolio Assignment Unit 8Document2 pagesPortfolio Assignment Unit 8Hanna St. JeanNo ratings yet

- DocumentDocument2 pagesDocumentNadella HemanthNo ratings yet

- MFDocument49 pagesMFDeep SekhonNo ratings yet

- Shamo's Resume - Dec 2022Document1 pageShamo's Resume - Dec 2022mt.anarNo ratings yet

- Accounting For State and Local Governmental Units - Proprietary and Fiduciary FundsDocument52 pagesAccounting For State and Local Governmental Units - Proprietary and Fiduciary FundsElizabeth StephanieNo ratings yet

- Lecture Notes 3Document38 pagesLecture Notes 3Jonathan Tran100% (1)

- QuantsDocument436 pagesQuantsShafin Khan100% (1)

- Filinvest Land Vs CA - EdDocument2 pagesFilinvest Land Vs CA - Edida_chua8023No ratings yet

- 10 Funds Flow StatementDocument13 pages10 Funds Flow Statementankush sardanaNo ratings yet

- 200 500 Full Company Update 20230309 PDFDocument19 pages200 500 Full Company Update 20230309 PDFContra Value Bets100% (1)

- BIR RMC 28-2017 Annex ADocument1 pageBIR RMC 28-2017 Annex AAnonymous yKUdPvwjNo ratings yet

- Shri Mahila Griha Udyog Lijjat PapadDocument86 pagesShri Mahila Griha Udyog Lijjat PapadpRiNcE DuDhAtRa60% (5)

- DRAFT First Semester 2023 2024 Examination Timetable NewDocument16 pagesDRAFT First Semester 2023 2024 Examination Timetable NewpalngnenchikaNo ratings yet