Download as pptx, pdf, or txt

You might also like

- UKF Payment Markets Summary 2022Document10 pagesUKF Payment Markets Summary 2022vetemNo ratings yet

- IB Econ SL NotEs Chapter 1Document5 pagesIB Econ SL NotEs Chapter 1John Ryan100% (1)

- Dry Cleaning Home Delivery Business PlanDocument39 pagesDry Cleaning Home Delivery Business PlanDivya AggarwalNo ratings yet

- Certificate of QualityDocument1 pageCertificate of QualityOlivia KurniaNo ratings yet

- CH 1 - Introduction MicroeconomicsDocument45 pagesCH 1 - Introduction MicroeconomicsAchmad TriantoNo ratings yet

- Unit-I EconomicsDocument88 pagesUnit-I EconomicspecmbaNo ratings yet

- Week 01-The Fundamentals of EconomicsDocument33 pagesWeek 01-The Fundamentals of EconomicsPutri WulandariNo ratings yet

- Basic Concepts of EconomicsDocument30 pagesBasic Concepts of EconomicsKashif SaeedNo ratings yet

- 1stweek - Ch01 - What Is EconomicsDocument39 pages1stweek - Ch01 - What Is EconomicsBerkay ÖzayNo ratings yet

- Topic 1: Introduction To Microeconomics: Economic ProblemDocument8 pagesTopic 1: Introduction To Microeconomics: Economic ProblemNadine EudelaNo ratings yet

- Lecture 1Document77 pagesLecture 1SUHANI GHAI 22111549No ratings yet

- Chapter 1: Introduction To Economics: Intended Learning OutcomesDocument9 pagesChapter 1: Introduction To Economics: Intended Learning OutcomesSanuNo ratings yet

- Lecture1. IntroDocument25 pagesLecture1. IntroMochiiiNo ratings yet

- Course Title: Building Economics: Prepared byDocument72 pagesCourse Title: Building Economics: Prepared byNusrat Bintee KhaledNo ratings yet

- ECON1220 (Midterms)Document492 pagesECON1220 (Midterms)meganyaptanNo ratings yet

- Lecture 1 & 2 PresentationDocument39 pagesLecture 1 & 2 Presentationmohamed morraNo ratings yet

- Introduction To MicroeconomicsDocument43 pagesIntroduction To MicroeconomicshassamNo ratings yet

- Microeconomics Notes - Saungweme - Nov2020Document54 pagesMicroeconomics Notes - Saungweme - Nov2020FARAI KABANo ratings yet

- Introduction To Agricultural Economics (AEB 212) : Group: Student Numbers: VENUE: Lecture Theatre 311/003Document46 pagesIntroduction To Agricultural Economics (AEB 212) : Group: Student Numbers: VENUE: Lecture Theatre 311/003Thabo ChuchuNo ratings yet

- The Global Economy by HAZEL MAY CERAFICADocument21 pagesThe Global Economy by HAZEL MAY CERAFICAHazel May CeraficaNo ratings yet

- Chapter 3A Business and EconomicsDocument40 pagesChapter 3A Business and EconomicsRosewin SevandalNo ratings yet

- Market System: Please Listen To The Audio As You Work Through The SlidesDocument31 pagesMarket System: Please Listen To The Audio As You Work Through The SlidesajudgesNo ratings yet

- Lecture 01 - An IntroductionDocument30 pagesLecture 01 - An IntroductionYashika GambhirNo ratings yet

- Economic AnalysisDocument61 pagesEconomic AnalysisMahrukh ChaudharyNo ratings yet

- 1 Prelim Introduction To EconomicsDocument51 pages1 Prelim Introduction To EconomicsLovely Jane MercadoNo ratings yet

- Btech Economics Updated Study Material Till 8th Feb 2022-WedDocument106 pagesBtech Economics Updated Study Material Till 8th Feb 2022-WedJashanpreet SinghNo ratings yet

- Introduction To Economics:: Definition of Economic, Understanding Scarcity, Microeconomics IssueDocument25 pagesIntroduction To Economics:: Definition of Economic, Understanding Scarcity, Microeconomics IssueArvind GiritharagopalanNo ratings yet

- Economics Reviewer 1Document3 pagesEconomics Reviewer 1Lorrianne RosanaNo ratings yet

- CH 01Document5 pagesCH 01Dhaval19101985No ratings yet

- Eco IntroDocument20 pagesEco IntroREHANRAJNo ratings yet

- Module 1 The Study of EconomicsDocument101 pagesModule 1 The Study of EconomicsEdrei Anthony RoblesNo ratings yet

- Ethics of The Environment, Greenwashing and Circular Economy (Lessons 3 4)Document34 pagesEthics of The Environment, Greenwashing and Circular Economy (Lessons 3 4)talha16250No ratings yet

- Chapter 1 Ten Principles of EconomicsDocument29 pagesChapter 1 Ten Principles of EconomicsNika AntelavaNo ratings yet

- Chapter 1 - Introduction To EconomicsDocument51 pagesChapter 1 - Introduction To EconomicsBhavana PrakashNo ratings yet

- Nature of Economics and Basic Economic Concepts - Block-1Document32 pagesNature of Economics and Basic Economic Concepts - Block-1ah523248No ratings yet

- Microeconomics Course: BY Emery Emerimana MBA-Project Management and Finance Email: Tel: 71 578 069/75 658 470Document103 pagesMicroeconomics Course: BY Emery Emerimana MBA-Project Management and Finance Email: Tel: 71 578 069/75 658 470dan dylan terimbereNo ratings yet

- What Is EconomicsDocument38 pagesWhat Is EconomicsFatimah HumayunNo ratings yet

- Ten Principles of Economics (EDIT)Document33 pagesTen Principles of Economics (EDIT)WALEED HAIDERNo ratings yet

- Eco 201 Mod 1 Notes CHDocument8 pagesEco 201 Mod 1 Notes CHJohn Mark TabusoNo ratings yet

- Micro1 Introduction & PrinciplesDocument46 pagesMicro1 Introduction & Principleskshubhanshu02No ratings yet

- Basic Microeconomics Eco101Document59 pagesBasic Microeconomics Eco101Kirk Angelu Victoria AdovasNo ratings yet

- Introduction To EconomicsDocument40 pagesIntroduction To EconomicsIrish DugayonNo ratings yet

- UTS Ekonomi 3 CombinepptDocument10 pagesUTS Ekonomi 3 Combineppttriaa.wulandNo ratings yet

- MICROECONOMICS Lec 1 02102023 101622am 15022024 112624amDocument255 pagesMICROECONOMICS Lec 1 02102023 101622am 15022024 112624amHanzala KhanNo ratings yet

- Introduction To Managerial EconomicsDocument53 pagesIntroduction To Managerial Economicssonarevankar100% (1)

- Day 1 SalesDocument32 pagesDay 1 SalesHanni MaNo ratings yet

- IntroductionDocument15 pagesIntroductiondev.m.dodiyaNo ratings yet

- Economics, Definitions, Economic Problem, Opportunities, Production Possibility ModelDocument27 pagesEconomics, Definitions, Economic Problem, Opportunities, Production Possibility Modelzero point sevenNo ratings yet

- Introduction and Basic Concepts: Instructor: Sajawal AslamDocument13 pagesIntroduction and Basic Concepts: Instructor: Sajawal AslamSajawal AslamNo ratings yet

- Economics For Managers - Notes-3Document23 pagesEconomics For Managers - Notes-3Phillip Gordon MulesNo ratings yet

- Economics Introduction - Unit 1Document62 pagesEconomics Introduction - Unit 1Raja SharmaNo ratings yet

- Micro EconomicsDocument52 pagesMicro EconomicsSaransh BagdiNo ratings yet

- Chapter 1: Managers, Profits, and Markets: Ninth EditionDocument60 pagesChapter 1: Managers, Profits, and Markets: Ninth Editionmoonaafreen100% (1)

- ME Class Day 2Document22 pagesME Class Day 2Harini BaskaranNo ratings yet

- Intro Econ Chapter OneDocument56 pagesIntro Econ Chapter OneReshid JewarNo ratings yet

- Micro - Chapter 1 - The IntroductionDocument43 pagesMicro - Chapter 1 - The IntroductionMaria Christina Ellaiza TalatagodNo ratings yet

- Macroeconomics - Arnold - Chapter 1Document10 pagesMacroeconomics - Arnold - Chapter 1tsam181618No ratings yet

- The Scope and Method of Economics: Dr. Abdul Ghafoor Al SaidiDocument98 pagesThe Scope and Method of Economics: Dr. Abdul Ghafoor Al SaidiADHAM SAFINo ratings yet

- Chapter 01 IntroductionDocument33 pagesChapter 01 IntroductionTanha RupontiNo ratings yet

- Applied Econ Lesson2Document50 pagesApplied Econ Lesson2Vanessa Joy BaluyutNo ratings yet

- MS5030: Data Analysis For Management: Rahul R MaratheDocument39 pagesMS5030: Data Analysis For Management: Rahul R MaratheAgANo ratings yet

- Association Between Random VariablesDocument45 pagesAssociation Between Random VariablesAgANo ratings yet

- 18.price DiscriminationDocument13 pages18.price DiscriminationAgANo ratings yet

- Practice ProblemsDocument14 pagesPractice ProblemsAgANo ratings yet

- This Lecture Covers The Types of Market Such As,, And, in Which Business Firms OperateDocument32 pagesThis Lecture Covers The Types of Market Such As,, And, in Which Business Firms OperateAgANo ratings yet

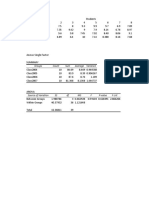

- Groups Count Sum Average VarianceDocument6 pagesGroups Count Sum Average VarianceAgANo ratings yet

- Inferential Statistics: Estimation Hypothesis TestingDocument59 pagesInferential Statistics: Estimation Hypothesis TestingAgANo ratings yet

- 2.foundations of EconomicsDocument10 pages2.foundations of EconomicsAgANo ratings yet

- Comparing Two or More Populations: Anova 1. One-Way ANOVA 2. Two-Way ANOVADocument15 pagesComparing Two or More Populations: Anova 1. One-Way ANOVA 2. Two-Way ANOVAAgANo ratings yet

- 9.the Cost of ProductionnewDocument25 pages9.the Cost of ProductionnewAgANo ratings yet

- Microeconomics Detailed SyllabusDocument3 pagesMicroeconomics Detailed SyllabusAgANo ratings yet

- MICROECONOMICS ASSIGNMENT Group 15Document7 pagesMICROECONOMICS ASSIGNMENT Group 15AgANo ratings yet

- FA - Quiz1 - Answers - All VersionDocument22 pagesFA - Quiz1 - Answers - All VersionAgANo ratings yet

- All The Data Imported Using Football - TablesDocument15 pagesAll The Data Imported Using Football - TablesAgANo ratings yet

- Duration 2 Hours Max Marks 70Document25 pagesDuration 2 Hours Max Marks 70AgANo ratings yet

- Cash Flow Excercise Questions-Set-2Document2 pagesCash Flow Excercise Questions-Set-2AgANo ratings yet

- From The Following Information, Prepare A Cash Flow StatementDocument2 pagesFrom The Following Information, Prepare A Cash Flow StatementAgANo ratings yet

- Marketing Doctor Symptoms: Market Researcher Initial DiagnosisDocument2 pagesMarketing Doctor Symptoms: Market Researcher Initial DiagnosisAgANo ratings yet

- B M S, I: Ennett S Achine HOP NCDocument18 pagesB M S, I: Ennett S Achine HOP NCAgANo ratings yet

- Accenture Project Report E1Document13 pagesAccenture Project Report E1AgA0% (1)

- Accenture Case StudyDocument12 pagesAccenture Case StudyAgANo ratings yet

- Group - 5 - IkeaDocument17 pagesGroup - 5 - IkeaAgANo ratings yet

- Gowthaman PortfolioData AnswersDocument32 pagesGowthaman PortfolioData AnswersAgANo ratings yet

- Group 3 - Mechanistic - Organic - StructureDocument10 pagesGroup 3 - Mechanistic - Organic - StructureAgANo ratings yet

- Push Vs PullDocument2 pagesPush Vs PullAYAN GHOSHNo ratings yet

- Full Download Strategic Management Text and Cases 6th Edition Dess Test BankDocument35 pagesFull Download Strategic Management Text and Cases 6th Edition Dess Test Bankboninablairvip100% (33)

- (BOC) PickarooDocument19 pages(BOC) PickarooalfhyoNo ratings yet

- Abm Research 2Document171 pagesAbm Research 2Mark Agustin Magbanua BarcebalNo ratings yet

- Brand and Demand:: The Key Principles of Marketing GrowthDocument36 pagesBrand and Demand:: The Key Principles of Marketing Growthzamilur shuvoNo ratings yet

- 12 Ipsas 12 Inventories 1Document19 pages12 Ipsas 12 Inventories 1Hastings KapalaNo ratings yet

- Exercises P Class 1 2022Document5 pagesExercises P Class 1 2022Angel MéndezNo ratings yet

- Navistar Logistics Ltd. Unit1, 10F, Tower A, Hunghom Commercial Centre Tau Wai Road, Hunghom Kowloon, HongkongDocument2 pagesNavistar Logistics Ltd. Unit1, 10F, Tower A, Hunghom Commercial Centre Tau Wai Road, Hunghom Kowloon, HongkongAnand SutharNo ratings yet

- Global Economics 13th Edition Robert Carbaugh Test BankDocument21 pagesGlobal Economics 13th Edition Robert Carbaugh Test Bankcovinoustomrig23vdx100% (36)

- Analyzing The Marketing Environment: Principles of Marketing Philip Kotler, Gary ArmstrongDocument27 pagesAnalyzing The Marketing Environment: Principles of Marketing Philip Kotler, Gary ArmstrongShadman Sakib FahimNo ratings yet

- BCIF - Ver7 Back With SignatureDocument1 pageBCIF - Ver7 Back With SignatureKatrina JarabejoNo ratings yet

- Rogers Sugar IncDocument117 pagesRogers Sugar IncAnukh AvinarshNo ratings yet

- What Programmatic Acquirers Do DifferentlyDocument7 pagesWhat Programmatic Acquirers Do DifferentlyMohammed ShalawyNo ratings yet

- CV For Sales Profile - Amul ShekhawatDocument2 pagesCV For Sales Profile - Amul ShekhawatPeedit admiNo ratings yet

- Advertising MCQDocument14 pagesAdvertising MCQArti Srivastava100% (1)

- Session 1 & 2 Financial Management - Kurnadi GularsoDocument23 pagesSession 1 & 2 Financial Management - Kurnadi GularsoChintya FransiscaNo ratings yet

- Chapter 2 - Standardisation and Food Food LegislationDocument49 pagesChapter 2 - Standardisation and Food Food LegislationLam Thoại NguyễnNo ratings yet

- Outward FDI From South Korea: The Relationship Between National Investment Position and Location ChoiceDocument20 pagesOutward FDI From South Korea: The Relationship Between National Investment Position and Location ChoiceLê Hoàng Thương TínNo ratings yet

- PT Cahaya Xii Akl SMK KartiniDocument40 pagesPT Cahaya Xii Akl SMK Kartiniwahyudi yudiNo ratings yet

- Corporate FinanceDocument42 pagesCorporate FinanceNguyễn Thụy Ngọc HânNo ratings yet

- Import FinalDocument5 pagesImport FinalRaza AliNo ratings yet

- CHAPTER 7 National IncomeDocument8 pagesCHAPTER 7 National IncomeAASHISH MISHRANo ratings yet

- IRCTC Retiring RoomDocument1 pageIRCTC Retiring Roomenjoy enjoy enjoyNo ratings yet

- Revocations Irc 501c3 Determinations 01292021Document40 pagesRevocations Irc 501c3 Determinations 01292021Bertha McGalliard PenceNo ratings yet

- Reorder Point FormulaDocument1 pageReorder Point FormulaMary Rose Manglal-lanNo ratings yet

- NUSATIC (EXHIBITOR MANUAL) JUNY (1) - OptDocument25 pagesNUSATIC (EXHIBITOR MANUAL) JUNY (1) - OptBuck AlanNo ratings yet

- Chapter 6: International Business and TradeDocument3 pagesChapter 6: International Business and Tradegian reyesNo ratings yet