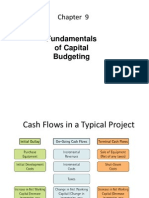

Capital Budgeting Cash Flow

Capital Budgeting Cash Flow

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- BDHCH 9Document37 pagesBDHCH 9tzsyxxwht100% (1)

- Chapter 11Document29 pagesChapter 11Fathan Mubina92% (12)

- Doosan TT Series CNCDocument7 pagesDoosan TT Series CNCRevolusiSoekarnoNo ratings yet

- 2600, 2400, 2300 FOGGERS: User'S ManualDocument2 pages2600, 2400, 2300 FOGGERS: User'S Manualver_at_work100% (1)

- Foundations of Finance: Tenth Edition, Global EditionDocument59 pagesFoundations of Finance: Tenth Edition, Global EditionSemih AYBASTINo ratings yet

- Capital BudgetDocument46 pagesCapital BudgetJohn Rick DayondonNo ratings yet

- Chapter 5 - Developing Project CashflowsDocument33 pagesChapter 5 - Developing Project CashflowsEhsanullah RahmatiNo ratings yet

- CAPITAL BUDGETING Deals With Analyzing The Profitability And/or Liquidity of A Given Project ProposalDocument6 pagesCAPITAL BUDGETING Deals With Analyzing The Profitability And/or Liquidity of A Given Project ProposalVal SarateNo ratings yet

- Hongkong Capital BudgetDocument77 pagesHongkong Capital BudgetZoloft Zithromax ProzacNo ratings yet

- Session 78 - Cashflows of Capital BudgetingDocument32 pagesSession 78 - Cashflows of Capital Budgeting11219203nguyen.nhungNo ratings yet

- 11 Zutter Smart MFBrief 15e ch11Document72 pages11 Zutter Smart MFBrief 15e ch11My videos My videoNo ratings yet

- Capital Budgeting 2022Document7 pagesCapital Budgeting 2022ChrysNo ratings yet

- Cash Flow Statement: 1 Presented by Anita Singhal 1Document25 pagesCash Flow Statement: 1 Presented by Anita Singhal 1anita singhalNo ratings yet

- CHP 11Document45 pagesCHP 11Khaled A. M. El-sherifNo ratings yet

- Capital BudgetingDocument34 pagesCapital BudgetingvijayluckeyNo ratings yet

- CHAPTER FIVE MGT Capital BugdeingDocument18 pagesCHAPTER FIVE MGT Capital Bugdeingnewaybeyene5No ratings yet

- MAhmed 3269 18189 2 Lecture Capital Budgeting and EstimatingDocument12 pagesMAhmed 3269 18189 2 Lecture Capital Budgeting and EstimatingSadia AbidNo ratings yet

- CHAPTER 2 (A) - Analyzing Project Cash FlowsDocument70 pagesCHAPTER 2 (A) - Analyzing Project Cash FlowsSarnisha Murugeshwaran (Shazzisha)No ratings yet

- Lec 1 After Mid TermDocument9 pagesLec 1 After Mid TermsherygafaarNo ratings yet

- Kelompok 2: Capital Budgeting Cash FlowDocument11 pagesKelompok 2: Capital Budgeting Cash FlowBidari DhaifinaNo ratings yet

- Exam 2 SolutionsDocument5 pagesExam 2 Solutions123xxNo ratings yet

- CAPBUDDocument10 pagesCAPBUDVitany Gyn Cabalfin TraifalgarNo ratings yet

- Session 06Document27 pagesSession 06Jaya RoyNo ratings yet

- Financial Management - Cost of Investment & Net Returns: Katrine Celine C. Gutierrez, CPADocument4 pagesFinancial Management - Cost of Investment & Net Returns: Katrine Celine C. Gutierrez, CPAJerichoNo ratings yet

- CHAPTER FIVE FM EdittedDocument26 pagesCHAPTER FIVE FM EdittedGemechis LemaNo ratings yet

- Cap Budgeting-Cash FlowsDocument55 pagesCap Budgeting-Cash FlowsthinkestanNo ratings yet

- Ch20 - Guan CM - AISEDocument38 pagesCh20 - Guan CM - AISEIassa MarcelinaNo ratings yet

- MBS Corporate Finance 2023 Slide Set 3Document104 pagesMBS Corporate Finance 2023 Slide Set 3PGNo ratings yet

- Project Cash FlowsDocument28 pagesProject Cash FlowsNandhini NallasamyNo ratings yet

- Chapters 8 and 9: Capital Budgeting: Ppts To Accompany Fundamentals of Corporate Finance 6E by Ross Et AlDocument42 pagesChapters 8 and 9: Capital Budgeting: Ppts To Accompany Fundamentals of Corporate Finance 6E by Ross Et AlAbel100% (1)

- S7-Capital BudgetingDocument78 pagesS7-Capital BudgetingShaheer BaigNo ratings yet

- Income Based Valuation - l3Document14 pagesIncome Based Valuation - l3Kristene Romarate DaelNo ratings yet

- Lecture 8Document28 pagesLecture 8Hồng LêNo ratings yet

- FINA 5120 - Fall (1) 2022 - Session 4 (With Answers) - Capital Budgeting - 26aug22Document69 pagesFINA 5120 - Fall (1) 2022 - Session 4 (With Answers) - Capital Budgeting - 26aug22Yilin YANGNo ratings yet

- Capital BudgetingDocument3 pagesCapital BudgetingNiña FajardoNo ratings yet

- L2 - Capital BudgetingDocument53 pagesL2 - Capital BudgetingZhenyi ZhuNo ratings yet

- CPALE Syllabus Covere1Document7 pagesCPALE Syllabus Covere1Rian EsperanzaNo ratings yet

- CHAPTER 2-Capital BudgetingDocument13 pagesCHAPTER 2-Capital BudgetingAndualem ZenebeNo ratings yet

- Week 5 - Slides Capital BudgetingDocument44 pagesWeek 5 - Slides Capital BudgetingAmelia MatherNo ratings yet

- Lecture Notes Section 5Document18 pagesLecture Notes Section 5Marc OurfaliNo ratings yet

- AccountingDocument26 pagesAccountingHaris AliNo ratings yet

- Cash Flow EstimationDocument36 pagesCash Flow EstimationVenus Tumbaga100% (1)

- MF 2 Capital Budgeting DecisionsDocument71 pagesMF 2 Capital Budgeting Decisionsarun yadavNo ratings yet

- Toaz - Info Chapter 11 PRDocument45 pagesToaz - Info Chapter 11 PRtaponic390No ratings yet

- Foundations of Finance: Tenth Edition, Global EditionDocument55 pagesFoundations of Finance: Tenth Edition, Global EditionSemih AYBASTINo ratings yet

- CH09 PPT MLDocument127 pagesCH09 PPT MLXianFa WongNo ratings yet

- Lecture 11Document62 pagesLecture 11lilyblooms.atlasNo ratings yet

- Ch11 - Capital Budgeting Cash Flows (G)Document30 pagesCh11 - Capital Budgeting Cash Flows (G)NerissaNo ratings yet

- Capital BudgetingDocument4 pagesCapital Budgetingprincessjaminelizardo9No ratings yet

- Acc 121 - Capital BudgetingDocument7 pagesAcc 121 - Capital BudgetingCin DyNo ratings yet

- AE24 Lesson 6: Analysis of Capital Investment DecisionsDocument17 pagesAE24 Lesson 6: Analysis of Capital Investment DecisionsMajoy BantocNo ratings yet

- Chapter 4Document18 pagesChapter 4Amjad J AliNo ratings yet

- 3 Statement & DCF ModelDocument17 pages3 Statement & DCF ModelarjunNo ratings yet

- Investment Appraisal Taxation, InflationDocument8 pagesInvestment Appraisal Taxation, InflationJiya RajputNo ratings yet

- 3 Statement & DCF ModelDocument17 pages3 Statement & DCF ModelArjun KhoslaNo ratings yet

- Additional Aspects in Capital BudgetingDocument12 pagesAdditional Aspects in Capital BudgetingDebashishNo ratings yet

- Estimation of Project Cash FlowsDocument16 pagesEstimation of Project Cash FlowssanjayttmNo ratings yet

- Capital Budgeting: DefinitionsDocument3 pagesCapital Budgeting: DefinitionsHelen TuberaNo ratings yet

- Caledonia Products FIN370Document8 pagesCaledonia Products FIN370huskergirlNo ratings yet

- Pfm15e Im Ch11Document40 pagesPfm15e Im Ch11vdav hadhNo ratings yet

- Credit TransactionsDocument29 pagesCredit TransactionsGabrielle Louise de Peralta0% (1)

- Bezier Curves For CowardsDocument7 pagesBezier Curves For Cowardsmuldermaster100% (1)

- How To Get Work Items From Workflow in Your Outlook Inbox PDFDocument9 pagesHow To Get Work Items From Workflow in Your Outlook Inbox PDFismailimran09No ratings yet

- R4ADocument23 pagesR4AJamailla MelendrezNo ratings yet

- Exercise On Chapter 8 Science Form 3Document3 pagesExercise On Chapter 8 Science Form 3Sasi RekaNo ratings yet

- Chapter 16Document30 pagesChapter 16Rajashekhar B BeedimaniNo ratings yet

- Prima h4 SBBDocument2 pagesPrima h4 SBBcosty_transNo ratings yet

- A Clinician's Guide To Cost-Effectiveness Analysis: Annals of Internal Medicine. 1990 113:147-154Document8 pagesA Clinician's Guide To Cost-Effectiveness Analysis: Annals of Internal Medicine. 1990 113:147-154dsjervisNo ratings yet

- MBA 111 - ControllingDocument39 pagesMBA 111 - ControllingJhoia BesinNo ratings yet

- Data Sheet SCLFP48100 3U Rev 2Document2 pagesData Sheet SCLFP48100 3U Rev 2hermantoNo ratings yet

- PLAN 423 - Module 3Document35 pagesPLAN 423 - Module 3ABCD EFGNo ratings yet

- HLW8012 User Manual: Work Phone:0755 29650970Document11 pagesHLW8012 User Manual: Work Phone:0755 29650970Abhishek GuptaNo ratings yet

- Boyce ODEch 2 S 1 P 32Document1 pageBoyce ODEch 2 S 1 P 32Charbel KaddoumNo ratings yet

- Optimizing A Battery Energy Storage System For Primary Frequency ControlDocument8 pagesOptimizing A Battery Energy Storage System For Primary Frequency Controlrdj00No ratings yet

- Fisa Technica Fibran20mmDocument6 pagesFisa Technica Fibran20mmFlorin RazvanNo ratings yet

- 03 eLMS Quiz 1Document1 page03 eLMS Quiz 1jaehan834No ratings yet

- 2023 SHRM Model RevisionDocument4 pages2023 SHRM Model RevisionPadmaja NaiduNo ratings yet

- Smart Lighting System Using Raspberry PIDocument9 pagesSmart Lighting System Using Raspberry PIChristosTsilionisNo ratings yet

- Unix BasicsDocument15 pagesUnix BasicsNancyNo ratings yet

- Mini Project Qos Analysis of WiMAxDocument60 pagesMini Project Qos Analysis of WiMAxAbdirihman100% (2)

- FortiSIEM 5.1 Study Guide-OnlineDocument461 pagesFortiSIEM 5.1 Study Guide-OnlineAlma AguilarNo ratings yet

- How To View and Interpret The Turnitin Similarity Score and Originality ReportsDocument5 pagesHow To View and Interpret The Turnitin Similarity Score and Originality ReportsRT LeeNo ratings yet

- Concert: Certified Installer Plus - Enterprise Solutions Partner (Cip-Esp)Document2 pagesConcert: Certified Installer Plus - Enterprise Solutions Partner (Cip-Esp)AndresNo ratings yet

- CSR Business Ethics in IBDocument10 pagesCSR Business Ethics in IBBhavya NagdaNo ratings yet

- Updating Your Device Via Wialon EN PDFDocument16 pagesUpdating Your Device Via Wialon EN PDFДмитрий ДмитриевичNo ratings yet

- SF AERO Skills Map Aircraft Maintenance Track PDFDocument50 pagesSF AERO Skills Map Aircraft Maintenance Track PDFrehannstNo ratings yet

- Optimization of The Setup Position of A Workpiece For Five-Axis Machining To Reduce Machining TimeDocument13 pagesOptimization of The Setup Position of A Workpiece For Five-Axis Machining To Reduce Machining TimeHungTranNo ratings yet

- MT6781 Android ScatterDocument34 pagesMT6781 Android ScatterOliver FischerNo ratings yet

Download as pptx, pdf, or txt

You might also like

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- BDHCH 9Document37 pagesBDHCH 9tzsyxxwht100% (1)

- Chapter 11Document29 pagesChapter 11Fathan Mubina92% (12)

- Doosan TT Series CNCDocument7 pagesDoosan TT Series CNCRevolusiSoekarnoNo ratings yet

- 2600, 2400, 2300 FOGGERS: User'S ManualDocument2 pages2600, 2400, 2300 FOGGERS: User'S Manualver_at_work100% (1)

- Foundations of Finance: Tenth Edition, Global EditionDocument59 pagesFoundations of Finance: Tenth Edition, Global EditionSemih AYBASTINo ratings yet

- Capital BudgetDocument46 pagesCapital BudgetJohn Rick DayondonNo ratings yet

- Chapter 5 - Developing Project CashflowsDocument33 pagesChapter 5 - Developing Project CashflowsEhsanullah RahmatiNo ratings yet

- CAPITAL BUDGETING Deals With Analyzing The Profitability And/or Liquidity of A Given Project ProposalDocument6 pagesCAPITAL BUDGETING Deals With Analyzing The Profitability And/or Liquidity of A Given Project ProposalVal SarateNo ratings yet

- Hongkong Capital BudgetDocument77 pagesHongkong Capital BudgetZoloft Zithromax ProzacNo ratings yet

- Session 78 - Cashflows of Capital BudgetingDocument32 pagesSession 78 - Cashflows of Capital Budgeting11219203nguyen.nhungNo ratings yet

- 11 Zutter Smart MFBrief 15e ch11Document72 pages11 Zutter Smart MFBrief 15e ch11My videos My videoNo ratings yet

- Capital Budgeting 2022Document7 pagesCapital Budgeting 2022ChrysNo ratings yet

- Cash Flow Statement: 1 Presented by Anita Singhal 1Document25 pagesCash Flow Statement: 1 Presented by Anita Singhal 1anita singhalNo ratings yet

- CHP 11Document45 pagesCHP 11Khaled A. M. El-sherifNo ratings yet

- Capital BudgetingDocument34 pagesCapital BudgetingvijayluckeyNo ratings yet

- CHAPTER FIVE MGT Capital BugdeingDocument18 pagesCHAPTER FIVE MGT Capital Bugdeingnewaybeyene5No ratings yet

- MAhmed 3269 18189 2 Lecture Capital Budgeting and EstimatingDocument12 pagesMAhmed 3269 18189 2 Lecture Capital Budgeting and EstimatingSadia AbidNo ratings yet

- CHAPTER 2 (A) - Analyzing Project Cash FlowsDocument70 pagesCHAPTER 2 (A) - Analyzing Project Cash FlowsSarnisha Murugeshwaran (Shazzisha)No ratings yet

- Lec 1 After Mid TermDocument9 pagesLec 1 After Mid TermsherygafaarNo ratings yet

- Kelompok 2: Capital Budgeting Cash FlowDocument11 pagesKelompok 2: Capital Budgeting Cash FlowBidari DhaifinaNo ratings yet

- Exam 2 SolutionsDocument5 pagesExam 2 Solutions123xxNo ratings yet

- CAPBUDDocument10 pagesCAPBUDVitany Gyn Cabalfin TraifalgarNo ratings yet

- Session 06Document27 pagesSession 06Jaya RoyNo ratings yet

- Financial Management - Cost of Investment & Net Returns: Katrine Celine C. Gutierrez, CPADocument4 pagesFinancial Management - Cost of Investment & Net Returns: Katrine Celine C. Gutierrez, CPAJerichoNo ratings yet

- CHAPTER FIVE FM EdittedDocument26 pagesCHAPTER FIVE FM EdittedGemechis LemaNo ratings yet

- Cap Budgeting-Cash FlowsDocument55 pagesCap Budgeting-Cash FlowsthinkestanNo ratings yet

- Ch20 - Guan CM - AISEDocument38 pagesCh20 - Guan CM - AISEIassa MarcelinaNo ratings yet

- MBS Corporate Finance 2023 Slide Set 3Document104 pagesMBS Corporate Finance 2023 Slide Set 3PGNo ratings yet

- Project Cash FlowsDocument28 pagesProject Cash FlowsNandhini NallasamyNo ratings yet

- Chapters 8 and 9: Capital Budgeting: Ppts To Accompany Fundamentals of Corporate Finance 6E by Ross Et AlDocument42 pagesChapters 8 and 9: Capital Budgeting: Ppts To Accompany Fundamentals of Corporate Finance 6E by Ross Et AlAbel100% (1)

- S7-Capital BudgetingDocument78 pagesS7-Capital BudgetingShaheer BaigNo ratings yet

- Income Based Valuation - l3Document14 pagesIncome Based Valuation - l3Kristene Romarate DaelNo ratings yet

- Lecture 8Document28 pagesLecture 8Hồng LêNo ratings yet

- FINA 5120 - Fall (1) 2022 - Session 4 (With Answers) - Capital Budgeting - 26aug22Document69 pagesFINA 5120 - Fall (1) 2022 - Session 4 (With Answers) - Capital Budgeting - 26aug22Yilin YANGNo ratings yet

- Capital BudgetingDocument3 pagesCapital BudgetingNiña FajardoNo ratings yet

- L2 - Capital BudgetingDocument53 pagesL2 - Capital BudgetingZhenyi ZhuNo ratings yet

- CPALE Syllabus Covere1Document7 pagesCPALE Syllabus Covere1Rian EsperanzaNo ratings yet

- CHAPTER 2-Capital BudgetingDocument13 pagesCHAPTER 2-Capital BudgetingAndualem ZenebeNo ratings yet

- Week 5 - Slides Capital BudgetingDocument44 pagesWeek 5 - Slides Capital BudgetingAmelia MatherNo ratings yet

- Lecture Notes Section 5Document18 pagesLecture Notes Section 5Marc OurfaliNo ratings yet

- AccountingDocument26 pagesAccountingHaris AliNo ratings yet

- Cash Flow EstimationDocument36 pagesCash Flow EstimationVenus Tumbaga100% (1)

- MF 2 Capital Budgeting DecisionsDocument71 pagesMF 2 Capital Budgeting Decisionsarun yadavNo ratings yet

- Toaz - Info Chapter 11 PRDocument45 pagesToaz - Info Chapter 11 PRtaponic390No ratings yet

- Foundations of Finance: Tenth Edition, Global EditionDocument55 pagesFoundations of Finance: Tenth Edition, Global EditionSemih AYBASTINo ratings yet

- CH09 PPT MLDocument127 pagesCH09 PPT MLXianFa WongNo ratings yet

- Lecture 11Document62 pagesLecture 11lilyblooms.atlasNo ratings yet

- Ch11 - Capital Budgeting Cash Flows (G)Document30 pagesCh11 - Capital Budgeting Cash Flows (G)NerissaNo ratings yet

- Capital BudgetingDocument4 pagesCapital Budgetingprincessjaminelizardo9No ratings yet

- Acc 121 - Capital BudgetingDocument7 pagesAcc 121 - Capital BudgetingCin DyNo ratings yet

- AE24 Lesson 6: Analysis of Capital Investment DecisionsDocument17 pagesAE24 Lesson 6: Analysis of Capital Investment DecisionsMajoy BantocNo ratings yet

- Chapter 4Document18 pagesChapter 4Amjad J AliNo ratings yet

- 3 Statement & DCF ModelDocument17 pages3 Statement & DCF ModelarjunNo ratings yet

- Investment Appraisal Taxation, InflationDocument8 pagesInvestment Appraisal Taxation, InflationJiya RajputNo ratings yet

- 3 Statement & DCF ModelDocument17 pages3 Statement & DCF ModelArjun KhoslaNo ratings yet

- Additional Aspects in Capital BudgetingDocument12 pagesAdditional Aspects in Capital BudgetingDebashishNo ratings yet

- Estimation of Project Cash FlowsDocument16 pagesEstimation of Project Cash FlowssanjayttmNo ratings yet

- Capital Budgeting: DefinitionsDocument3 pagesCapital Budgeting: DefinitionsHelen TuberaNo ratings yet

- Caledonia Products FIN370Document8 pagesCaledonia Products FIN370huskergirlNo ratings yet

- Pfm15e Im Ch11Document40 pagesPfm15e Im Ch11vdav hadhNo ratings yet

- Credit TransactionsDocument29 pagesCredit TransactionsGabrielle Louise de Peralta0% (1)

- Bezier Curves For CowardsDocument7 pagesBezier Curves For Cowardsmuldermaster100% (1)

- How To Get Work Items From Workflow in Your Outlook Inbox PDFDocument9 pagesHow To Get Work Items From Workflow in Your Outlook Inbox PDFismailimran09No ratings yet

- R4ADocument23 pagesR4AJamailla MelendrezNo ratings yet

- Exercise On Chapter 8 Science Form 3Document3 pagesExercise On Chapter 8 Science Form 3Sasi RekaNo ratings yet

- Chapter 16Document30 pagesChapter 16Rajashekhar B BeedimaniNo ratings yet

- Prima h4 SBBDocument2 pagesPrima h4 SBBcosty_transNo ratings yet

- A Clinician's Guide To Cost-Effectiveness Analysis: Annals of Internal Medicine. 1990 113:147-154Document8 pagesA Clinician's Guide To Cost-Effectiveness Analysis: Annals of Internal Medicine. 1990 113:147-154dsjervisNo ratings yet

- MBA 111 - ControllingDocument39 pagesMBA 111 - ControllingJhoia BesinNo ratings yet

- Data Sheet SCLFP48100 3U Rev 2Document2 pagesData Sheet SCLFP48100 3U Rev 2hermantoNo ratings yet

- PLAN 423 - Module 3Document35 pagesPLAN 423 - Module 3ABCD EFGNo ratings yet

- HLW8012 User Manual: Work Phone:0755 29650970Document11 pagesHLW8012 User Manual: Work Phone:0755 29650970Abhishek GuptaNo ratings yet

- Boyce ODEch 2 S 1 P 32Document1 pageBoyce ODEch 2 S 1 P 32Charbel KaddoumNo ratings yet

- Optimizing A Battery Energy Storage System For Primary Frequency ControlDocument8 pagesOptimizing A Battery Energy Storage System For Primary Frequency Controlrdj00No ratings yet

- Fisa Technica Fibran20mmDocument6 pagesFisa Technica Fibran20mmFlorin RazvanNo ratings yet

- 03 eLMS Quiz 1Document1 page03 eLMS Quiz 1jaehan834No ratings yet

- 2023 SHRM Model RevisionDocument4 pages2023 SHRM Model RevisionPadmaja NaiduNo ratings yet

- Smart Lighting System Using Raspberry PIDocument9 pagesSmart Lighting System Using Raspberry PIChristosTsilionisNo ratings yet

- Unix BasicsDocument15 pagesUnix BasicsNancyNo ratings yet

- Mini Project Qos Analysis of WiMAxDocument60 pagesMini Project Qos Analysis of WiMAxAbdirihman100% (2)

- FortiSIEM 5.1 Study Guide-OnlineDocument461 pagesFortiSIEM 5.1 Study Guide-OnlineAlma AguilarNo ratings yet

- How To View and Interpret The Turnitin Similarity Score and Originality ReportsDocument5 pagesHow To View and Interpret The Turnitin Similarity Score and Originality ReportsRT LeeNo ratings yet

- Concert: Certified Installer Plus - Enterprise Solutions Partner (Cip-Esp)Document2 pagesConcert: Certified Installer Plus - Enterprise Solutions Partner (Cip-Esp)AndresNo ratings yet

- CSR Business Ethics in IBDocument10 pagesCSR Business Ethics in IBBhavya NagdaNo ratings yet

- Updating Your Device Via Wialon EN PDFDocument16 pagesUpdating Your Device Via Wialon EN PDFДмитрий ДмитриевичNo ratings yet

- SF AERO Skills Map Aircraft Maintenance Track PDFDocument50 pagesSF AERO Skills Map Aircraft Maintenance Track PDFrehannstNo ratings yet

- Optimization of The Setup Position of A Workpiece For Five-Axis Machining To Reduce Machining TimeDocument13 pagesOptimization of The Setup Position of A Workpiece For Five-Axis Machining To Reduce Machining TimeHungTranNo ratings yet

- MT6781 Android ScatterDocument34 pagesMT6781 Android ScatterOliver FischerNo ratings yet